regional daily berjaya corp 0.475 (1.0) 36.8 december 26

TRANSCRIPT

REGIONAL DAILY

December 26, 2012

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT.

MALAYSIA

Malaysia Daybreak | 10 July 2014

▌What’s on the Table…

——————————————————————————————————————————————————————————————————————

Eco World Development Group Bhd - Property mover and shaker

Eco World has made the headlines in recent months due to the group's hugely successful launches and aggressive landbanking. This should not be a surprise given that the company has the best people from the property industry, as well as the biggest ambitions. We cut our FY14 EPS forecast by 55% to factor in no launches from existing projects but retain FY15/16 numbers. Our implied target price (still based on parity with RNAV) rises after revising its RNAV for the surplus value from the new Semenyih landbank. Eco World remains an Add and one of our top sector picks, with the asset injection exercise and landbanking being the key catalysts.

Prestariang - Money makes more money?

We scale back our FY14-16 EPS by 5-6% to factor in the dilution from Prestariang’s recently completed private placement of 44m new shares at RM1.74 apiece, which raised around RM76m cash. In the past year, the stock was trading between 12-19x forward P/E. Our target price is revised to the higher end of its trading range at 19x 2015 P/E, a 20% premium over the 16x sector target (previously at 16x sector target) to reflect potential earnings from this fundraising. We maintain an Add rating. Potential catalysts for the stock include news on potential new projects and strong student numbers for the oil & gas school.

UMW Oil & Gas - Take five? Not for this jack-up

The Southeast Asian jack-up market is so hot that UMW-OG's Naga 5 will be mobilised to Myanmar right after the completion of its current contract in the Philippines this month. The company announced today that it has bagged a US$51.3m spot charter for Naga 5 in Myanmar effective next month. We continue to value the stock at 23.4x CY15 P/E, a 40% premium over our implied target market P/E of 16.7x, but still within the historical P/E range of the oil & gas big caps. We maintain our Add call. The aggressive fleet expansion and early deliveries are potential re-rating catalysts.

Plantations - NBPOL appeals to the suitors

Kulim is reportedly close to selling its 49% stake in London-listed New Britain Palm Oil Ltd (NBPOL) as sources have revealed that FGV, Sime Darby and Wilmar are among the four players that have been shortlisted to acquire the stake. Our analysis has revealed that the acquisition will be earnings enhancing for all three players at £6 per NBPOL share. Wilmar could potentially provide the best synergies for NBPOL’s assets while Sime Darby has the best financial resources to scoop up the assets. However, the acquisition will enhance FGV's earnings the most and could reduce the age profile of its combined estates though it will raise FGV's gearing level to 57%. We maintain our Neutral call on the sector, with First Resources and AALI as our top picks.

▌News of the Day…

——————————————————————————————————————————————————————————————————————

• CIMB exploring a three-way merger with RHB Cap and MBSB?

• UMW Oil & Gas secured US$51.3m (RM162.7m) contract from PTTEP for Naga 5

• MAS & American Airlines will be enhancing their current code-share agreement

• Proton Holdings needs at least a year to turn around

• Prestariang completed private placement of 44m new shares at RM1.74/share

• US Federal Reserve plans to end bond purchases to end in Oct

Sources: CIMB. COMPANY REPORTS

Sources: CIMB. COMPANY REPORTS

Key Metrics

FBMKLCI Index

1,650

1,700

1,750

1,800

1,850

1,900

Jul-13 Sep-13 Nov-13 Jan-14 Mar-14 May-14 Jul-14

———————————————————————————

FBMKLCI

1891.16 -1.49pts -0.08%July Futures Aug Futures

1891 - (-0.05% ) 1889.5 - (1.00% )———————————————————————————

Gainers Losers Unchanged344 495 308

———————————————————————————

Turnover1783.97m shares / RM1987.606m

3m avg volume traded 1757.75m shares

3m avg value traded RM2002.28m———————————————————————————

Regional IndicesFBMKLCI FSSTI JCI SET HSI

1,891 3,275 5,025 1,508 23,176 ————————————————————————————————

Close % chg YTD % chg

FBMKLCI 1,891.16 (0.1) 1.3

FBM100 12,763.31 (0.1) 1.4

FBMSC 18,333.55 (0.2) 16.8

FBMMES 6,748.64 (0.5) 18.9

Dow Jones 16,985.61 0.5 2.5

NASDAQ 4,419.03 0.6 5.8

FSSTI 3,275.46 (0.2) 3.4

FTSE-100 6,718.04 (0.3) (0.5)

SENSEX 25,444.81 (0.5) 20.2

Hang Seng 23,176.07 (1.6) (0.6)

JCI 5,024.71 0.7 17.6

KOSPI 2,000.50 (0.3) (0.5)

Nikkei 225 15,302.65 (0.1) (6.1)

PCOMP 6,903.79 (0.6) 17.2

SET 1,507.92 0.0 16.1

Shanghai 2,038.61 (1.2) (3.7)

Taiwan 9,489.98 (0.4) 10.2————————————————————————————————

Close % chg Vol. (m)

CHINA STATIONERY 0.100 17.6 81.4

SUMATEC 0.310 (3.1) 80.3

MAS 0.225 (2.2) 58.9

BERJAYA CORP 0.475 (1.0) 36.8

MULPHA INTL 0.475 0.0 31.7

PDZ HOLDINGS 0.150 0.0 28.2

KNM GROUP 0.995 0.5 27.0

SONA PETROLEUM 0.500 4.2 25.3————————————————————————————————

Close % chg

US$/Euro 1.3642 0.00

RM/US$ (Spot) 3.1725 (0.03)

RM/US$ (12-mth NDF) 3.2385 (0.15)

OPR (% ) 2.98 (0.67)

BLR (% , CIMB Bank) 6.60 0.00

GOLD ( US$/oz) 1,327.78 (0.00)

WTI crude oil US spot (US$/barrel) 102.29 (1.07)

CPO spot price (RM/tonne) 2,426.00 (1.46)

Market Indices

Top Actives

Economic Statistics

————————————————————————————————————————

Terence WONG CFA T (60) 3 2261 9088 E [email protected]

Daybreak│Malaysia

July 10, 2014

2

Global Economic News…

The US Federal Reserve plans to end bond purchases to end in Oct, winding up a five-year stimulus effort to support the US economy, according to its Jun Federal Open Market Committee (FOMC) meeting minutes.

The FOMC expects it would not begin raising its near-zero benchmark interest rate for "a considerable time" after the asset purchase program ends, the minutes said, "especially if projected inflation continued to run below the Committee's 2 per cent longer-run goal."

Fed officials also expressed concern about investors growing too complacent about the economic outlook and the central bank should be on the lookout for excessive risk-taking. (AFP, Bloomberg)

The package of policy measures the European Central Bank (ECB) announced in Jun will take time to have an effect on the euro zone economy, ECB Executive Board member Peter Praet said.

He added that a protracted period of monetary accommodation may have implications for financial stability: "There are two major risks: first, postponement in bank balance sheet repair; and second, bubbles in asset prices." However, he said concerns that the ECB's new targeted lending program could stoke a housing bubble seemed unwarranted. (Reuters)

European Central Bank (ECB) executive board member Benoit Coeure said the strong euro is being integrated in monetary policy, and that he “doesn’t think the strong euro is the most important issue.” (WSJ)

European Central Bank (ECB) President Mario Draghi said the region needs more-centralized powers to push governments to overhaul their economies. “There is a case for some form of common governance over structural reforms,” he said in a speech. “This is because the outcome of structural reforms, a continuously high level of productivity and competitiveness, is not merely in a country’s own interest. It is in the interest of the union as a whole.” (Bloomberg)

Japan’s M3 money stock added an annual 2.4% yoy to ¥1,187.0tr in Jun (+2.6% yoy in May). (RTT)

China’s producer-price index (PPI) declined 1.1% yoy in Jun (-1.4% yoy in May) while consumer-price index (CPI) increased 2.3% yoy (+2.5% yoy in May). (Bloomberg)

China said it can’t stop intervention in the yuan because economic growth is too weak and capital flows aren’t steady enough to warrant changes. Finance Minister Lou Jiwei said “under the current situation, when the economy hasn’t recovered fully and when cross-border capital flows are not completely normal, we’ll continue” existing practices. (Bloomberg)

India's fiscal situation is worse than it appears, Prime Minister Narendra Modi's government said in an economic report that called for tough measures to shore up public finances and reduce inflation, increasing speculation that Finance Minister Arun Jaitley will announce a higher fiscal deficit target in his maiden budget, which he will present to parliament on 10 Jul. (Reuters)

Daybreak│Malaysia

July 10, 2014

3

India's economy is likely to grow in the range of between 5.4% to 5.9% in 2014-15. This will surpass the below five per cent growth in the GDP over the last two years, the Economic Survey 2014 revealed.

The downside risks to the economy are a poor monsoon, the external environment and poor investment climate, the survey said.

It also highlighted that apart from fiscal consolidation, maintaining a stable external balance and further control of inflation, are priorities for growth revival.

The pre-budget Economic Survey, was tabled in Parliament by Finance Minister, Arun Jaitley. (Bernama)

The Australian Melbourne Institute and Westpac Bank index of consumer sentiment rose a seasonally adjusted 1.9% mom in Jul (+0.2% mom in Jun). (Reuters)

Singapore overtook Bangkok to take the top spot for international visitor spending in the Asia Pacific, MasterCard said, highlighting the city-state's growing prominence as one of the world's "destination cities". (CNA)

Jakarta Governor Joko Widodo, also known as Jokowi, led unofficial tallies for president of Indonesia as opponent Prabowo Subianto declared himself the probable winner, raising the prospect of a contested result.

Jokowi, had 53.3% of the vote to Prabowo’s 46.7% with 99.4% of ballots counted, according to Lingkaran Survei Indonesia, an organization conducting quick counts. Another quick count by Saiful Mujani & Research Consulting had Jokowi at 52.9% and Prabowo at 47.1%, on 99% counted.

Prabowo, however, said other survey agencies showed his team in the lead.

Official results will be announce on 20 Jul. (Bloomberg)

The Thailand University of Thai Chamber of Commerce sees the economy galloping ahead at 4% a month on average in the remaining quarters, thanks to improving consumer confidence and the junta's measures to stimulate investment and spending. (The Nation)

Malaysian Economic News…

The Brunei, Indonesia, Malaysia and the Philippines East Asean Growth Area (BIMP-EAGA) and Malaysia Business Council (BEMBC) is working closely with a biotechnology company to revive Sabah's timber industry. Chairman Datuk Roselan Johar Mohamed said the Council has been working on sustainable forest timber farming of light hardwood timber with BioJadi Technology Sdn Bhd. (Bernama)

The implementation of the Goods and Services Tax (GST) on Apr 1 next year is expected to contribute 0.3% to Malaysia's economic growth with exports expanding 0.5% from the second quarter. Deputy Finance Minister Datuk Ahmad Maslan said the country's export products will also be more competitive, as the Sales and Services Tax (SST) at present on average at about 10%, will be abolished. He also said most of Malaysia's products exported at present are 10% more expensive compared to the 160 countries which have implemented the GST. Meanwhile, Ahmad said the government has created the Price Control and Profiteering Act to avoid economic sabotage when the GST is implemented next year to control any rise in prices. (Bernama)

Daybreak│Malaysia

July 10, 2014

4

Asia-Pacific has again bested itself with five out of the top ten destinations for international travellers hailing from the region, up from four in the previous year, according to the MasterCard Global Destination Cities Index released. Kuala Lumpur, despite a marginally lower projected growth rate of 13.1%, made it to Asia-Pacific's top ten for international visitors by sheer arrival numbers. (Bernama)

The European Union (EU) has launched the EU Business Avenues in South-East Asia, a business support programme which aims to assist small- and medium-sized enterprises (SMEs) from the EU, looking to enter or expand their businesses in the region. During this pilot phase, 120 companies will be selected to take part in three one-week business missions, where they will engage with relevant counterparts in Singapore, Malaysia and Vietnam. Dr Michael Pulch, the EU Ambassador here, said the programme would strengthen the presence of SMEs from the EU in key markets in South-East Asia. (Bernama)

Several agencies under the Rural and Regional Development Ministry, especially the village security and development committees, have been mobilised to help explain the implementation of the Goods and Services Tax (GST) to the people. Its minister Datuk Seri Mohd Shafie Apdal said this was to ensure that the people right down to the grassroots, particularly those in the rural areas, would understand the GST. (Bernama)

All civil servants in Negeri Sembilan, Perak, Terengganu and Kelantan will receive Special Financial Aid of RM500 as preparation for Hari Raya Aidilfitri. In Seremban, Negeri Sembilan Menteri Besar Datuk Seri Mohamad Hasan said the special payment was decided during the state exco meeting. "The state government will follow the financial assistance that Prime Minister Datuk Seri Najib Tun Razak had announced for civil servants. (Bernama)

The priority of the Negeri Sembilan government under the 11th Malaysia Plan (11MP) is still on communication infrastructure development.

Menteri Besar Datuk Seri Mohamad Hasan said infrastructure development such as roads will be the catalyst to the development of Negeri Sembilan.

"When there are new roads, the highways and expressways will be upgraded, including Jalan Kuala Pilah and Jalan Sungai Gadut-Rembau. Mohamad Hasan said under 11MP, the state government would apply for the construction of a highway from KLIA to Port Dickson (25 km). The projects will improve the road network in Negeri Sembilan and complement the new KLIA-Seremban highway (37 km).

"The construction of two new highways for new growth areas in the central corridor (Negeri Sembilan) will also benefit Greater Klang Valley (GKV). Since the Klang Valley is overcrowded, the state government would request that Seremban, Port Dickson and Rembau be included in GKV. "We must have a network of good roads and highways to accommodate future development. The inclusion of Seremban, Port Dickson and Rembau in Greater Klang Valley will bring rapid development to Negeri Sembilan," he added. (Bernama)

Come next year, the Johor Government is expected to table the state environment enactment to hasten the process of studying nature and determining development in the state. State health and environment committee chairman Datuk Ayub Rahmat said the enactment, however, was still under discussion and studies were being carried out by the Johor Department of Environment and Johor Economic Planning Unit. (Bernama)

Daybreak│Malaysia

July 10, 2014

5

Political News…

Deputy Prime Minister Muhyiddin Yassin should mount a leadership challenge against his boss, said former minister Zaid Ibrahim. He said it would be better for Muhyiddin to lock horns with Najib Abdul Razak in a contest instead of attempting to shake the latter by questioning policies and decisions supported in the cabinet.

"Even if he loses, the party will be stronger and better for it. Most probably, there will be no actual contest and the PM will gracefully make way for him to take over in 2017. "That's what we call a 'win-win situation' in this blessed country," he added.

Zaid was responding to Muhyiddin's remarks during a recent speech regarding another racial riot taking place, which invited a barrage of criticism. As for Muhyiddin's sleepless nights, Zaid believes that what is keeping him awake is the fact that Najib is growing stronger by the day.

"At least that's how it looks from where I am sitting, and the deputy is feeling frustrated that his chances of becoming PM are being thwarted bit by bit. "His erstwhile allies in Umno seem to be unbelievably quiet and the PM has been able to deal with these groups well. As you know, our PM is adept at taking care of those within the party who have grouses," he said.

However, Zaid said he was disappointed that the DPM resorted to the May 13 incident to make his point about Najib's weaknesses and failures. "There is nothing to be proud of in May 13 and certainly nothing that warrants reminding people about it constantly." (Malaysiakini)

Corporate News…

Prestariang has just completed the private placement of 44m new shares at RM1.74/share, raising around RM76m and increasing its share base from 440m shares to 484m shares. (BMSB)

Please refer to our note for further details.

UMW Oil & Gas has secured a US$51.3m (RM162.7m) contract from PTTEP for Naga 5. The jack-up will support the client's drilling campaign in the Gulf of Mottama, Myanmar for 250 days effective Aug 2014. (BMSB)

Please refer to our note for further details.

CIMB Group Holdings Bhd is exploring a three-way merger with its rivals RHB Capital Bhd (RHB Cap) and Malaysia Building Society (MBSB) in a move to create the country's largest banking group by assets, sources said. The enlarged banking group, with combined assets of RM614bn as at 31 March, would also end up ranking as the fourth largest in Asean, behind DBS Group, Oversea-Chinese Banking Corp and United Overseas Bank.

Sources said all three parties had yesterday submitted an application to Bank Negara Malaysia to begin talks on "how to create value from the enlarged combined assets". Approval is expected as soon as today. The boards of the three groups met yesterday. (Financial Daily)

Telekom Malaysia Bhd does not see Puncak Semangat Sdn Bhd, which is set to implement its proposed digital terrestrial television (DTT) broadcast service next year, as competition to its Internet Protocol television arm, HyppTV. "It is not competition because all our free-to-air channels are also offered free to our subscribers (via UniFi)", said TM Net Sdn Bhd CEO and vice-president of new media, Jeremy Kung. (The Edge)

Daybreak│Malaysia

July 10, 2014

6

Malaysian Airline System Bhd (MAS) and American Airlines will be enhancing their current code-share agreement by adding access to 11 more cities across the US via 260 domestic connecting flights to Los Angeles and New York from 1 August. "[Passengers can now] travel seamlessly on our "MH" code flights on a number of domestic services operated by American Airlines between Los Angeles and New York to major cities like Austin, Dallas, Washington, Orlando, Miami, Chicago, St Louis and more," said MAS group CEO Ahmad Jauhari Yahya. Additionally, MAS will codeshare on American Airlines' services to Dallas from Hong Kong and Seoul from 11 and 24 July respectively. (Financial Daily)

Yinson Holdings Bhd has received an offer from BW Offshore Ltd to either sell down or increase its stake in the Petroleo Nautipa floating production, storage and offloading facility (FPSO), which is currently in Nigerian waters. The company said BW Offshore had proposed to reach a mutual agreement over the eventual 100% ownership of the Petroleo Nautipa FPSO and its owner Tinworth Pte Ltd by either parties.

Tinworth is a 50:50 joint venture between Nautipa AS, a wholly owned subsidiary of Yinson Production, and Prosafe Nautipa AS, a subsidiary of Prosafe Production Public Ltd, which is ultimately held by BW Offshore. It has been proposed that the sale and purchase be in respect of a 100% equity interest in Prosafe Production or 100% equity of Nautipa, as the case may be. Completion will be conditional upon receipt of Yinson’s shareholder approval. (StarBiz)

Proton Holdings Bhd needs at least a year to turn around, with the focus on enhancing the quality of its products, said its chairman Tun Dr Mahathir Mohamad. He said Proton will need to provide more training for its staff and get capital injection so that it can produce cars with uncompromised quality. “It’s going to take some time as it is not easy to turn around a company. There is public perception that Proton manufactures low-quality cars.

To convince people that Proton has improved the quality of its products is not easy. But God willing, we will be able to turn around. “It should take not less than a year. Even one year is not sufficient for Proton to recover completely. There will still be problems but we will improve as we go along,” he said after breaking fast with Proton staff, here, on Tuesday. (BT)

Despite slipping into PN17 category, China Stationery Ltd’s (CSL) share price has reacted positively, as the company escaped from being suspended at the eleventh hour. The stock rose to an intra-day high of 10.5 sen before closing 1.5 sen, or 17.65%, higher than its reference price of 8.5 sen. It is understood that the company is looking to appoint an investment bank to assist with its regularisation plan as soon as next week. (StarBiz)

Daybreak│Malaysia

July 10, 2014

7

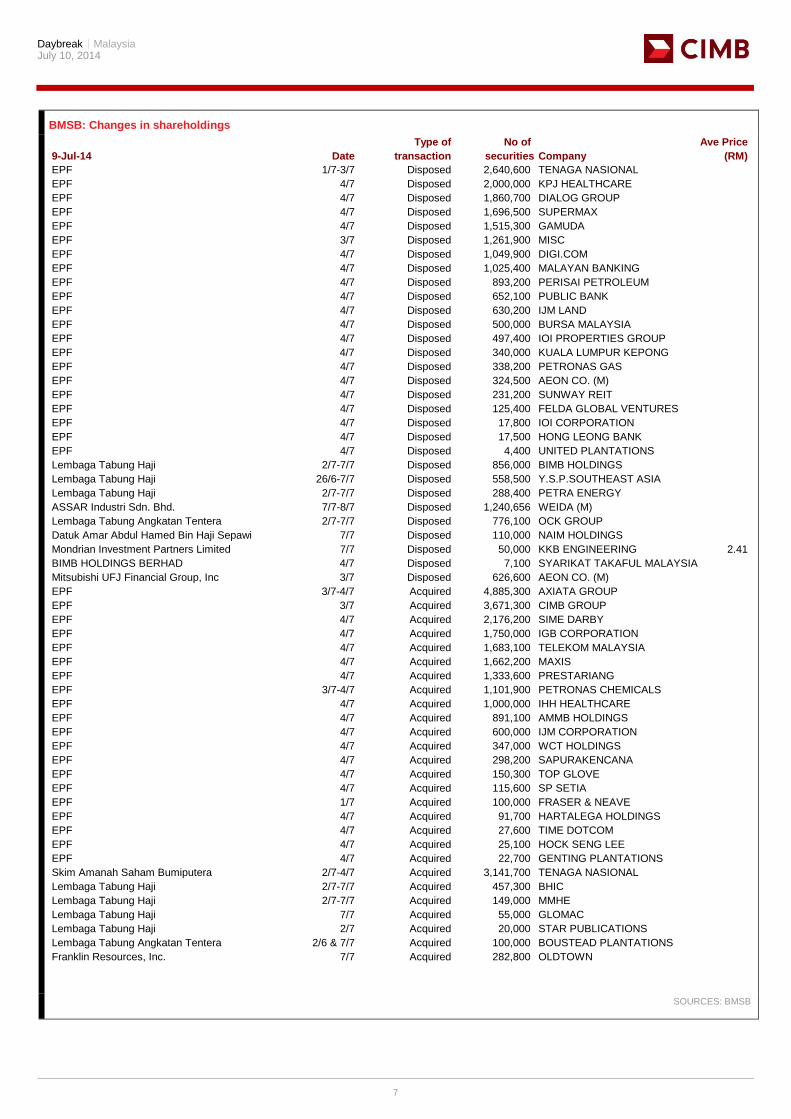

BMSB: Changes in shareholdings

Type of No of Ave Price

9-Jul-14 Date transaction securities Company (RM)

EPF 1/7-3/7 Disposed 2,640,600 TENAGA NASIONAL

EPF 4/7 Disposed 2,000,000 KPJ HEALTHCARE

EPF 4/7 Disposed 1,860,700 DIALOG GROUP

EPF 4/7 Disposed 1,696,500 SUPERMAX

EPF 4/7 Disposed 1,515,300 GAMUDA

EPF 3/7 Disposed 1,261,900 MISC

EPF 4/7 Disposed 1,049,900 DIGI.COM

EPF 4/7 Disposed 1,025,400 MALAYAN BANKING

EPF 4/7 Disposed 893,200 PERISAI PETROLEUM

EPF 4/7 Disposed 652,100 PUBLIC BANK

EPF 4/7 Disposed 630,200 IJM LAND

EPF 4/7 Disposed 500,000 BURSA MALAYSIA

EPF 4/7 Disposed 497,400 IOI PROPERTIES GROUP

EPF 4/7 Disposed 340,000 KUALA LUMPUR KEPONG

EPF 4/7 Disposed 338,200 PETRONAS GAS

EPF 4/7 Disposed 324,500 AEON CO. (M)

EPF 4/7 Disposed 231,200 SUNWAY REIT

EPF 4/7 Disposed 125,400 FELDA GLOBAL VENTURES

EPF 4/7 Disposed 17,800 IOI CORPORATION

EPF 4/7 Disposed 17,500 HONG LEONG BANK

EPF 4/7 Disposed 4,400 UNITED PLANTATIONS

Lembaga Tabung Haji 2/7-7/7 Disposed 856,000 BIMB HOLDINGS

Lembaga Tabung Haji 26/6-7/7 Disposed 558,500 Y.S.P.SOUTHEAST ASIA

Lembaga Tabung Haji 2/7-7/7 Disposed 288,400 PETRA ENERGY

ASSAR Industri Sdn. Bhd. 7/7-8/7 Disposed 1,240,656 WEIDA (M)

Lembaga Tabung Angkatan Tentera 2/7-7/7 Disposed 776,100 OCK GROUP

Datuk Amar Abdul Hamed Bin Haji Sepawi 7/7 Disposed 110,000 NAIM HOLDINGS

Mondrian Investment Partners Limited 7/7 Disposed 50,000 KKB ENGINEERING 2.41

BIMB HOLDINGS BERHAD 4/7 Disposed 7,100 SYARIKAT TAKAFUL MALAYSIA

Mitsubishi UFJ Financial Group, Inc 3/7 Disposed 626,600 AEON CO. (M)

EPF 3/7-4/7 Acquired 4,885,300 AXIATA GROUP

EPF 3/7 Acquired 3,671,300 CIMB GROUP

EPF 4/7 Acquired 2,176,200 SIME DARBY

EPF 4/7 Acquired 1,750,000 IGB CORPORATION

EPF 4/7 Acquired 1,683,100 TELEKOM MALAYSIA

EPF 4/7 Acquired 1,662,200 MAXIS

EPF 4/7 Acquired 1,333,600 PRESTARIANG

EPF 3/7-4/7 Acquired 1,101,900 PETRONAS CHEMICALS

EPF 4/7 Acquired 1,000,000 IHH HEALTHCARE

EPF 4/7 Acquired 891,100 AMMB HOLDINGS

EPF 4/7 Acquired 600,000 IJM CORPORATION

EPF 4/7 Acquired 347,000 WCT HOLDINGS

EPF 4/7 Acquired 298,200 SAPURAKENCANA

EPF 4/7 Acquired 150,300 TOP GLOVE

EPF 4/7 Acquired 115,600 SP SETIA

EPF 1/7 Acquired 100,000 FRASER & NEAVE

EPF 4/7 Acquired 91,700 HARTALEGA HOLDINGS

EPF 4/7 Acquired 27,600 TIME DOTCOM

EPF 4/7 Acquired 25,100 HOCK SENG LEE

EPF 4/7 Acquired 22,700 GENTING PLANTATIONS

Skim Amanah Saham Bumiputera 2/7-4/7 Acquired 3,141,700 TENAGA NASIONAL

Lembaga Tabung Haji 2/7-7/7 Acquired 457,300 BHIC

Lembaga Tabung Haji 2/7-7/7 Acquired 149,000 MMHE

Lembaga Tabung Haji 7/7 Acquired 55,000 GLOMAC

Lembaga Tabung Haji 2/7 Acquired 20,000 STAR PUBLICATIONS

Lembaga Tabung Angkatan Tentera 2/6 & 7/7 Acquired 100,000 BOUSTEAD PLANTATIONS

Franklin Resources, Inc. 7/7 Acquired 282,800 OLDTOWN

SOURCES: BMSB

Daybreak│Malaysia

July 10, 2014

8

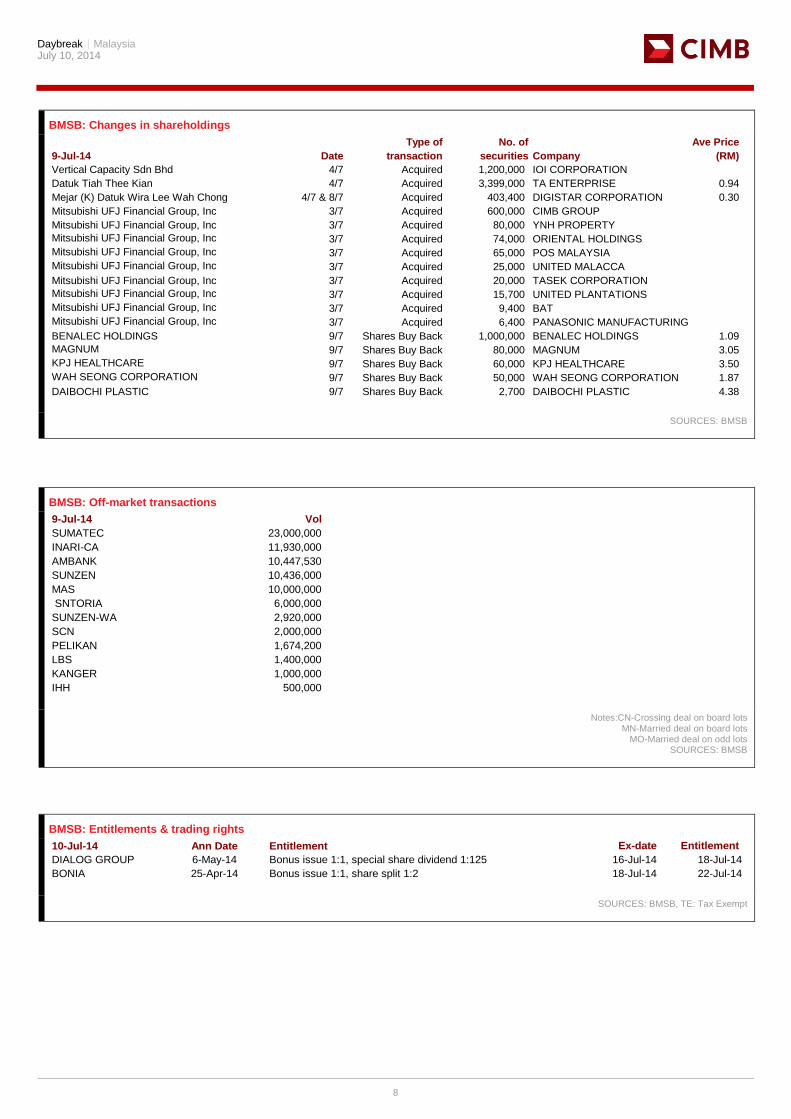

BMSB: Changes in shareholdings

Type of No. of Ave Price

9-Jul-14 Date transaction securities Company (RM)

Vertical Capacity Sdn Bhd 4/7 Acquired 1,200,000 IOI CORPORATION

Datuk Tiah Thee Kian 4/7 Acquired 3,399,000 TA ENTERPRISE 0.94

Mejar (K) Datuk Wira Lee Wah Chong 4/7 & 8/7 Acquired 403,400 DIGISTAR CORPORATION 0.30

Mitsubishi UFJ Financial Group, Inc 3/7 Acquired 600,000 CIMB GROUP

Mitsubishi UFJ Financial Group, Inc 3/7 Acquired 80,000 YNH PROPERTY

Mitsubishi UFJ Financial Group, Inc 3/7 Acquired 74,000 ORIENTAL HOLDINGS

Mitsubishi UFJ Financial Group, Inc 3/7 Acquired 65,000 POS MALAYSIA

Mitsubishi UFJ Financial Group, Inc 3/7 Acquired 25,000 UNITED MALACCA

Mitsubishi UFJ Financial Group, Inc 3/7 Acquired 20,000 TASEK CORPORATION

Mitsubishi UFJ Financial Group, Inc 3/7 Acquired 15,700 UNITED PLANTATIONS

Mitsubishi UFJ Financial Group, Inc 3/7 Acquired 9,400 BAT

Mitsubishi UFJ Financial Group, Inc 3/7 Acquired 6,400 PANASONIC MANUFACTURING

BENALEC HOLDINGS 9/7 Shares Buy Back 1,000,000 BENALEC HOLDINGS 1.09

MAGNUM 9/7 Shares Buy Back 80,000 MAGNUM 3.05

KPJ HEALTHCARE 9/7 Shares Buy Back 60,000 KPJ HEALTHCARE 3.50

WAH SEONG CORPORATION 9/7 Shares Buy Back 50,000 WAH SEONG CORPORATION 1.87

DAIBOCHI PLASTIC 9/7 Shares Buy Back 2,700 DAIBOCHI PLASTIC 4.38

SOURCES: BMSB

BMSB: Off-market transactions

9-Jul-14 Vol

SUMATEC 23,000,000

INARI-CA 11,930,000

AMBANK 10,447,530

SUNZEN 10,436,000

MAS 10,000,000

SNTORIA 6,000,000

SUNZEN-WA 2,920,000

SCN 2,000,000

PELIKAN 1,674,200

LBS 1,400,000

KANGER 1,000,000

IHH 500,000

Notes:CN-Crossing deal on board lots

MN-Married deal on board lots MO-Married deal on odd lots

SOURCES: BMSB

BMSB: Entitlements & trading rights

10-Jul-14 Ann Date Entitlement Ex-date Entitlement

DIALOG GROUP 6-May-14 Bonus issue 1:1, special share dividend 1:125 16-Jul-14 18-Jul-14

BONIA

CORPORATION

25-Apr-14 Bonus issue 1:1, share split 1:2 18-Jul-14 22-Jul-14

SOURCES: BMSB, TE: Tax Exempt

Daybreak│Malaysia

July 10, 2014

9

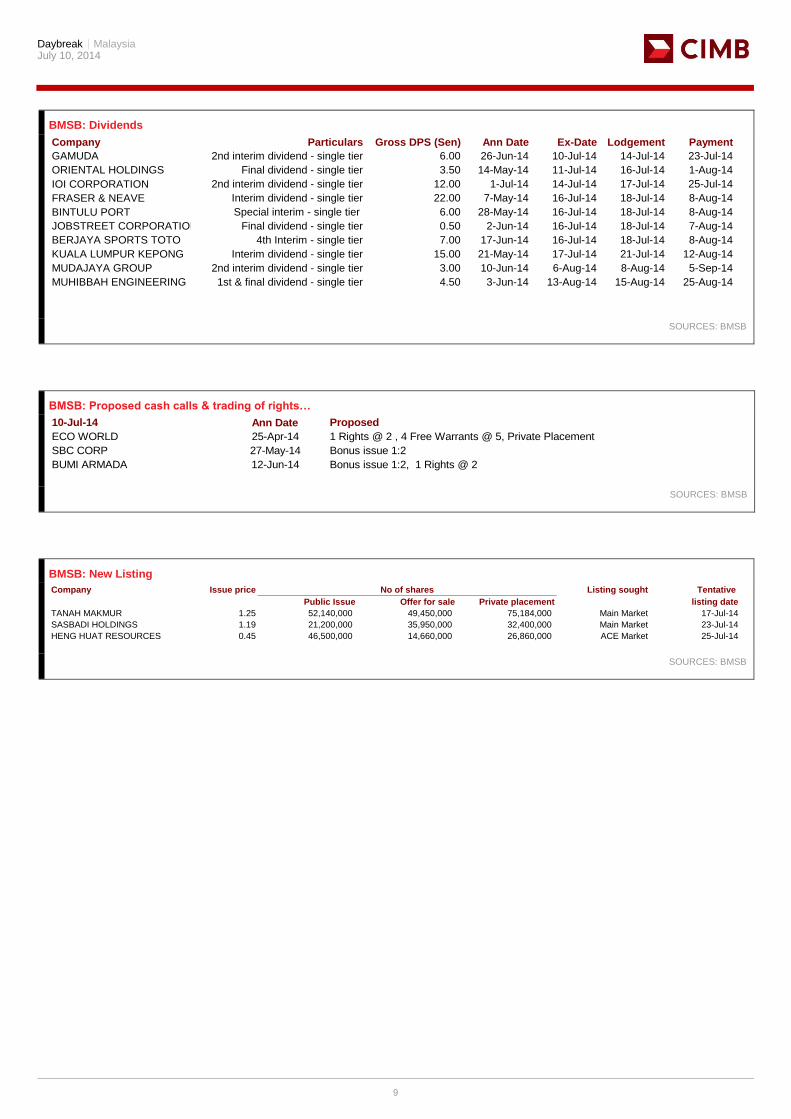

BMSB: Dividends

Company Particulars Gross DPS (Sen) Ann Date Ex-Date Lodgement Payment

GAMUDA 2nd interim dividend - single tier 6.00 26-Jun-14 10-Jul-14 14-Jul-14 23-Jul-14

ORIENTAL HOLDINGS Final dividend - single tier 3.50 14-May-14 11-Jul-14 16-Jul-14 1-Aug-14

IOI CORPORATION 2nd interim dividend - single tier 12.00 1-Jul-14 14-Jul-14 17-Jul-14 25-Jul-14

FRASER & NEAVE Interim dividend - single tier 22.00 7-May-14 16-Jul-14 18-Jul-14 8-Aug-14

BINTULU PORT Special interim - single tier 6.00 28-May-14 16-Jul-14 18-Jul-14 8-Aug-14

JOBSTREET CORPORATION Final dividend - single tier 0.50 2-Jun-14 16-Jul-14 18-Jul-14 7-Aug-14

BERJAYA SPORTS TOTO 4th Interim - single tier 7.00 17-Jun-14 16-Jul-14 18-Jul-14 8-Aug-14

KUALA LUMPUR KEPONG Interim dividend - single tier 15.00 21-May-14 17-Jul-14 21-Jul-14 12-Aug-14

MUDAJAYA GROUP 2nd interim dividend - single tier 3.00 10-Jun-14 6-Aug-14 8-Aug-14 5-Sep-14

MUHIBBAH ENGINEERING 1st & final dividend - single tier 4.50 3-Jun-14 13-Aug-14 15-Aug-14 25-Aug-14

SOURCES: BMSB

BMSB: Proposed cash calls & trading of rights…

10-Jul-14 Ann Date Proposed

ECO WORLD 25-Apr-14 1 Rights @ 2 , 4 Free Warrants @ 5, Private Placement

SBC CORP 27-May-14 Bonus issue 1:2

BUMI ARMADA 12-Jun-14 Bonus issue 1:2, 1 Rights @ 2

SOURCES: BMSB

BMSB: New Listing

Company Issue price Listing sought Tentative

Public Issue Offer for sale Private placement listing date

TANAH MAKMUR 1.25 52,140,000 49,450,000 75,184,000 Main Market 17-Jul-14

SASBADI HOLDINGS 1.19 21,200,000 35,950,000 32,400,000 Main Market 23-Jul-14

HENG HUAT RESOURCES 0.45 46,500,000 14,660,000 26,860,000 ACE Market 25-Jul-14

No of shares

SOURCES: BMSB

Daybreak│Malaysia

July 10, 2014

10

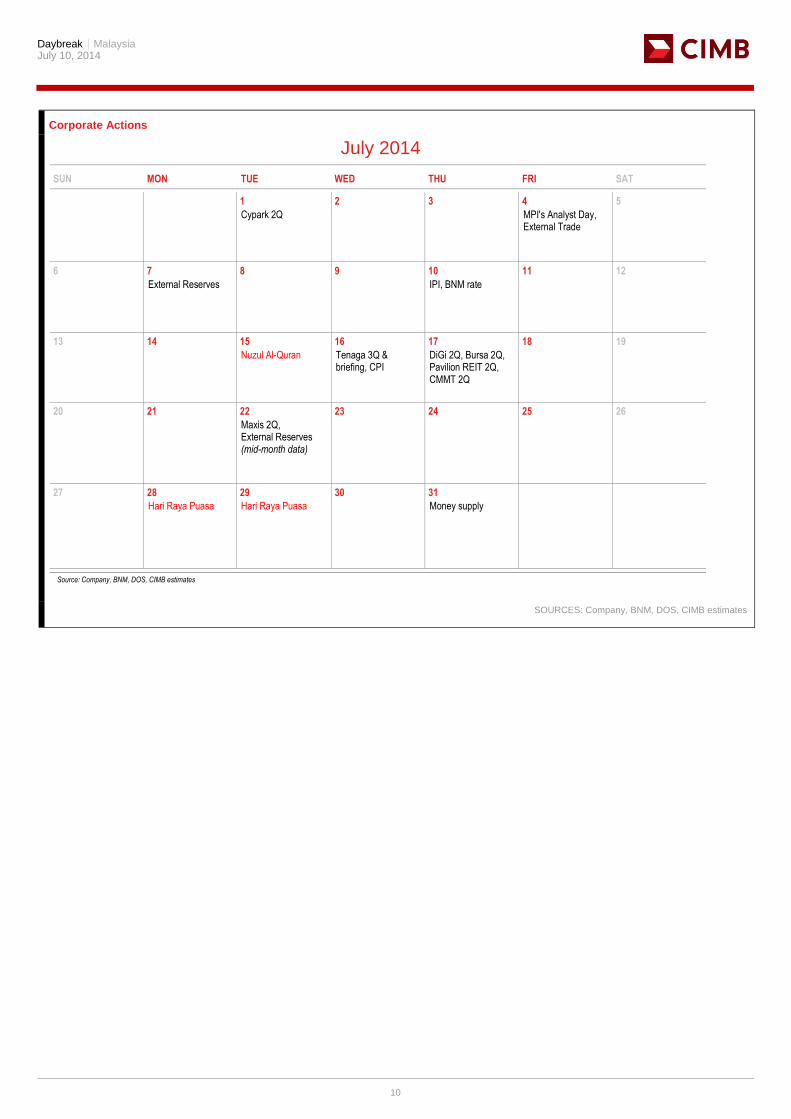

Corporate Actions

July 2014

SUN MON TUE WED THU FRI SAT

1 2 3 4 5

Cypark 2Q MPI's Analyst Day, External Trade

6 7 8 9 10 11 12

External Reserves IPI, BNM rate

13 14 15 16 17 18 19

Nuzul Al-Quran Tenaga 3Q & briefing, CPI

DiGi 2Q, Bursa 2Q, Pavilion REIT 2Q, CMMT 2Q

20 21 22 23 24 25 26

Maxis 2Q, External Reserves (mid-month data)

27 28 29 30 31

Hari Raya Puasa Hari Raya Puasa Money supply

Source: Company, BNM, DOS, CIMB estimates

SOURCES: Company, BNM, DOS, CIMB estimates

Daybreak│Malaysia

July 10, 2014

11

Corporate Actions

August 2014

SUN MON TUE WED THU FRI SAT

31 1 2

National Day

3 4 5 6 7 8 9

External Trade External Reserve (month-end data)

10 11 12 13 14 15 16

IPI GDP, BoP Current Account Balance

17 18 19 20 21 22 23

CPI Eco World 3Q External Reserves (mid-month data)

24 25 26 27 28 29 30

UOA Dev 2Q, E&O 1Q

UEM Sunrise 2Q Mah Sing 2Q, Money supply

Source: Company, BNM, DOS, CIMB estimates

SOURCES: Company, BNM, DOS, CIMB estimates

Daybreak│Malaysia

July 10, 2014

12

DISCLAIMER

This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

By accepting this report, the recipient hereof represents and warrants that he is entitled to receive such report in accordance with the restrictions set forth below and agrees to be bound by the limitations contained herein (including the “Restrictions on Distributions” set out below). Any failure to comply with these limitations may constitute a violation of law. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this report may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB.

Unless otherwise specified, this report is based upon sources which CIMB considers to be reasonable. Such sources will, unless otherwise specified, for market data, be market data and prices available from the main stock exchange or market where the relevant security is listed, or, where appropriate, any other market. Information on the accounts and business of company(ies) will generally be based on published statements of the company(ies), information disseminated by regulatory information services, other publicly available information and information resulting from our research.

Whilst every effort is made to ensure that statements of facts made in this report are accurate, all estimates, projections, forecasts, expressions of opinion and other subjective judgments contained in this report are based on assumptions considered to be reasonable as of the date of the document in which they are contained and must not be construed as a representation that the matters referred to therein will occur. Past performance is not a reliable indicator of future performance. The value of investments may go down as well as up and those investing may, depending on the investments in question, lose more than the initial investment. No report shall constitute an offer or an invitation by or on behalf of CIMB or its affiliates to any person to buy or sell any investments.

CIMB, its affiliates and related companies, their directors, associates, connected parties and/or employees may own or have positions in securities of the company(ies) covered in this research report or any securities related thereto and may from time to time add to or dispose of, or may be materially interested in, any such securities. Further, CIMB, its affiliates and its related companies do and seek to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory, underwriting or placement services for or relating to such company(ies) as well as solicit such investment, advisory or other services from any entity mentioned in this report.

CIMB or its affiliates may enter into an agreement with the company(ies) covered in this report relating to the production of research reports. CIMB may disclose the contents of this report to the company(ies) covered by it and may have amended the contents of this report following such disclosure.

The analyst responsible for the production of this report hereby certifies that the views expressed herein accurately and exclusively reflect his or her personal views and opinions about any and all of the issuers or securities analysed in this report and were prepared independently and autonomously. No part of the compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendations(s) or view(s) in this report. CIMB prohibits the analyst(s) who prepared this research report from receiving any compensation, incentive or bonus based on specific investment banking transactions or for providing a specific recommendation for, or view of, a particular company. Information barriers and other arrangements may be established where necessary to prevent conflicts of interests arising. However, the analyst(s) may receive compensation that is based on his/their coverage of company(ies) in the performance of his/their duties or the performance of his/their recommendations and the research personnel involved in the preparation of this report may also participate in the solicitation of the businesses as described above. In reviewing this research report, an investor should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additional information is, subject to the duties of confidentiality, available on request.

Reports relating to a specific geographical area are produced by the corresponding CIMB entity as listed in the table below. The term “CIMB” shall denote, where appropriate, the relevant entity distributing or disseminating the report in the particular jurisdiction referenced below, or, in every other case, CIMB Group Holdings Berhad ("CIMBGH") and its affiliates, subsidiaries and related companies.

Country CIMB Entity Regulated by

Australia CIMB Securities (Australia) Limited Australian Securities & Investments Commission

Hong Kong CIMB Securities Limited Securities and Futures Commission Hong Kong

Indonesia PT CIMB Securities Indonesia Financial Services Authority of Indonesia

India CIMB Securities (India) Private Limited Securities and Exchange Board of India (SEBI)

Malaysia CIMB Investment Bank Berhad Securities Commission Malaysia

Singapore CIMB Research Pte. Ltd. Monetary Authority of Singapore

South Korea CIMB Securities Limited, Korea Branch Financial Services Commission and Financial Supervisory Service

Taiwan CIMB Securities Limited, Taiwan Branch Financial Supervisory Commission

Thailand CIMB Securities (Thailand) Co. Ltd. Securities and Exchange Commission Thailand

Information in this report is a summary derived from CIMB individual research reports. As such, readers are directed to the CIMB individual research report or note to review the individual Research Analyst's full analysis of the subject company. Important disclosures relating to the companies that are the subject of research reports published by CIMB and the proprietary positions by CIMB and shareholdings of its Research Analysts’ who prepared the report in the securities of the company(s) are available in the individual research report.

The information contained in this research report is prepared from data believed to be correct and reliable at the time of issue of this report. CIMB may or may not issue regular reports on the subject matter of this report at any frequency and may cease to do so or change the periodicity of reports at any time. CIMB is under no obligation to update this report in the event of a material change to the information contained in this report. This report does not purport to contain all the information that a prospective investor may require. CIMB or any of its affiliates does not make any guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information and opinion contained in this report. Neither CIMB nor any of its affiliates nor its related persons shall be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof.

This report is general in nature and has been prepared for information purposes only. It is intended for circulation amongst CIMB and its affiliates’ clients generally and does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. The information and opinions in this report are not and should not be construed or considered as an offer, recommendation or solicitation to buy or sell the subject securities, related investments or other financial instruments thereof.

Investors are advised to make their own independent evaluation of the information contained in this research report, consider their own individual investment objectives, financial situation and particular needs and consult their own professional and financial advisers as to the legal, business, financial, tax and other aspects before participating in any transaction in respect of the securities of company(ies) covered in this research report. The securities of such company(ies) may not be eligible for sale in all jurisdictions or to all categories of investors.

Australia: Despite anything in this report to the contrary, this research is provided in Australia by CIMB Securities (Australia) Limited (“CSAL”) (ABN 84 002 768 701, AFS Licence number 240 530). CSAL is a Market Participant of ASX Ltd, a Clearing Participant of ASX Clear Pty Ltd, a Settlement Participant of ASX Settlement Pty Ltd, and, a participant of Chi X Australia Pty Ltd. This research is only available in Australia to persons who are “wholesale clients” (within the meaning of the Corporations Act 2001 (Cth)) and is supplied solely for the use of such wholesale clients and shall not be distributed or passed on to any other person. This research has been prepared without taking into account the objectives, financial situation or needs of the individual recipient.

France: Only qualified investors within the meaning of French law shall have access to this report. This report shall not be considered as an offer to subscribe to, or used in connection with, any offer for subscription or sale or marketing or direct or indirect distribution of financial instruments and it is not intended as a solicitation for the purchase of any financial instrument.

Hong Kong: This report is issued and distributed in Hong Kong by CIMB Securities Limited (“CHK”) which is licensed in Hong Kong by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 6 (advising on corporate finance) activities. Any investors wishing to purchase or otherwise deal in the securities covered in this report should contact the Head of Sales at CIMB Securities Limited. The views and opinions in this research report are our own as of the date hereof and are subject to

Daybreak│Malaysia

July 10, 2014

13

change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CHK has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CHK. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CHK. Unless permitted to do so by the securities laws of Hong Kong, no person may issue or have in its possession for the purposes of issue, whether in Hong Kong or elsewhere, any advertisement, invitation or document relating to the securities covered in this report, which is directed at, or the contents of which are likely to be accessed or read by, the public in Hong Kong (except if permitted to do so under the securities laws of Hong Kong).

India: This report is issued and distributed in India by CIMB Securities (India) Private Limited (“CIMB India”) which is registered with SEBI as a stock-broker under the Securities and Exchange Board of India (Stock Brokers and Sub-Brokers) Regulations, 1992 and in accordance with the provisions of Regulation 4 (g) of the Securities and Exchange Board of India (Investment Advisers) Regulations, 2013, CIMB India is not required to seek registration with SEBI as an Investment Adviser.

The research analysts, strategists or economists principally responsible for the preparation of this research report are segregated from the other activities of CIMB India and they have received compensation based upon various factors, including quality, accuracy and value of research, firm profitability or revenues, client feedback and competitive factors. Research analysts', strategists' or economists' compensation is not linked to investment banking or capital markets transactions performed or proposed to be performed by CIMB India or its affiliates.

Indonesia: This report is issued and distributed by PT CIMB Securities Indonesia (“CIMBI”). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBI has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMBI. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBI. Neither this report nor any copy hereof may be distributed in Indonesia or to any Indonesian citizens wherever they are domiciled or to Indonesia residents except in compliance with applicable Indonesian capital market laws and regulations.

Malaysia: This report is issued and distributed by CIMB Investment Bank Berhad (“CIMB”). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMB has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMB. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB.

New Zealand: In New Zealand, this report is for distribution only to persons whose principal business is the investment of money or who, in the course of, and for the purposes of their business, habitually invest money pursuant to Section 3(2)(a)(ii) of the Securities Act 1978.

Singapore: This report is issued and distributed by CIMB Research Pte Ltd (“CIMBR”). Recipients of this report are to contact CIMBR in S ingapore in respect of any matters arising from, or in connection with, this report. The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBR has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only. If the recipient of this research report is not an accredited investor, expert investor or institutional investor, CIMBR accepts legal responsibility for the contents of the report without any disclaimer limiting or otherwise curtailing such legal responsibility. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBR.

As of July 9, 2014, CIMBR does not have a proprietary position in the recommended securities in this report.

South Korea: This report is issued and distributed in South Korea by CIMB Securities Limited, Korea Branch ("CIMB Korea") which is licensed as a cash equity broker, and regulated by the Financial Services Commission and Financial Supervisory Service of Korea.

The views and opinions in this research report are our own as of the date hereof and are subject to change, and this report shall not be considered as an offer to subscribe to, or used in connection with, any offer for subscription or sale or marketing or direct or indirect distribution of financial investment instruments and it is not intended as a solicitation for the purchase of any financial investment instrument.

This publication is strictly confidential and is for private circulation only, and no part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB Korea.

Sweden: This report contains only marketing information and has not been approved by the Swedish Financial Supervisory Authority. The distribution of this report is not an offer to sell to any person in Sweden or a solicitation to any person in Sweden to buy any instruments described herein and may not be forwarded to the public in Sweden.

Taiwan: This research report is not an offer or marketing of foreign securities in Taiwan. The securities as referred to in this research report have not been and will not be registered with the Financial Supervisory Commission of the Republic of China pursuant to relevant securities laws and regulations and may not be offered or sold within the Republic of China through a public offering or in circumstances which constitutes an offer within the meaning of the Securities and Exchange Law of the Republic of China that requires a registration or approval of the Financial Supervisory Commission of the Republic of China.

Taiwan: This research report is not an offer or marketing of foreign securities in Taiwan. The securities as referred to in this research report have not been and will not be registered with the Financial Supervisory Commission of the Republic of China pursuant to relevant securities laws and regulations and may not be offered or sold within the Republic of China through a public offering or in circumstances which constitutes an offer or a placement within the meaning of the Securities and Exchange Law of the Republic of China that requires a registration or approval of the Financial Supervisory Commission of the Republic of China.

Thailand: This report is issued and distributed by CIMB Securities (Thailand) Company Limited (CIMBS). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBS has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMBS. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBS.

Corporate Governance Report:

The disclosure of the survey result of the Thai Institute of Directors Association (“IOD”) regarding corporate governance is made pursuant to the policy of the Office of the Securities and Exchange Commission. The survey of the IOD is based on the information of a company listed on the Stock Exchange of Thailand and the Market for Alternative Investment disclosed to the public and able to be accessed by a general public investor. The result, therefore, is from the perspective of a third party. It is not an evaluation of operation and is not based on inside information.

The survey result is as of the date appearing in the Corporate Governance Report of Thai Listed Companies. As a result, the survey result may be changed after that date. CIMBS does not confirm nor certify the accuracy of such survey result.

Score Range 90 – 100 80 – 89 70 – 79 Below 70 or No Survey Result

Description Excellent Very Good Good N/A

United Arab Emirates: The distributor of this report has not been approved or licensed by the UAE Central Bank or any other relevant licensing authorities or governmental agencies in the United Arab Emirates. This report is strictly private and confidential and has not been reviewed by, deposited or registered with UAE Central Bank or any other licensing authority or governmental agencies in the United Arab Emirates. This report is being issued outside the United Arab Emirates to a limited number of institutional investors and must not be provided to any person other than the original recipient and may not be reproduced or used for any other purpose. Further, the information contained in this report is not intended to lead to the

Daybreak│Malaysia

July 10, 2014

14

sale of investments under any subscription agreement or the conclusion of any other contract of whatsoever nature within the territory of the United Arab Emirates.

United Kingdom and Europe: In the United Kingdom and European Economic Area, this report is being disseminated by CIMB Securities (UK) Limited (“CIMB UK”). CIMB UK is authorised and regulated by the Financial Services Authority and its registered office is at 27 Knightsbridge, London, SW1X 7YB. This report is for distribution only to, and is solely directed at, selected persons on the basis that those persons: (a) are persons that are eligible counterparties and professional clients of CIMB UK; (b) have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended, the “Order”); (c) are persons falling within Article 49 (2) (a) to (d) (“high net worth companies, unincorporated associations etc”) of the Order; (d) are outside the United Kingdom; or (e) are persons to whom an invitation or inducement to engage in investment activity (within the meaning of section 21 of the Financial Services and Markets Act 2000) in connection with any investments to which this report relates may otherwise lawfully be communicated or caused to be communicated (all such persons together being referred to as “relevant persons”). This report is directed only at relevant persons and must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this report relates is available only to relevant persons and will be engaged in only with relevant persons.

Only where this report is labelled as non-independent, it does not provide an impartial or objective assessment of the subject matter and does not constitute independent "investment research" under the applicable rules of the Financial Services Authority in the UK. Consequently, any such non-independent report will not have been prepared in accordance with legal requirements designed to promote the independence of investment research and will not subject to any prohibition on dealing ahead of the dissemination of investment research.

United States: This research report is distributed in the United States of America by CIMB Securities (USA) Inc, a U.S.-registered broker-dealer and a related company of

CIMB Research Pte Ltd, CIMB Investment Bank Berhad, PT CIMB Securities Indonesia, CIMB Securities (Thailand) Co. Ltd, CIMB Securities Limited, CIMB Securities

(Australia) Limited, CIMB Securities (India) Private Limited, and is distributed solely to persons who qualify as "U.S. Institutional Investors" as defined in Rule 15a-6 under the

Securities and Exchange Act of 1934. This communication is only for Institutional Investors whose ordinary business activities involve investing in shares, bonds and

associated securities and/or derivative securities and who have professional experience in such investments. Any person who is not a U.S. Institutional Investor or Major

Institutional Investor must not rely on this communication. The delivery of this research report to any person in the United States of America is not a recommendation to

effect any transactions in the securities discussed herein, or an endorsement of any opinion expressed herein. CIMB Securities (USA) Inc, is a FINRA/SIPC member and

takes responsibility for the content of this report. For further information or to place an order in any of the above-mentioned securities please contact a registered

representative of CIMB Securities (USA) Inc.

Other jurisdictions: In any other jurisdictions, except if otherwise restricted by laws or regulations, this report is only for distribution to professional, institutional or sophisticated investors as defined in the laws and regulations of such jurisdictions.

As at the time of publishing this report CIMB is phasing in an absolute recommendation structure for stocks (Framework #1). Please refer to all frameworks for a definition of any recommendations stated in this report.

CIMB Recommendation Framework #1 Stock Ratings Definition Add The stock’s total return is expected to exceed 10% over the next 12 months. Hold The stock’s total return is expected to be between 0% and positive 10% over the next 12 months. Reduce The stock’s total return is expected to fall below 0% or more over the next 12 months. The total expected return of a stock is defined as the sum of the: (i) percentage difference between the target price and the current price and (ii) the forward net dividend yields of the stock. Stock price targets have an investment horizon of 12 months. Sector Ratings Definition Overweight An Overweight rating means stocks in the sector have, on a market cap-weighted basis, a positive absolute recommendation. Neutral A Neutral rating means stocks in the sector have, on a market cap-weighted basis, a neutral absolute recommendation. Underweight An Underweight rating means stocks in the sector have, on a market cap-weighted basis, a negative absolute recommendation. Country Ratings Definition Overweight An Overweight rating means investors should be positioned with an above-market weight in this country relative to benchmark. Neutral A Neutral rating means investors should be positioned with a neutral weight in this country relative to benchmark. Underweight An Underweight rating means investors should be positioned with a below-market weight in this country relative to benchmark.

CIMB Stock Recommendation Framework #2 * Outperform The stock's total return is expected to exceed a relevant benchmark's total return by 5% or more over the next 12 months. Neutral The stock's total return is expected to be within +/-5% of a relevant benchmark's total return. Underperform The stock's total return is expected to be below a relevant benchmark's total return by 5% or more over the next 12 months. Trading Buy The stock's total return is expected to exceed a relevant benchmark's total return by 3% or more over the next 3 months. Trading Sell The stock's total return is expected to be below a relevant benchmark's total return by 3% or more over the next 3 months. * This framework only applies to stocks listed on the Singapore Stock Exchange, Bursa Malaysia, Stock Exchange of Thailand, Jakarta Stock Exchange, Australian Securities Exchange, Taiwan Stock Exchange and National Stock Exchange of India/Bombay Stock Exchange. Occasionally, it is permitted for the total expected returns to be temporarily outside the prescribed ranges due to extreme market volatility or other justifiable company or industry-specific reasons. CIMB Research Pte Ltd (Co. Reg. No. 198701620M)

CIMB Stock Recommendation Framework #3 ** Outperform Expected positive total returns of 10% or more over the next 12 months. Neutral Expected total returns of between -10% and +10% over the next 12 months. Underperform Expected negative total returns of 10% or more over the next 12 months. Trading Buy Expected positive total returns of 10% or more over the next 3 months. Trading Sell Expected negative total returns of 10% or more over the next 3 months. ** This framework only applies to stocks listed on the Korea Exchange, Hong Kong Stock Exchange and China listings on the Singapore Stock Exchange. Occasionally, it is permitted for the total expected returns to be temporarily outside the prescribed ranges due to extreme market volatility or other justifiable company or industry-specific reasons.

Daybreak│Malaysia

July 10, 2014

15

Corporate Governance Report of Thai Listed Companies (CGR). CG Rating by the Thai Institute of Directors Association (IOD) in 2013. AAV – Good, ADVANC - Excellent, AMATA - Very Good, ANAN – Good, AOT - Excellent, AP - Very Good, BANPU - Excellent , BAY - Excellent , BBL - Excellent, BCH – Good, BCP - Excellent, BEC - Very Good, BGH - not available, BJC – Very Good, BH - Very Good, BIGC - Very Good, BTS - Excellent, CCET – Very Good, CENTEL – Very Good, CK - Excellent, CPALL - Very Good, CPF – Excellent, CPN - Excellent, DELTA - Very Good, DTAC - Excellent, EGCO – Excellent, GLOBAL - Good, GLOW - Very Good, GRAMMY – Excellent, HANA - Excellent, HEMRAJ - Excellent, HMPRO - Very Good, INTUCH – Excellent, ITD – Very Good, IVL - Excellent, JAS – Very Good, KAMART – not available, KBANK - Excellent, KKP – Excellent, KTB - Excellent, LH - Very Good, LPN - Excellent, MAJOR – Very Good, MAKRO – Very Good, MCOT - Excellent, MINT - Excellent, PS - Excellent, PSL - Excellent, PTT - Excellent, PTTGC - Excellent, PTTEP - Excellent, QH - Excellent, RATCH - Excellent, ROBINS - Excellent, RS – Excellent, SAMART – Excellent, SC – Excellent, SCB - Excellent, SCC - Excellent, SCCC - Very Good, SIRI – Very Good, SPALI - Excellent, STA - Good, STEC - Very Good, TCAP - Excellent, THAI - Excellent, THCOM – Excellent, TICON – Very Good, TISCO - Excellent, TMB - Excellent, TOP - Excellent, TRUE - Excellent, TTW – Excellent, TUF - Very Good, VGI – Excellent, WORK – Good.