telekom malaysia berhad · 2013-06-28 · - final dividend: 14.25 sen gross or rm382m net of tax...

TRANSCRIPT

TELEKOM MALAYSIA BERHAD

FY 2008 RESULTS

24 February 2009

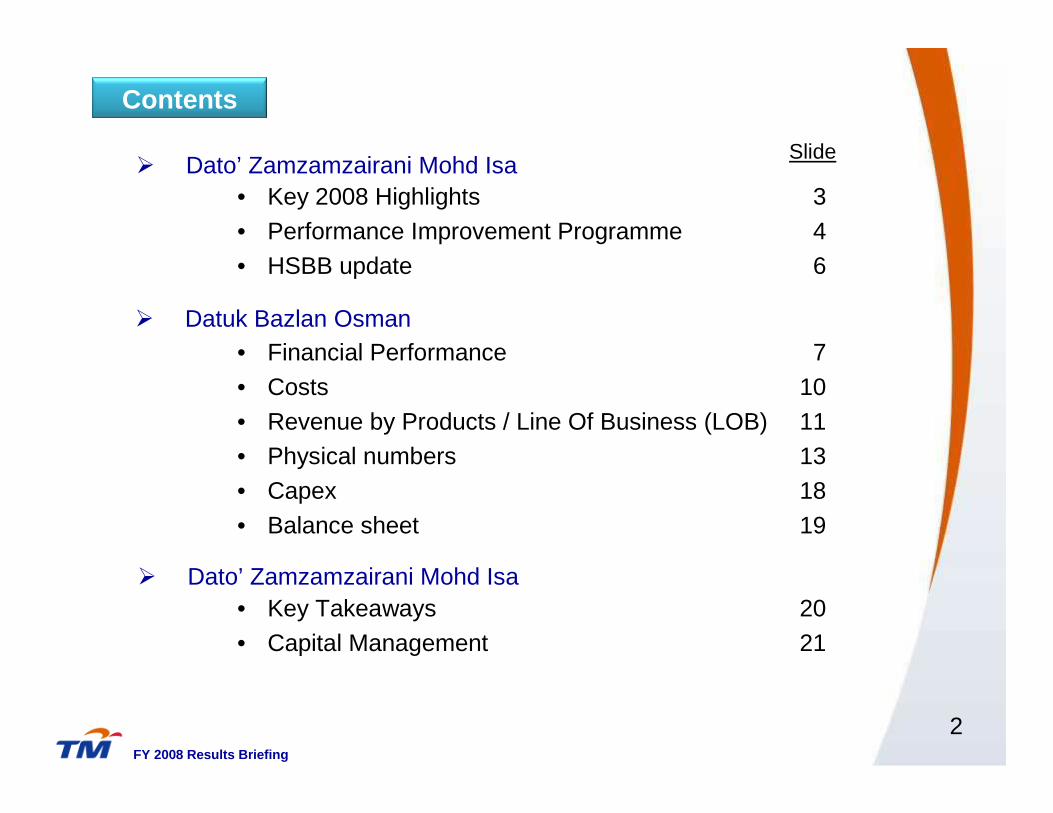

• Key 2008 Highlights 3

• Performance Improvement Programme 4

• HSBB update 6

2FY 2008 Results Briefing

� Dato’ Zamzamzairani Mohd Isa

• Financial Performance 7

• Costs 10

• Revenue by Products / Line Of Business (LOB) 11• Physical numbers 13

• Capex 18

• Balance sheet 19

� Datuk Bazlan Osman

• Key Takeaways 20

• Capital Management 21

� Dato’ Zamzamzairani Mohd Isa

Contents

Slide

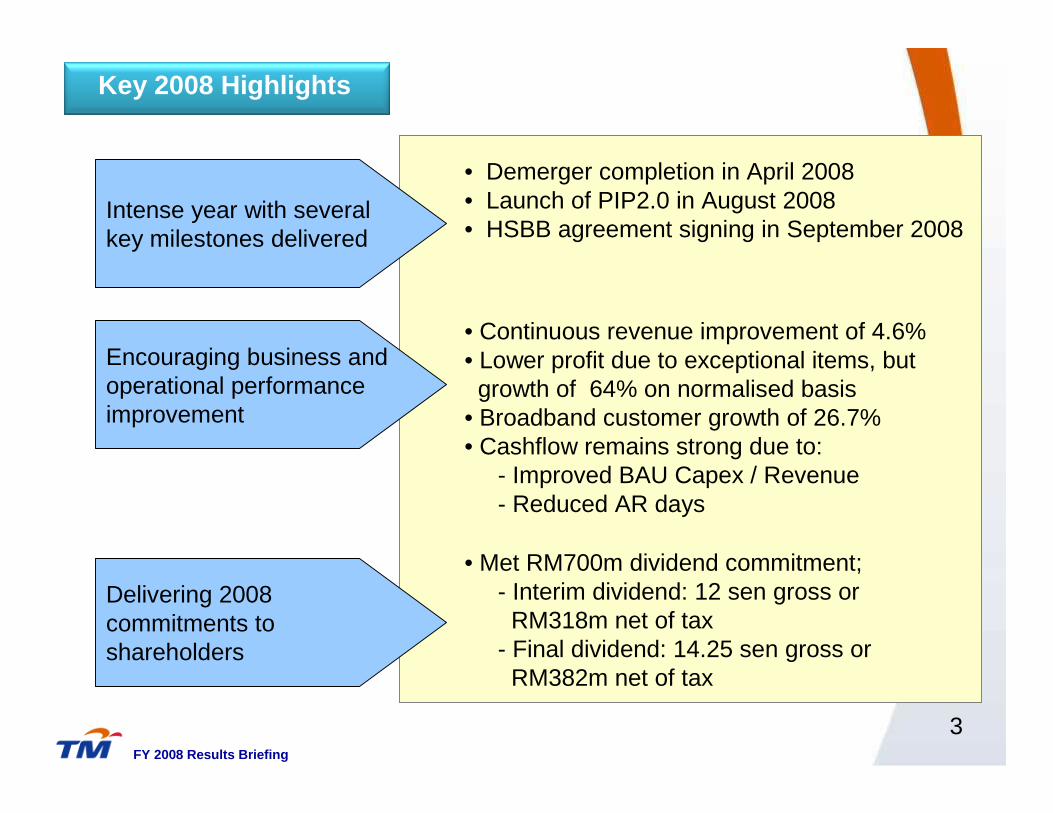

• Demerger completion in April 2008• Launch of PIP2.0 in August 2008• HSBB agreement signing in September 2008

• Met RM700m dividend commitment; - Interim dividend: 12 sen gross or

RM318m net of tax- Final dividend: 14.25 sen gross or

RM382m net of tax

Encouraging business and operational performance improvement

Intense year with several key milestones delivered

Delivering 2008 commitments to shareholders

Key 2008 Highlights

3FY 2008 Results Briefing

• Continuous revenue improvement of 4.6%• Lower profit due to exceptional items, but

growth of 64% on normalised basis• Broadband customer growth of 26.7%• Cashflow remains strong due to:

- Improved BAU Capex / Revenue - Reduced AR days

4FY 2008 Results Briefing

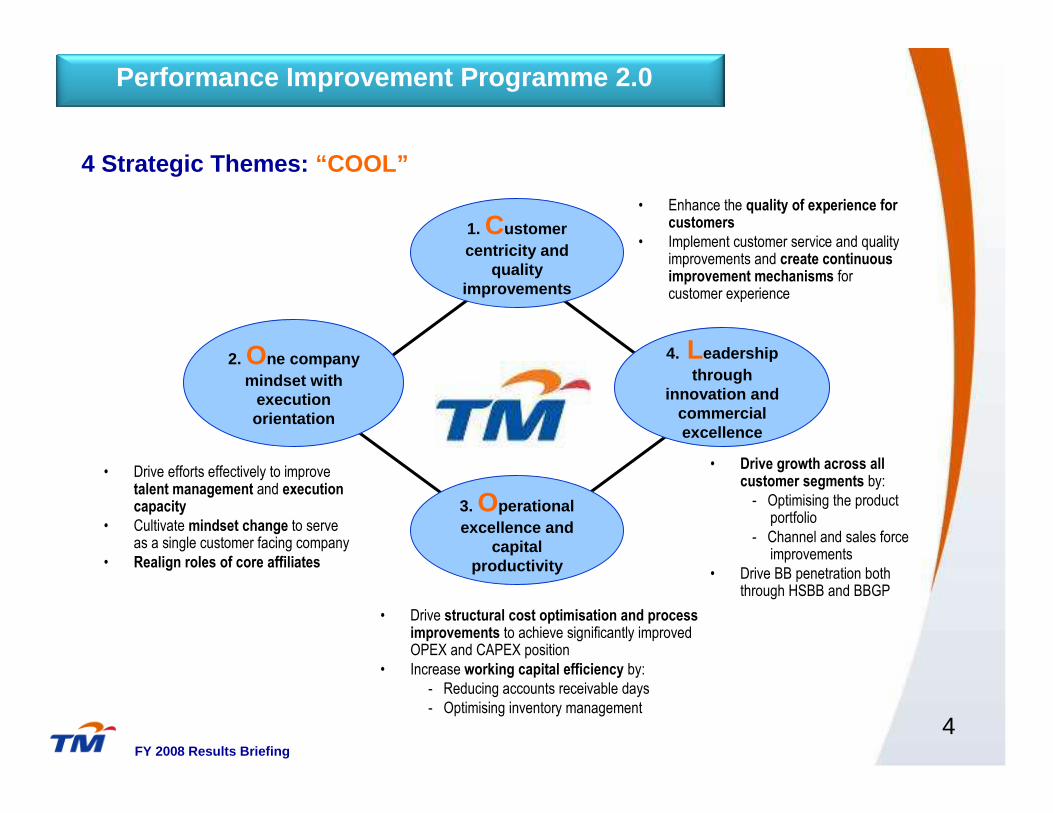

Performance Improvement Programme 2.0

• Enhance the quality of experience for customers

• Implement customer service and quality improvements and create continuous improvement mechanisms for customer experience

• Drive growth across all customer segments by:

- Optimising the product portfolio

- Channel and sales force improvements

• Drive BB penetration both through HSBB and BBGP

• Drive efforts effectively to improve talent management and execution capacity

• Cultivate mindset change to serve as a single customer facing company

• Realign roles of core affiliates

• Drive structural cost optimisation and process improvements to achieve significantly improved OPEX and CAPEX position

• Increase working capital efficiency by:

- Reducing accounts receivable days

- Optimising inventory management

2. One company mindset with

execution orientation

3. Operational excellence and

capital productivity

1. Customer centricity and

quality improvements

4. Leadership through

innovation and commercial excellence

4 Strategic Themes: “COOL”

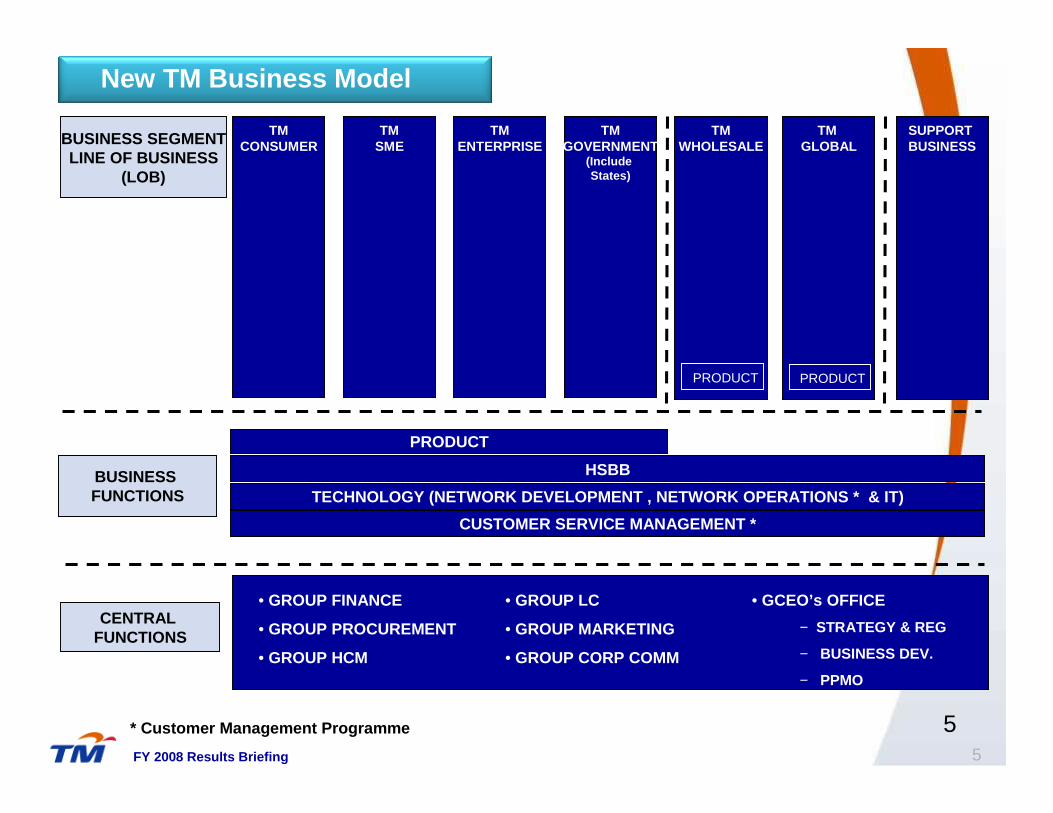

CENTRAL FUNCTIONS

• GROUP FINANCE

• GROUP PROCUREMENT

• GROUP HCM

• GROUP LC

• GROUP MARKETING

• GROUP CORP COMM

• GCEO’s OFFICE

− STRATEGY & REG

− BUSINESS DEV.

− PPMO

TMCONSUMER

TMSME

TMENTERPRISE

TMGOVERNMENT

(Include States)

TMWHOLESALE

TM GLOBALBUSINESS SEGMENT

LINE OF BUSINESS(LOB)

BUSINESS FUNCTIONS

SUPPORT BUSINESS

PRODUCT

HSBB

CUSTOMER SERVICE MANAGEMENT *

TECHNOLOGY (NETWORK DEVELOPMENT , NETWORK OPERATION S * & IT)

* Customer Management Programme

5

PRODUCT PRODUCT

New TM Business Model

FY 2008 Results Briefing

5

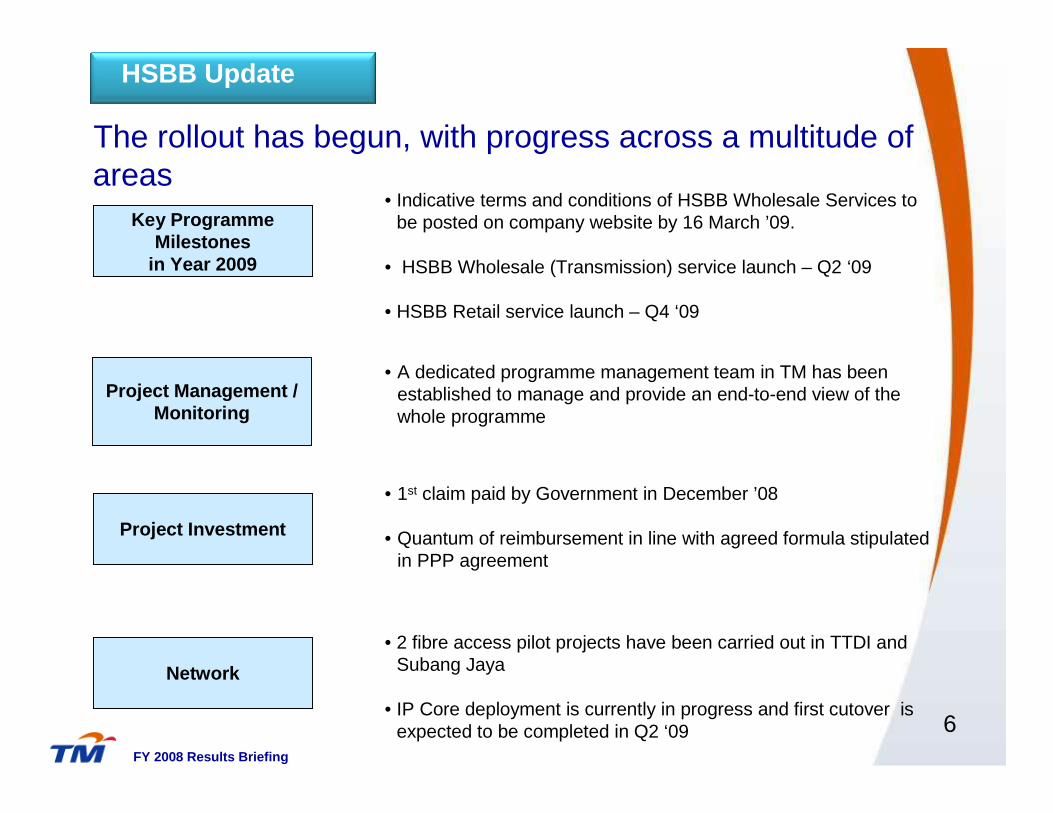

The rollout has begun, with progress across a multitude of areas

Key ProgrammeMilestones

in Year 2009

Project Investment

Network

• Indicative terms and conditions of HSBB Wholesale Services to be posted on company website by 16 March ’09.

• HSBB Wholesale (Transmission) service launch – Q2 ‘09

• HSBB Retail service launch – Q4 ‘09

• 1st claim paid by Government in December ’08

• Quantum of reimbursement in line with agreed formula stipulated in PPP agreement

• 2 fibre access pilot projects have been carried out in TTDI and Subang Jaya

• IP Core deployment is currently in progress and first cutover is expected to be completed in Q2 ‘09

Project Management / Monitoring

• A dedicated programme management team in TM has been established to manage and provide an end-to-end view of the whole programme

HSBB Update

6FY 2008 Results Briefing

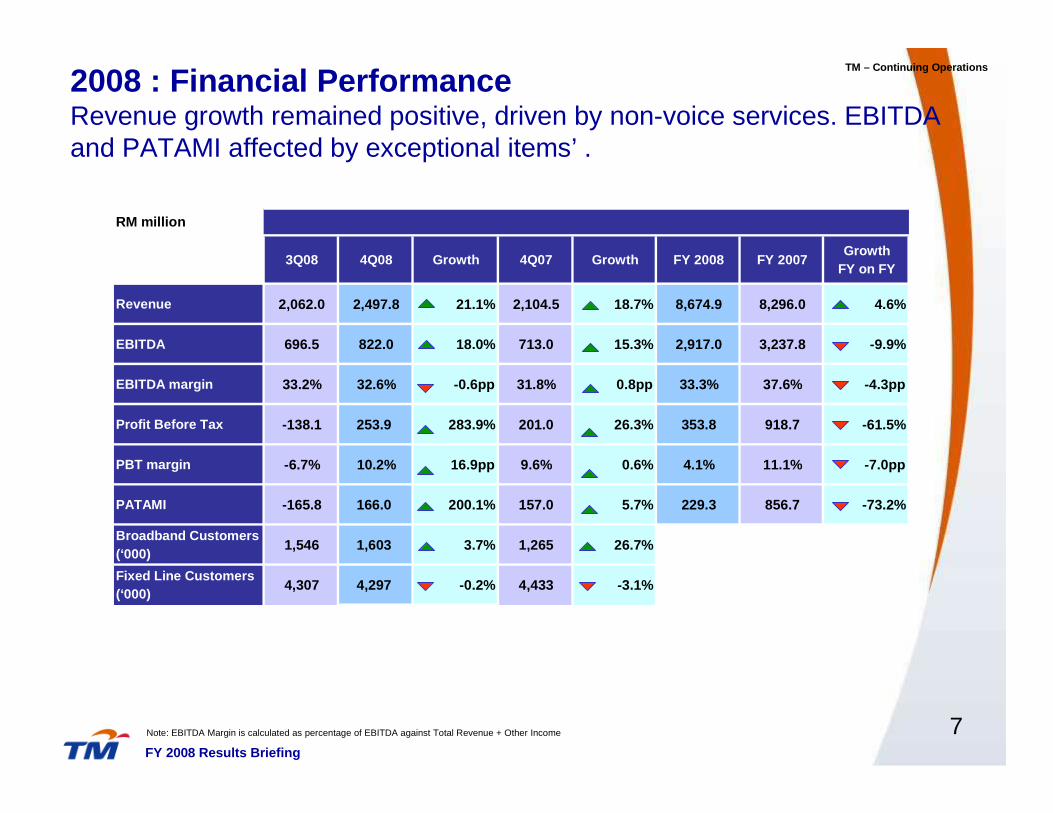

RM million

3Q08 4Q08 Growth 4Q07 Growth FY 2008 FY 2007Growth

FY on FY

Revenue 2,062.0 2,497.8 21.1% 2,104.5 18.7% 8,674.9 8,296.0 4.6%

EBITDA 696.5 822.0 18.0% 713.0 15.3% 2,917.0 3,237.8 -9.9%

EBITDA margin 33.2% 32.6% -0.6pp 31.8% 0.8pp 33.3% 37.6% -4.3pp

Profit Before Tax -138.1 253.9 283.9% 201.0 26.3% 353.8 918.7 -61.5%

PBT margin -6.7% 10.2% 16.9pp 9.6% 0.6% 4.1% 11.1% -7.0pp

PATAMI -165.8 166.0 200.1% 157.0 5.7% 229.3 856.7 -73.2%

Broadband Customers (‘000)

1,546 1,603 3.7% 1,265 26.7%

Fixed Line Customers (‘000)

4,307 4,297 -0.2% 4,433 -3.1%

2008 : Financial Performance Revenue growth remained positive, driven by non-voice services. EBITDA and PATAMI affected by exceptional items’ .

7Note: EBITDA Margin is calculated as percentage of EBITDA against Total Revenue + Other Income

TM – Continuing Operations

FY 2008 Results Briefing

8

TM – Continuing Operations

FY 2008 Results Briefing

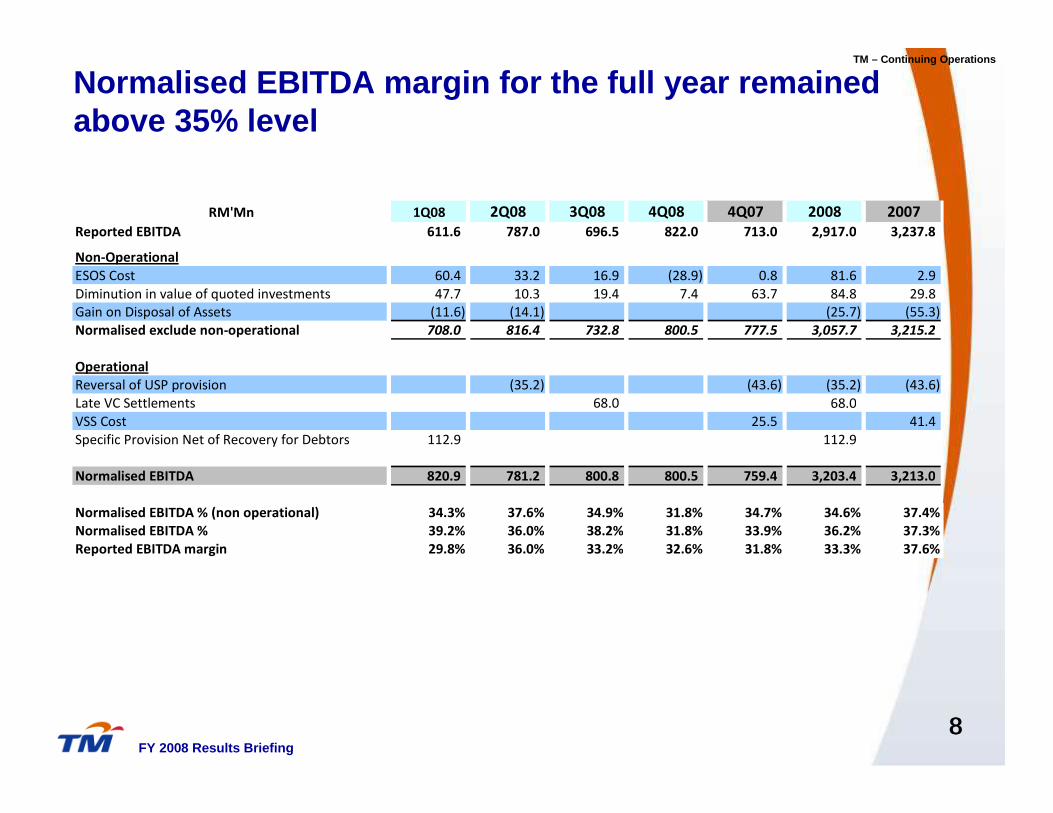

Normalised EBITDA margin for the full year remained above 35% level

8

RM'Mn 1Q08 2Q08 3Q08 4Q08 4Q07 2008 2007

Reported EBITDA 611.6 787.0 696.5 822.0 713.0 2,917.0 3,237.8

Non-Operational

ESOS Cost 60.4 33.2 16.9 (28.9) 0.8 81.6 2.9

Diminution in value of quoted investments 47.7 10.3 19.4 7.4 63.7 84.8 29.8

Gain on Disposal of Assets (11.6) (14.1) (25.7) (55.3)

Normalised exclude non-operational 708.0 816.4 732.8 800.5 777.5 3,057.7 3,215.2

Operational

Reversal of USP provision (35.2) (43.6) (35.2) (43.6)

Late VC Settlements 68.0 68.0

VSS Cost 25.5 41.4

Specific Provision Net of Recovery for Debtors 112.9 112.9

Normalised EBITDA 820.9 781.2 800.8 800.5 759.4 3,203.4 3,213.0

Normalised EBITDA % (non operational) 34.3% 37.6% 34.9% 31.8% 34.7% 34.6% 37.4%

Normalised EBITDA % 39.2% 36.0% 38.2% 31.8% 33.9% 36.2% 37.3%

Reported EBITDA margin 29.8% 36.0% 33.2% 32.6% 31.8% 33.3% 37.6%

9

Normalised PATAMI indicates strong underlying business performance

TM – Continuing Operations

FY 2008 Results Briefing

RM'Mn 1Q08 2Q08 3Q08 4Q08 4Q07 2008 2007

Reported PATAMI 114.4 114.7 (165.8) 166.0 157.0 229.3 856.7

Non-Operational

ESOS Cost 60.4 33.2 16.9 (28.9) 0.8 81.6 2.9

Diminution in value of quoted investments 47.7 10.3 19.4 7.4 63.7 84.8 29.8

FX Loss/(Gain) on Loans (118.8) 74.9 195.7 18.2 (110.1) 170.0 (262.4)

Gain on Disposal of Assets (11.6) (14.1) (25.7) (46.0)

Loss on termination of financial swaps 66.1 15.9 82.0

Deconsolidation of Sotelgui 88.8 88.8

Disposal of TNL Malawi (9.3)

Minority Interest (0.2) (0.1) (0.2) (0.4) (0.9)

Normalised PATAMI 158.0 234.8 154.8 162.4 111.4 709.9 571.7

Operational

Reversal of USP provision (35.2) (43.6) (35.2) (43.6)

Late VC Settlements 68.0 68.0

VSS cost 25.5 41.4

Fixed Assets Written Off/Impairment 16.6 49.8

Specific Provision Net of Recovery for Debtors 112.9 112.9

Prior Year Tax Provision (51.9) (28.7) (28.6) (53.9) (109.2) (192.1)

Impact of Tax (29.4) 9.2 (17.7) 4.9 (37.9) 5.0

Normalised PATAMI 241.5 156.8 176.4 133.8 60.9 708.5 432.2

Costs as a % of Revenue

10

Cost affected by exceptional items

92.6

8,035.4

2,098.9

24.2

1,539.0

17.7

370.9

4.3

196.4

2.3

422.6

4.9

1,527.8

17.6

1,879.9

21.7

8,674.9

FY 2008

93.9

1,936.0

533.6

25.9

318.4

15.4

80.2

3.9

4.1

0.2

89.3

4.3

382.4

18.5

527.0

25.6

2,062.0

3Q 2008

89.2

2,228.4

529.6

21.2

555.4

22.2

92.9

3.7

69.6

2.8

98.2

3.9

337.4

13.5

545.3

21.8

2,497.8

4Q 2008

91.696.8Total (% of Revenue)

7,598.32,037.0Total (RM mil)

2,311.4589.5RM mil.

27.928.0Depreciation & Amortisation %

1,125.6330.1RM mil.

13.615.7Other Operating Costs %

387.6127.2RM mil.

4.76.0Marketing Expenses %

263.845.9RM mil.

3.22.2Bad & Doubtful Debts %

455.2170.4RM mil.

5.58.1Supplies & Materials %

1,420.1355.4RM mil.

17.116.9Manpower %

1,634.6418.4RM mil.

19.719.9Direct Costs %

8,296.0 2,104.5Revenue (RM mil)

FY 20074Q 2007 YoY Review• Higher Other Operating

Costs mainly due to higher maintenance (MERS 999), rental, utilities and diminution in value of quoted investment.

• Manpower cost stable except for special ESOS provision (RM81.6mn)

• Direct cost increased due to higher international and interconnect outpayment(RM158.3mn)

• Depreciation lower mainly due to sale and leaseback of 4 buildings

Note: Cost for 4Q 2007 and FY 2007 exclude Measat Impairment

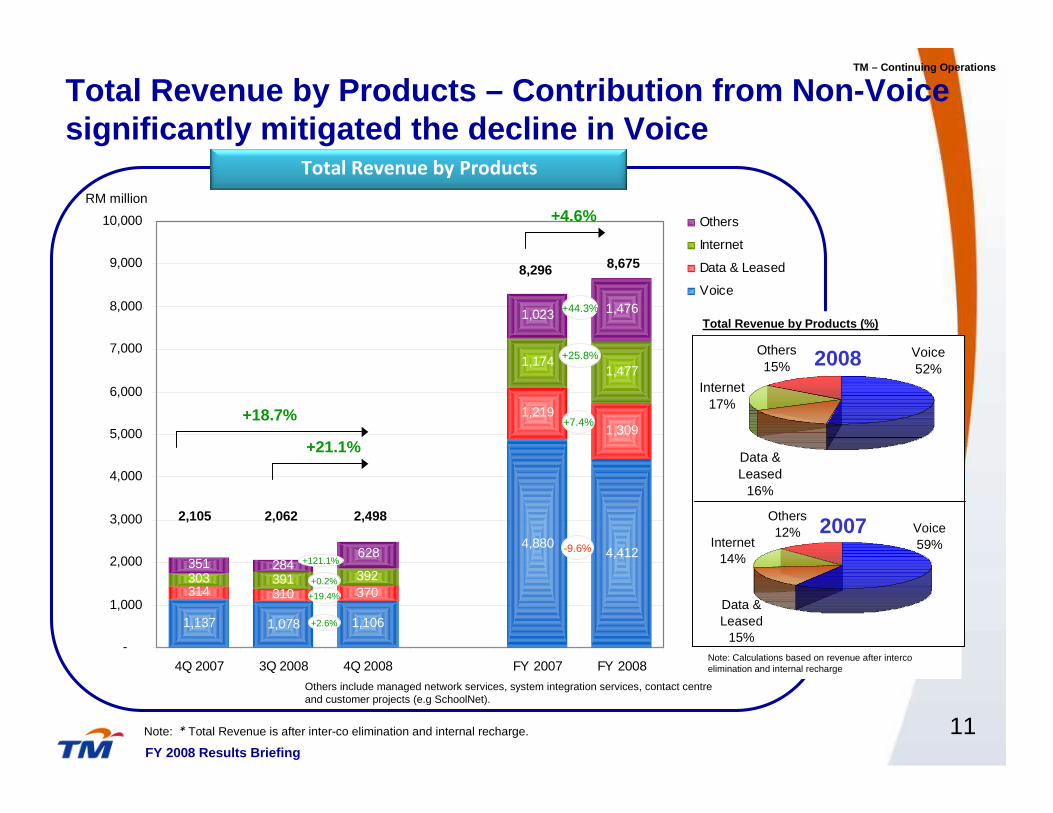

1,137 1,078 1,106

4,412

314 310

1,2191,309

303 391 392

1,1741,477

351 284

1,023 1,476

4,880

370

628

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

4Q 2007 3Q 2008 4Q 2008 FY 2007 FY 2008

Others

Internet

Data & Leased

Voice

Total Revenue by Products – Contribution from Non-Vo ice significantly mitigated the decline in Voice

Note: * Total Revenue is after inter-co elimination and internal recharge.

Total Revenue by Products

11

2,105 2,062 2,498

8,296 8,675

+18.7%

+4.6%

+21.1%

+44.3%

+25.8%

-9.6%+121.1%

+0.2%

+19.4%

+2.6%

RM million

+7.4%

TM – Continuing Operations

Others include managed network services, system integration services, contact centre and customer projects (e.g SchoolNet).

FY 2008 Results Briefing

2008

2007

Data & Leased

16%

Internet17%

Others15%

Voice52%

Data & Leased

15%

Internet14%

Others12% Voice

59%

Total Revenue by Products (%)

Note: Calculations based on revenue after intercoelimination and internal recharge

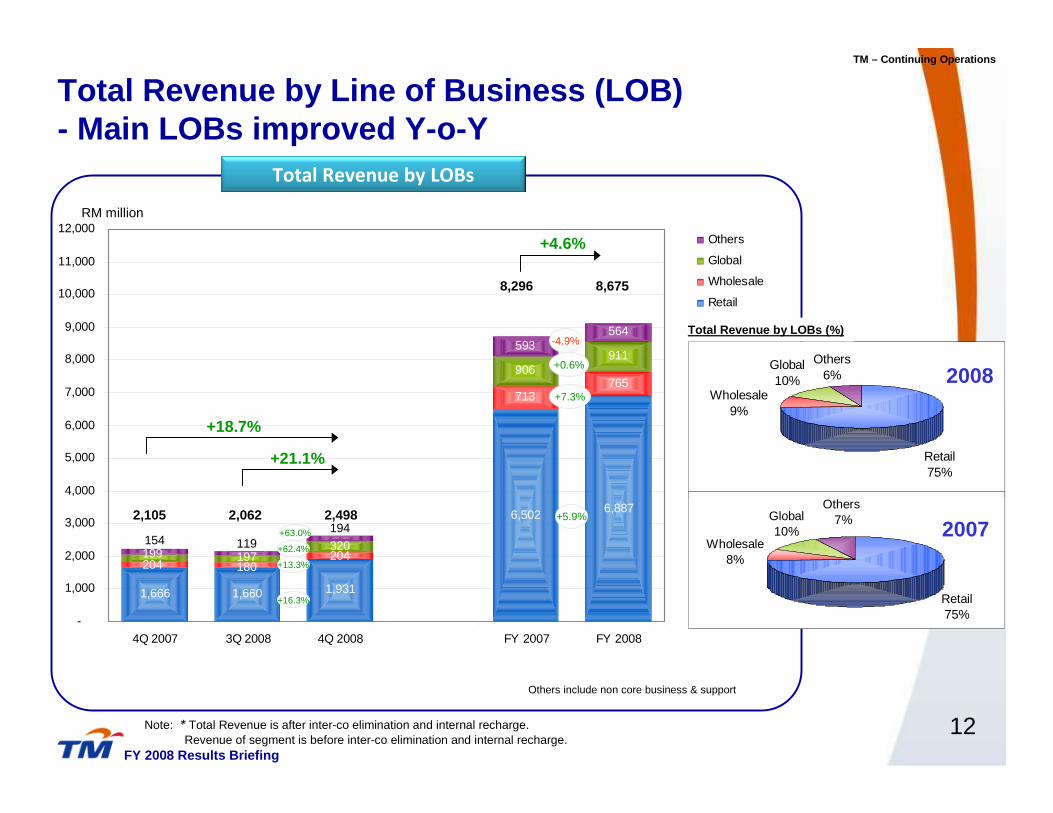

1,666 1,660 1,931

6,887

713765

320

906911

593564

6,502

180204204197199

194154 119

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

4Q 2007 3Q 2008 4Q 2008 FY 2007 FY 2008

Others

Global

Wholesale

Retail

Total Revenue by Line of Business (LOB) - Main LOBs improved Y-o-Y

Note: * Total Revenue is after inter-co elimination and internal recharge. Revenue of segment is before inter-co elimination and internal recharge.

Total Revenue by LOBs

12

+5.9%

+7.3%

+0.6%

-4.9%

+63.0%

+62.4%

+13.3%

+16.3%

RM million

TM – Continuing Operations

Others include non core business & support

2,105 2,062 2,498

8,296 8,675

+18.7%

+4.6%

+21.1%

FY 2008 Results Briefing

Retail75%

Global10%

Others6%

Wholesale9%

2008

Wholesale8%

Global10%

Others 7%

Retail75%

2007

Total Revenue by LOBs (%)

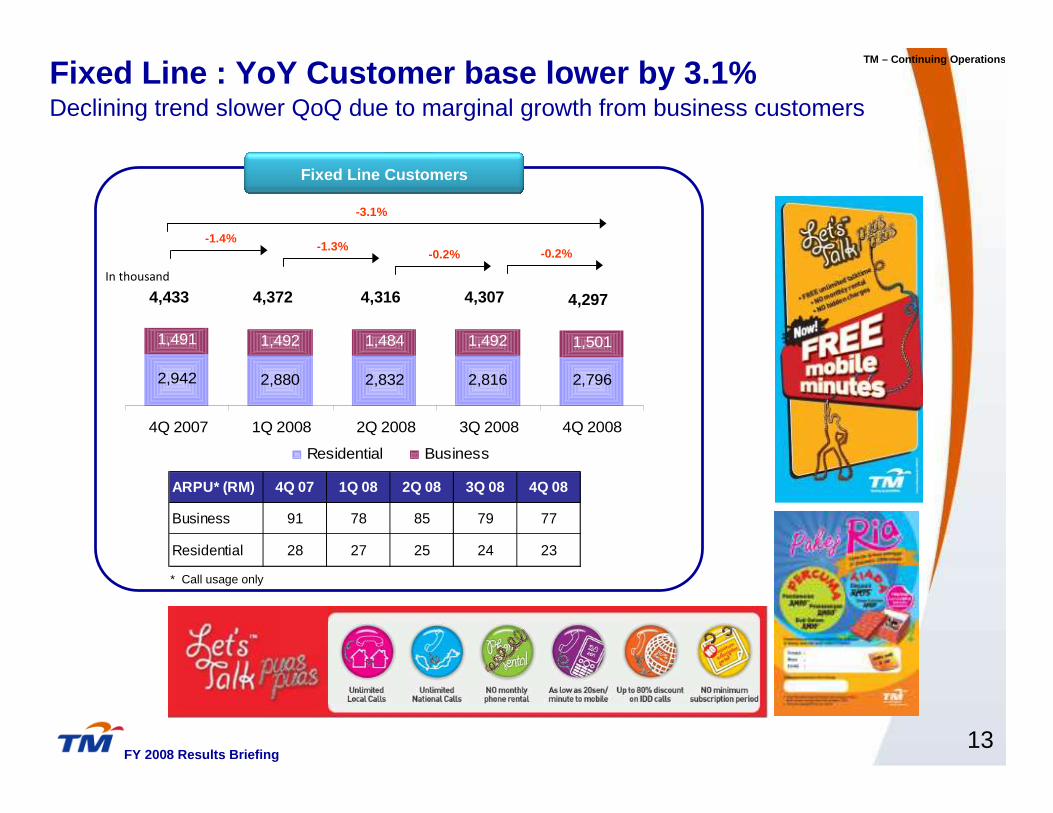

2,942 2,880 2,832 2,816 2,796

1,491 1,492 1,484 1,492 1,501

4Q 2007 1Q 2008 2Q 2008 3Q 2008 4Q 2008

Residential Business

In thousand

4,316 4,2974,433 4,372

13

Fixed Line Customers

* Call usage only

4,307

-0.2%-1.4%

-1.3%-0.2%

TM – Continuing Operations

Fixed Line : YoY Customer base lower by 3.1%Declining trend slower QoQ due to marginal growth from business customers

-3.1%

FY 2008 Results Briefing

ARPU* (RM) 4Q 07 1Q 08 2Q 08 3Q 08 4Q 08

Business 91 78 85 79 77

Residential 28 27 25 24 23

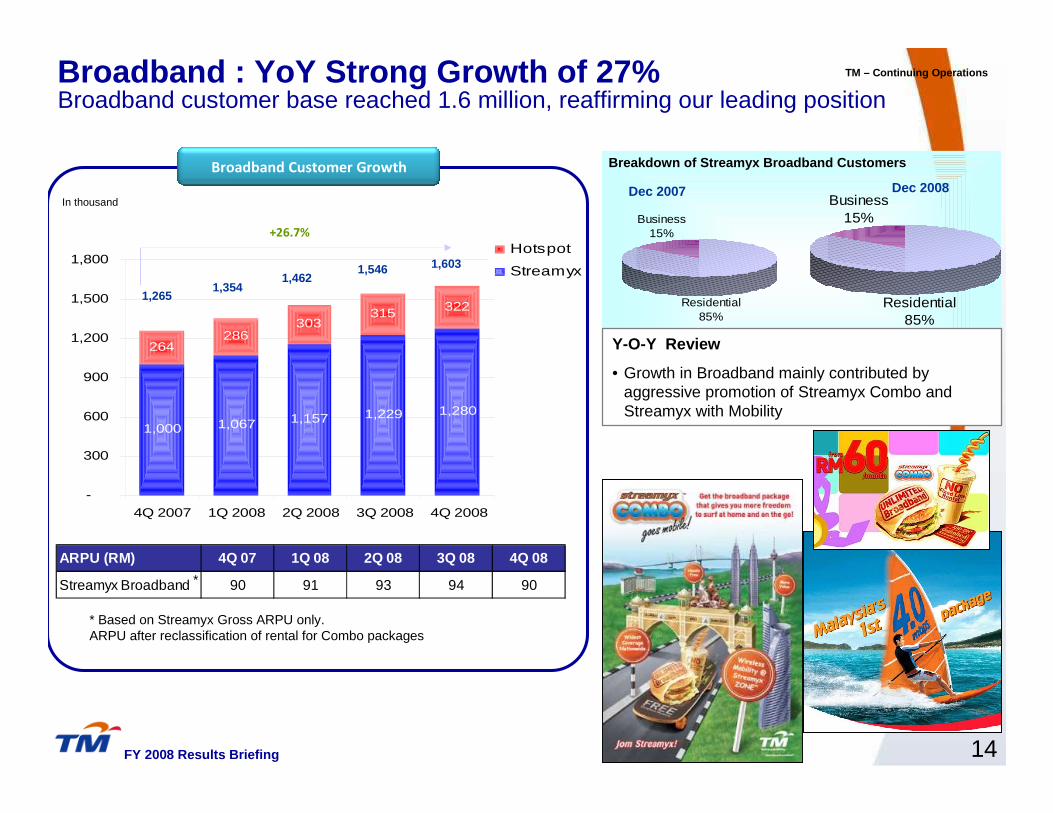

Broadband : YoY Strong Growth of 27%

14

1,000 1,067 1,157 1,229 1,280

264286

303315 322

-

300

600

900

1,200

1,500

1,800

4Q 2007 1Q 2008 2Q 2008 3Q 2008 4Q 2008

Hotspot

Streamyx

In thousand

1,603

1,2651,354

1,462

+26.7%

1,546

* Based on Streamyx Gross ARPU only.ARPU after reclassification of rental for Combo packages

*

Breakdown of Streamyx Broadband Customers

Dec 2007 Dec 2008Business

15%

Residential85%

Y-O-Y Review

• Growth in Broadband mainly contributed by aggressive promotion of Streamyx Combo and Streamyx with Mobility

TM – Continuing Operations

Business15%

Residential85%

Broadband Customer Growth

FY 2008 Results Briefing

ARPU (RM) 4Q 07 1Q 08 2Q 08 3Q 08 4Q 08

Streamyx Broadband 90 91 93 94 90

Broadband customer base reached 1.6 million, reaffirming our leading position

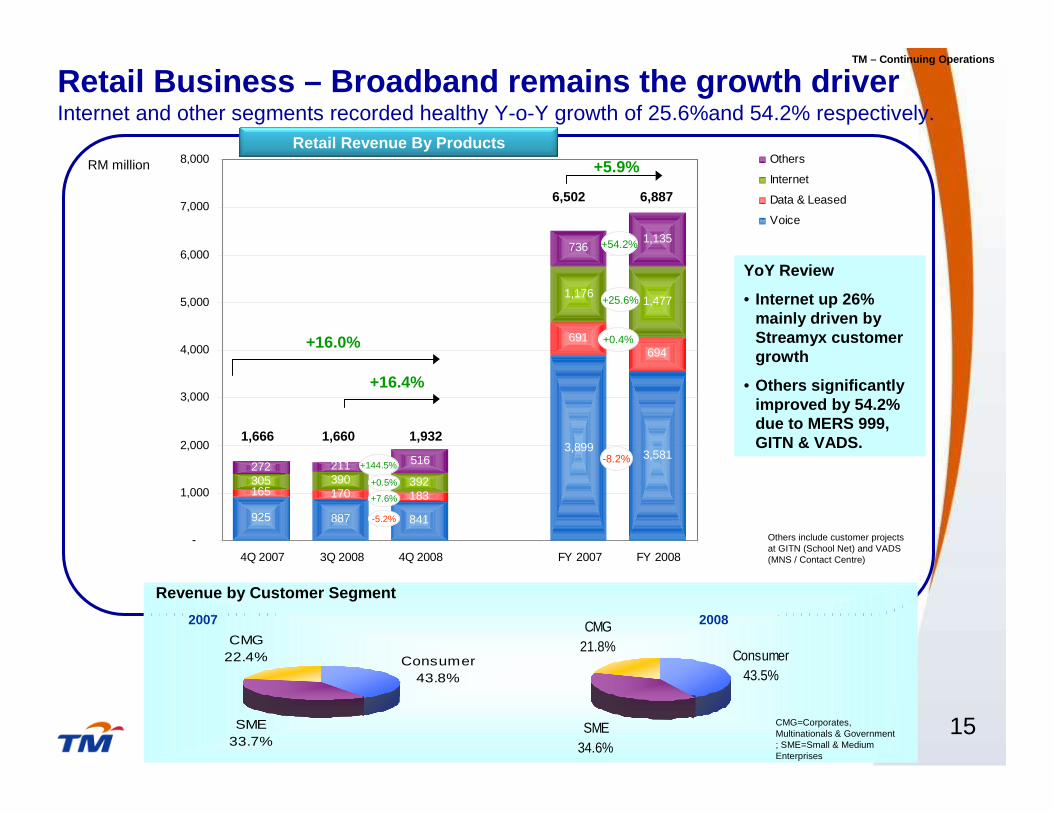

925 887 841

3,581

165 170 183

691694

305 390 392

1,1761,477

272 211

7361,135

3,899516

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

4Q 2007 3Q 2008 4Q 2008 FY 2007 FY 2008

Others

Internet

Data & Leased

Voice

1,666 1,660 1,932

6,502 6,887

+16.0%

+5.9%

+16.4%

-8.2%

+0.4%

+25.6%

+54.2%

+144.5%

+0.5%

+7.6%

-5.2%

RM million

Retail Business – Broadband remains the growth drive r Internet and other segments recorded healthy Y-o-Y growth of 25.6%and 54.2% respectively.

15

Retail Revenue By Products

YoY Review

• Internet up 26% mainly driven by Streamyx customer growth

• Others significantly improved by 54.2% due to MERS 999, GITN & VADS.

Revenue by Customer Segment

20082007

CMG=Corporates, Multinationals & Government ; SME=Small & Medium Enterprises

CMG21.8%

SME34.6%

Consumer43.5%

CMG22.4% Consumer

43.8%

SME33.7%

TM – Continuing Operations

Others include customer projects at GITN (School Net) and VADS (MNS / Contact Centre)

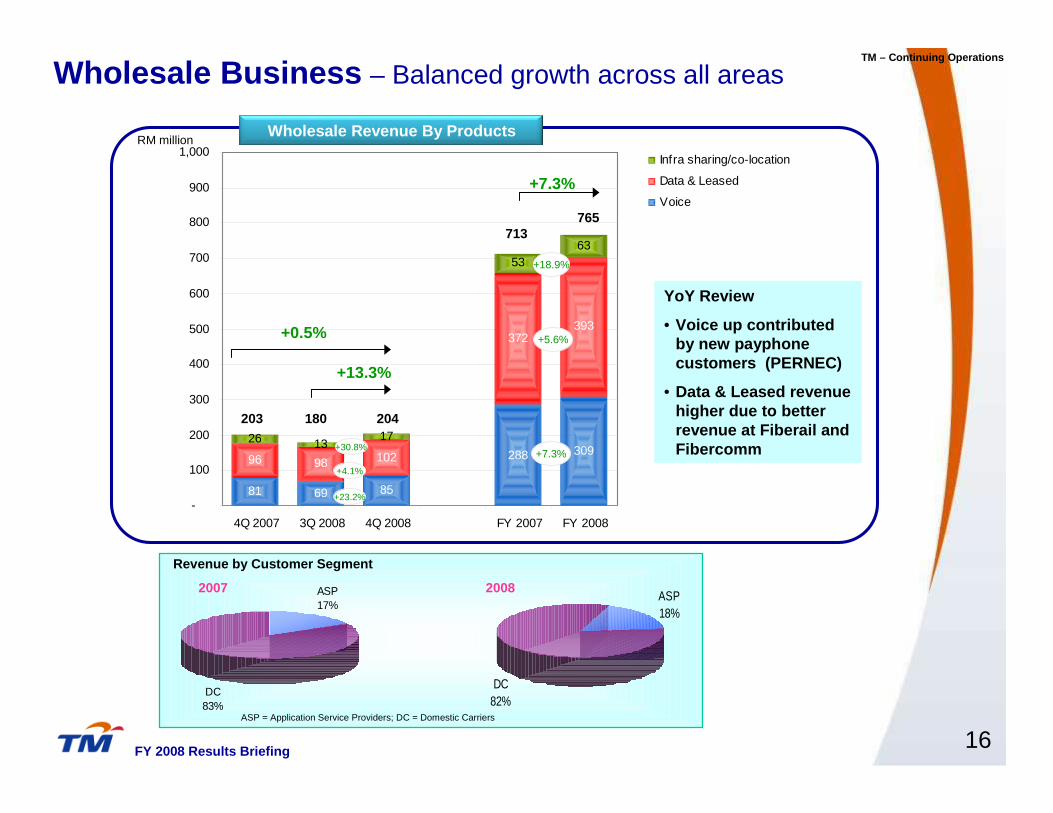

81 69 85

30996 98 102

372393

26 1317

5363

288

-

100

200

300

400

500

600

700

800

900

1,000

4Q 2007 3Q 2008 4Q 2008 FY 2007 FY 2008

Infra sharing/co-location

Data & Leased

Voice

16

RM millionWholesale Revenue By Products

16

Wholesale Business – Balanced growth across all areas

203 180 204

713765

+7.3%

+13.3%

+5.6%

+18.9%

+30.8%

+4.1%

+23.2%

+0.5%

+7.3%

ASP17%

DC83%

Revenue by Customer Segment

ASP = Application Service Providers; DC = Domestic Carriers

DC82%

ASP18%

20082007

TM – Continuing Operations

FY 2008 Results Briefing

YoY Review

• Voice up contributed by new payphone customers (PERNEC)

• Data & Leased revenue higher due to better revenue at Fiberail and Fibercomm

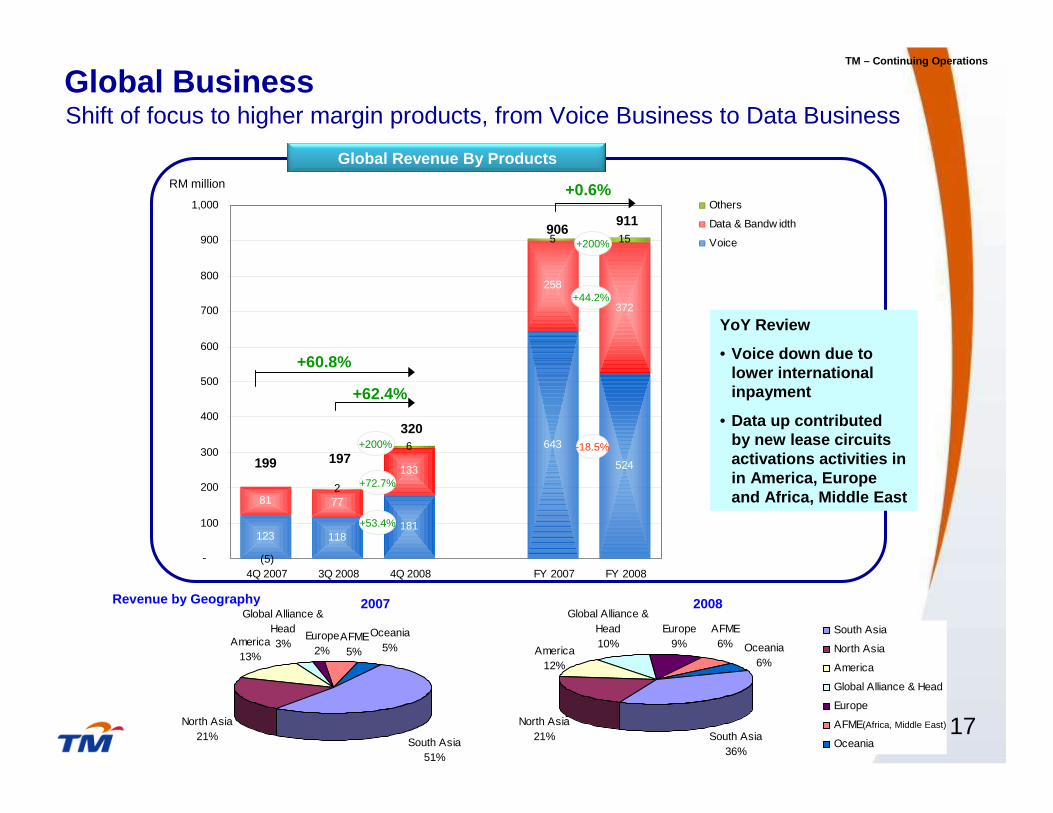

123 118181

524

81 77

133

258

372

(5)

2

6

5 15

643

-

100

200

300

400

500

600

700

800

900

1,000

4Q 2007 3Q 2008 4Q 2008 FY 2007 FY 2008

Others

Data & Bandw idth

Voice

Global Business

17

199 197

320

906911

+60.8%

+0.6%

+62.4%

-18.5%

+44.2%

+200%

RM million

Global Revenue By Products

Revenue by Geography 20082007

TM – Continuing Operations

+200%

+72.7%

+53.4%

North Asia21%

Oceania6%

AFME6%

Europe9%

South Asia36%

Global Alliance & Head10%

America 12%

South Asia

North Asia

America

Global Alliance & Head

Europe

AFME

Oceania

America 13%

Global Alliance & Head3%

South Asia51%

Europe2%

AFME5%

Oceania5%

North Asia21%

(Africa, Middle East)

Shift of focus to higher margin products, from Voice Business to Data Business

YoY Review

• Voice down due to lower international inpayment

• Data up contributed by new lease circuits activations activities in in America, Europe and Africa, Middle East

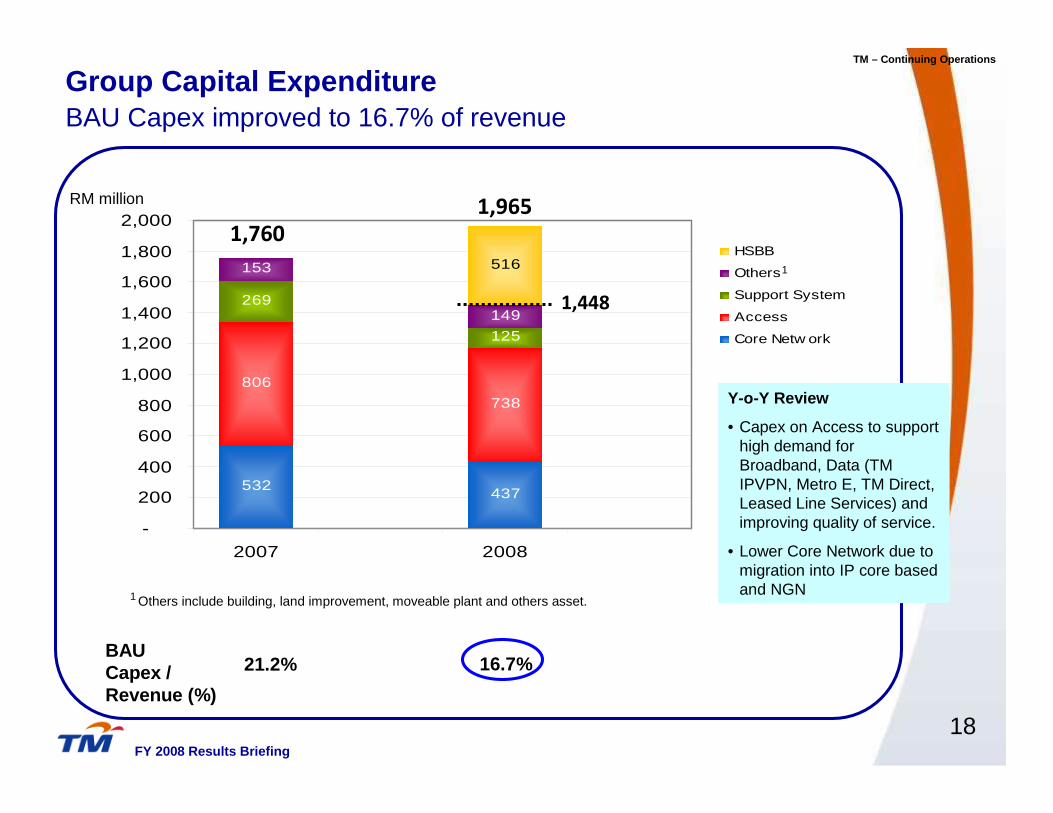

532437

806

738

269

125

153

149

516

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2007 2008

HSBB

Others

Support System

Access

Core Netw ork

Group Capital Expenditure

18

Others include building, land improvement, moveable plant and others asset.

RM million

1

1

1,760

1,965

BAU Capex improved to 16.7% of revenue

Y-o-Y Review

• Capex on Access to support high demand for Broadband, Data (TM IPVPN, Metro E, TM Direct, Leased Line Services) and improving quality of service.

• Lower Core Network due to migration into IP core based and NGN

TM – Continuing Operations

BAU Capex /Revenue (%)

21.2%

FY 2008 Results Briefing

16.7%

1,448

10,248.1

226.5

8,587.3

6,965.1

1,362.0

260.2.

19,061.9

9,412.4

2,127.9

763.4

4,025.0

2,095.2

400.9

3,471.3

2,812.6

34.9

-

623.8

5,941.1

11,772.1

1,348.7

19,061.9

31 Dec 08 31 Dec 07 31 Dec 08 31 Dec 07Return on Invested Capital 4.50% 4.30% Gross Debt/ Equity* 0.68 0.68Return on Equity 6.99% 4.31% Gross Debt/ Equity** 0.29 0.28Return on Assets 3.15% 3.89% Net Debt/ Equity* 0.48 0.46Current Ratio 2.71 2.00 Net Debt/ Equity** 0.09 0.06Debt to EBITDA 2.45 2.11 Net Assets/Share (sen) 296.5 291.5

10,025.7

172.9

8,064.9

6,587.4

1,431.3

46.2.

18,263.5

11,101.1

2,647.5

784.4

4,025.0

2,172.9

1,471.3

5,558.8

3,014.6

243.9

1,654.5

645.8

5,542.3

11,821.5

899.7

18,263.5

Balance Sheet and Key Financial Ratios

Shareholders’ Funds

Minority Interests

Deferred & Long Term Liabilities

Long Term Borrowings

Deferred Tax

Deferred Income

Current Assets

Trade Receivables

Other Receivables

Amount due from TMI

Cash & Bank Balances

Others

Current Liabilities

Trade and other Payables

Short Term Borrowings

Dividend Payable

Others

Net Current Assets

Property Plant & Equipment

Other Non-current Assets

RM Million As at 31 Dec 2007As at 31 Dec 2008

* Before Amount Due from TMI** After Amount Due from TMI

19

• Improved collections resulting in lower Trade Receivables

• Lower Fixed Assets due to efficient Capexspending

• Cash and Bank balances remain strong

TM – Continuing Operations

1

1 ROE Normalised

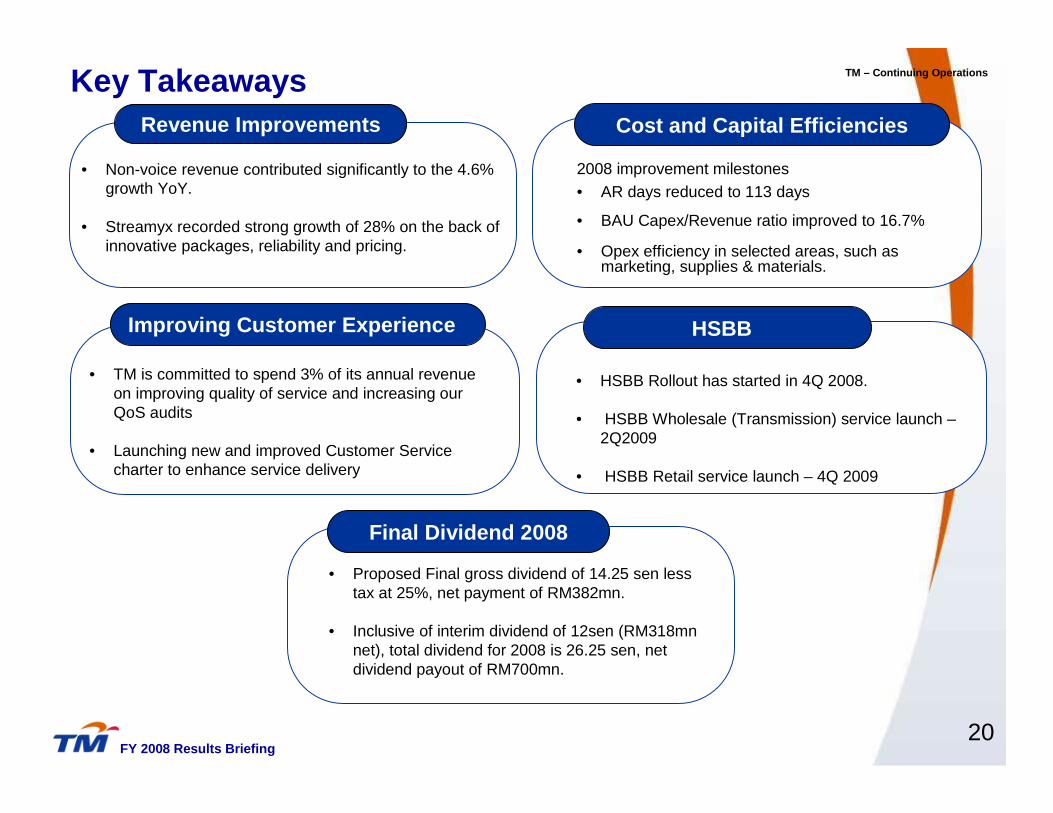

Improving Customer Experience

Cost and Capital Efficiencies

Final Dividend 2008

• Proposed Final gross dividend of 14.25 sen less tax at 25%, net payment of RM382mn.

• Inclusive of interim dividend of 12sen (RM318mn net), total dividend for 2008 is 26.25 sen, net dividend payout of RM700mn.

2008 improvement milestones• AR days reduced to 113 days

• BAU Capex/Revenue ratio improved to 16.7%

• Opex efficiency in selected areas, such as marketing, supplies & materials.

• TM is committed to spend 3% of its annual revenue on improving quality of service and increasing our QoS audits

• Launching new and improved Customer Service charter to enhance service delivery

Key Takeaways

20

Revenue Improvements

• Non-voice revenue contributed significantly to the 4.6% growth YoY.

• Streamyx recorded strong growth of 28% on the back of innovative packages, reliability and pricing.

TM – Continuing Operations

HSBB

FY 2008 Results Briefing

• HSBB Rollout has started in 4Q 2008.

• HSBB Wholesale (Transmission) service launch –2Q2009

• HSBB Retail service launch – 4Q 2009

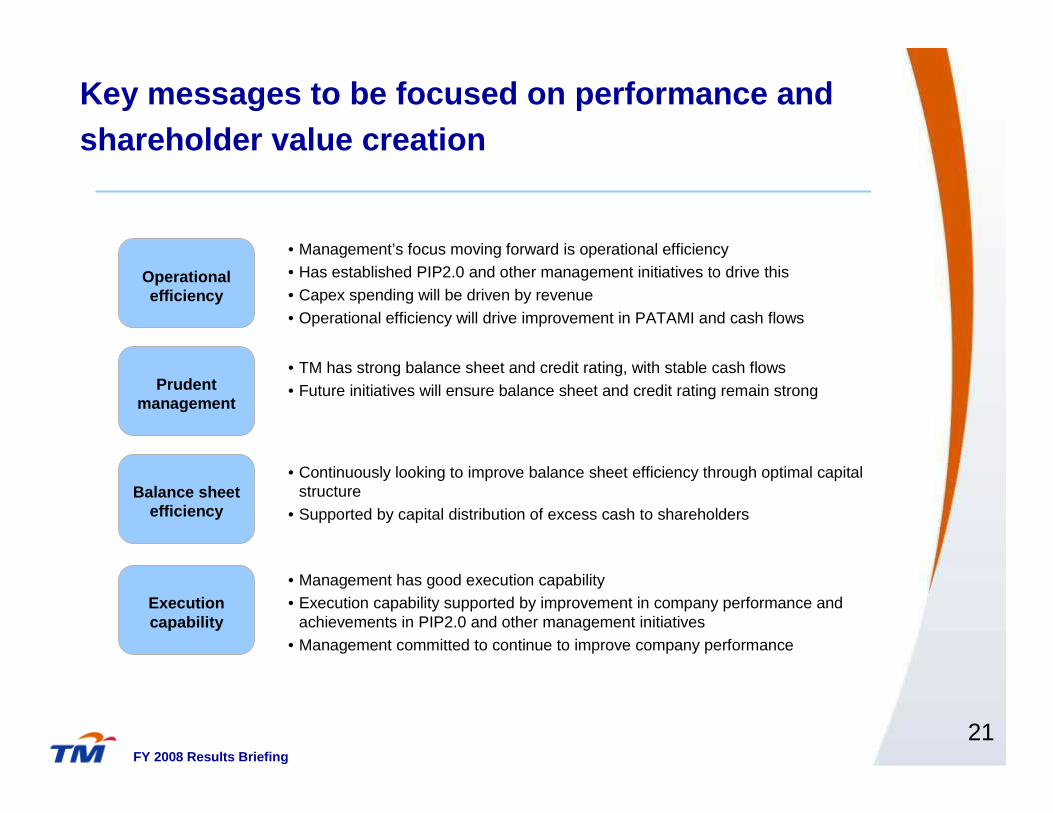

Key messages to be focused on performance and shareholder value creation

Operational efficiency

• Management has good execution capability• Execution capability supported by improvement in company performance and

achievements in PIP2.0 and other management initiatives• Management committed to continue to improve company performance

Prudent management

Balance sheet efficiency

Execution capability

• Management’s focus moving forward is operational efficiency• Has established PIP2.0 and other management initiatives to drive this• Capex spending will be driven by revenue• Operational efficiency will drive improvement in PATAMI and cash flows

• TM has strong balance sheet and credit rating, with stable cash flows• Future initiatives will ensure balance sheet and credit rating remain strong

• Continuously looking to improve balance sheet efficiency through optimal capital structure

• Supported by capital distribution of excess cash to shareholders

FY 2008 Results Briefing

21

Capital management approach guided by 3 main principles

Exercise prudent approach to managing capital struc ture

Strive to optimise performance

A

B

Create value for shareholders

C

Guiding principles

FY 2008 Results Briefing

22

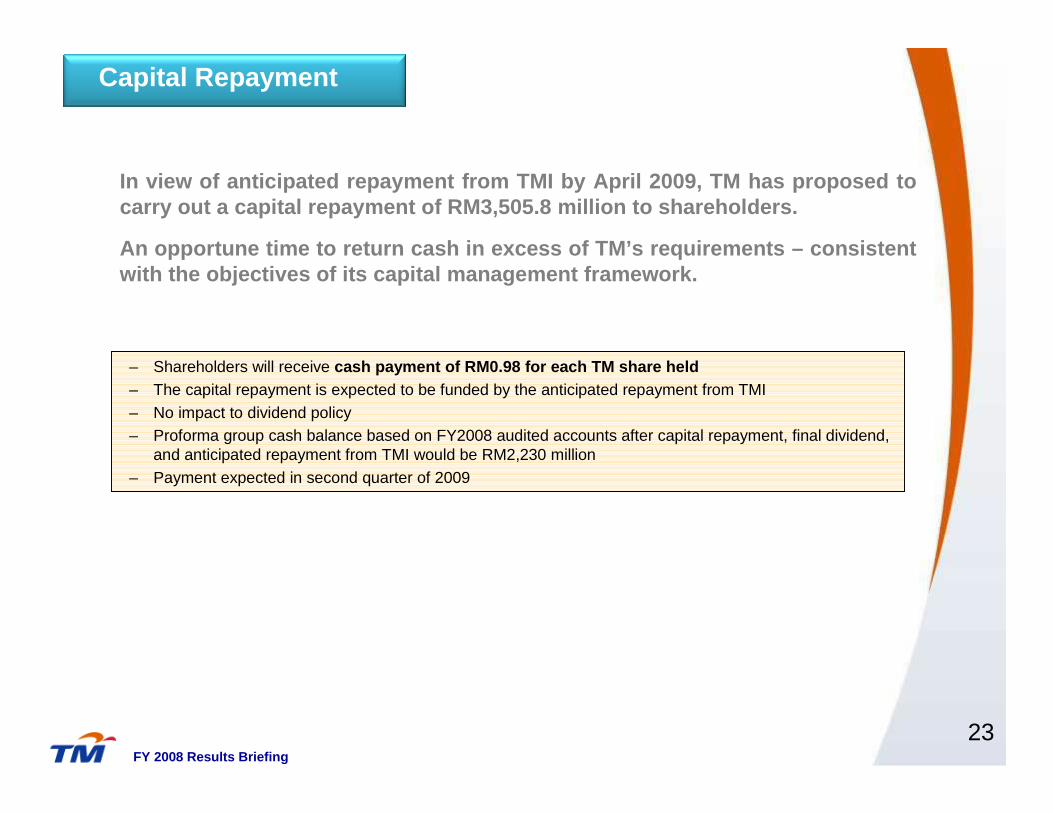

– Shareholders will receive cash payment of RM0.98 for each TM share held– The capital repayment is expected to be funded by the anticipated repayment from TMI– No impact to dividend policy– Proforma group cash balance based on FY2008 audited accounts after capital repayment, final dividend,

and anticipated repayment from TMI would be RM2,230 million– Payment expected in second quarter of 2009

In view of anticipated repayment from TMI by April 2 009, TM has proposed to carry out a capital repayment of RM3,505.8 million t o shareholders.

An opportune time to return cash in excess of TM’s requirements – consistent with the objectives of its capital management frame work.

FY 2008 Results Briefing

Capital Repayment

23

This presentation is not and does not constitute an offer, invitation, solicitation or recommendation to subscribe for, or purchase, any securities and neither this presentation nor anything contained in it shall form the basis of, or be relied on in connection with any contract or commitment or investment decision.

This presentation has been prepared solely for use at this presentation. By your continued attendance at this presentation, you are deemed to have agreed and confirmed to Telekom Malaysia Berhad (the “Company”) that: (a) you agree not to trade in any securities of the Company or its respective affiliates until the public disclosure of the information contained herein; and (b) you agree to maintain absolute confidentiality regarding the information disclosed in this presentation until the public disclosure of such information, or unless you have been otherwise notified by the Company.

Reliance should not be placed on the information or opinions contained in this presentation or on its completeness. This presentation does not take into consideration the investment objectives, financial situation or particular needs of any particular investor. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information, opinions and conclusions contained in this presentation. None of the Company and its affiliates and related bodies corporate, and their respective officers, directors, employees and agents disclaim any liability (including, without limitation, any liability arising from fault or negligence) for any loss arising from any use of this presentation or its contents or otherwise arising in connection with it.

This presentation contains projections and “forward-looking statements” relating to the Company’s business and the sectors in which the Company operates. These forward-looking statements include statements relating to the Company’s performance. These statements reflect the current views of the Company with respect to future events and are subject to certain risks, uncertainties and assumptions. It is important to note that actual results could differ materially from those anticipated in these forward looking statements. The Company does not undertake to inform you of any matters or information which may come to light or be brought to the Company’s attention after the date hereof.

The forecasts and other forward-looking statements set out in this presentation are based on a number of estimates and assumptions that are subject to business, economic and competitive uncertainties and contingencies, with respect to future business decisions, which are subject to change and in many cases outside the control of the Company. The directors and officers of the Company believe that they have prepared the forecasts with due care and attention and consider all best estimates and assumptions when taken as a whole to be reasonable at the time of preparing the presentation. However, the Company’s forecasts presented in this presentation may vary from actual financial results, and these variations may be material and, accordingly, neither the Company nor its directors or officers can give any assurance that the forecast performance in the forecasts or any forward-looking statement contained in this presentation will be achieved. Details of the forecasts and the assumptions on which they are based are set out in the presentation.

This presentation may not be copied or otherwise reproduced without the written consent of the Company.

Disclaimer

25FY 2008 Results Briefing