minit mesyuarat - mia.org.my · ms. 3 / 7 b. wakil persatuan akauntan dan pengamal percukaian 1....

TRANSCRIPT

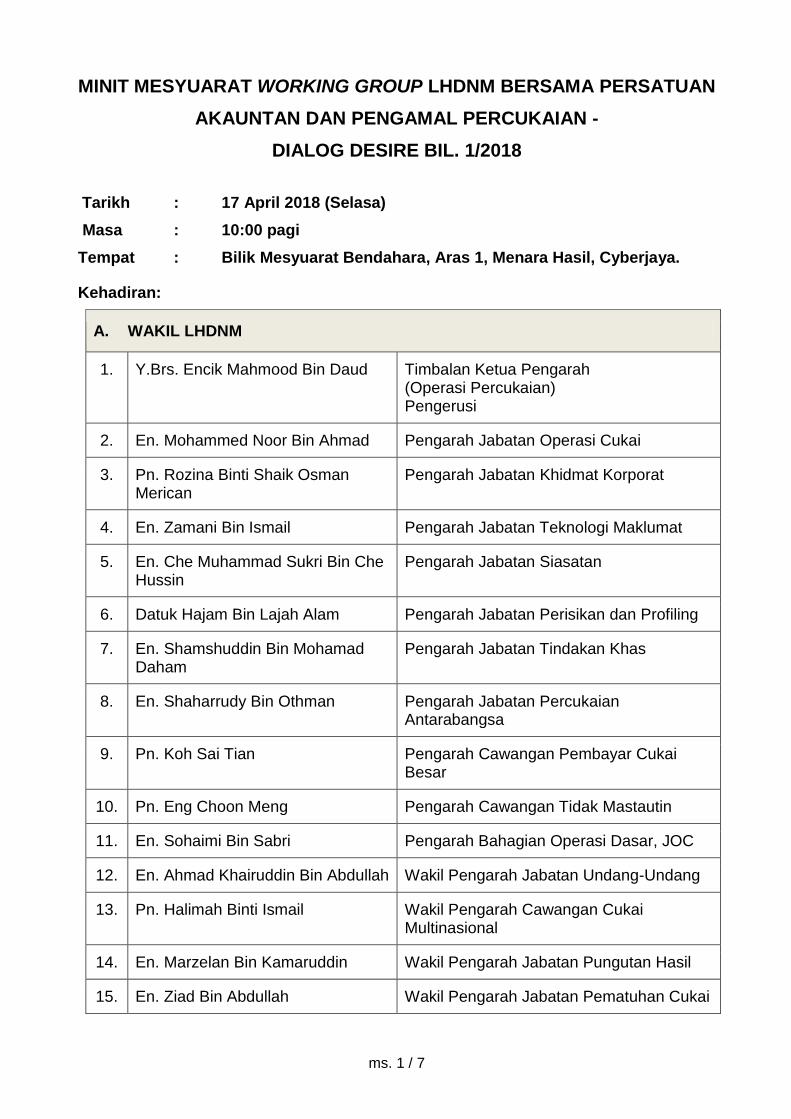

ms. 1 / 7

MINIT MESYUARAT WORKING GROUP LHDNM BERSAMA PERSATUAN

AKAUNTAN DAN PENGAMAL PERCUKAIAN -

DIALOG DESIRE BIL. 1/2018

Tarikh : 17 April 2018 (Selasa)

Masa : 10:00 pagi

Tempat : Bilik Mesyuarat Bendahara, Aras 1, Menara Hasil, Cyberjaya.

Kehadiran:

A. WAKIL LHDNM

1. Y.Brs. Encik Mahmood Bin Daud Timbalan Ketua Pengarah (Operasi Percukaian) Pengerusi

2. En. Mohammed Noor Bin Ahmad Pengarah Jabatan Operasi Cukai

3. Pn. Rozina Binti Shaik Osman Merican

Pengarah Jabatan Khidmat Korporat

4. En. Zamani Bin Ismail Pengarah Jabatan Teknologi Maklumat

5. En. Che Muhammad Sukri Bin Che Hussin

Pengarah Jabatan Siasatan

6. Datuk Hajam Bin Lajah Alam Pengarah Jabatan Perisikan dan Profiling

7. En. Shamshuddin Bin Mohamad Daham

Pengarah Jabatan Tindakan Khas

8. En. Shaharrudy Bin Othman Pengarah Jabatan Percukaian Antarabangsa

9. Pn. Koh Sai Tian Pengarah Cawangan Pembayar Cukai Besar

10. Pn. Eng Choon Meng Pengarah Cawangan Tidak Mastautin

11. En. Sohaimi Bin Sabri Pengarah Bahagian Operasi Dasar, JOC

12. En. Ahmad Khairuddin Bin Abdullah Wakil Pengarah Jabatan Undang-Undang

13. Pn. Halimah Binti Ismail Wakil Pengarah Cawangan Cukai Multinasional

14. En. Marzelan Bin Kamaruddin Wakil Pengarah Jabatan Pungutan Hasil

15. En. Ziad Bin Abdullah Wakil Pengarah Jabatan Pematuhan Cukai

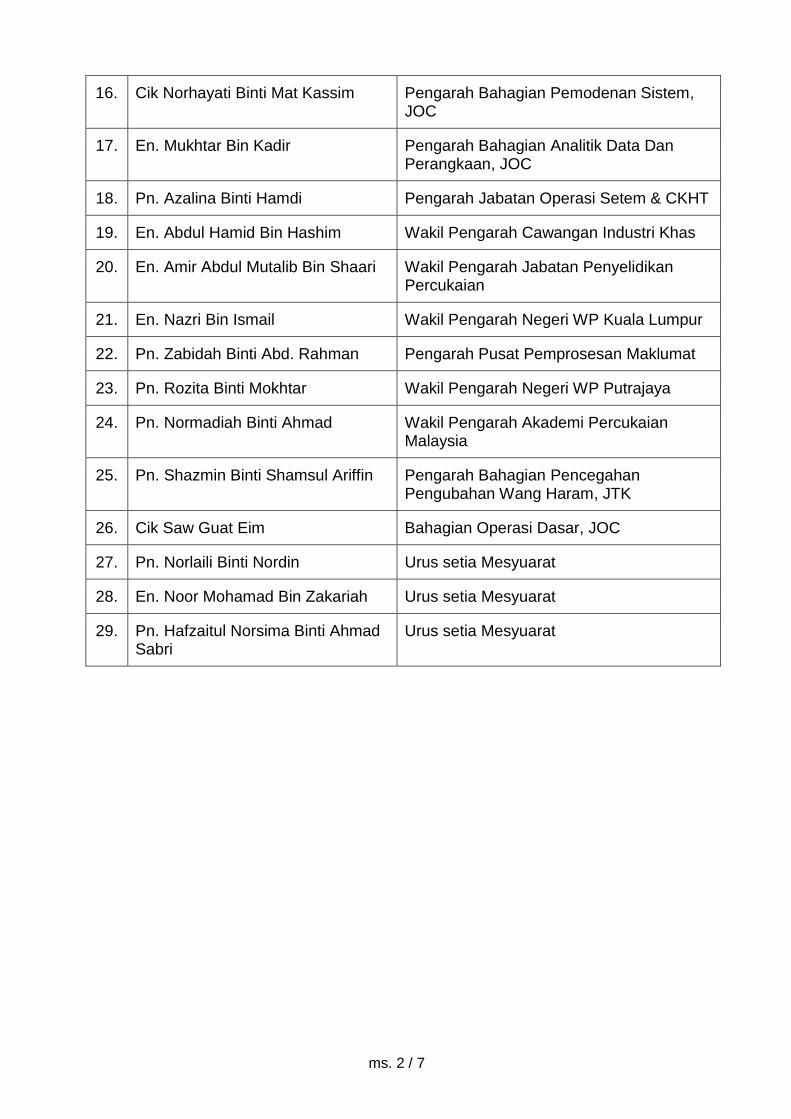

ms. 2 / 7

16. Cik Norhayati Binti Mat Kassim Pengarah Bahagian Pemodenan Sistem, JOC

17. En. Mukhtar Bin Kadir Pengarah Bahagian Analitik Data Dan Perangkaan, JOC

18. Pn. Azalina Binti Hamdi Pengarah Jabatan Operasi Setem & CKHT

19. En. Abdul Hamid Bin Hashim Wakil Pengarah Cawangan Industri Khas

20. En. Amir Abdul Mutalib Bin Shaari Wakil Pengarah Jabatan Penyelidikan Percukaian

21. En. Nazri Bin Ismail Wakil Pengarah Negeri WP Kuala Lumpur

22. Pn. Zabidah Binti Abd. Rahman Pengarah Pusat Pemprosesan Maklumat

23. Pn. Rozita Binti Mokhtar Wakil Pengarah Negeri WP Putrajaya

24. Pn. Normadiah Binti Ahmad Wakil Pengarah Akademi Percukaian Malaysia

25. Pn. Shazmin Binti Shamsul Ariffin Pengarah Bahagian Pencegahan Pengubahan Wang Haram, JTK

26. Cik Saw Guat Eim Bahagian Operasi Dasar, JOC

27. Pn. Norlaili Binti Nordin Urus setia Mesyuarat

28. En. Noor Mohamad Bin Zakariah Urus setia Mesyuarat

29. Pn. Hafzaitul Norsima Binti Ahmad Sabri

Urus setia Mesyuarat

ms. 3 / 7

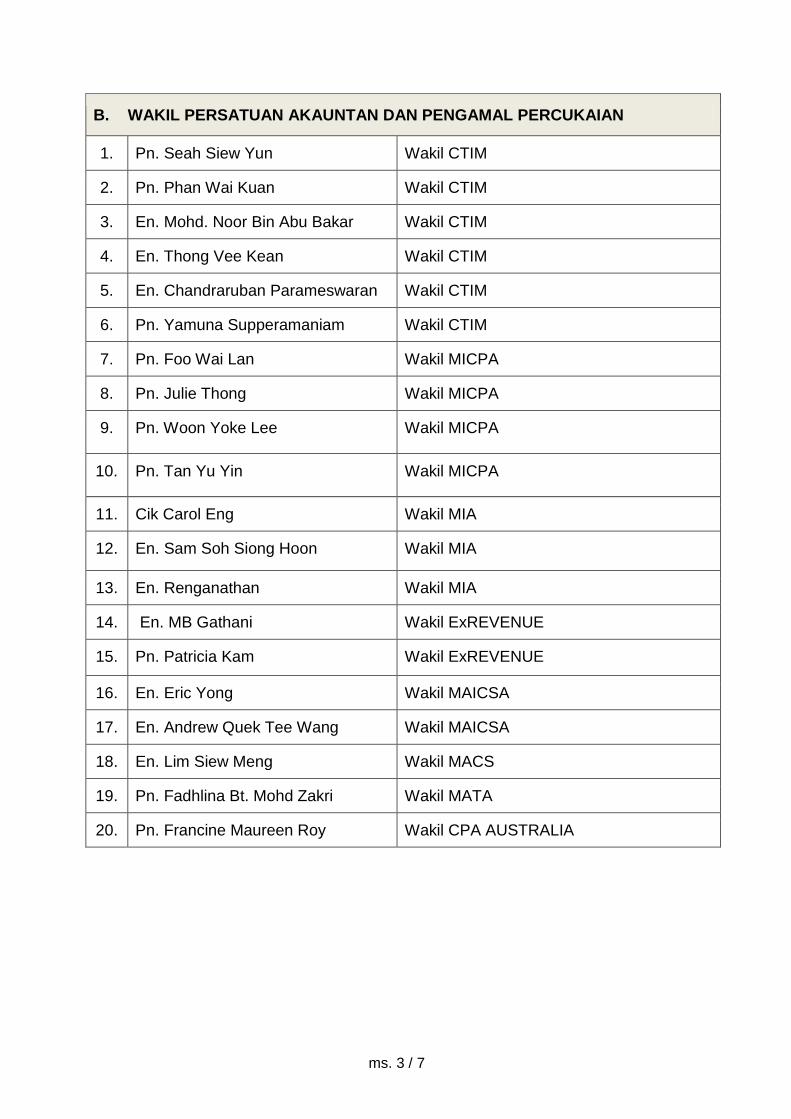

B. WAKIL PERSATUAN AKAUNTAN DAN PENGAMAL PERCUKAIAN

1. Pn. Seah Siew Yun Wakil CTIM

2. Pn. Phan Wai Kuan Wakil CTIM

3. En. Mohd. Noor Bin Abu Bakar Wakil CTIM

4. En. Thong Vee Kean Wakil CTIM

5. En. Chandraruban Parameswaran Wakil CTIM

6. Pn. Yamuna Supperamaniam Wakil CTIM

7. Pn. Foo Wai Lan Wakil MICPA

8. Pn. Julie Thong Wakil MICPA

9. Pn. Woon Yoke Lee Wakil MICPA

10. Pn. Tan Yu Yin Wakil MICPA

11. Cik Carol Eng Wakil MIA

12. En. Sam Soh Siong Hoon Wakil MIA

13. En. Renganathan Wakil MIA

14. En. MB Gathani Wakil ExREVENUE

15. Pn. Patricia Kam Wakil ExREVENUE

16. En. Eric Yong Wakil MAICSA

17. En. Andrew Quek Tee Wang Wakil MAICSA

18. En. Lim Siew Meng Wakil MACS

19. Pn. Fadhlina Bt. Mohd Zakri Wakil MATA

20. Pn. Francine Maureen Roy Wakil CPA AUSTRALIA

ms. 4 / 7

1. UCAPAN PENDAHULUAN PENGERUSI

1.1. Pengerusi memulakan dengan ucapan salam, selamat pagi dan selamat

datang kepada ahli-ahli mesyuarat yang terdiri daripada wakil-wakil badan

profesional dan pengarah-pengarah Jabatan / Bahagian yang hadir ke

mesyuarat DESIRE yang pertama bagi tahun 2018.

1.2. Sesi dialog ini adalah bertujuan untuk menambahbaik sistem penyampaian

perkhidmatan LHDNM kepada pembayar cukai dan mewujudkan tax

ecosystem yang sihat. Pengerusi mengalu-alukan sebarang proposal dari

badan-badan profesional berkaitan penambahbaikan prosedur operasi untuk

meningkatkan perkhidmatan LHDNM.

1.3. LHDNM juga secara berterusan meningkatkan inovasi dalam bidang teknologi

maklumat setanding dengan negara luar di peringkat antarabangsa dalam

menyediakan kemudahan dan perkhidmatan kepada pembayar cukai.

Pelbagai inisiatif diwujudkan dari masa ke masa mengikut trend dan

keperluan semasa demi melancarkan sistem percukaian. Selari dengan era

digital, LHDNM telah membangunkan Hasil Power Data untuk

mengembangkan penggunaan teknologi dalam operasi seharian. Pengerusi

juga memaklumkan LHDNM telah mengambil inisiatif untuk mengoptimumkan

penggunaan teknologi terkini dengan membangunkan Hasil InfoQ iaitu

aplikasi mobil yang lebih mesra pengguna, mudah dan senang untuk diakses.

1.4. Badan profesional ini memainkan peranan yang penting kepada kerajaan,

khususnya LHDNM kerana sebagai pihak yang berhubung rapat dengan

pembayar cukai perlu bertanggungjawab membantu kerajaan dan LHDNM

dalam memberikan penerangan kepada pembayar cukai berkaitan sistem-

sistem percukaian dan perkhidmatan baharu yang diperkenalkan sebagai

kemudahan kepada pembayar-pembayar cukai.

1.5. Walau bagaimanapun, terdapat ejen cukai yang menggunakan kemudahan

yang disediakan LHDNM ini untuk kepentingan peribadi terutama dalam

menyelesaikan kes pelanggan mereka seperti menghubungi Hasil Care Line

dengan pertanyaan teknikal seperti penetapan tempoh asas dan sebagainya.

ms. 5 / 7

Pengerusi mohon kerjasama badan profesional untuk menasihati ahli

persatuan masing-masing untuk tidak menyalahgunakan kemudahan ini yang

sepatutnya dinikmati oleh pembayar cukai yang sebenar untuk

menyelesaikan masalah percukaian mereka.

1.6. Dalam mesyuarat ini, isu-isu berkaitan operasi yang dikemukakan oleh

Persatuan Akauntan dan Badan Pengamal Percukaian atau badan

profesional ini telah di semak dan di buat penambahbaikan bagi melancarkan

lagi operasi percukaian serta meningkatkan kecekapan sistem percukaian di

samping memudahkan urusan percukaian di pihak pembayar cukai dan ejen

cukai.

1.7. Pengerusi menekankan supaya badan profesional mengemukakan isu yang

melibatkan prosedur operasi dan kelemahan sistem percukaian. Manakala

isu-isu kecil perlu diselesaikan di peringkat jabatan / cawangan berkaitan.

Langkah ini juga penting supaya permasalahan yang berlaku boleh

diselesaikan dengan kadar segera dan tidak perlu menunggu mesyuarat ini

yang hanya bersidang setahun sekali.

2. PERBINCANGAN ISU DAN MAKLUM BALAS PEMILIK PROSES

A. Lampiran 1 – CTIM Memorandum On Compliance And Operational

Issues dated 23 January 2018

B. Lampiran 2 – MAICSA Issues For Discussion at DESIRE Bil.1/2018 Dialogue

C. Lampiran 3 – CTIM Additional 7 Issues dated 13 April 2018

(isu-isu ini tidak dibentangkan dalam mesyuarat)

3. PERKARA BERBANGKIT

3.1 Encik Sam Soh, seorang wakil MIA dari Johor Bahru membangkitkan

beberapa isu seperti berikut:

3.1.1 Yuran Pengarah dilaporkan dalam dua kaedah – asas akruan (accrual)

atau peruntukan (provision); wakil Jabatan Pematuhan Cukai memaklumkan

ms. 6 / 7

sekiranya item ini telah dilaporkan dalam Penyata Tahunan Pengarah

tersebut, maka perbelanjaan adalah dibenarkan dituntut oleh syarikat di

bawah peruntukan seksyen 33 ACP 1967;

3.1.2 minta pegawai LHDNM hanya berurusan dengan ejen cukai sahaja

berkenaan pelanggan yang kena tindakan audit dan bukannya dengan

peguam kerana mereka tidak memahami isu teknikal percukaian – perkara

ini di ambil maklum oleh pihak LHDNM;

3.1.3 beliau nyatakan pengendalian penalti melebihi RM35 juta dikendalikan

di Ibu Pejabat akan menyukarkan pelanggan untuk datang ke Kuala Lumpur.

Pengerusi mohon kemukakan kes untuk semakan. Walau bagaimanapun,

beliau maklumkan kes berkaitan telah dikemukakan kepada LHDNM dan

telah dimaklumkan oleh LHDNM bahawa kes ini masih dalam pertimbangan;

3.1.4 dialog seperti ini biasanya diadakan di Johor Bahru iaitu di peringkat

negeri tetapi telah lama tidak diadakan selama dua tahun berturut-turut

kerana Pengarah LHDNM terlalu sibuk dan tidak dapat meluangkan masa.

Mohon dialog ini diadakan di Johor Bahru bagi memudahkan ejen-ejen cukai

yang berdekatan – perkara ini di ambil maklum oleh pihak LHDNM.

3.2 Pn. Seah Siew Yun, Presiden CTIM membangkitkan isu tunggakan kes

Pesuruhjaya Khas Cukai Pendapatan yang berjumlah 796 yang telah

dimaklumkan dalam mesyuarat PEMUDAH. Daripada jumlah itu, hanya 409

kes sahaja yang telah mendapat tarikh giliran sehingga Jun 2021. Bakinya

yang berjumlah 387 kes akan melangkaui hingga ke tahun 2024. Dalam masa

yang sama, kes-kes baru akan bertambah dari masa ke masa. Tempoh masa

yang lama ini juga adalah disebabkan hanya ada satu panel sahaja

mengendalikan kes-kes ini. Beliau mohon penyelesaian berkenaan isu ini

dibuat dengan kadar segera.

3.3 Wakil exRevenue membangkitkan dua (2) isu seperti berikut:

3.3.1 Surat Sekatan Perjalanan Ke Luar Negara di bawah Seksyen 104 ACP

1967 dihantar ke alamat ejen cukai dan menyebabkan kelewatan

pemberitahuan ini disampaikan kepada pelanggan / pembayar cukai.

Pengerusi maklumkan setiap individu boleh membuat semakan sendiri sama

ms. 7 / 7

ada di laman web LHDNM, Hasil InfoQ dan aplikasi mobil tanpa perlu

menunggu surat yang di hantar secara pos.

3.3.2 Terdapat satu kes bayaran balik yang telah tertunggak semenjak tahun

2011 hingga kini masih belum selesai. Pengerusi minta kes ini di rujuk ke

Pengarah Negeri yang berkaitan untuk tindakan sewajarnya.

3.4 En. Renganathan Wakil MIA membangkitkan dua (2) isu seperti berikut:

3.4.1 mohon kerjasama pihak LHDNM untuk tidak melayan wakil yang tidak

dilantik sebagai ejen cukai. Terdapat kes yang memerlukan resolusi pertikaian

yang dikendalikan oleh beliau tetapi telah agak lewat dan menyukarkan untuk

mencari penyelesaian. Pengerusi maklumkan sememangnya LHDNM telah

mengarahkan pegawai LHDNM untuk tidak berurusan dengan wakil yang

tidak dilantik secara sah. Pengerusi minta beliau membuat laporan sekiranya

perkara ini masih berlaku dan kemukakan nama pegawai dan cawangan

LHDNM berkenaan yang dikatakan gagal mematuhi perintah ini

3.4.2 Proses Rayuan perlu dikendalikan oleh cawangan di mana pembayar

cukai berkenaan berdaftar. Perkara ini menimbulkan kesukaran kepada ejen

cukai untuk hadir ke cawangan jika melibatkan lokasi yang jauh. Oleh kerana

LHDNM telah meningkatkan penggunaan digital, beliau minta LHDNM

menambahbaik prosedur rayuan supaya proses ini dapat di buat dimana-

mana cawangan tanpa mengira cawangan sebenar yang mengendalikan

pembayar cukai terbabit. Kaedah seumpamanya juga perlu dipanjangkan

kepada kes yang melibatkan Jabatan Undang-undang. Pengerusi maklumkan

bahawa tidak semua proses kerja boleh didigitalkan. Walau bagaimanapun,

pihak LHDNM mengambil maklum perkara ini.

4. PENUTUP

4.1 Pengerusi mengucapkan ribuan terima kasih kepada semua yang hadir

kerana penglibatan dalam dialog ini. Beliau juga turut merakamkan

penghargaan kepada pihak persatuan yang telah memberikan input dan

maklum balas kepada LHDNM melalui sesi ini.

Mesyuarat ditamatkan pada jam 12 tengah hari.

MEMORANDUM ON COMPLIANCE AND OPERATIONAL ISSUES

23 January 2018

Prepared by: Compliance & Operations Working Group (COWG) Chartered Tax Institute of Malaysia

Memorandum on Compliance and Operational Issues

Page 2 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

Contents

Page No.

Systems Issues

1. Systems update 3

2. CP17SA(I)(STS) – Notification of Penalty Imposed for Underestimation of Tax Estimate

4

3. Section 107C(4)(a) of the ITA – Submission of Tax Estimate 5

Filing Issues

4. Appeal to Revise Tax Estimate in The Last Month of The Basis Period 6

5. Filing of tax return based on audited accounts 7

6. Form C 2017 – Set-off of Withholding Tax Deducted under the S.107A(1)(a) 8

7. Closing of Companies 9

8. Form E 11

Expatriate Issues

9. Verification of passport for individual leaver – To determine tax residence status 12

Payment Issues

10. Mode of payment for withholding tax 13

Other Issues

11. Late Receipt of Correspondences 14

12. Item XVII – Carry on e-Trading business (Form e-C YA 2016 / YA 2017) 15

13. Application for Certificate of Residence (CoR) for Labuan companies 16

Appendix 17

Memorandum on Compliance and Operational Issues

Page 3 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

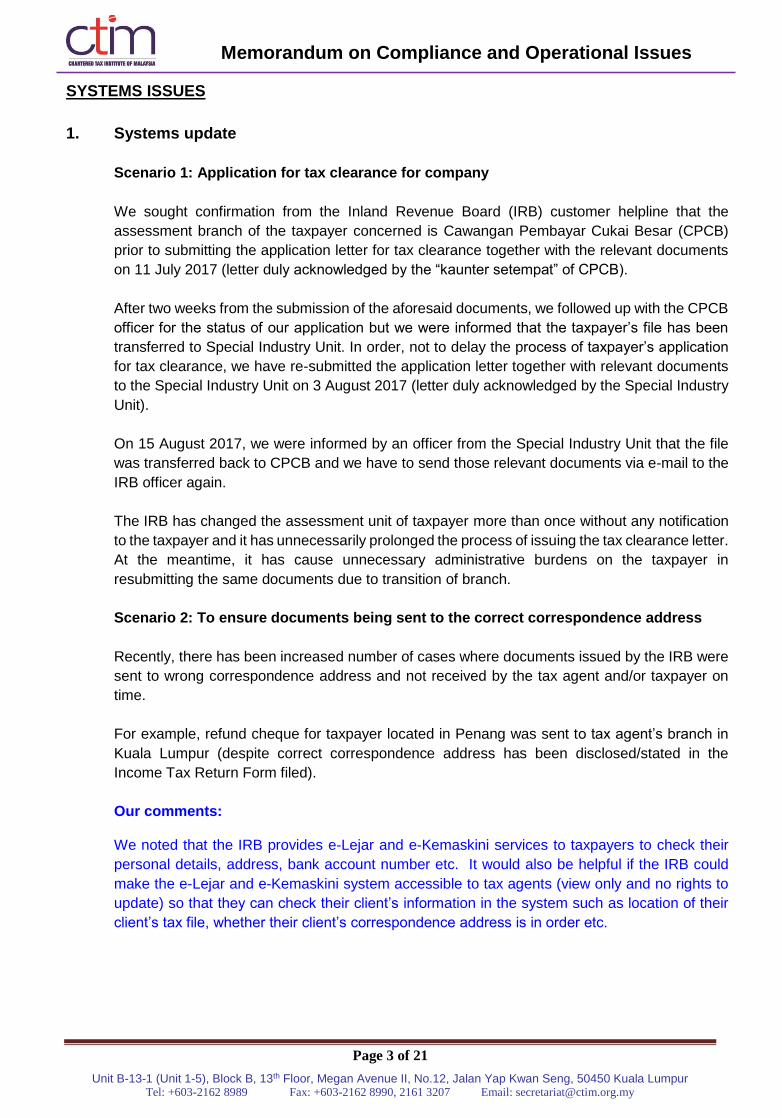

SYSTEMS ISSUES

1. Systems update

Scenario 1: Application for tax clearance for company

We sought confirmation from the Inland Revenue Board (IRB) customer helpline that the

assessment branch of the taxpayer concerned is Cawangan Pembayar Cukai Besar (CPCB)

prior to submitting the application letter for tax clearance together with the relevant documents

on 11 July 2017 (letter duly acknowledged by the “kaunter setempat” of CPCB).

After two weeks from the submission of the aforesaid documents, we followed up with the CPCB

officer for the status of our application but we were informed that the taxpayer’s file has been

transferred to Special Industry Unit. In order, not to delay the process of taxpayer’s application

for tax clearance, we have re-submitted the application letter together with relevant documents

to the Special Industry Unit on 3 August 2017 (letter duly acknowledged by the Special Industry

Unit).

On 15 August 2017, we were informed by an officer from the Special Industry Unit that the file

was transferred back to CPCB and we have to send those relevant documents via e-mail to the

IRB officer again.

The IRB has changed the assessment unit of taxpayer more than once without any notification

to the taxpayer and it has unnecessarily prolonged the process of issuing the tax clearance letter.

At the meantime, it has cause unnecessary administrative burdens on the taxpayer in

resubmitting the same documents due to transition of branch.

Scenario 2: To ensure documents being sent to the correct correspondence address

Recently, there has been increased number of cases where documents issued by the IRB were

sent to wrong correspondence address and not received by the tax agent and/or taxpayer on

time.

For example, refund cheque for taxpayer located in Penang was sent to tax agent’s branch in

Kuala Lumpur (despite correct correspondence address has been disclosed/stated in the

Income Tax Return Form filed).

Our comments: We noted that the IRB provides e-Lejar and e-Kemaskini services to taxpayers to check their

personal details, address, bank account number etc. It would also be helpful if the IRB could

make the e-Lejar and e-Kemaskini system accessible to tax agents (view only and no rights to

update) so that they can check their client’s information in the system such as location of their

client’s tax file, whether their client’s correspondence address is in order etc.

Memorandum on Compliance and Operational Issues

Page 4 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

Maklum balas LHDNM

Senario 1

Perkara tersebut diambil maklum dan pihak Persatuan dinasihatkan agar mengemukakan

nama dan no. cukai pendapatan syarikat berkenaan untuk semakan LHDNM.

Maklumat telah dikemukakan oleh CTIM. Emel Peringatan telah dikeluarkan kepada

cawangan berkenaan supaya perkara ini tidak berulang kerana LHDNM telah menerapkan

prinsip ‘No Wrong Door Policy’.

Senario 2

Sistem e-Lejar dan e-Kemaskini hanya boleh di akses oleh pembayar cukai sahaja kerana

melibatkan isu integriti dan keselamatan data.

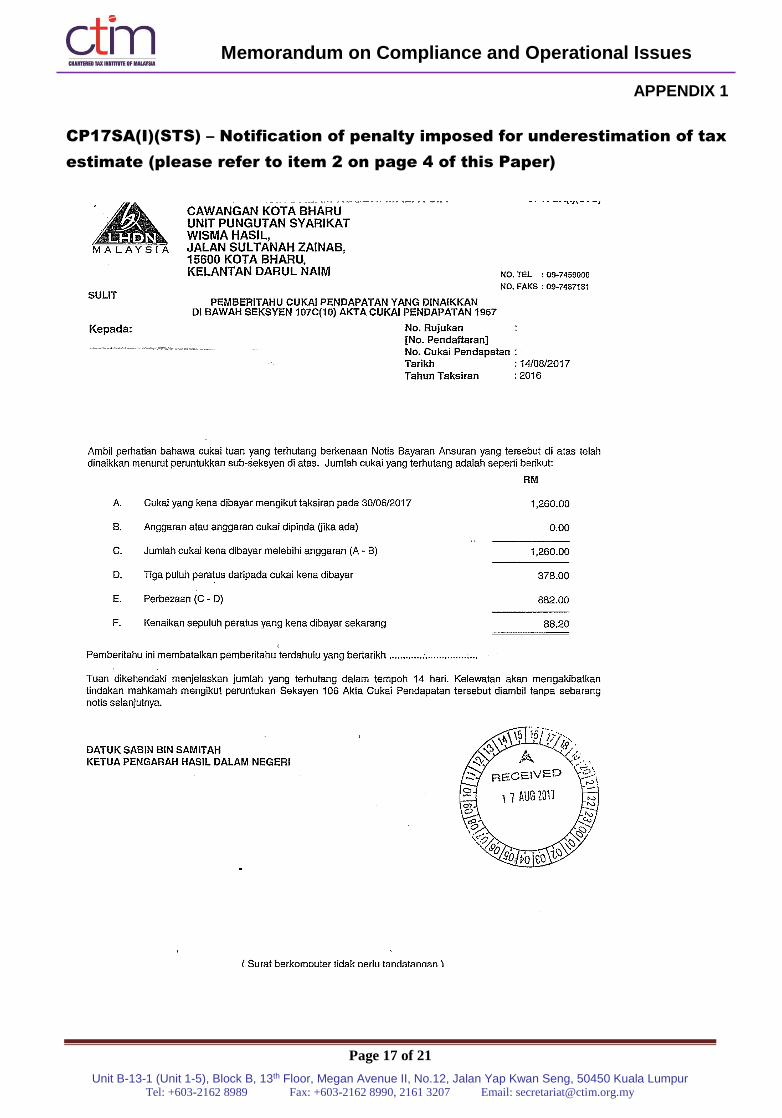

2. CP17SA(I)(STS) – Notification of penalty imposed for underestimation of tax

estimate

Taxpayer’s accounting year end is 31 October 2016 and submitted its tax return by the extended

filing deadline of 30 June 2017 granted by the IRB. Taxpayer has also settled the payment of

the penalty for underestimation of tax estimate under Section 107C(10) on 30 June 2017.

Despite the payment of penalty made on 30 June 2017, the notification on penalty imposed for

underestimation of tax estimate dated 14 August 2017 was issued by the IRB. [Please refer to

Appendix 1].

Our comments:

a. We would like know whether the above-mentioned notification is automatically generated by

the IRB’s system because it has created an unnecessary burden to taxpayers in terms of

administrative work.

b. We would like to propose the following for the IRB’s consideration:

i. Look into the IRB’s system to ensure that it links the collection of taxes with the

generation of notifications so that it does not generate a notification to impose penalties

once tax payments have been received on time.

ii. Send the notification to taxpayers who have outstanding tax balances only.

iii. Provide an updated summary of tax position to the taxpayer together with the notification.

Maklum balas LHDNM

Makluman CP17SA(I)(STS) akan ditambah baik dengan tambahan ayat “Sekiranya bayaran

telah dijelaskan, sila abaikan notis ini”.

Pengerusi minta pihak CTIM mengemukakan statistik kekerapan berkenaan perkara ini untuk

memastikan ianya bukanlah kes terpencil dan aduan yang dibangkitkan adalah berasas.

Memorandum on Compliance and Operational Issues

Page 5 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

3. Section 107C(4)(a) of the ITA – Submission of tax estimate

Pursuant to Section 107C(4)(a) –

Where a company, other than a company to which subsection (4A) applies, limited

liability partnership, trust body or co-operative society first commences operation in a

year of assessment and the basis period for that year is not less than six months –

(a) the estimate of its tax payable for that year of assessment shall be made in the

prescribed form and furnished to the Director General within three months from the

date of commencement of operations; and

By virtue of Section 107C(4)(a), where a company first commences operation in a year of

assessment (YA) and the basis period for that year is less than six months, the company is not

statutorily required to furnish any estimate of its tax payable for that YA.

There is a case where the taxpayer’s basis period for its first YA upon commencement of

operation is less than six months, the taxpayer received a notification from the IRB for non-

submission of its tax estimate for that YA and penalty was imposed pursuant to Section

107C(10).

In the same notification, the taxpayer who had settled its balance of tax for the same YA within

the statutory due date was imposed with a late payment penalty under Section 103.

Upon appeal, both the above penalty imposed under Section 103 and Section 107C(10) were

waived by the IRB.

Our comments:

We would request the IRB to look into ways to improve the IRB’s system so that it does not

generate such notifications. Perhaps the IRB may also want consider any steps that they would

like the taxpayer to take to avoid the above-mentioned issue from arising.

Maklum balas LHDNM

Pengeluaran notis kenaikan Seksyen 107C (10) tidak akan dikeluarkan kerana DG Direct CP205

tidak dikeluarkan bagi syarikat yang baru beroperasi.

Pengenaan kenaikan di bawah Seksyen 103 akan dikenakan bagi kes yang ada baki cukai atau

dibayar diluar tempoh. Sekiranya pembayar cukai menerima notis kenaikan kemungkinan

berlaku salah pembukuan bayaran atau kesilapan kod bayaran. Dalam keadaan ini, pembayar

cukai perlu mengemukakan rayuan kepada cawangan berkaitan untuk tujuan remit kenaikan.

Memorandum on Compliance and Operational Issues

Page 6 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

FILING ISSUES

4. Appeal to revise tax estimate in the last month of the basis period

The taxpayer changed its accounting year end from 30 March to 31 December in 2016. The

taxpayer submitted an appeal to revise its estimate of tax payable (ETP) for YA 2016 in

December 2016 (i.e. last month of its basis period).

The IRB responded that they will not consider the taxpayer’s appeal in the last month of the

basis period for YA 2016 on the grounds that taxpayer had revised its ETP for YA 2016 three

times. Prior to the appeal to revise its ETP in the last month of the basis period for YA 2016, the

taxpayer had submitted three forms:

1st – CP 204A for 6th month revision in Sep 2015 (before change of accounting period)

2nd – CP 204B upon change of accounting period in Nov 2015

3rd – CP 204A for 9th month revision in Dec 2015

The taxpayer was informed by the IRB that it is the IRB’s internal policy to allow a company to

revise its ETP up to three times only and the IRB’s system can only cater for a maximum of three

revisions.

Our comments:

In our view, the CP204B is a notification of change in accounting period and not a notification of

revised ETP. Kindly confirm that our understanding is correct.

Maklum balas LHDNM

Tiada sebarang peruntukan dinyatakan di dalam Akta Cukai Pendapatan (ACP) 1967 atau

arahan dalaman berhubung pindaan anggaran cukai dihadkan sebanyak 3 kali sahaja.

Pindaan anggaran cukai yang dibenarkan menurut ACP 1967 ialah di bawah Seksyen 107C(7)

iaitu pindaan yang dibuat dalam bulan ke-6 atau ke-9 atau dalam kedua-dua bulan dalam

tempoh asas bagi sesuatu tahun taksiran.

Bagi pindaan selain dari yang diperuntukkan di bawah Seksyen 107C(7), pemprosesan dan

kelulusan adalah tertakluk kepada budibicara LHDNM.

Sebagai makluman, CP204B adalah borang yang digunakan oleh pembayar cukai untuk

memaklumkan pertukaran tempoh perakaunan dan bukan borang untuk membuat pindaan

anggaran cukai.

Memorandum on Compliance and Operational Issues

Page 7 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

5. Filing of tax return based on audited accounts

Section 267(2) of the Companies Act 2016 gives the power to the Registrar to exempt any private

company from the requirement to appoint an auditor. Subsequently, CCM had issued Practice

Directive No. 3/2017 entitled “Qualifying Criteria for Audit Exemption for Certain Categories of

Private Companies”.

Our comments:

We refer to the IRB Tax Policy Department’s announcement in March 2014 as follows:

“If there are provisions in the CA 1965 which state that a company is not required to submit

audited accounts to the CCM, then S77A(4) does not apply to that company. However, the

company must submit its income tax return based on information in the final accounts.”

a. In view of the above announcement, we would like to seek the IRB’s confirmation that a

company is not required to submit its income tax return based on audited accounts (instead

it will be based on final accounts) under the following circumstances:

i. Where Section 267(2) of the Companies Act 2016 applies.

ii. Where Practice Directive No. 3/2017 entitled “Qualifying Criteria for Audit Exemption for

Certain Categories of Private Companies” applies.

iii. Where any other provisions in the Companies Act 2016 exempt that company from

appointing an auditor or submitting audited accounts to the CCM.

b. We would like to request the IRB to insert the categories of companies which are not required

to file income tax returns based on audited accounts (instead it will be based on final

accounts) in the annual Filing Programme.

Maklum balas LHDNM

Kewajiban atau pengecualian sesebuah syarikat untuk menyediakan akaun beraudit adalah di

kawal selia oleh Suruhanjaya Syarikat Malaysia (SSM) yang dikuatkuasakan di bawah

peruntukan Akta Syarikat 2016.

Sehubungan itu, LHDNM berpendirian bahawa sekiranya tiada pengecualian diberi kepada

sesebuah syarikat untuk menyediakan akaun beraudit maka syarikat tersebut hendaklah

mengemukakan Borang Nyata Cukai Pendapatan berdasarkan akaun beraudit seperti mana di

bawah subseksyen 77A(4) ACP 1967.

Oleh kerana peruntukan sedia ada mencukupi untuk tujuan ini, maka tiada keperluan untuk

LHDNM menyenaraikan mana-mana kategori syarikat yang mengemukakan BNCP tanpa akaun

beraudit.

Makluman tambahan: Sekiranya sesebuah syarikat dikecualikan dalam penyediaan akaun

beraudit berdasarkan ketetapan SSM, syarikat dalam kategori ini hanya perlu mengemukakan

Penyata Akaun Muktamad (Final Accounts) kepada LHDNM.

Memorandum on Compliance and Operational Issues

Page 8 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

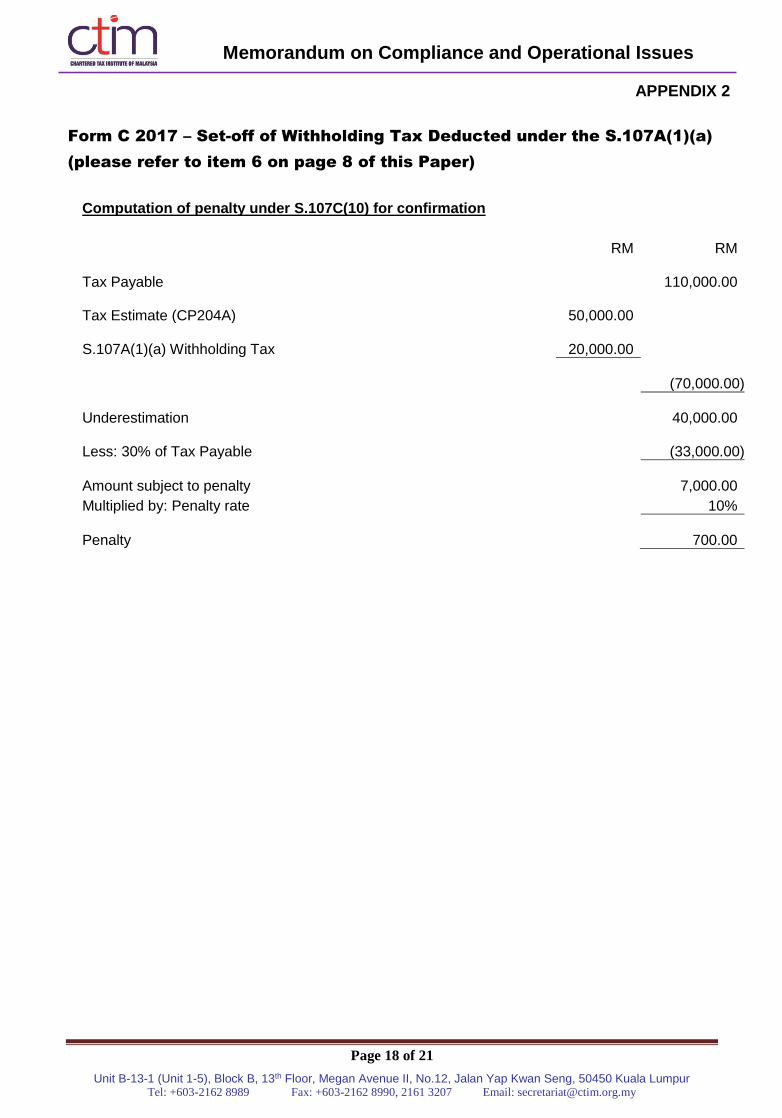

6. Form C 2017 – Set-off of Withholding Tax Deducted under the S.107A(1)(a)

A space (Item C2B) has been included in the Form C for the year of assessment 2017 to allow

the withholding tax (WHT) deducted under S.107A(1)(a) to be filled in to set-off against the tax

payable.

Our comments:

In view of the above, we would request for the IRB’s consideration to be given on the following

matters:

a. Amendment of the relevant provisions in the Income Tax Act 1967, in particular S.110, to be

in line with the Form C (i.e. the set-off of WHT against tax payable);

b. Confirmation that the IRB’s system would compute the penalty under S.107C(10) as set-out

in the attached Appendix 2;

c. Amendment of S.107C(10) in respect of a non-resident company, so that the WHT deducted

from its income under S.107A(1)(a) and/or S.109B is included together with its estimate of

tax payable for comparison with its actual tax payable to determine whether it has an

underestimation of tax payable; and

d. Amendment of S.107C(3) and S.107C(7) to reflect the practice that the estimate of tax

payable is not required to be filled in the Form CP204/CP204A for a non-resident company

if its income is fully subjected to WHT under S.107A.

Maklum balas LHDNM

Cadangan diambil maklum.

Memorandum on Compliance and Operational Issues

Page 9 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

7. Closing of Companies

a. We refer to an extract of the IRB’s response in item 5 (Closing of Companies) on page 18 of

the Minutes of the Working Group Meeting between the IRB and the Professional Bodies -

DESIRE Dialogue No.1 /2017 held on 20 June 2017 as follows:

“Syarikat tidak perlu mengemukakan BNCP hanya sekiranya ia dibubarkan sepenuhnya

dan fail cukai dimatikan oleh LHDNM”

Our comments:

Based on the above feedback from the IRB, the Form C needs to be submitted until the tax

file is closed by the IRB. So even if the company has received the final strike off notice from

the Registrar of Companies, we understand that the Form C for the subsequent YAs still

need to be submitted.

Clarification is sought on whether the following fields in the Form C (to be submitted for the

subsequent YAs after the final strike off notice has been received from the Registrar of

Companies) can be left blank since the company no longer exists as a result of the final strike

off:

i. Basis Period and Accounting Period

ii. Business Address

iii. Directors' details

iv. Shareholder details

Maklum balas LHDNM

a) Semua maklumat berkenaan perlu di isi dalam BNCP.

b. We refer to an extract of item 34 (Confirmation / clarification sought in relation to a company

which is winding up) on page 31 of the Minutes of the Working Group Meeting between the

IRB and the Professional Bodies - DESIRE Dialogue No. 1/2016 held on 19 May 2016 as

follows:

“It is stated in the LHDNM’s Filing Programme for ITRF in the year 2015 that companies,

limited liability partnerships, trust bodies and co-operative societies which have not

commenced operation need not furnish Form CP204. Where a company is winding up

its operations, it would be difficult to determine the estimate of its tax payable for the

purposes of S.107C of the ITA 1967 e.g. after the deadline for the ninth month revision

of the estimate, the company which did not have any income, may suddenly receive bad

debts recovered or income from sale of stock/scrap (these examples are not exhaustive).

Our comments:

Please clarify whether the company is required to comply with the provisions of S.107C

of the ITA 1967 for the YA in which the winding up commences and the subsequent YAs.

Memorandum on Compliance and Operational Issues

Page 10 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

Jawapan LHDNM:

Secara am, syarikat yang dalam penggulungan, akan ada liquidator yang mengendalikan

syarikat. Liquidator akan menjual semua aset syarikat di mana penerimaan wang akan

agihkan kepada penerima/pemiutang mengikut senarai keutamaan. Bagi kes ini di mana

jika ada hasil jualan stok/skrap atau hutang lapok pulih, perincian kes hendaklah

dikemukakan untuk penelitian lanjut pihak LHDNM.

Sekiranya pendapatan yang diterima tersebut daripada faedah simpanan tetap atau

penerimaan sewa, ia boleh dikenakan cukai dan pembayar cukai perlu meminda CP204.

Oleh itu, syarikat dalam proses penggulungan masih perlu mengemukakan anggaran

cukai.

Pihak persatuan mengambil maklum dan memahami jawapan LHDNM.”

Our comments:

i. Based on the feedback from the IRB as set-out in items 7(a) and 7(b) above, we

understand that the Form CP204 needs to be submitted until the tax file is closed by the

IRB. Kindly confirm.

ii. Clarification is sought on how the accounting period and the basis period should be filled

up in the Form CP204 when the company no longer exists as a result of the final strike

off by the Registrar of Companies.

Maklum balas LHDNM

b) Mana-mana syarikat dalam penggulungan atau dibubarkan perlu menghantar akaun

setiap 6 bulan. Oleh itu, tempoh asas yang perlu di isi dalam CP 204 adalah seperti mana

biasa pengisian Borang C sehingga tarikh syarikat berkenaan tidak menerima apa-apa

pendapatan dan Surat Penyelesaian Cukai telah dikeluarkan oleh LHDNM.

Nota: Ketetapan Umum No. 7/2016 – Tempoh Asas bagi Syarikat Dalam Pembubaran

berkaitan. Pemakluman pertukaran tempoh asas disebabkan penggulungan /

pembubaran adalah sama seperti mana pengenalan peruntukan subseksyen 21(3A),

seksyen 107C (11B) dan 112(3A) ACP 1967 yang berkuatkuasa mulai Tahun Taksiran

2019 dan perenggan 120(1)(i) yang berkuatkuasa mulai 31.12.2017.

Memorandum on Compliance and Operational Issues

Page 11 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

8. Form E

We are now required to fill in all workers’ details in the Form E starting from YA 2016.

Kindly clarify what is the scope of the workers whose details are to be stated in the Form E?

Does it include contract workers, part time workers, foreign workers, or even foreign workers in

which their permits belong to another company?

Our comments:

We would like to request the IRB to provide the above clarification in the explanatory notes of

the Form E.

Maklum balas LHDNM

Pekerja yang dimaksudkan dalam Borang E adalah seperti takrifan dalam seksyen 2 Akta Cukai

Pendapatan 1967 bagi ‘pekerja’, ‘majikan’ dan ‘penggajian’ yang mana saraan dibayar, tidak

kira sama ada pekerja itu adalah pekerja kontrak / sambilan, pekerja asing ataupun pekerja

asing yang mana permit mereka dipegang oleh syarikat lain.

Memorandum on Compliance and Operational Issues

Page 12 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

EXPATRIATE ISSUES

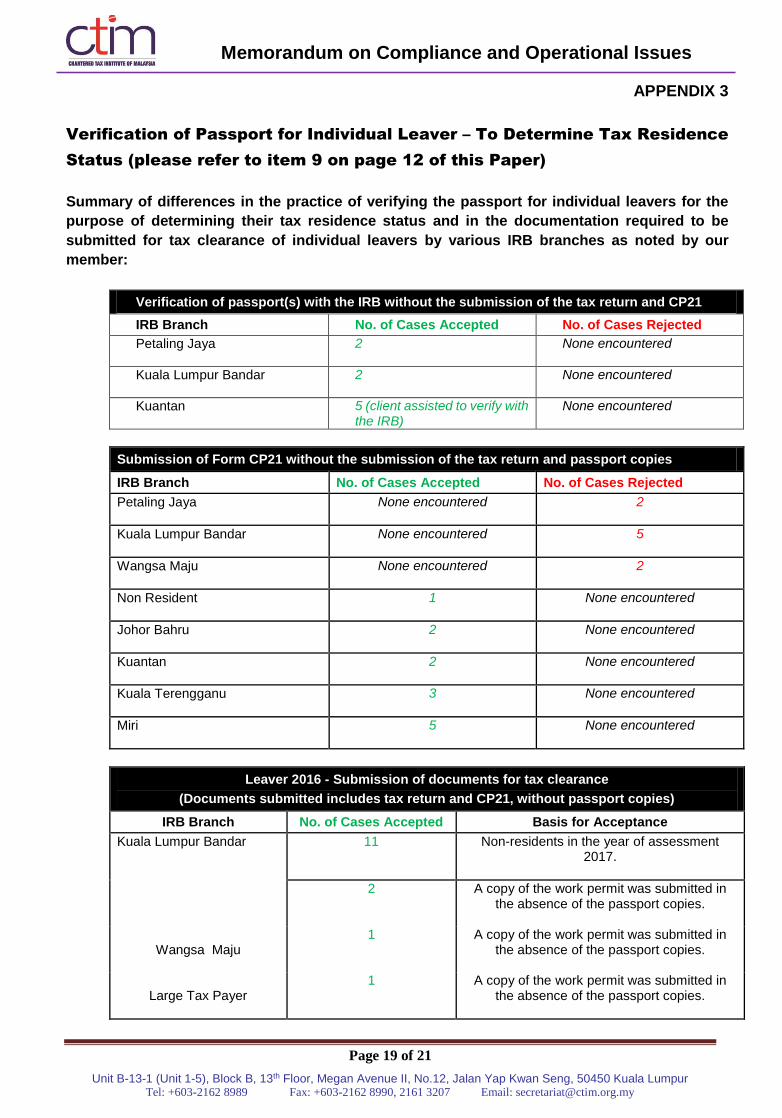

9. Verification of passport for individual leaver – To determine tax residence status

It is noted that there have been differences among the IRB branches in the practice of verifying

the passport for individual leavers for the purpose of determining their tax residence status and

in the documentation required to be submitted for tax clearance of individual leavers as

summarised in Appendix 3.

Our comments:

We would like to request the IRB to include the requirements for passport verification and

certification and the documentation required to be submitted to the IRB for tax clearance of

individual leavers in the LHDNM Operational Guidelines No.2/2016 on Application Procedure

For Individual Tax Settlement Letter (SPC). This would facilitate the standardising of the

documentation required to be submitted for applications for tax clearance of individual leavers.

Maklum balas LHDNM

LHDNM mengambil maklum cadangan pihak Persatuan.

Memorandum on Compliance and Operational Issues

Page 13 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

PAYMENT ISSUES

10. Mode of payment for WHT

Currently, the payment for WHT can be made only by post or at the payment counters as stated

in the WHT Forms from the IRB’s website.

Telegraphic transfer is only available for “urgent payment” where the payer may send the Forms

CP 37A/ CP 37/ CP 37D together with the payment, copy of invoice and remittance slip

(telegraphic transfer) directly to:

Director

Non-Resident Branch

Withholding Tax Unit

7th Floor, Block 8

Government Office Complex

Our comments:

We understand that the facility for e-payment of WHT is only available for WHT paid under

S.107A contract payment (CP37A). We would like to know when the IRB will be implementing

the e-payment facilities for the other categories of WHT payments.

Maklum balas LHDNM

The e-payment facilities for other than S.107A contract payment is still at development stage.

Memorandum on Compliance and Operational Issues

Page 14 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

OTHER ISSUES

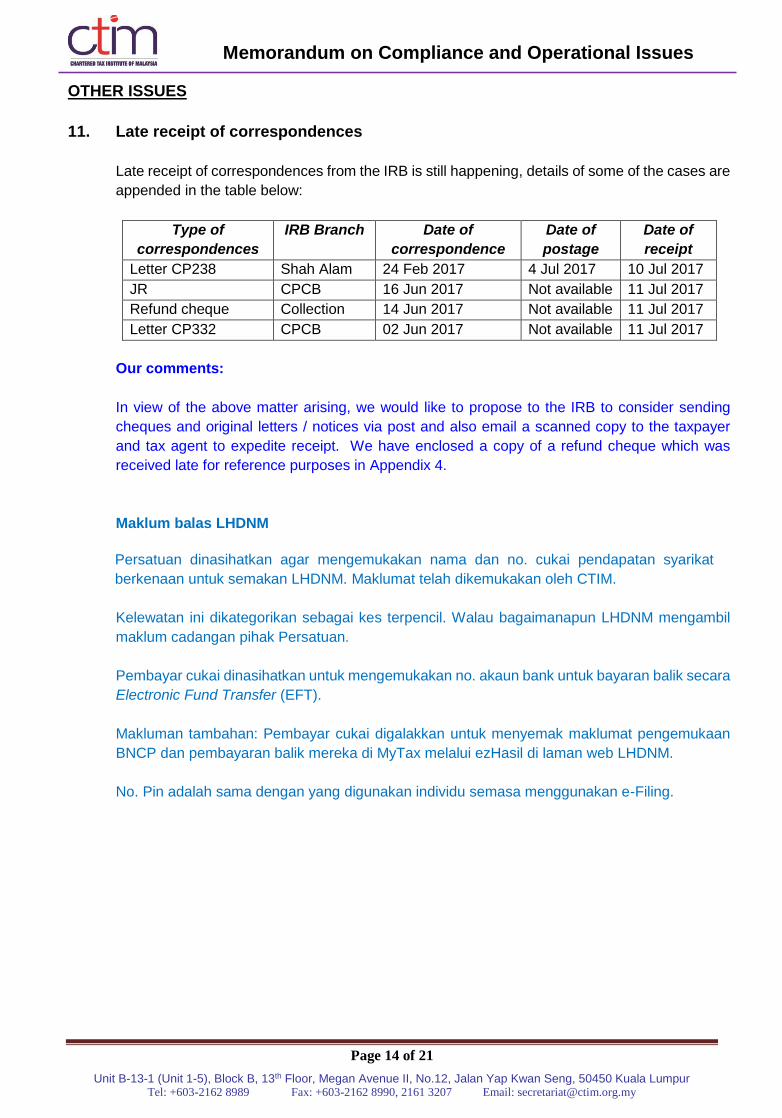

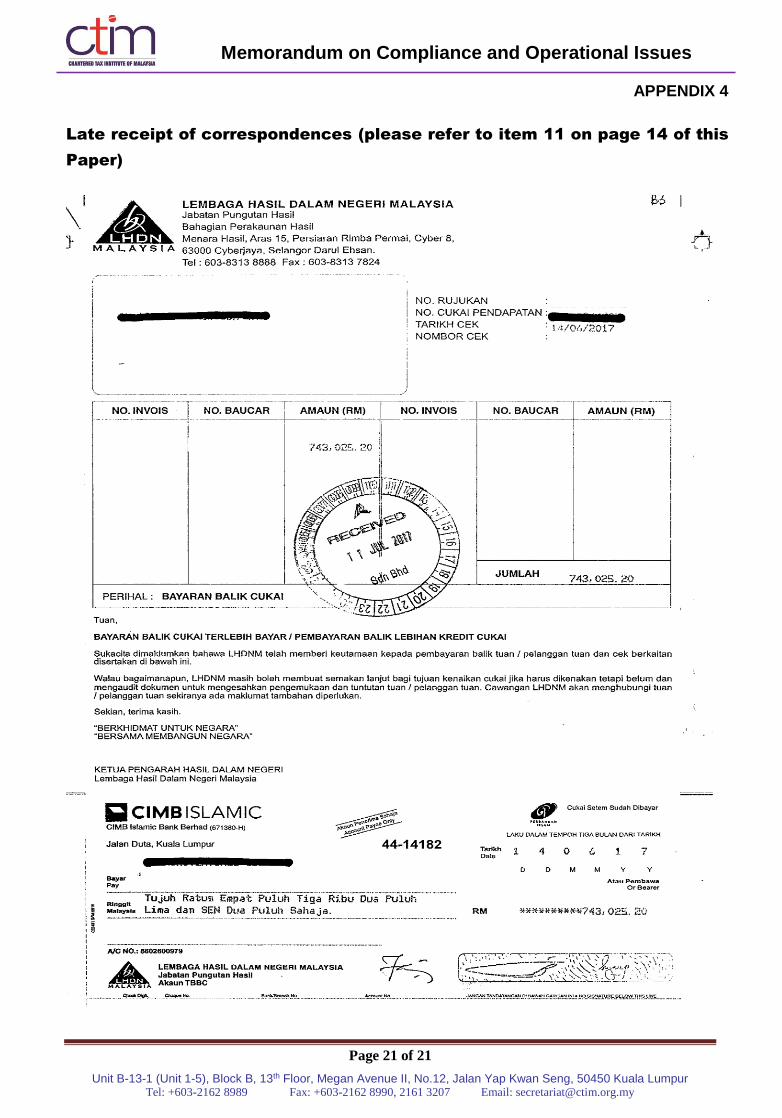

11. Late receipt of correspondences

Late receipt of correspondences from the IRB is still happening, details of some of the cases are

appended in the table below:

Type of

correspondences

IRB Branch Date of

correspondence

Date of

postage

Date of

receipt

Letter CP238 Shah Alam 24 Feb 2017 4 Jul 2017 10 Jul 2017

JR CPCB 16 Jun 2017 Not available 11 Jul 2017

Refund cheque Collection 14 Jun 2017 Not available 11 Jul 2017

Letter CP332 CPCB 02 Jun 2017 Not available 11 Jul 2017

Our comments:

In view of the above matter arising, we would like to propose to the IRB to consider sending

cheques and original letters / notices via post and also email a scanned copy to the taxpayer

and tax agent to expedite receipt. We have enclosed a copy of a refund cheque which was

received late for reference purposes in Appendix 4.

Maklum balas LHDNM

Persatuan dinasihatkan agar mengemukakan nama dan no. cukai pendapatan syarikat

berkenaan untuk semakan LHDNM. Maklumat telah dikemukakan oleh CTIM.

Kelewatan ini dikategorikan sebagai kes terpencil. Walau bagaimanapun LHDNM mengambil

maklum cadangan pihak Persatuan.

Pembayar cukai dinasihatkan untuk mengemukakan no. akaun bank untuk bayaran balik secara

Electronic Fund Transfer (EFT).

Makluman tambahan: Pembayar cukai digalakkan untuk menyemak maklumat pengemukaan

BNCP dan pembayaran balik mereka di MyTax melalui ezHasil di laman web LHDNM.

No. Pin adalah sama dengan yang digunakan individu semasa menggunakan e-Filing.

Memorandum on Compliance and Operational Issues

Page 15 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

12. Item XVII – Carry on e-Commerce business (Form e-C YA 2016 / YA 2017)

Based on the Form e-C guide book, a Company is considered to carry on e-Commerce business

if in deriving its income, the company uses internet for:

i) receiving orders for goods or services.

Example:

The company receives orders via e-mail, website or social media, and not by

conventional post, telephone or facsimile.

ii) receiving payment in respect of good or services.

Example:

The company receives digital cash payment from credit card or charge card via e-mail or

website, and not by conventional post, telephone or facsimile.

iii) delivering goods or services.

Example:

- The company uses e-mail, internet or file transfer protocol to deliver digitized music,

articles or software instead of the conventional method of delivering software on disk.

- The company uses both e-mail and website to offer its advice and receives payment

for the advice.

- The company advertises the goods or services of other entities on internet for a fee.

- The company hosts the website(s).

- The company renders service in providing access to internet.

Our comments:

1) In view that the income tax treatment for offline / conventional businesses is the same, we

would like to enquire on the rationale for ticking the box for carrying on an e-Commerce

business in the tax return.

2) Based on the examples above, companies that receive orders via e-mail or use e-mail to

deliver articles would be considered as carrying on an e-Commerce business. In this digital

era, it is very common to use e-mail as a mode of communication. In the case of the above

examples, many companies may fall within the scope of carrying on an e-Commerce

business as long as the companies use e-mail even though they do not actually carry on an

e-Commerce business. Would such companies that do not carry on an e-Commerce

business but fall within the scope of online business be penalised for not ticking the box for

carrying on an e-Commerce business in the tax return?

Memorandum on Compliance and Operational Issues

Page 16 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

Maklum balas LHDNM

1) Keperluan menandakan kotak jika menjalankan perniagaan atas talian adalah

bagi:

Membezakan pembayar cukai yang menjalankan perniagaan atas talian

dengan perniagaan secara konvensional.

Memastikan peniaga yang menjalankan perniagaan atas talian melaporkan

pendapatan perniagaan atas taliannya.

Mendapatkan statistik jumlah pembayar cukai yang menjalankan

perniagaan atas talian.

2) Kriteria perniagaan atas talian bukan hanya ditentukan dengan penggunaan emel

sahaja. Fakta dan kes perlu dilihat sebelum menentukan perniagaan itu

dikategorikan sebagai perniagaan atas talian. Jika syarikat tidak menjalankan

perniagaan atas talian dan menggunakan emel sebagai medium perantaraan,

tidak menjadi kesalahan jika kotak menjalankan perniagaan atas talian tidak

ditanda.

13. Application for Certificate of Residence (CoR) for Labuan companies

A CoR is issued by the IRB to confirm the tax residence status of a taxpayer and enables the

Malaysian tax resident to claim tax benefits from the Double Tax Agreement (DTA). For Labuan

companies, it will be handled by Labuan Branch. Recently, it has been noted that the IRB

Labuan Branch no longer issues the CoR for the Labuan companies.

Our comments:

In view that the IRB Labuan Branch no longer issues the CoR for the Labuan companies, kindly

let us know where the applications for COR for Labuan companies can be submitted to.

Maklum balas LHDNM

Permohonan Sijil Taraf Mastautin perlu / boleh dikemukakan kepada Cawangan

Labuan.

Memorandum on Compliance and Operational Issues

Page 17 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

APPENDIX 1

CP17SA(I)(STS) – Notification of penalty imposed for underestimation of tax

estimate (please refer to item 2 on page 4 of this Paper)

Memorandum on Compliance and Operational Issues

Page 18 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

APPENDIX 2

Form C 2017 – Set-off of Withholding Tax Deducted under the S.107A(1)(a)

(please refer to item 6 on page 8 of this Paper)

Computation of penalty under S.107C(10) for confirmation

RM RM

Tax Payable

110,000.00

Tax Estimate (CP204A)

50,000.00

S.107A(1)(a) Withholding Tax

20,000.00

(70,000.00)

Underestimation

40,000.00

Less: 30% of Tax Payable

(33,000.00)

Amount subject to penalty

7,000.00

Multiplied by: Penalty rate 10%

Penalty

700.00

Memorandum on Compliance and Operational Issues

Page 19 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

APPENDIX 3

Verification of Passport for Individual Leaver – To Determine Tax Residence

Status (please refer to item 9 on page 12 of this Paper)

Summary of differences in the practice of verifying the passport for individual leavers for the

purpose of determining their tax residence status and in the documentation required to be

submitted for tax clearance of individual leavers by various IRB branches as noted by our

member:

Verification of passport(s) with the IRB without the submission of the tax return and CP21

IRB Branch No. of Cases Accepted No. of Cases Rejected

Petaling Jaya

2 None encountered

Kuala Lumpur Bandar

2 None encountered

Kuantan 5 (client assisted to verify with the IRB)

None encountered

Submission of Form CP21 without the submission of the tax return and passport copies

IRB Branch No. of Cases Accepted No. of Cases Rejected

Petaling Jaya

None encountered 2

Kuala Lumpur Bandar

None encountered 5

Wangsa Maju

None encountered 2

Non Resident 1

None encountered

Johor Bahru

2 None encountered

Kuantan

2 None encountered

Kuala Terengganu

3 None encountered

Miri

5 None encountered

Leaver 2016 - Submission of documents for tax clearance

(Documents submitted includes tax return and CP21, without passport copies)

IRB Branch No. of Cases Accepted Basis for Acceptance

Kuala Lumpur Bandar 11 Non-residents in the year of assessment 2017.

2 A copy of the work permit was submitted in the absence of the passport copies.

Wangsa Maju 1 A copy of the work permit was submitted in

the absence of the passport copies.

Large Tax Payer 1 A copy of the work permit was submitted in

the absence of the passport copies.

Memorandum on Compliance and Operational Issues

Page 20 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

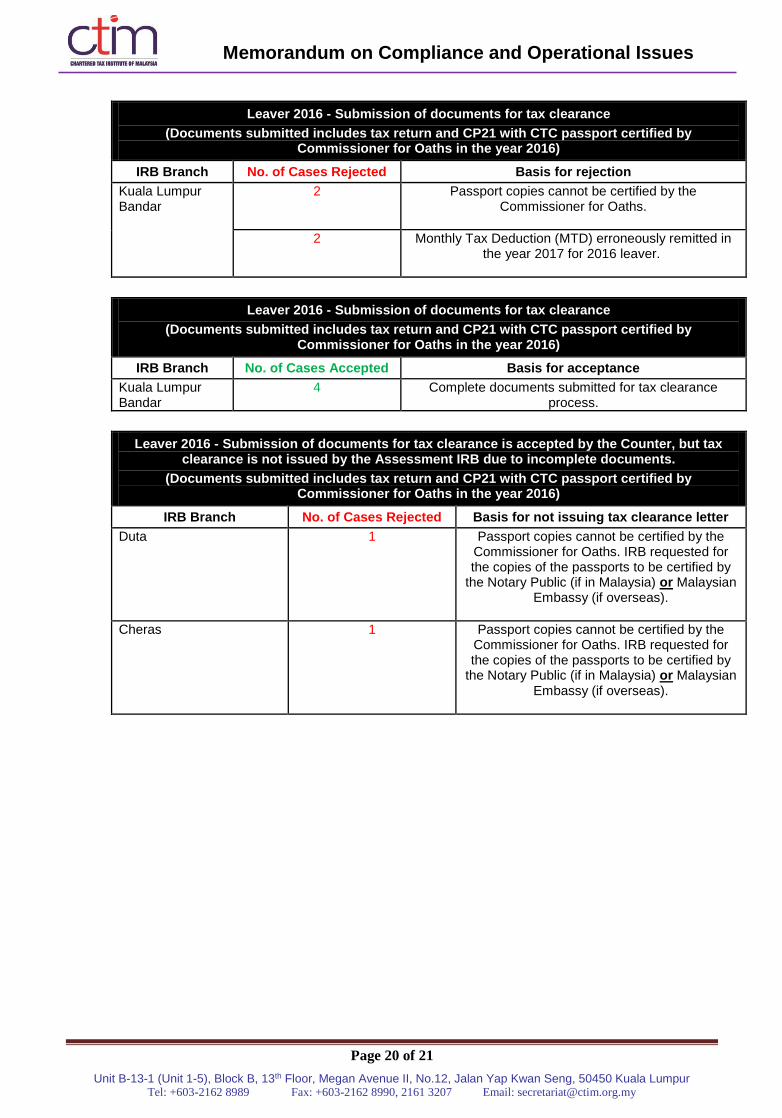

Leaver 2016 - Submission of documents for tax clearance

(Documents submitted includes tax return and CP21 with CTC passport certified by Commissioner for Oaths in the year 2016)

IRB Branch No. of Cases Rejected Basis for rejection

Kuala Lumpur Bandar

2

Passport copies cannot be certified by the Commissioner for Oaths.

2 Monthly Tax Deduction (MTD) erroneously remitted in the year 2017 for 2016 leaver.

Leaver 2016 - Submission of documents for tax clearance

(Documents submitted includes tax return and CP21 with CTC passport certified by Commissioner for Oaths in the year 2016)

IRB Branch No. of Cases Accepted Basis for acceptance

Kuala Lumpur Bandar

4

Complete documents submitted for tax clearance process.

Leaver 2016 - Submission of documents for tax clearance is accepted by the Counter, but tax clearance is not issued by the Assessment IRB due to incomplete documents.

(Documents submitted includes tax return and CP21 with CTC passport certified by Commissioner for Oaths in the year 2016)

IRB Branch No. of Cases Rejected Basis for not issuing tax clearance letter

Duta 1 Passport copies cannot be certified by the Commissioner for Oaths. IRB requested for the copies of the passports to be certified by

the Notary Public (if in Malaysia) or Malaysian Embassy (if overseas).

Cheras 1 Passport copies cannot be certified by the Commissioner for Oaths. IRB requested for the copies of the passports to be certified by

the Notary Public (if in Malaysia) or Malaysian Embassy (if overseas).

Memorandum on Compliance and Operational Issues

Page 21 of 21

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

APPENDIX 4

Late receipt of correspondences (please refer to item 11 on page 14 of this

Paper)

THE MALAYSIAN INSTITUTE OF CHARTERED

SECRETARIES AND ADMINISTRATORS

ISSUES FOR DISCUSSION AT DESIRE BILL 1/2018 DIALOGUE

Page 1

Issue 1

Is work permit fee paid by employer tax deductible?

Employer has been treating work permit fee paid on behalf of foreign general workers as employee's

perquisite since Year of Assessment (YA) 2013.

Question: Would LHDNM accept such treatment as tax deductible to employer?

Maklum balas LHDNM

Bayaran fi yang dilakukan oleh majikan dibenarkan potongan di bawah subseksyen 33(1) ACP

1967 kecuali bayaran fi dilakukan sebelum perniagaan bermula.

Issue 2

Are motorcar maintenance expenses tax deductible?

Under PR 3/2013, motorcar provided to employee inclusive of petrol, its benefit is to be assessed and

the Benefit In Kind has been declared in the employee's EA Form.

Question: LHDNM to confirm on whether motorcar maintenance expenses (such as road tax, insurance

and repairs & maintenance) are tax deductible to employer.

Maklum balas LHDNM Perbelanjaan penyenggaraan kenderaan dibenarkan potongan di bawah subseksyen 33(1)

ACP 1967 kepada majikan sekiranya majikan yang melakukan perbelanjaan ini.

Issue 3

Guideline on filing of Form Q

Certain LHDNM branches have been rejecting filing of Form Q due to non-compliance with certain

conditions such as to produce evidence of payment of the disputed tax and the tax payable figures, and

at times, officer was not available to accept the Form Q.

Question: Suggest LHDNM to provide a clearer guideline to complete and file the Form Q, pursuant to

Section 99 of the Income Tax Act 1967 (ITA) in order to expedite the appeal process.

Maklum balas LHDNM Syarat-syarat dan panduan yang ditetapkan bagi maklumat yang diperlukan semasa

pengisian rayuan Borang Q telah dinyatakan dengan jelas dalam perenggan 6 dan 7

Ketetapan Umum 12/2017.

THE MALAYSIAN INSTITUTE OF CHARTERED

SECRETARIES AND ADMINISTRATORS

ISSUES FOR DISCUSSION AT DESIRE BILL 1/2018 DIALOGUE

Page 2

Issue 4

Clarification on filing of 2017 Form C with regard to Bahagian P1

a) Under “Status Syarikat” on Page 8 of the 2016 and 2017 Form C (referred to as Bahagian P1 in

the Contoh Borang Nyata Syarikat Tahun Taksiran 2016 and 2017), 15 options were listed ranging

from MSC, Awam, Bio Nexus, Harta Tanah to Lain-lain (nyatakan).

b) “Sdn. Bhd.” is not specifically listed in the 15 options.

c) Normally, where a “Sdn. Bhd.” is involved, the option “Lain-lain” is selected.

d) Up to YA2016, when “Lain-lain” is chosen, no further elaboration is needed.

e) However, with effect from YA2017, if the “Lain-lain” option is chosen, we are required to

elaborate further under “Nyatakan”.

f) Some practitioners are of the view that the principal activity should be stated. But this information

would have already been disclosed on Page 5 in Bahagian L1A under the heading “Maklumat

Kewangan Syarikat (Perniagaan Utama)” of the Form C.

g) While others are of the view that since “Sdn. Bhd.” is not listed, we should state “Sdn. Bhd.”, if

that is applicable.

h) What if a company is limited by guarantee, and is set up for educational purposes, should we state

the company as limited by guarantee or for educational purposes under “Lain-lain”?

i) We could not find any guidance from the “Buku Panduan 2017”.

Maklum balas LHDNM

Dalam Buku Panduan C 2017 terdapat empat belas jenis status (tidak termasuk ‘Lain-lain’)

yang diberikan di ruangan P1 Borang C adalah contoh.

Secara umumnya, status untuk pengisian di ruangan P1 merujuk kepada bidang perniagaan

/ aktiviti syarikat pelapor di ruangan I Borang C, manakala ‘Maklumat Kewangan Syarikat’

merujuk kepada perniagaan utama yang mungkin adalah salah satu daripada beberapa

perniagaan syarikat pelapor.

‘Sdn. Bhd.’ atau ‘Bhd’ merujuk kepada jenis syarikat yang mana maklumat tersebut boleh

diketahui daripada nama syarikat di ruangan I Borang C, dan oleh itu tidak perlu ada pilihan

‘Sdn Bhd’ dan ‘Bhd’ di ruangan P1.

Bagi syarikat berhad menurut jaminan yang ditubuhkan bagi tujuan pendidikan, syarikat boleh

mengisi ‘Pendidikan’ dalam petak untuk ‘Lain-lain’ di ruangan P1.

THE MALAYSIAN INSTITUTE OF CHARTERED

SECRETARIES AND ADMINISTRATORS

ISSUES FOR DISCUSSION AT DESIRE BILL 1/2018 DIALOGUE

Page 3

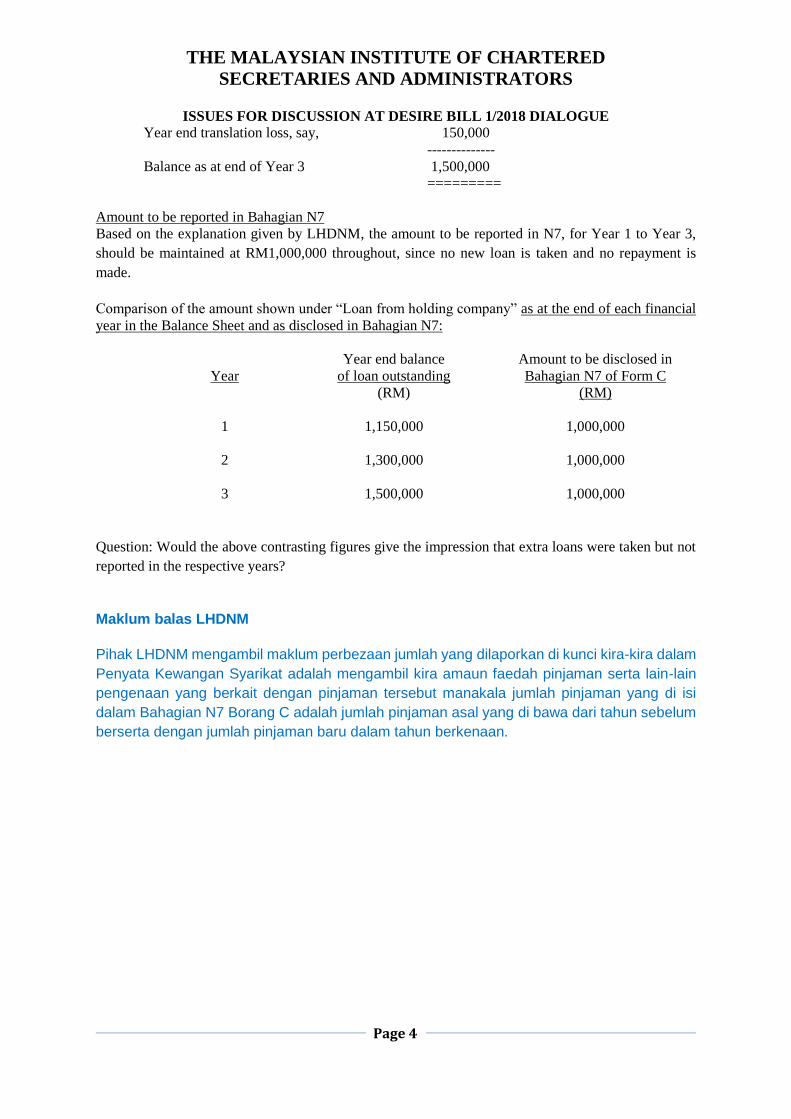

Issue 5

Loans to / from related companies

(Bahagian N7 – N10 TT 2017 Borang C)

In Para 4 of the minutes of the DESIRE Dialogue Bil. 1/2017 dated 20 June 2017, LHDNM confirmed

that the amount of loan to be reported in N7 (Loans to related companies in Malaysia), is the balance

of the loan brought forward, plus any new loan granted during the current year.

Repayment of loan during the current year is to be ignored.

Question: Clarification on the following scenario:

M Co. (Malaysia incorporated subsidiary company of S Co.) and S Co. (Singapore incorporated holding

company of M Co.). M Co. took a loan of SGD350,000 from S Co. which is equivalent to RM1,000,000

at an interest rate of 5% per annum, with no fixed term of repayment. No repayment was made for the

past 3 years. M Co. has suffered year end translation loss for the 3 consecutive years. The position in

the Balance Sheet for each of the 3 years is depicted below:-

a) Year 1 RM

Loan Principal 1,000,000

Add : Accrued interest 50,000

--------------

1,050,000

Year end translation loss, say, 100,000

--------------

Balance as at end of Year 1 1,150,000

=========

b) Year 2 RM

Balance b/f from Year 1 1,150,000

Add : Accrued interest 50,000

--------------

1,200,000

Year end translation loss, say, 100,000

--------------

Balance as at end of Year 2 1,300,000

=========

c) Year 3 RM

Balance b/f from Year 2 1,300,000

Add : Accrued interest 50,000

--------------

1,350,000

THE MALAYSIAN INSTITUTE OF CHARTERED

SECRETARIES AND ADMINISTRATORS

ISSUES FOR DISCUSSION AT DESIRE BILL 1/2018 DIALOGUE

Page 4

Year end translation loss, say, 150,000

--------------

Balance as at end of Year 3 1,500,000

=========

Amount to be reported in Bahagian N7

Based on the explanation given by LHDNM, the amount to be reported in N7, for Year 1 to Year 3,

should be maintained at RM1,000,000 throughout, since no new loan is taken and no repayment is

made.

Comparison of the amount shown under “Loan from holding company” as at the end of each financial

year in the Balance Sheet and as disclosed in Bahagian N7:

Year

Year end balance

of loan outstanding

Amount to be disclosed in

Bahagian N7 of Form C

(RM) (RM)

1 1,150,000 1,000,000

2 1,300,000 1,000,000

3 1,500,000 1,000,000

Question: Would the above contrasting figures give the impression that extra loans were taken but not

reported in the respective years?

Maklum balas LHDNM

Pihak LHDNM mengambil maklum perbezaan jumlah yang dilaporkan di kunci kira-kira dalam

Penyata Kewangan Syarikat adalah mengambil kira amaun faedah pinjaman serta lain-lain

pengenaan yang berkait dengan pinjaman tersebut manakala jumlah pinjaman yang di isi

dalam Bahagian N7 Borang C adalah jumlah pinjaman asal yang di bawa dari tahun sebelum

berserta dengan jumlah pinjaman baru dalam tahun berkenaan.

THE MALAYSIAN INSTITUTE OF CHARTERED

SECRETARIES AND ADMINISTRATORS

ISSUES FOR DISCUSSION AT DESIRE BILL 1/2018 DIALOGUE

Page 5

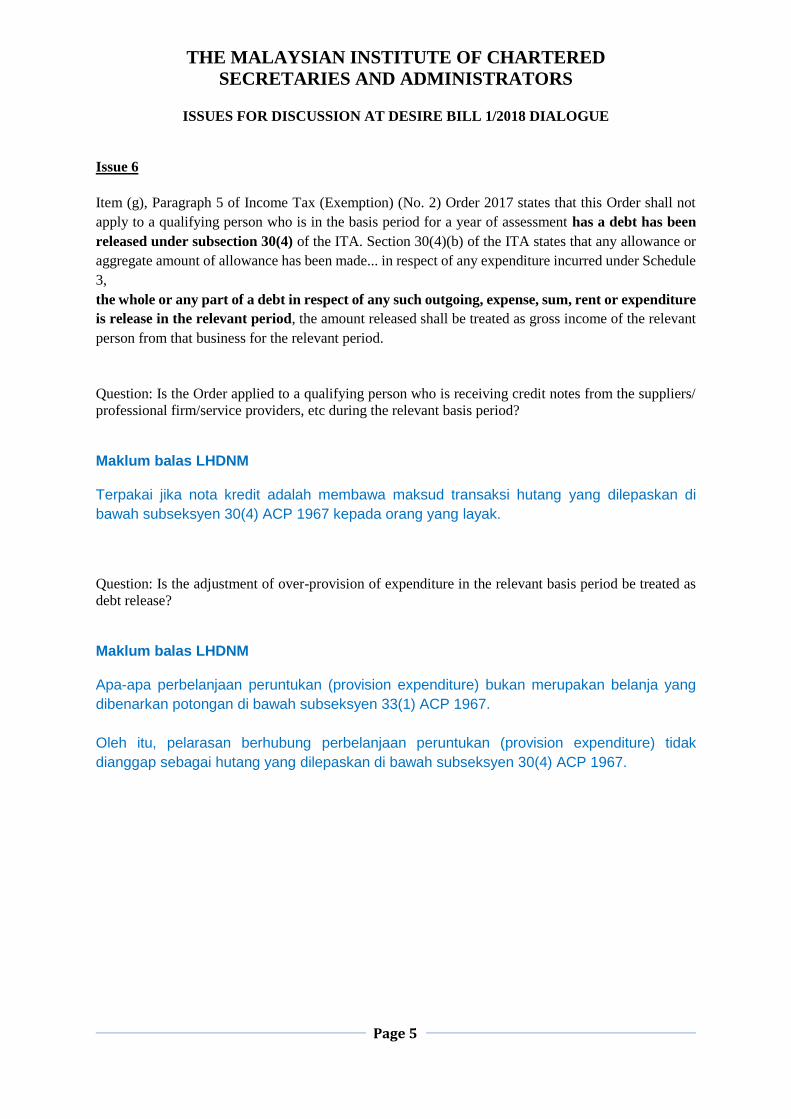

Issue 6

Item (g), Paragraph 5 of Income Tax (Exemption) (No. 2) Order 2017 states that this Order shall not

apply to a qualifying person who is in the basis period for a year of assessment has a debt has been

released under subsection 30(4) of the ITA. Section 30(4)(b) of the ITA states that any allowance or

aggregate amount of allowance has been made... in respect of any expenditure incurred under Schedule

3,

the whole or any part of a debt in respect of any such outgoing, expense, sum, rent or expenditure

is release in the relevant period, the amount released shall be treated as gross income of the relevant

person from that business for the relevant period.

Question: Is the Order applied to a qualifying person who is receiving credit notes from the suppliers/

professional firm/service providers, etc during the relevant basis period?

Maklum balas LHDNM Terpakai jika nota kredit adalah membawa maksud transaksi hutang yang dilepaskan di

bawah subseksyen 30(4) ACP 1967 kepada orang yang layak.

Question: Is the adjustment of over-provision of expenditure in the relevant basis period be treated as

debt release?

Maklum balas LHDNM Apa-apa perbelanjaan peruntukan (provision expenditure) bukan merupakan belanja yang

dibenarkan potongan di bawah subseksyen 33(1) ACP 1967.

Oleh itu, pelarasan berhubung perbelanjaan peruntukan (provision expenditure) tidak

dianggap sebagai hutang yang dilepaskan di bawah subseksyen 30(4) ACP 1967.

MEMORANDUM ON COMPLIANCE AND OPERATIONAL ISSUES

(NO.2/2018)

13 April 2018

Prepared by:

Compliance & Operations Working Group (COWG)

Chartered Tax Institute of Malaysia

Memorandum on Compliance and Operational Issues (No.2/2018)

Contents

Page No.

PENALTY ISSUES

1. Penalty under S.112(3) of the Income Tax Act (ITA) 1967 3

FILING ISSUES

2. Disclosure in the Form C (Part L) – Biological asset / Others 5

3. Disclosure in the Form C (Part L) – Financial Particulars of Company (Main Business): Item L1A: Type of business activity

6

4. Disclosure in the Form C (Part L) – Financial Particulars of Company (Main Business): L41: Loans to directors and L49: Loans from directors

7

5. Disclosures in the Form C (Part N) – Transaction Between Related Companies: Definition of related companies

8

TAX PAYMENT / REFUND ISSUES

6. Form CP 349 – “Pemberitahuan Penangguhan Bayaran Balik Cukai Pendapatan”

9

7. Revision of Estimate of Tax Payable (ETP) outside the 9th month of the basis period

11

Appendix 1 12

Appendix 2 13

Memorandum on Compliance and Operational Issues (No.2/2018)

Page 3 of 13

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

1. Penalty under S.112(3) of the Income Tax Act (ITA) 1967

The company was late in submitting the Form e-C for YA 2016. The IRB raised the Form J

under S.90(3) and imposed a penalty under S.112(3) – 20% of the estimated tax.

Example:

Form J under S.90(3) – tax payable of RM100,000 and penalty of RM20,000 (i.e. 20% of

RM100,000)

Subsequently, the company filed the Form e-C (within 6 months after the due date) and the

actual tax payable is as follows:-

a) Scenario 1: RM40,000

b) Scenario 2: RM0

c) Scenario 3: RM200,000

CTIM comments:

We would like to seek the IRB’s answers to the following:-

a) Can the IRB state what would be the penalty rate and amount that will be imposed under

Section 112(3) for each of the above 3 scenarios?

b) We seek the rationale from the IRB to indicate or explain the relevant provisions in the

Income Tax Act for the basis for imposing the penalty as per the answers in question (a)

above.

Memorandum on Compliance and Operational Issues (No.2/2018)

Page 4 of 13

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

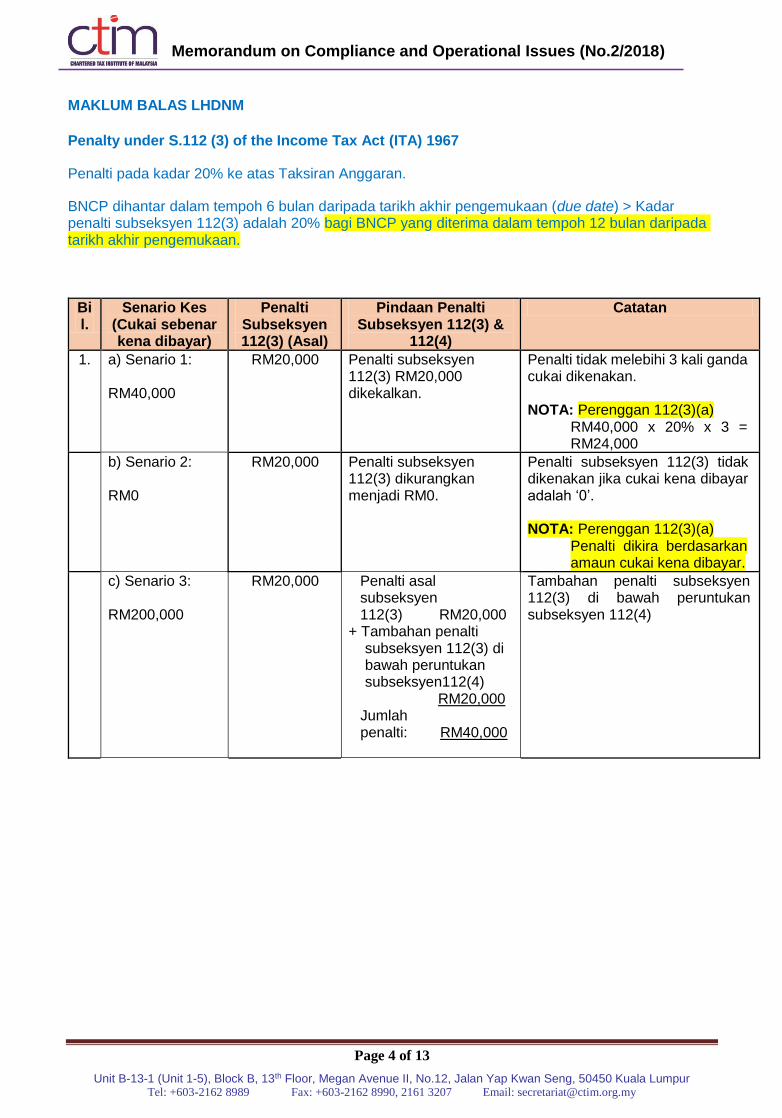

MAKLUM BALAS LHDNM

Penalty under S.112 (3) of the Income Tax Act (ITA) 1967

Penalti pada kadar 20% ke atas Taksiran Anggaran.

BNCP dihantar dalam tempoh 6 bulan daripada tarikh akhir pengemukaan (due date) > Kadar penalti subseksyen 112(3) adalah 20% bagi BNCP yang diterima dalam tempoh 12 bulan daripada tarikh akhir pengemukaan.

Bil.

Senario Kes (Cukai sebenar kena dibayar)

Penalti Subseksyen 112(3) (Asal)

Pindaan Penalti Subseksyen 112(3) &

112(4)

Catatan

1. a) Senario 1: RM40,000

RM20,000 Penalti subseksyen 112(3) RM20,000 dikekalkan.

Penalti tidak melebihi 3 kali ganda cukai dikenakan. NOTA: Perenggan 112(3)(a)

RM40,000 x 20% x 3 = RM24,000

b) Senario 2: RM0

RM20,000 Penalti subseksyen 112(3) dikurangkan menjadi RM0.

Penalti subseksyen 112(3) tidak dikenakan jika cukai kena dibayar adalah ‘0’. NOTA: Perenggan 112(3)(a)

Penalti dikira berdasarkan amaun cukai kena dibayar.

c) Senario 3: RM200,000

RM20,000 Penalti asal subseksyen 112(3) RM20,000

+ Tambahan penalti subseksyen 112(3) di bawah peruntukan subseksyen112(4) RM20,000

Jumlah penalti: RM40,000

Tambahan penalti subseksyen 112(3) di bawah peruntukan subseksyen 112(4)

Memorandum on Compliance and Operational Issues (No.2/2018)

Page 5 of 13

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

2. Disclosure in the Form C (Part L) – Biological asset / Others

2.1 Under the Malaysian Private Entity Reporting Standard (MPERS), new and replanting

expenditure are capitalised as biological assets of bearer plants and are measured at cost

less accumulated amortisation and accumulated impairment losses. The biological assets

are separately disclosed in the balance sheet under “non-current assets”.

Currently, the only available items for disclosure in Part L are L34: Other fixed assets or L37:

Investments.

The explanations for these items per the Company Return Form Guidebook 2016 and 2017

are as follows:-

L34: Other fixed assets - Net book value as per Balance Sheet (net book value of fixed

assets other than motor vehicles, plant and machinery and land and buildings)

L37: Investments - Cost of investments and fixed deposits.

CTIM comments:

For the purposes of disclosure in Part L of the Form C, we seek the IRB’s confirmation on

whether the biological assets should be disclosed under L34: Other fixed assets.

MAKLUM BALAS LHDNM

Biological assets should be disclosed under L34: Other fixed assets.

2.2 Other example – Investment in equity instruments

The investment is carried at fair value and is disclosed as such in the audited report.

However, investments are required to be disclosed at cost in Part L of the Form C (L37:

Investments).

CTIM comments:

In view of the many changes in the accounting standards in recent years, we would request

the IRB to revisit the disclosure items in the Form C and also provide more detailed guidance

on the disclosure requirements. To avoid ambiguity and for the purposes of consistency, we

would suggest that the disclosure in the Form C follow the disclosure in the audited accounts

MAKLUM BALAS LHDNM

Syarikat perlu mengemukakan maklumat dalam BNCP berdasarkan kepada akaun beraudit.

Penerangan dalam Buku Panduan Borang Nyata Syarikat akan di pinda sewajarnya.

Memorandum on Compliance and Operational Issues (No.2/2018)

Page 6 of 13

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

3. Disclosure in the Form C (Part L) – Financial Particulars of Company (Main

Business): Item L1A: Type of business activity

As per the Company Return Form Guidebook 2016 and 2017, the explanations for items L1,

L1A, L2 and L10 are as follows:

L1: Business Code – Enter the business code for the main business only. If there is

more than one main business, enter the business code for the business with the

highest turnover.

L1A: Type of business activity - Specify the type of activity of the business concerned

in the box provided.

L2: Sales / Turnover - Total gross income of the main business including accrued

income.

L10: Other business income - Total net income from business sources other than L1.

The company’s principal activities as disclosed in the audited report is investment holding,

rubber and oil palm production on estates in Malaysia. For tax purposes, both rubber and

oil palm are assessed under the same source.

For disclosure in the Form C, L1: Business code, the business code for the business with

the highest turnover is 01261 – Growing of oil palm (estate).

CTIM comments:

Please confirm that all the activities carried out by the company i.e. investment holding,

rubber and oil palm (as disclosed in the audited report) are required to be disclosed in Item

L1A: Type of business activity.

MAKLUM BALAS LHDNM

Tiga (3) Aktiviti perniagaan – pegangan pelaburan, perladangan getah dan perladangan

kelapa sawit. Aktiviti getah dan kelapa sawit adalah dua jenis aktiviti yang berlainan.

Merujuk kepada contoh yang diberikan, perladangan kelapa sawit perlu dilaporkan di item

L1A.

Memorandum on Compliance and Operational Issues (No.2/2018)

Page 7 of 13

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

4. Disclosure in the Form C (Part L) – Financial Particulars of Company (Main

Business): L41: Loans to directors and L49: Loans from directors

As per the Company Return Form Guidebook 2016 and 2017, the explanations for items

L41 and L49 are as follows:-

L41: Loans to directors – Amount as per Balance Sheet.

L49: Loans from directors – In the form of loans and advances as per Balance Sheet.

CTIM comments:

To avoid ambiguity and for the purposes of consistency, we would suggest that the above

explanation for L49: Loan from directors be amended to “Amount as per Balance Sheet.”

which is the same as the explanation for L41: Loans to directors.

MAKLUM BALAS LHDNM

Item L49 membezakan maksud pinjaman dan pendahuluan. Pinjaman mungkin

melibatkan lain-lain kos semasa memperolehi pinjaman berkenaan seperti faedah, yuran

dan perbelanjaan pentadbiran. Manakala pendahuluan mungkin tidak melibatkan kos dan

perbelanjaan tersebut.

Memorandum on Compliance and Operational Issues (No.2/2018)

Page 8 of 13

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

5. Disclosures in the Form C (Part N) – Transaction Between Related

Companies: Definition of related companies

Definition of related companies

As per the Company Return Form Guidebook 2016 and 2017, related companies refer to

companies related through equity shareholding.

However, with reference to the IRB’s letter dated 19 August 2015, the IRB clarified that

the definition of “related companies” for the purposes of Part N of Form C should be based

on paragraph 5 of the Transfer Pricing Guidelines 2015. Paragraph 5.1 of the Transfer

Pricing Guidelines 2012 states “Section 139 of the ITA refers to “control” as both direct

and indirect control. The interpretation of related companies or companies in the same

group (referred to in the context of holding and subsidiary companies) is provided for under

Subsection 2(4) of the same Act”.

CTIM comments:

a) In view of the difference in the definition for “related companies” in the Company Return

Form Guidebook 2016 & 2017 compared to the above paragraph, we would like to

seek the IRB’s clarification on which definition the company should rely on for the

purposes of the disclosure in Part N of the Form C.

MAKLUM BALAS LHDNM

Untuk tujuan pelaporan di Bahagian N Borang C, takrifan ‘syarikat berkaitan’ adalah

berasaskan perenggan 5, Garis Panduan Pindahan Harga 2012.

For the purposes of the disclosure in Part N of the Form C, the definition of ‘related

companies’ is based on paragraph 5 of the Transfer Pricing Guidelines 2012.

b) However, it is a very tedious exercise for tax payer or even tax practitioners to

determine related companies through equity shareholding.

In order to ease compliance, for the purposes of consistency and also to avoid incorrect

return implications, we would propose that the information in Part N of Form C be

completed based on disclosures in the Audited Account.

MAKLUM BALAS LHDNM

Memandangkan penentuan syarikat berkaitan bukan berasaskan pegangan ekuiti,

soalan ini adalah tidak relevan. Maklumat di Bahagian N Borang C hendaklah

dilaporkan seperti maklumbalas kepada soalan 5(a).

Since the determination of related companies is not through equity shareholding, this

question is not relevant. The disclosure in Part N of Form C should be completed

based on the reply to question 5(a).

Memorandum on Compliance and Operational Issues (No.2/2018)

Page 9 of 13

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

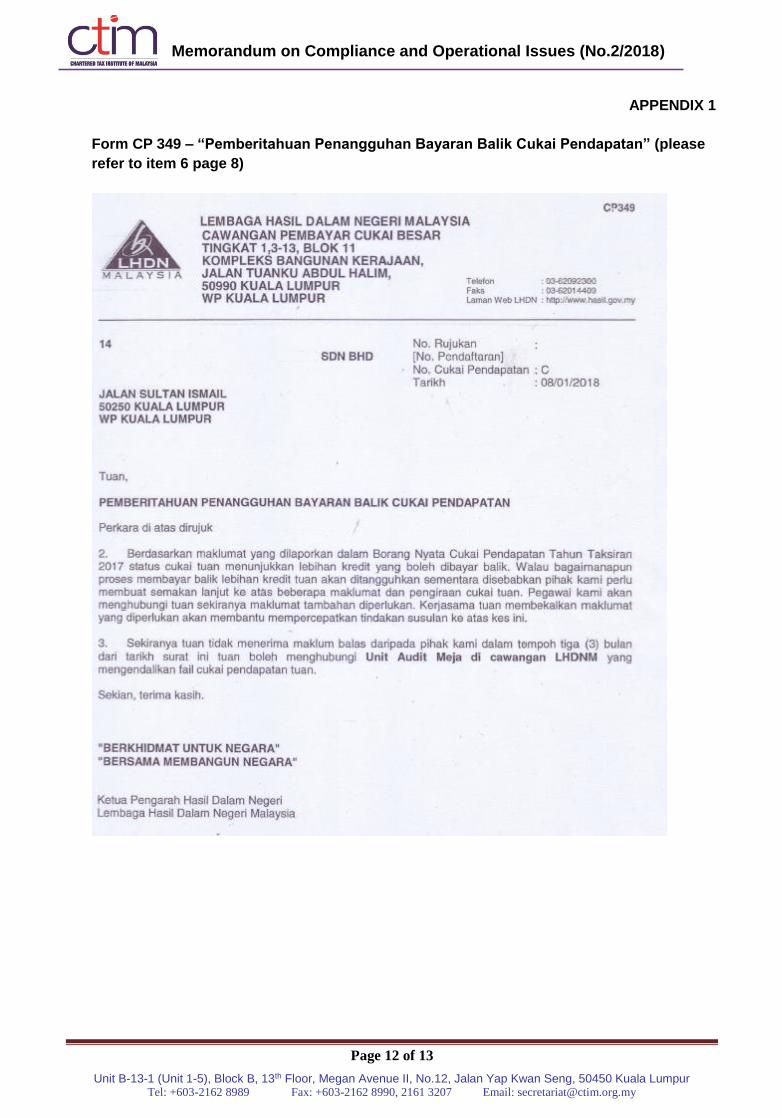

6. Form CP349 – “Pemberitahuan Penangguhan Bayaran Balik Cukai

Pendapatan”

The IRB issued the Form CP349. Please refer to the enclosed sample in the Appendix 1.

It is mentioned in this standard letter that the IRB needs three months to reply and

meanwhile, any tax credit with the IRB will not be refunded.

In our recent inquiry, we have been informed that unless the taxpayers take the initiative

of writing to the IRB to invite an audit, it is not likely for the taxpayers to receive any refund.

However, this is not made known anywhere in the IRB’s letter.

CTIM comments: (with reference to Appendix 1)

a) We hope to get the IRB’s clarification on the third paragraph above. If it is correct, this

standard letter has to be amended.

MAKLUM BALAS LHDNM

Terdapat segelintir ejen-ejen/pembayar cukai dengan inisiatif sendiri telah menulis

surat mempelawa LHDNM menjalankan tindakan audit ke atas mereka kerana percaya

bahawa bayaran balik kredit cukai akan diterima segera selepas audit dijalankan.

Sedangkan LHDNM tidak memerlukan inisiatif tersebut sebelum bayaran balik cukai

disegerakan untuk kelulusan. Oleh itu, syarat dan terma tersebut tidak dimaklumkan

dalam mana-mana surat LHDNM.

Borang CP349 adalah notis pemberitahuan sebagai pengesahan bahawa pembayar

cukai mempunyai baki kredit cukai yang ditangguhkan bayaran balik sehingga

tindakan audit diselesaikan. Perenggan 3 dalam CP349 dikekalkan tanpa pindaan.

b) This Form CP349 letter is an auto-generated letter with no undersign officer in charge.

Can we be directed to liaise with a particular officer in charge in order for us to follow

up on these cases?

MAKLUM BALAS LHDNM

Pembayar cukai boleh menghubungi cawangan seperti yang tertera di kepala surat

CP349 untuk mengetahui status kes.

c) We would like to seek the IRB’s confirmation on whether this issuance of Form CP349

is tantamount to informing the taxpayer that the IRB is carrying out a tax audit?

MAKLUM BALAS LHDNM

Borang CP349 dikeluarkan semata-mata bertujuan untuk memaklumkan bayaran balik

ditangguhkan sehingga selesai semakan audit.

Memorandum on Compliance and Operational Issues (No.2/2018)

Page 10 of 13

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

d) In the above situation, is the taxpayer still entitled to a compensation for the

overpayment of tax under S.111D of the ITA 1967 if the Return was filed within the

statutory deadline?

MAKLUM BALAS LHDNM

Kes-kes yang dikenakan tindakan audit tidak layak menerima pampasan di bawah

Seksyen 111D Akta Cukai Pendapatan 1967.

Memorandum on Compliance and Operational Issues (No.2/2018)

Page 11 of 13

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

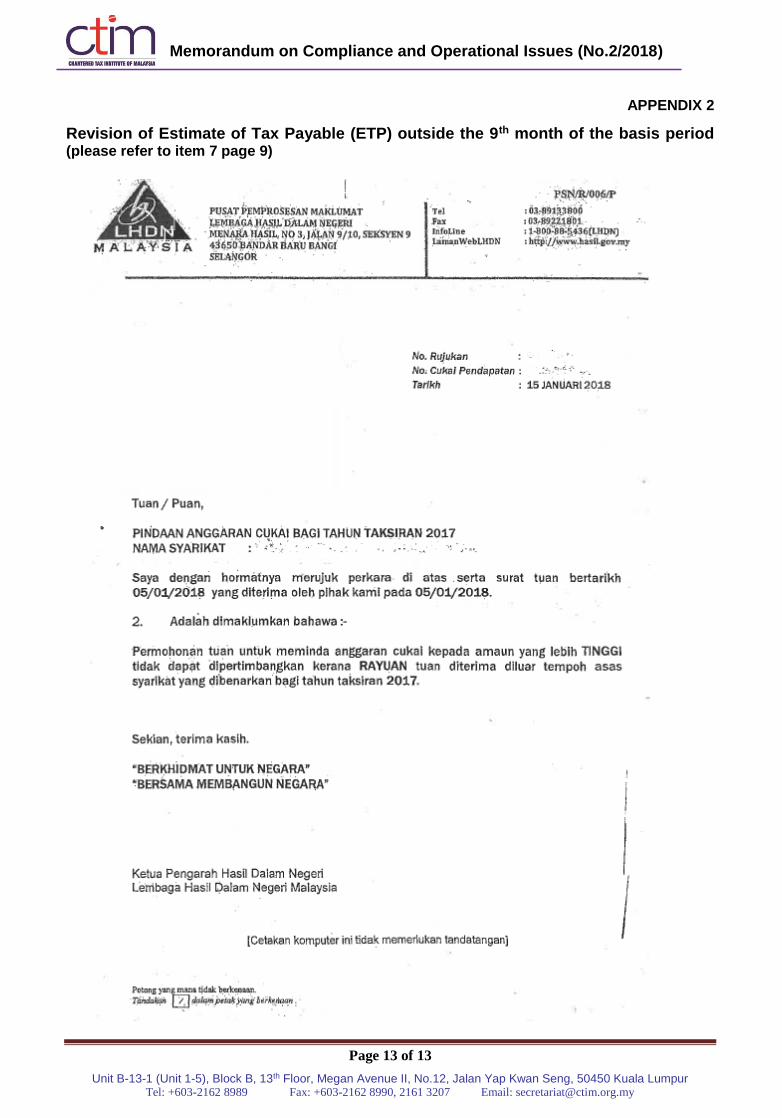

7. Revision of Estimate of Tax Payable (ETP) outside the 9th month of the basis period

Recently one of our clients in the construction industry had applied for a revision of the

ETP outside the 9th month of the basis period. Reason being they had made an application

to the relevant authorities in year 2015 to seek reimbursement of the maintenance

expenses incurred for the last 2 to 3 years. In October 2017, the client was notified by the

relevant authorities that they would be expecting a refund of an amount (quite a substantial

sum) from the authorities.

Since the client is expected to receive this substantial sum of money in YA 2017 (year end

31 December), this amount will be brought to tax in YA 2017 and hence the ETP needs to

be revised. The client has submitted the revised ETP for YA 2017 to the Pusat

Pemprosesan in early January 2018. The officer in charge has rejected the client’s

application on the basis that in accordance to their internal guide the revised ETP has to

be submitted within the basis period of YA 2017 (i.e on or before 31 December 2017). The

internal guide only provides that the IRB has the right to reject the revision of the ETP if

no initial ETP has been submitted earlier. It is not reasonable for the IRB to insist that the

revised ETP has to be submitted within the basis period of YA 2017 as the client has

submitted all the supporting documents and to justify that they had to work out a detailed

calculation to allocate part of the refund amount to other sub-contractors and only bring

the correct portion to be subjected to tax. Please refer to the enclosed sample in the

Appendix 2.

If a client unexpectedly receives a huge sales order in late December 2017 (i.e. after

Christmas), it is impossible for the Finance and Accounts Department of a firm to be able

to do the necessary submission for the revised ETP in time before 31 December 2017.

CTIM comments: (with reference to Appendix 2)

We would appreciate that the IRB exercise its discretion to grant the revision of the ETP

outside the 9th month if the taxpayer has strong grounds and justifications and also had

made a voluntary payment on or before the last instalment is due to be paid.

MAKLUM BALAS LHDNM

Tiada sebarang peruntukan dinyatakan di dalam Akta Cukai Pendapatan 1967 yang

membenarkan rayuan pindaan anggaran cukai dibuat selain daripada bulan ke-6 dan ke-

9 dalam suatu tempoh asas. Walau bagaimanapun, berasaskan setiap kes, permohonan

rayuan yang dikemukakan dalam tempoh asas masih boleh dipertimbangkan dengan

syarat alasan yang diberikan dan dokumen sokongan yang disertakan adalah lengkap dan

relevan.

Bagi kes di mana permohonan rayuan dikemukakan di luar tempoh asas, rayuan tersebut

tidak akan dipertimbangkan oleh pihak LHDNM.

Memorandum on Compliance and Operational Issues (No.2/2018)

Page 12 of 13

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

APPENDIX 1

Form CP 349 – “Pemberitahuan Penangguhan Bayaran Balik Cukai Pendapatan” (please

refer to item 6 page 8)

Memorandum on Compliance and Operational Issues (No.2/2018)

Page 13 of 13

Unit B-13-1 (Unit 1-5), Block B, 13th Floor, Megan Avenue II, No.12, Jalan Yap Kwan Seng, 50450 Kuala Lumpur Tel: +603-2162 8989 Fax: +603-2162 8990, 2161 3207 Email: [email protected]

APPENDIX 2

Revision of Estimate of Tax Payable (ETP) outside the 9th month of the basis period (please refer to item 7 page 9)