gwadar port master plan - shani-med.comshani-med.com/destra/courses/1387397437_aurthur d. little...

TRANSCRIPT

Arthur D. Little (M) Sdn BhdOffice Suite, 19-13-2Level 13, UOA Centre19 Jalan Pinang50450 Kuala LumpurMalaysia

Gwadar Port Master Plan- Implications for Energy Sector Development

25-26 April 2006

1

Gwadar port master plan

Gwadar port current situation

Port development potential

Industrial development potential

Traffic forecasts

Port zoning plan

Development program 2006-2021

Investment opportunities

Outline

2

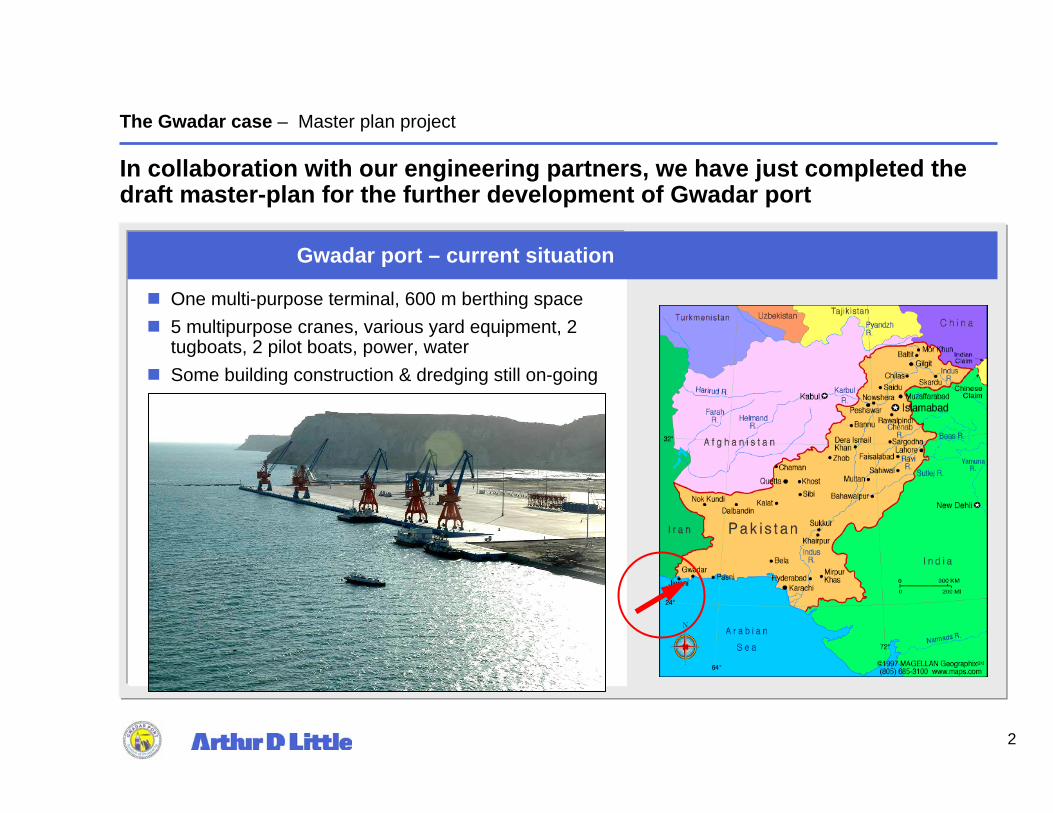

One multi-purpose terminal, 600 m berthing space 5 multipurpose cranes, various yard equipment, 2 tugboats, 2 pilot boats, power, waterSome building construction & dredging still on-going

Gwadar port – current situation

The Gwadar case – Master plan project

In collaboration with our engineering partners, we have just completed the draft master-plan for the further development of Gwadar port

3

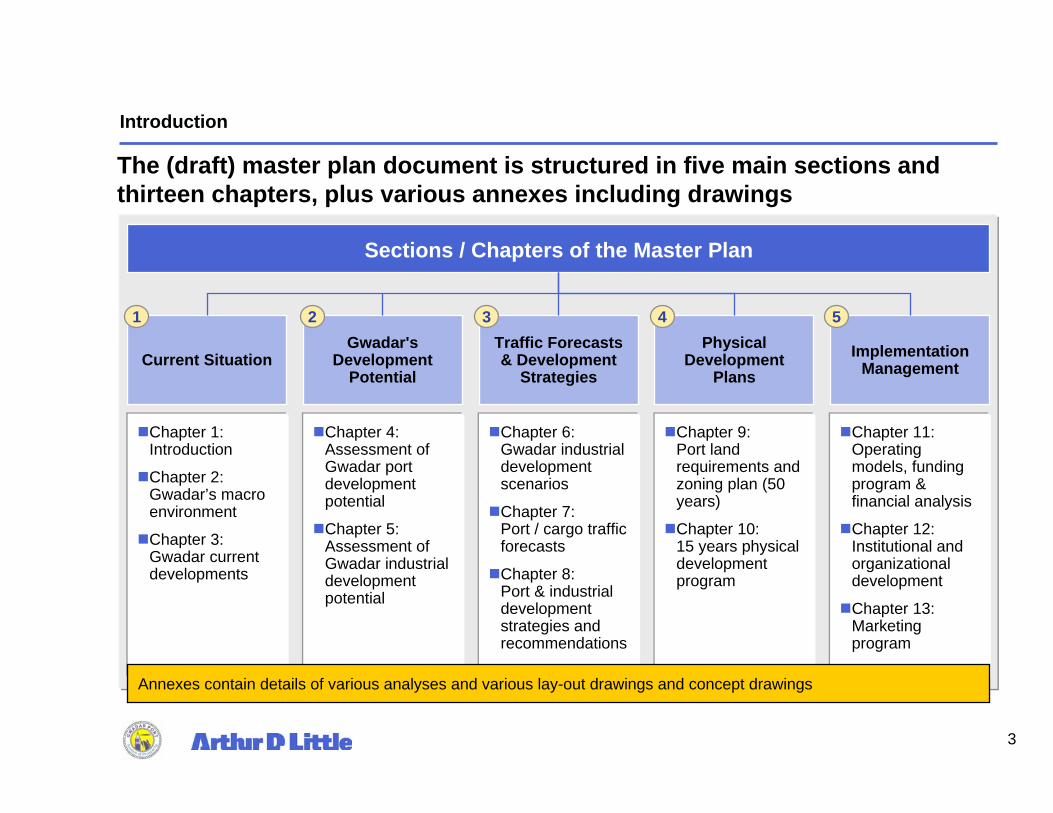

Chapter 1: Introduction

Chapter 2: Gwadar’s macro environment

Chapter 3: Gwadar current developments

Sections / Chapters of the Master Plan

Physical Development

Plans

Gwadar's Development

PotentialCurrent Situation

The (draft) master plan document is structured in five main sections and thirteen chapters, plus various annexes including drawings

Traffic Forecasts & Development

Strategies

Chapter 4: Assessment of Gwadar port development potential

Chapter 5: Assessment of Gwadar industrial development potential

Chapter 6: Gwadar industrial development scenarios

Chapter 7: Port / cargo traffic forecasts

Chapter 8: Port & industrial development strategies and recommendations

Chapter 9: Port land requirements and zoning plan (50 years)

Chapter 10: 15 years physical development program

1 2 3 4

Introduction

Implementation Management

Chapter 11: Operating models, funding program & financial analysis

Chapter 12: Institutional and organizational development

Chapter 13: Marketing program

5

Annexes contain details of various analyses and various lay-out drawings and concept drawings

4

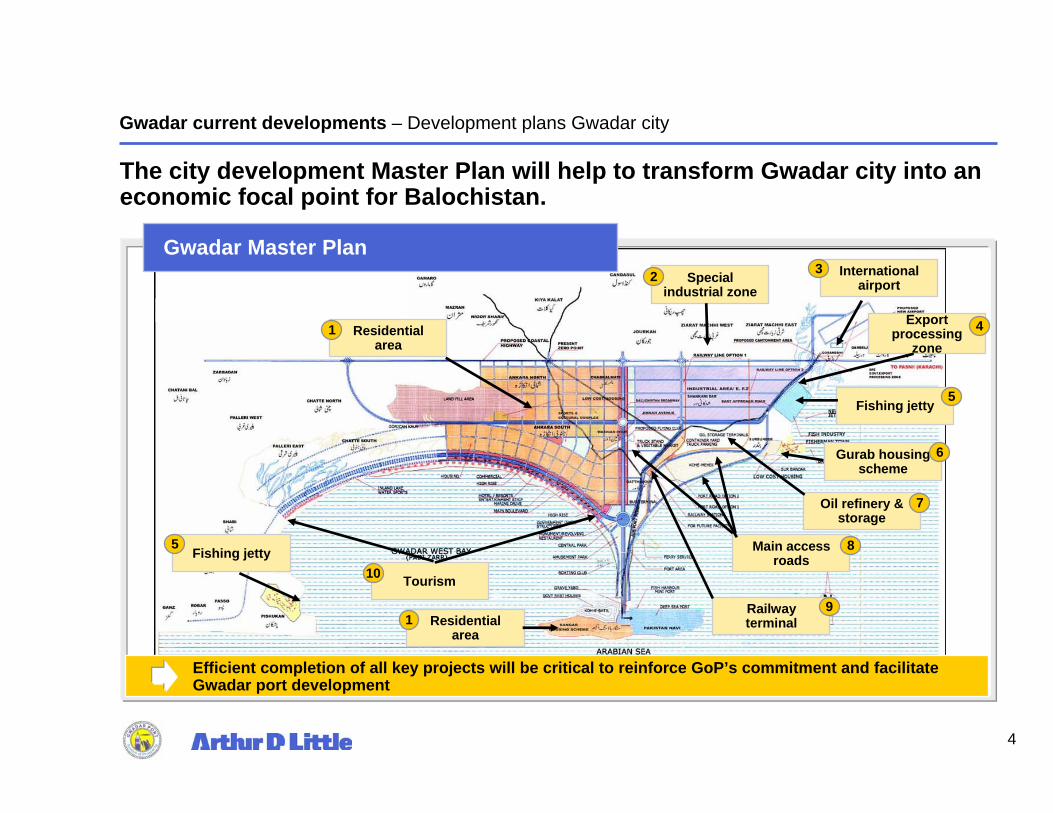

The city development Master Plan will help to transform Gwadar city into an economic focal point for Balochistan.

Oil refinery & storage

Railway terminal

Main access roads

Special industrial zone

Residential area

Fishing jetty

Tourism

Residential area

1

1

2

7

8

9

10

International airport

Export processing

zone4

Fishing jetty

3

5

Gurab housing scheme

6

5

Gwadar Master Plan

Efficient completion of all key projects will be critical to reinforce GoP’s commitment and facilitate Gwadar port development

Gwadar current developments – Development plans Gwadar city

5

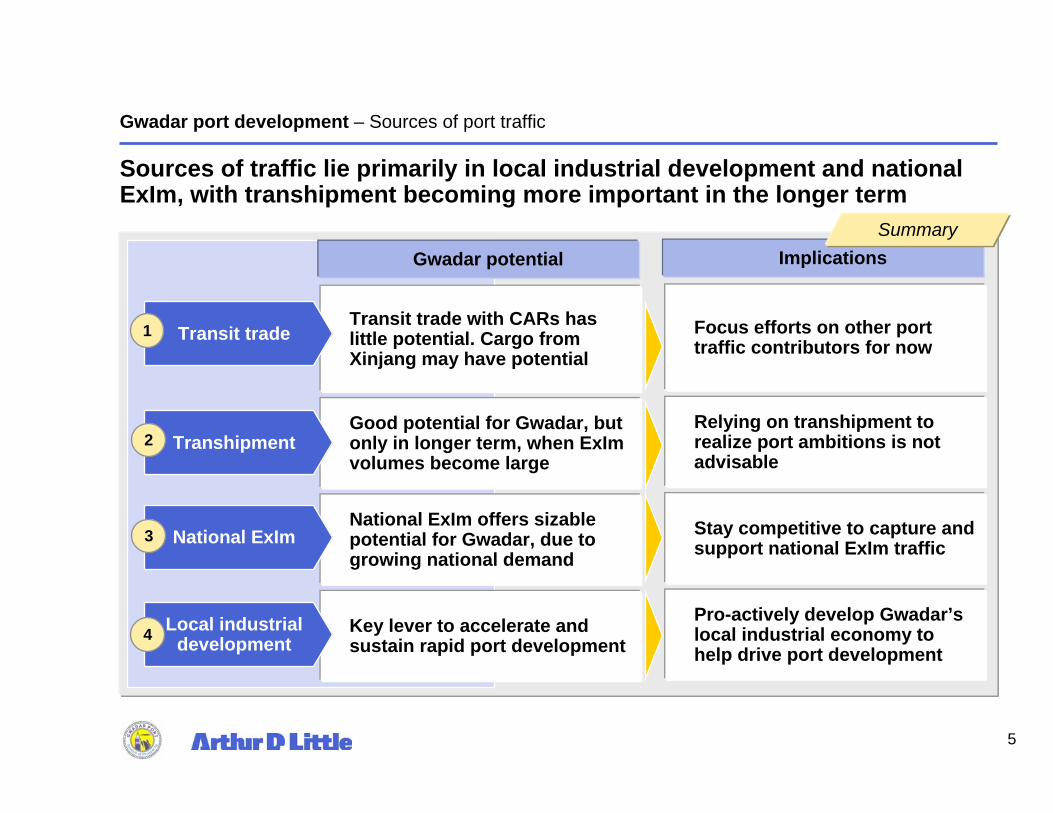

Sources of traffic lie primarily in local industrial development and national ExIm, with transhipment becoming more important in the longer term

Gwadar potential Implications

Transit trade with CARs has little potential. Cargo from Xinjang may have potential

Good potential for Gwadar, but only in longer term, when ExImvolumes become large

National ExIm offers sizable potential for Gwadar, due to growing national demand

Key lever to accelerate and sustain rapid port development

Focus efforts on other port traffic contributors for now

Relying on transhipment to realize port ambitions is not advisable

Stay competitive to capture and support national ExIm traffic

Pro-actively develop Gwadar’s local industrial economy to help drive port development

Transit trade

Transhipment

National ExIm

Local industrial development

1

2

3

4

Gwadar port development – Sources of port traffic

Summary

6

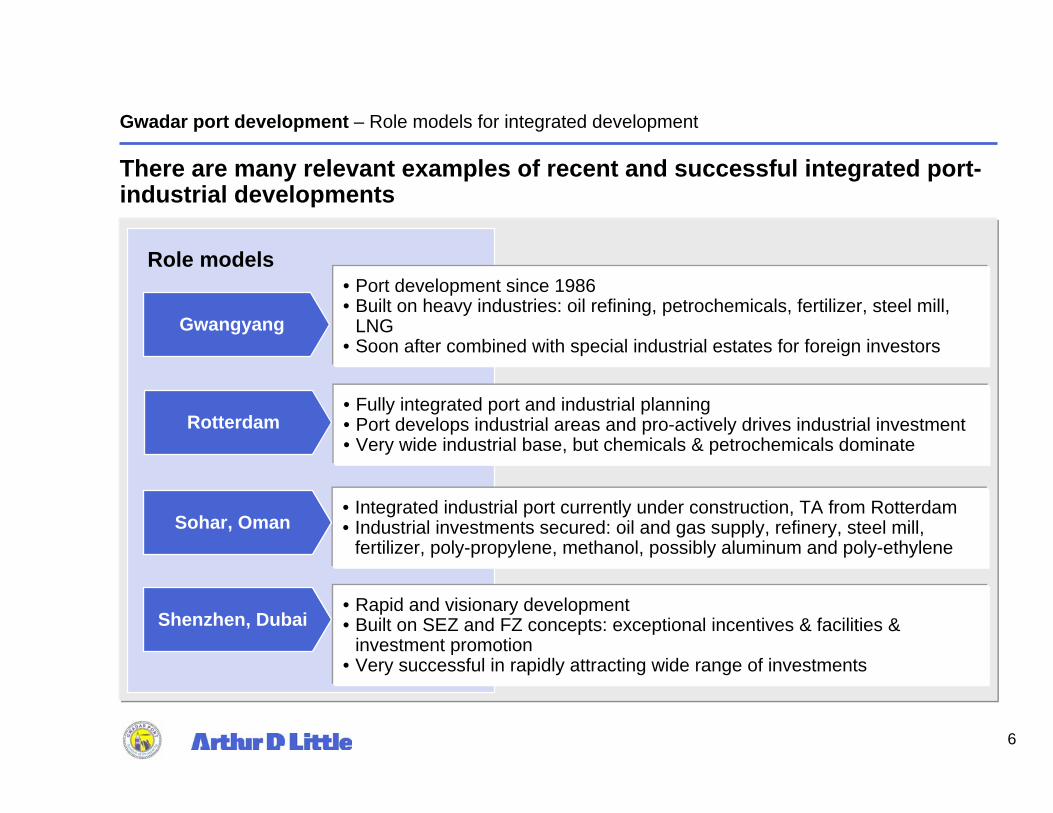

Role models

• Integrated industrial port currently under construction, TA from Rotterdam• Industrial investments secured: oil and gas supply, refinery, steel mill,

fertilizer, poly-propylene, methanol, possibly aluminum and poly-ethylene

Gwadar port development – Role models for integrated development

There are many relevant examples of recent and successful integrated port-industrial developments

Sohar, Oman

Shenzhen, Dubai

Gwangyang

Rotterdam• Fully integrated port and industrial planning• Port develops industrial areas and pro-actively drives industrial investment• Very wide industrial base, but chemicals & petrochemicals dominate

• Rapid and visionary development• Built on SEZ and FZ concepts: exceptional incentives & facilities &

investment promotion• Very successful in rapidly attracting wide range of investments

• Port development since 1986• Built on heavy industries: oil refining, petrochemicals, fertilizer, steel mill,

LNG• Soon after combined with special industrial estates for foreign investors

7

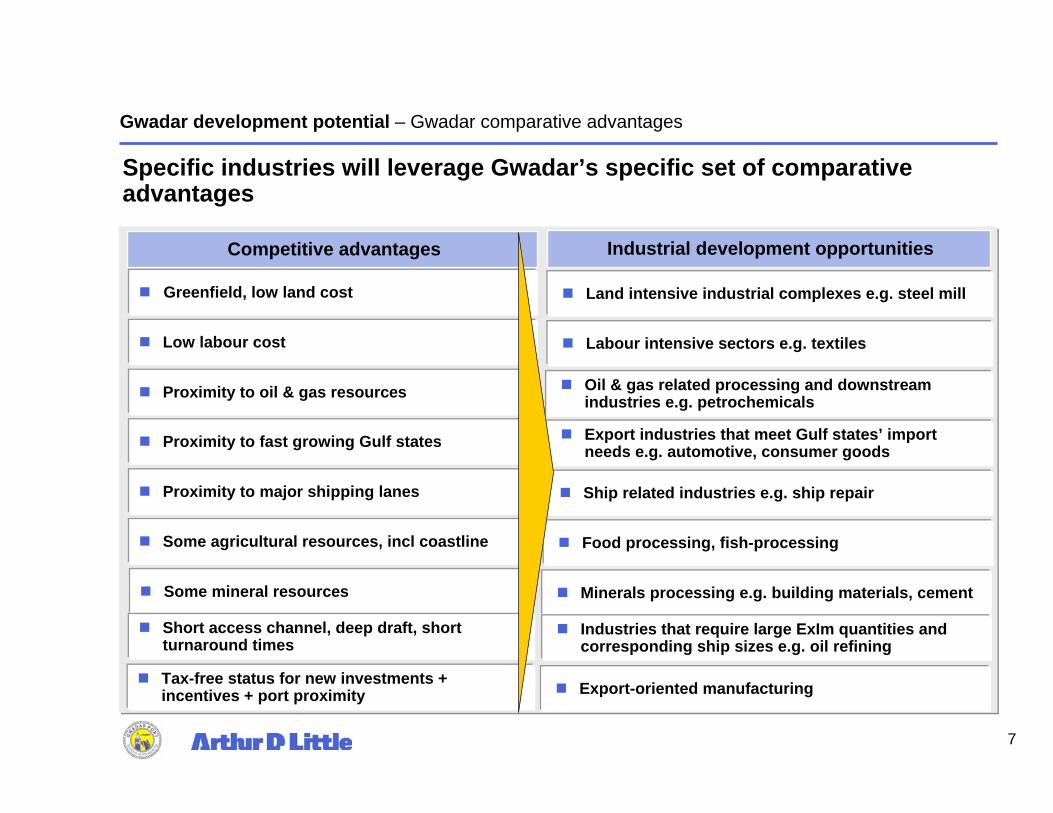

Specific industries will leverage Gwadar’s specific set of comparative advantages

Competitive advantages

Ship related industries e.g. ship repair

Food processing, fish-processing

Export industries that meet Gulf states’ import needs e.g. automotive, consumer goods

Labour intensive sectors e.g. textiles

Oil & gas related processing and downstream industries e.g. petrochemicals

Land intensive industrial complexes e.g. steel mill

Minerals processing e.g. building materials, cement

Industries that require large ExIm quantities and corresponding ship sizes e.g. oil refining

Industrial development opportunities

Proximity to major shipping lanes

Some agricultural resources, incl coastline

Proximity to fast growing Gulf states

Low labour cost

Proximity to oil & gas resources

Greenfield, low land cost

Some mineral resources

Short access channel, deep draft, short turnaround times

Gwadar development potential – Gwadar comparative advantages

Export-oriented manufacturingTax-free status for new investments + incentives + port proximity

8

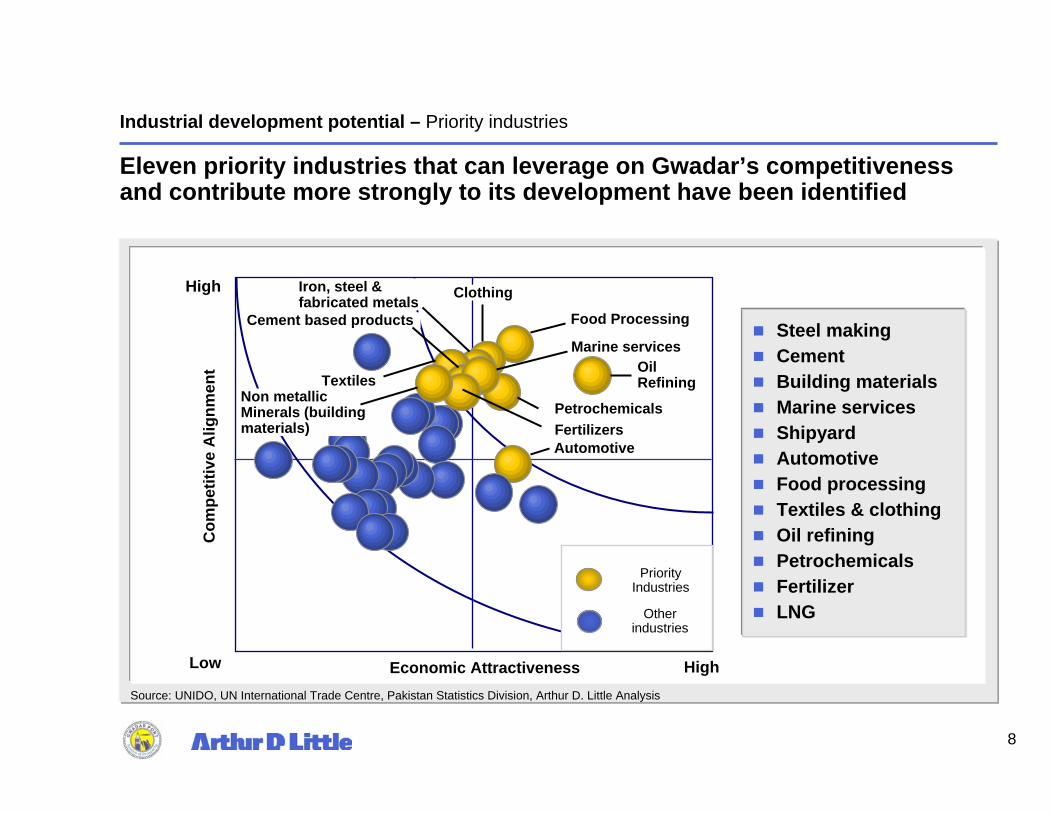

Eleven priority industries that can leverage on Gwadar’s competitiveness and contribute more strongly to its development have been identified

Source: UNIDO, UN International Trade Centre, Pakistan Statistics Division, Arthur D. Little Analysis

Com

petit

ive

Alig

nmen

t

Low

High

HighEconomic Attractiveness

Priority Industries

Other industries

Oil Refining

Food Processing

Petrochemicals

Clothing

Textiles

Iron, steel & fabricated metals

Automotive

Non metallicMinerals (building materials)

Marine services

Fertilizers

Cement based products

Industrial development potential – Priority industries

Steel makingCementBuilding materialsMarine servicesShipyardAutomotiveFood processingTextiles & clothingOil refiningPetrochemicalsFertilizerLNG

9

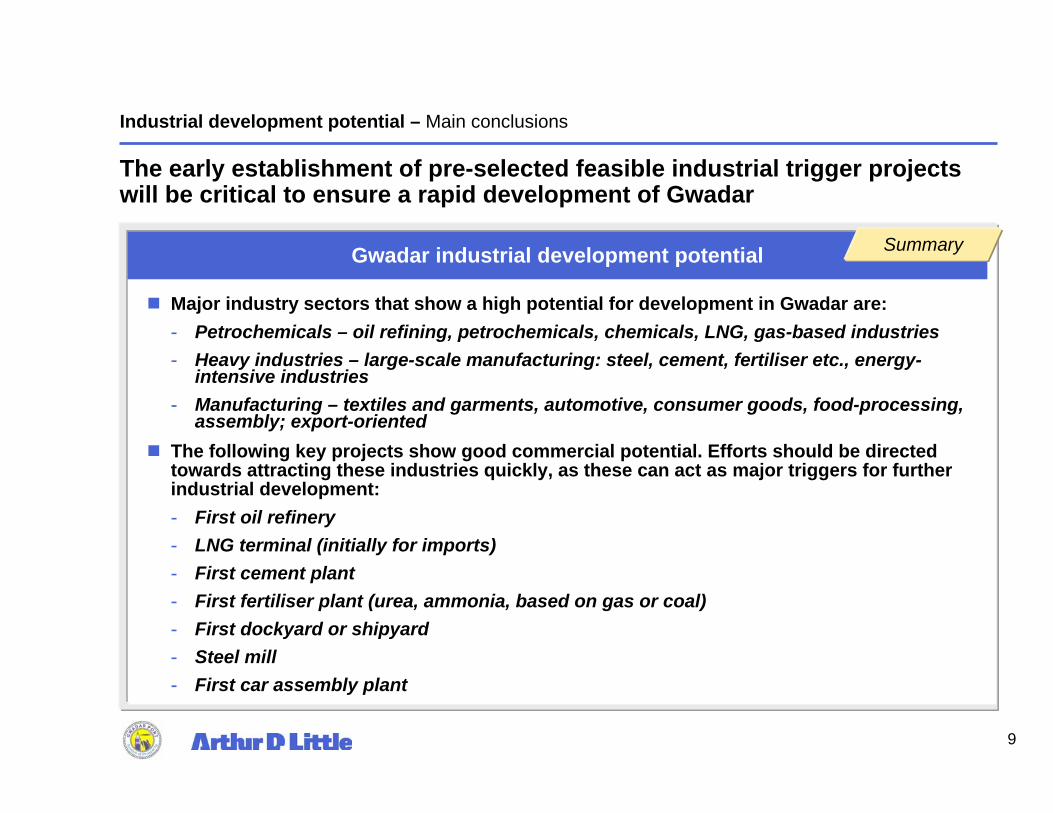

Major industry sectors that show a high potential for development in Gwadar are:- Petrochemicals – oil refining, petrochemicals, chemicals, LNG, gas-based industries- Heavy industries – large-scale manufacturing: steel, cement, fertiliser etc., energy-

intensive industries- Manufacturing – textiles and garments, automotive, consumer goods, food-processing,

assembly; export-oriented The following key projects show good commercial potential. Efforts should be directed towards attracting these industries quickly, as these can act as major triggers for further industrial development:- First oil refinery- LNG terminal (initially for imports)- First cement plant- First fertiliser plant (urea, ammonia, based on gas or coal)- First dockyard or shipyard- Steel mill - First car assembly plant

Gwadar industrial development potential

Industrial development potential – Main conclusions

The early establishment of pre-selected feasible industrial trigger projects will be critical to ensure a rapid development of Gwadar

Summary

10

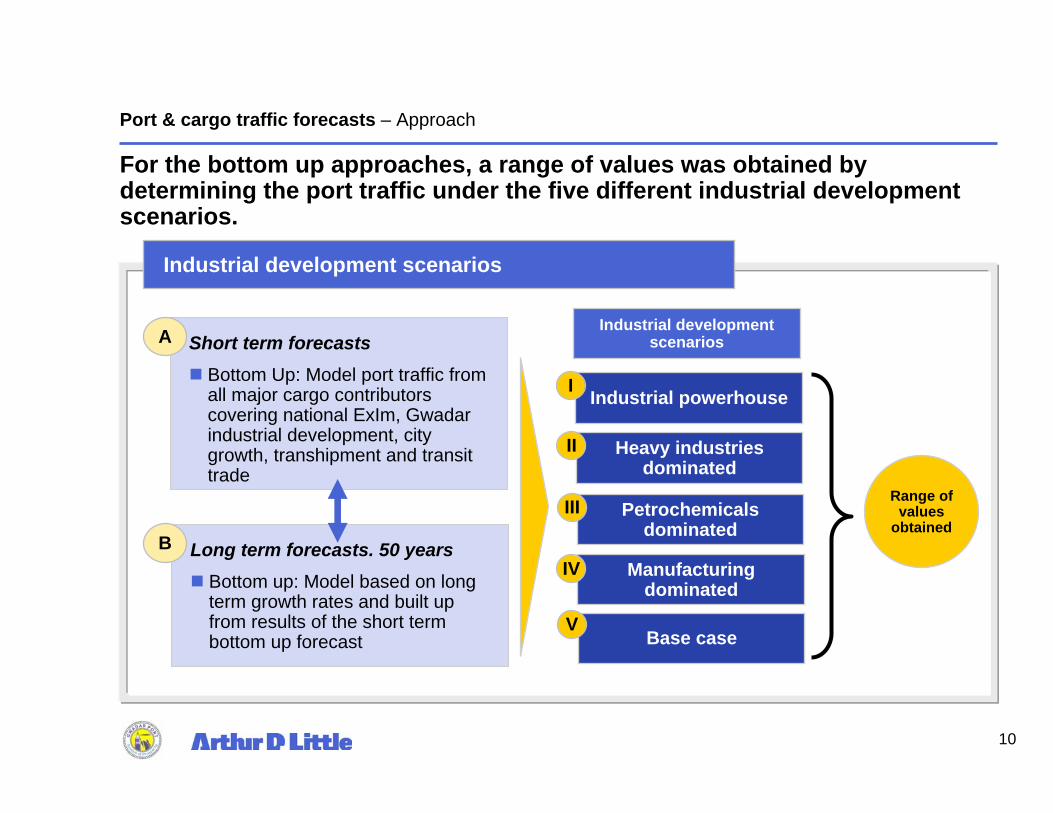

For the bottom up approaches, a range of values was obtained by determining the port traffic under the five different industrial development scenarios.

Short term forecastsBottom Up: Model port traffic from all major cargo contributors covering national ExIm, Gwadar industrial development, city growth, transhipment and transit trade

Long term forecasts. 50 yearsBottom up: Model based on long term growth rates and built up from results of the short term bottom up forecast

Industrial development scenarios

A

B

Industrial development scenarios

Industrial powerhouse

Heavy industries dominated

Petrochemicals dominated

Manufacturing dominated

Base case

I

II

III

IV

V

Range of values

obtained

Port & cargo traffic forecasts – Approach

11

0

100

200

300

400

500

600

700

800

900

1000

1100

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50

2nd PortGwadar

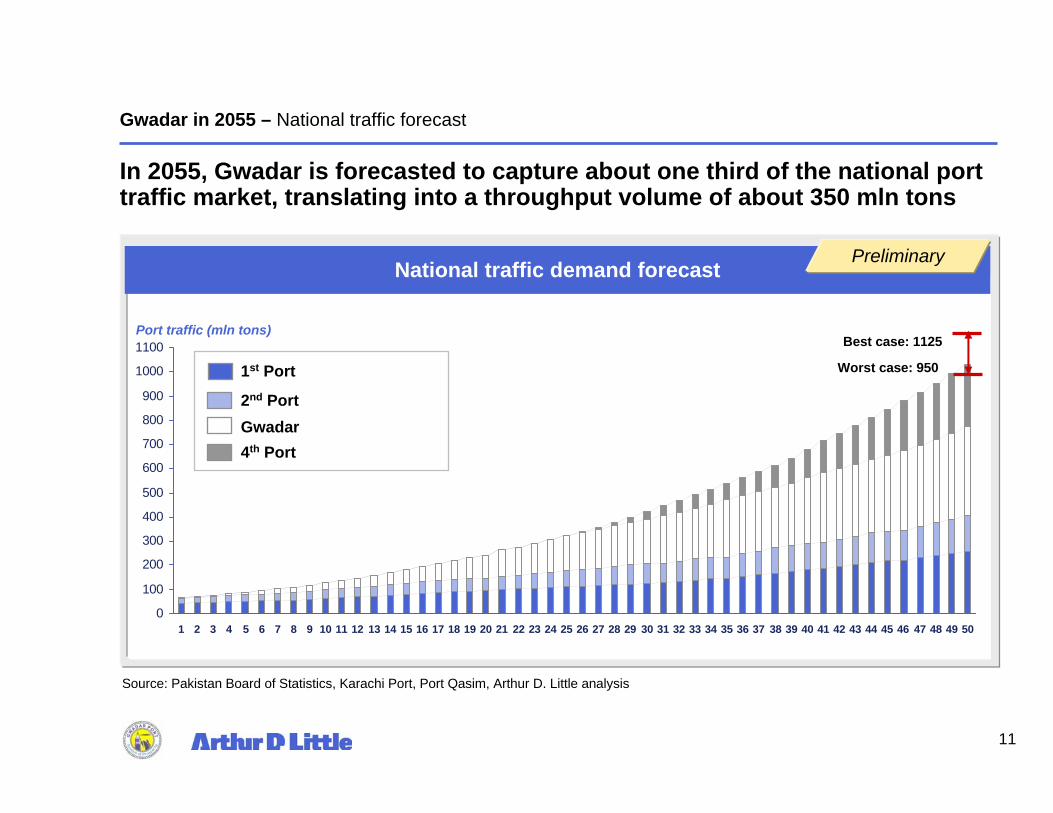

In 2055, Gwadar is forecasted to capture about one third of the national port traffic market, translating into a throughput volume of about 350 mln tons

Port traffic (mln tons)

National traffic demand forecast

Source: Pakistan Board of Statistics, Karachi Port, Port Qasim, Arthur D. Little analysis

1st Port

Best case: 1125

Worst case: 950

4th Port

Gwadar in 2055 – National traffic forecast

Preliminary

12

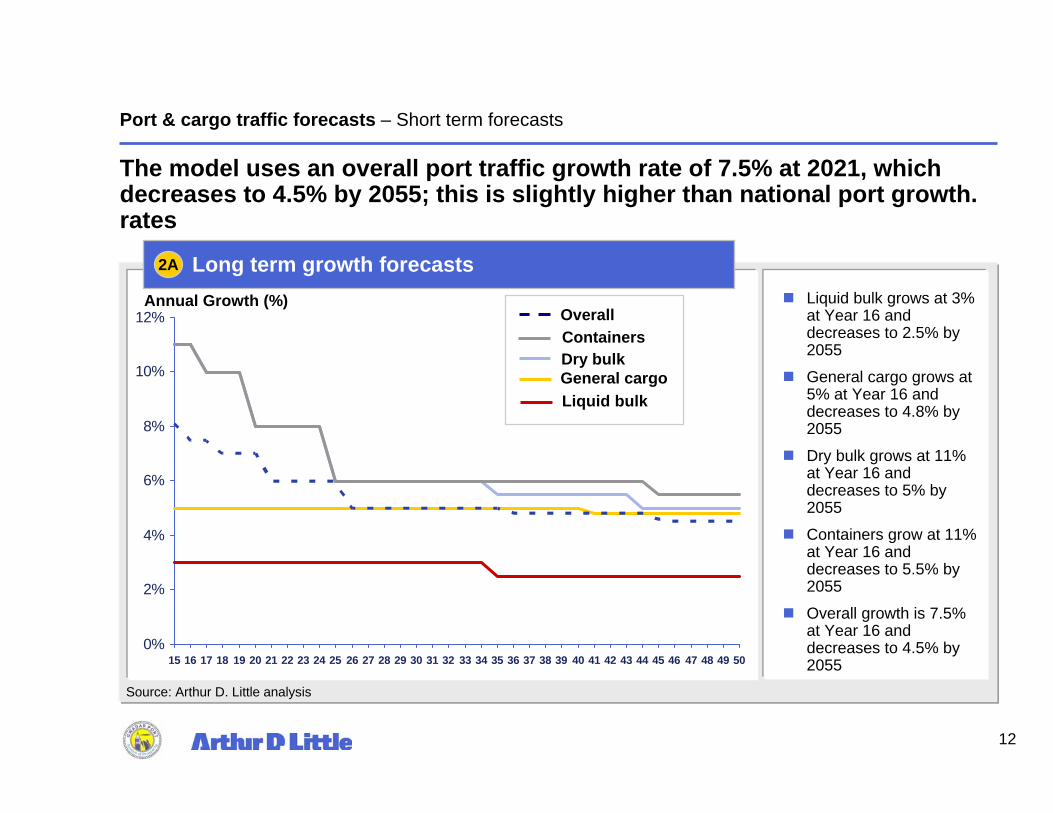

The model uses an overall port traffic growth rate of 7.5% at 2021, which decreases to 4.5% by 2055; this is slightly higher than national port growth. rates

0%

2%

4%

6%

8%

10%

12%

15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50

Long term growth forecasts

General cargo

Annual Growth (%)

Source: Arthur D. Little analysis

Liquid bulk grows at 3% at Year 16 and decreases to 2.5% by 2055

General cargo grows at 5% at Year 16 and decreases to 4.8% by 2055

Dry bulk grows at 11% at Year 16 and decreases to 5% by 2055

Containers grow at 11% at Year 16 and decreases to 5.5% by 2055

Overall growth is 7.5% at Year 16 and decreases to 4.5% by 2055

2A

Overall

Liquid bulk

Dry bulk Containers

Port & cargo traffic forecasts – Short term forecasts

13

Dry Bulk General Cargo Liquid Build Containers

Cargo Traffic (mio tons)

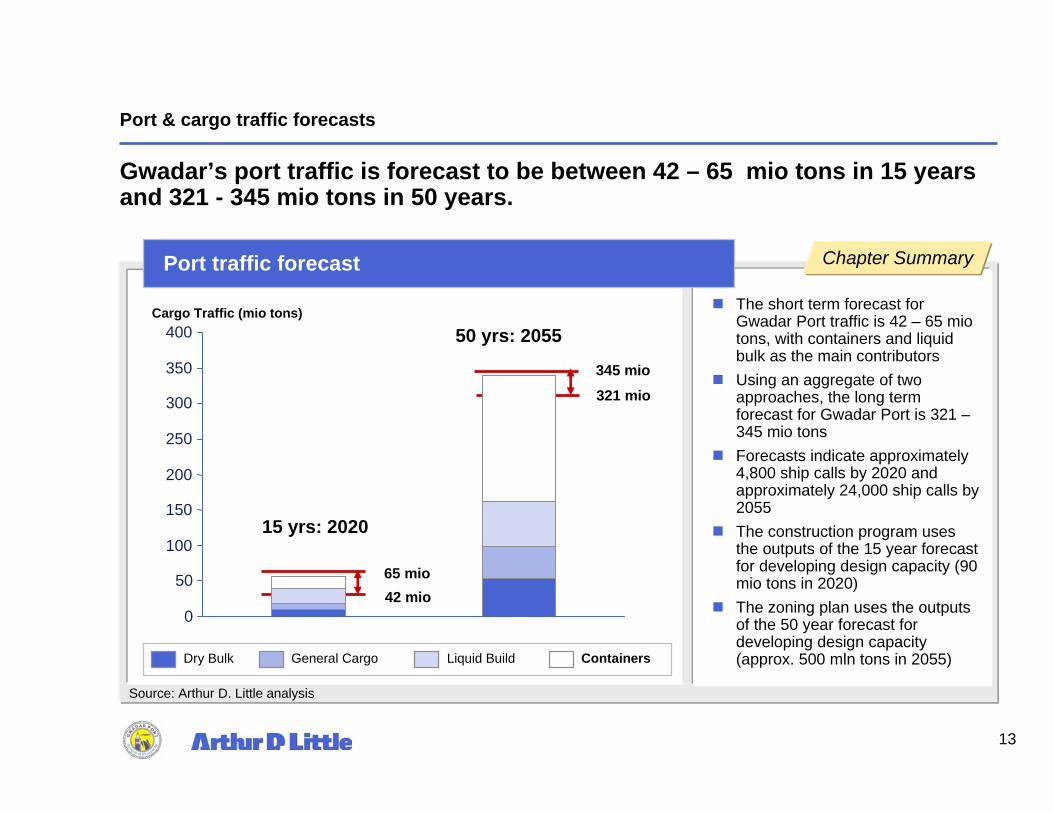

Gwadar’s port traffic is forecast to be between 42 – 65 mio tons in 15 years and 321 - 345 mio tons in 50 years.

Port & cargo traffic forecasts

65 mio42 mio

345 mio321 mio

The short term forecast for Gwadar Port traffic is 42 – 65 mio tons, with containers and liquid bulk as the main contributorsUsing an aggregate of two approaches, the long term forecast for Gwadar Port is 321 –345 mio tonsForecasts indicate approximately 4,800 ship calls by 2020 and approximately 24,000 ship calls by 2055The construction program uses the outputs of the 15 year forecast for developing design capacity (90 mio tons in 2020)The zoning plan uses the outputs of the 50 year forecast for developing design capacity (approx. 500 mln tons in 2055)

Port traffic forecast

Source: Arthur D. Little analysis

0

50

100

150

200

250

300

350

400

15 yrs: 2020

50 yrs: 2055

Chapter Summary

14

0

10

20

30

40

50

60

70

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Gwadar industry development

Transit trade

Transhipment

National ExIm

Cargo Traffic (mio tons)

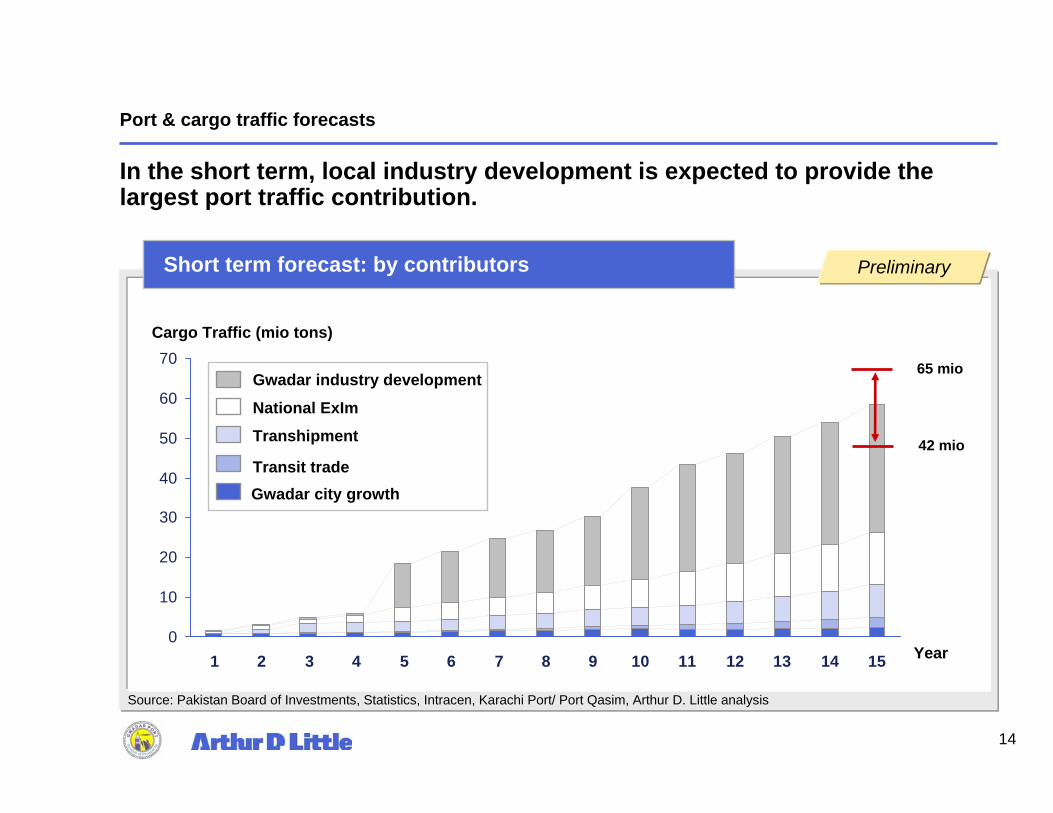

In the short term, local industry development is expected to provide the largest port traffic contribution.

Short term forecast: by contributors

Gwadar city growth

Source: Pakistan Board of Investments, Statistics, Intracen, Karachi Port/ Port Qasim, Arthur D. Little analysis

Year

65 mio

42 mio

Preliminary

Port & cargo traffic forecasts

15

0

10

20

30

40

50

60

70

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Liquid bulk

General cargo

Dry bulk

Cargo Traffic (mio tons)

Short term forecast: by cargo type

Containers

Source: Pakistan Board of Investments, Statistics, Intracen, Karachi Port/ Port Qasim, Arthur D. Little analysis

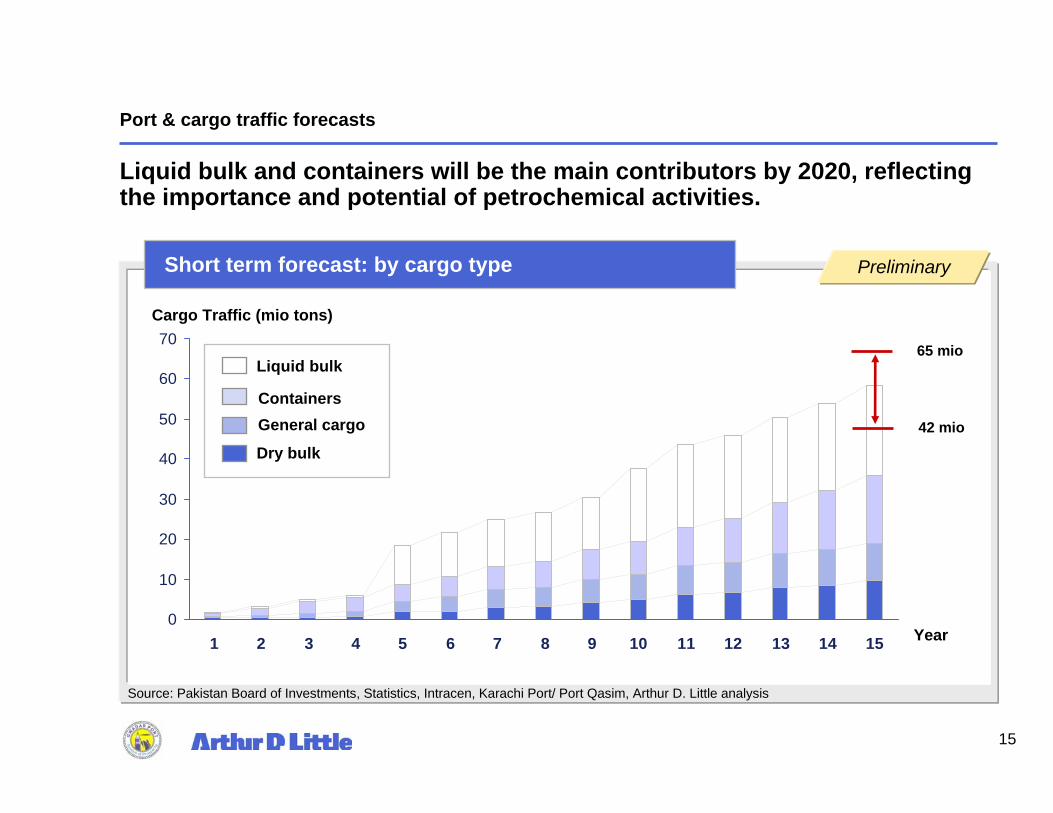

Liquid bulk and containers will be the main contributors by 2020, reflecting the importance and potential of petrochemical activities.

Year

65 mio

42 mio

Preliminary

Port & cargo traffic forecasts

16

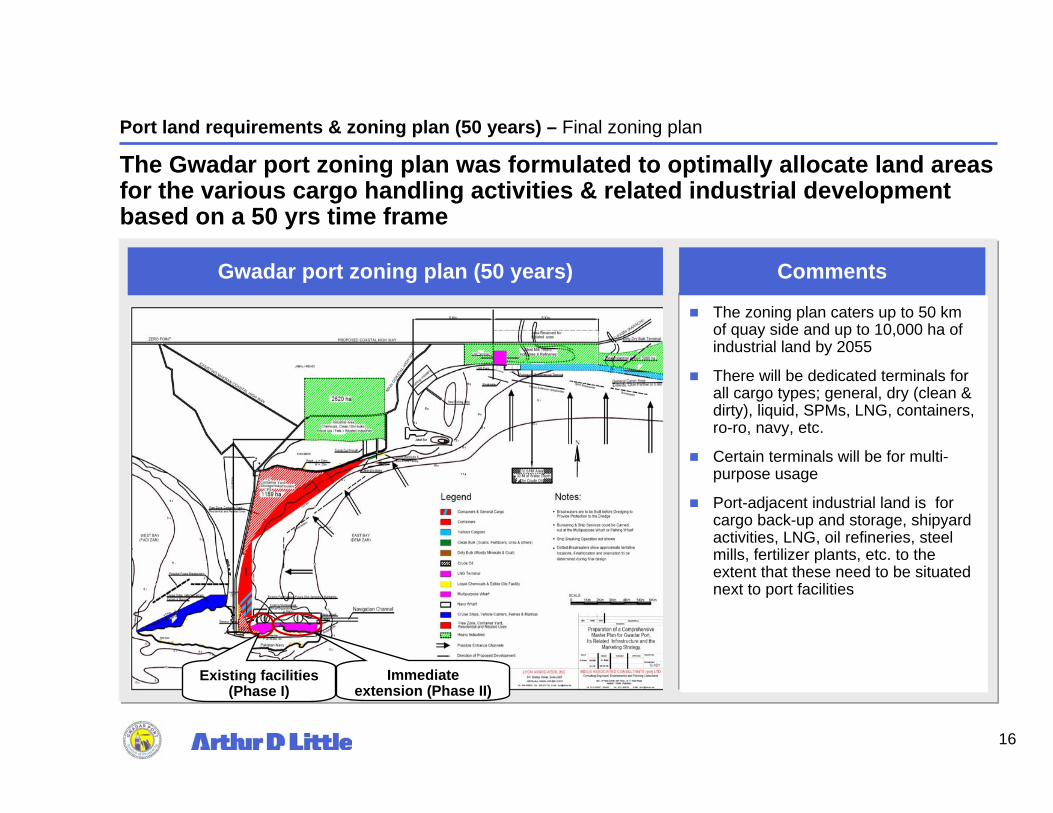

The Gwadar port zoning plan was formulated to optimally allocate land areas for the various cargo handling activities & related industrial development based on a 50 yrs time frame

The zoning plan caters up to 50 km of quay side and up to 10,000 ha of industrial land by 2055

There will be dedicated terminals for all cargo types; general, dry (clean & dirty), liquid, SPMs, LNG, containers, ro-ro, navy, etc.

Certain terminals will be for multi-purpose usage

Port-adjacent industrial land is for cargo back-up and storage, shipyard activities, LNG, oil refineries, steel mills, fertilizer plants, etc. to the extent that these need to be situated next to port facilities

CommentsGwadar port zoning plan (50 years)

Port land requirements & zoning plan (50 years) – Final zoning plan

Existing facilities (Phase I)

Immediate extension (Phase II)

17

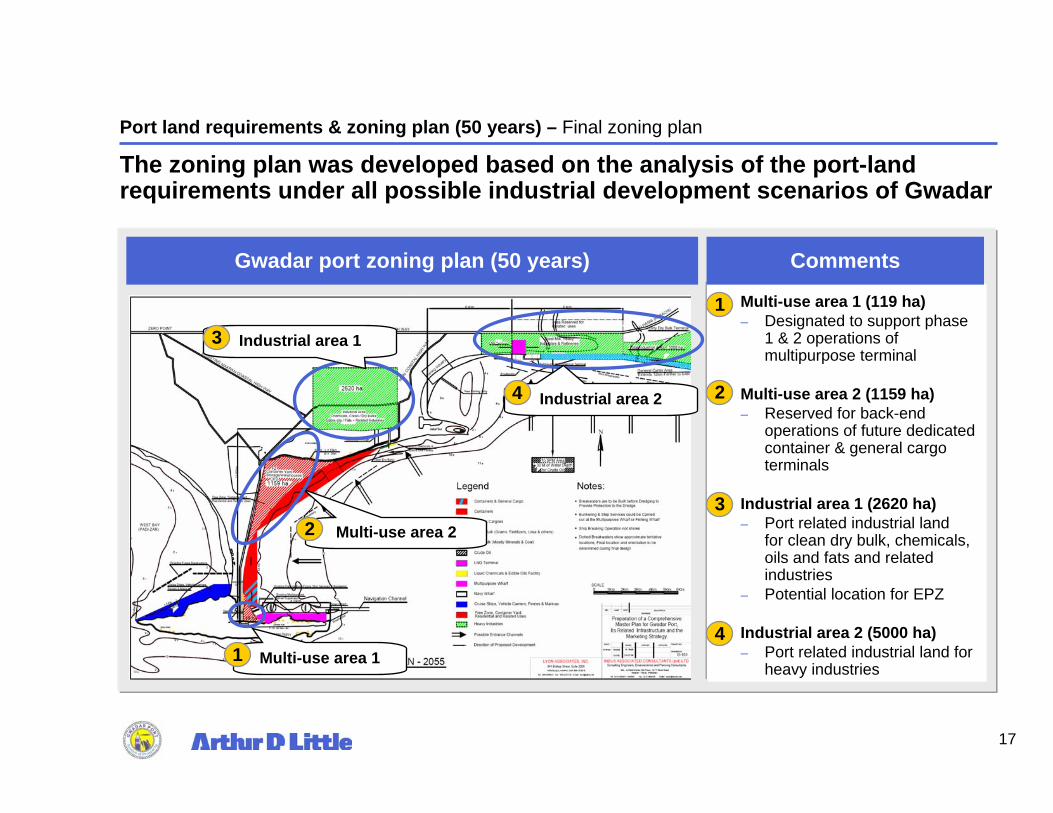

The zoning plan was developed based on the analysis of the port-land requirements under all possible industrial development scenarios of Gwadar

Multi-use area 1 (119 ha)– Designated to support phase

1 & 2 operations of multipurpose terminal

Multi-use area 2 (1159 ha)– Reserved for back-end

operations of future dedicated container & general cargo terminals

Industrial area 1 (2620 ha)– Port related industrial land

for clean dry bulk, chemicals, oils and fats and related industries

– Potential location for EPZ

Industrial area 2 (5000 ha)– Port related industrial land for

heavy industries

CommentsGwadar port zoning plan (50 years)

Port land requirements & zoning plan (50 years) – Final zoning plan

1

2

3

4

Multi-use area 2

Industrial area 1

Industrial area 2

3

4

2

Multi-use area 11

18

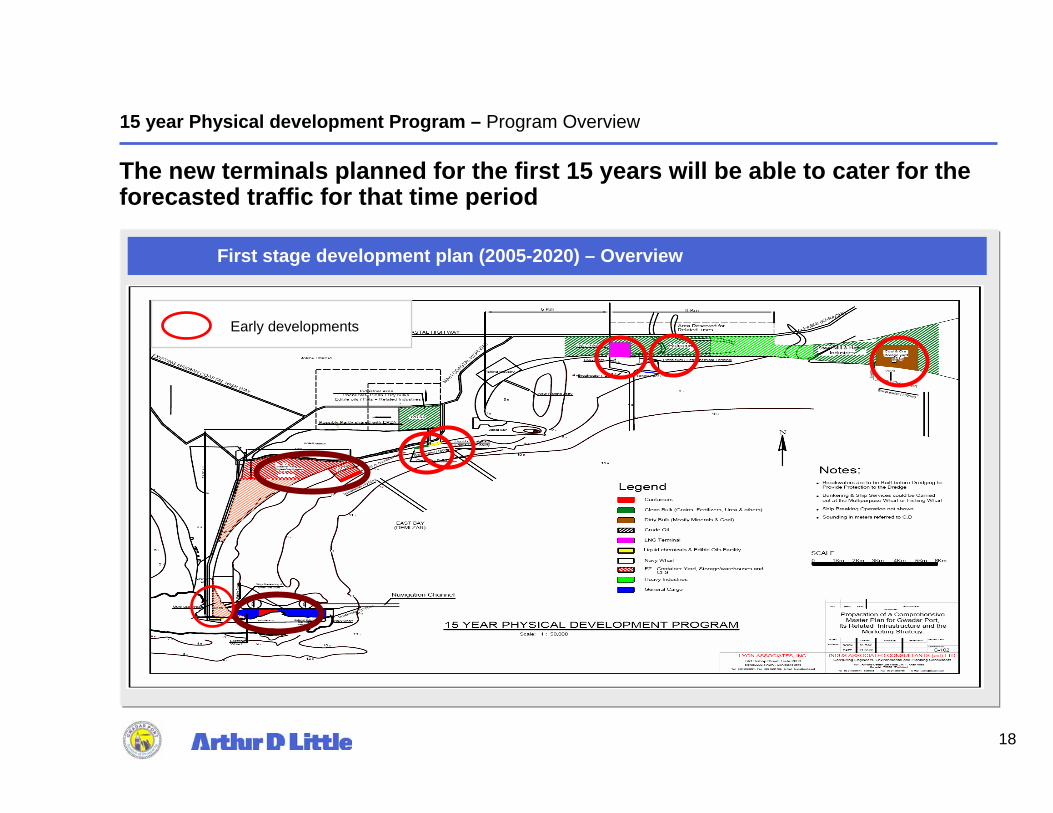

The new terminals planned for the first 15 years will be able to cater for the forecasted traffic for that time period

First stage development plan (2005-2020) – Overview

15 year Physical development Program – Program Overview

Early developments

19

The terminals planned for the first 15 years will be able to cater for the forecasted traffic for that time period

First Stage Development Plan (2005-2020) – Main facilities

Multipurpose terminal expansion to the east

Navy base at end of hammerheadConversion of the existing fishing wharf to provide bunkering and other ship servicesContainer terminal (northwest in East Bay)Free zone development adjacent to container terminalLiquid bulk terminal (for edible oils, chemicals etc) (northern end of East Bay)Clean dry bulk terminal (northern end of East Bay)LNG terminal (east of East Bay)Petroleum/ Petrochemical Terminal (east of East Bay)Dirty bulk terminal (east of East Bay)Four additional access channelsBreakwaters where needed

15 year Physical development Program – Program Overview

20

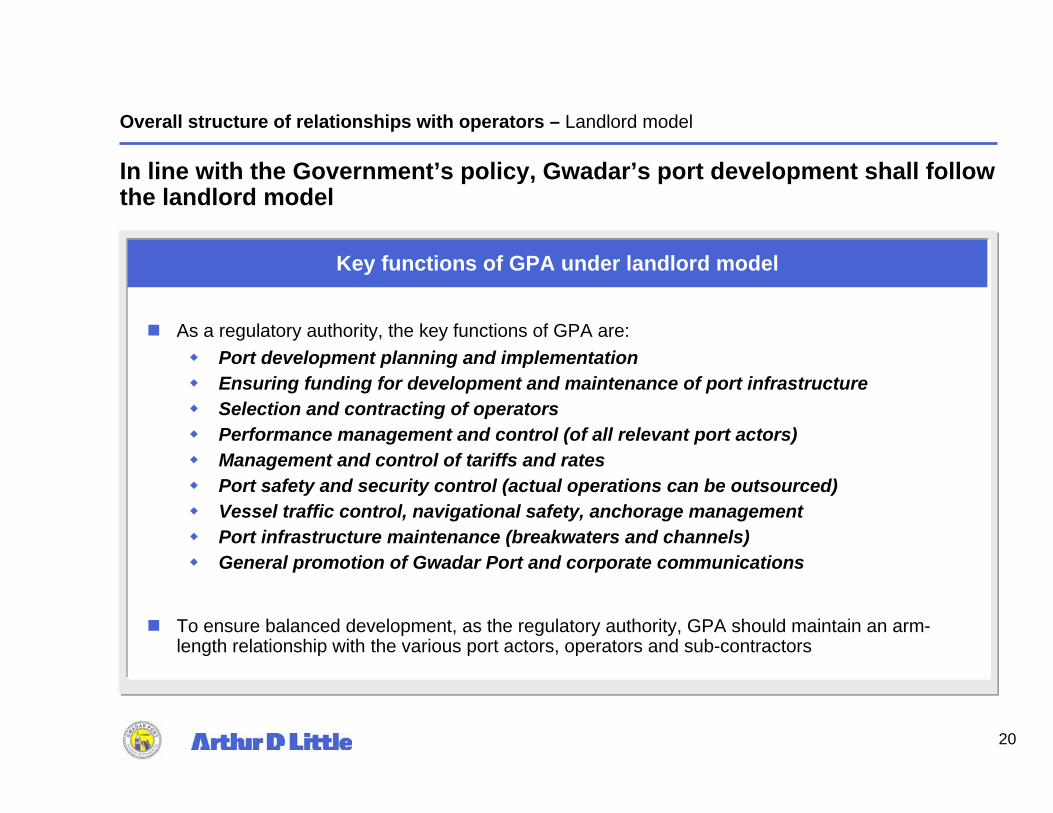

In line with the Government’s policy, Gwadar’s port development shall follow the landlord model

As a regulatory authority, the key functions of GPA are:Port development planning and implementation Ensuring funding for development and maintenance of port infrastructureSelection and contracting of operatorsPerformance management and control (of all relevant port actors)Management and control of tariffs and ratesPort safety and security control (actual operations can be outsourced)Vessel traffic control, navigational safety, anchorage management Port infrastructure maintenance (breakwaters and channels)General promotion of Gwadar Port and corporate communications

To ensure balanced development, as the regulatory authority, GPA should maintain an arm-length relationship with the various port actors, operators and sub-contractors

Key functions of GPA under landlord model

Overall structure of relationships with operators – Landlord model

21

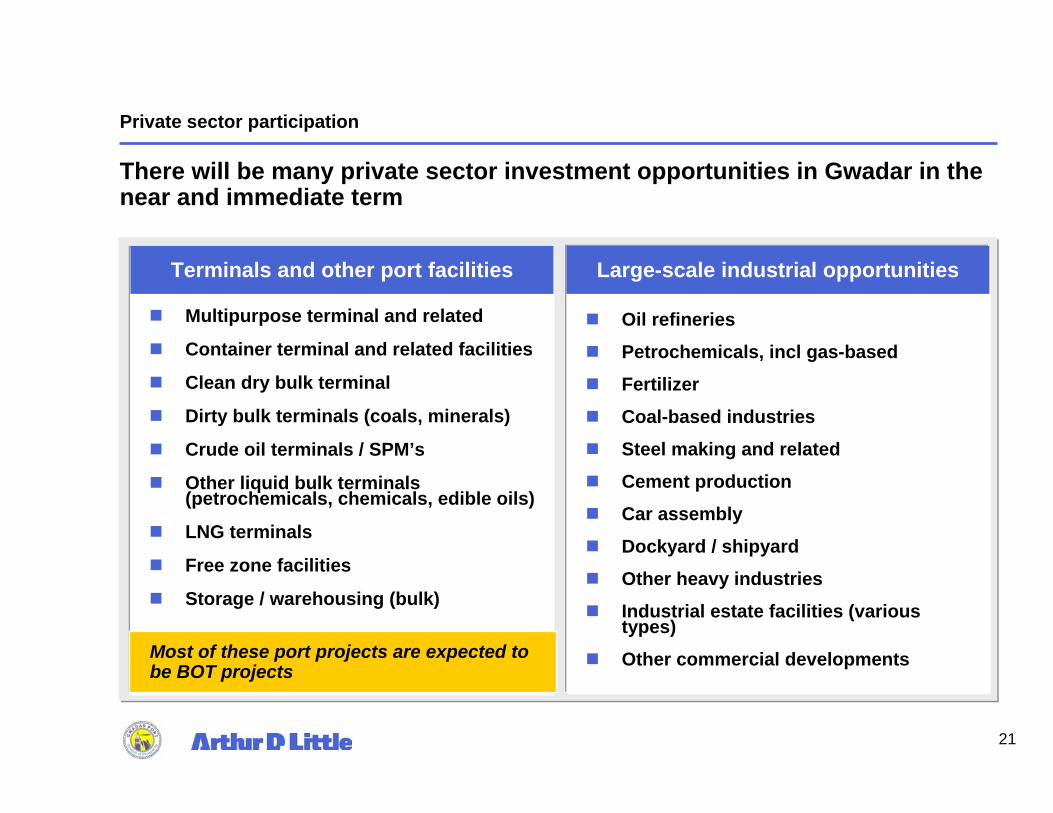

There will be many private sector investment opportunities in Gwadar in the near and immediate term

Oil refineries

Petrochemicals, incl gas-based

Fertilizer

Coal-based industries

Steel making and related

Cement production

Car assembly

Dockyard / shipyard

Other heavy industries

Industrial estate facilities (various types)

Other commercial developments

Large-scale industrial opportunities

Multipurpose terminal and related

Container terminal and related facilities

Clean dry bulk terminal

Dirty bulk terminals (coals, minerals)

Crude oil terminals / SPM’s

Other liquid bulk terminals (petrochemicals, chemicals, edible oils)

LNG terminals

Free zone facilities

Storage / warehousing (bulk)

Terminals and other port facilities

Private sector participation

Most of these port projects are expected to be BOT projects

22

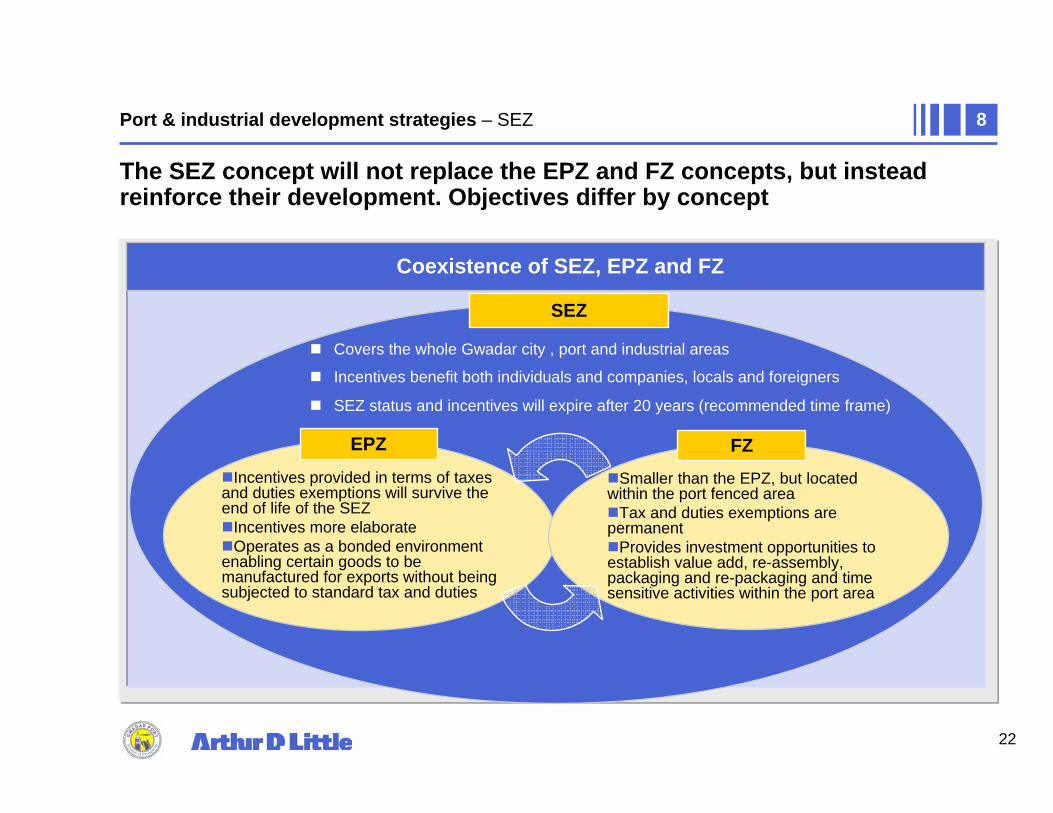

The SEZ concept will not replace the EPZ and FZ concepts, but instead reinforce their development. Objectives differ by concept

Coexistence of SEZ, EPZ and FZ

Incentives provided in terms of taxes and duties exemptions will survive the end of life of the SEZ

Incentives more elaborateOperates as a bonded environment

enabling certain goods to be manufactured for exports without being subjected to standard tax and duties

Smaller than the EPZ, but located within the port fenced area

Tax and duties exemptions are permanent

Provides investment opportunities to establish value add, re-assembly, packaging and re-packaging and time sensitive activities within the port area

Covers the whole Gwadar city , port and industrial areas

Incentives benefit both individuals and companies, locals and foreigners

SEZ status and incentives will expire after 20 years (recommended time frame)

EPZ FZ

SEZ

Port & industrial development strategies – SEZ 8

23

Integrated port & industrial development

Thank You