contentsdocshare01.docshare.tips/files/3879/38796930.pdf · premium adalah cost kepada option.....

TRANSCRIPT

1 | P a g e

Contents APRIL 2009 ........................................................................................................................................ 3

Question 1 ..................................................................................................................................... 3

Question 2 ..................................................................................................................................... 4

Question 3 ..................................................................................................................................... 5

Question 4 ..................................................................................................................................... 6

Question 5 ..................................................................................................................................... 7

Question 6 ..................................................................................................................................... 9

Question 7 ................................................................................................................................... 10

OCTOBER 2008 ................................................................................................................................ 11

Question 1 ................................................................................................................................... 11

Question 2 ................................................................................................................................... 12

Question 3 ................................................................................................................................... 13

Question 4 ................................................................................................................................... 13

Question 5 ................................................................................................................................... 14

Question 6 ................................................................................................................................... 16

Question 7 ................................................................................................................................... 17

APRIL 2008 ...................................................................................................................................... 19

Question 1 ................................................................................................................................... 19

Question 2 ................................................................................................................................... 20

Question 3 ................................................................................................................................... 22

Question 4 ................................................................................................................................... 23

Question 5 ................................................................................................................................... 23

Question 6 ................................................................................................................................... 24

Question 7 ................................................................................................................................... 25

OCTOBER 2007 ................................................................................................................................ 26

Question 1 ................................................................................................................................... 26

Question 2 ................................................................................................................................... 27

Question 3 ................................................................................................................................... 28

Question 4 ................................................................................................................................... 28

Question 5 ................................................................................................................................... 29

Question 6 ................................................................................................................................... 30

Question 7 ................................................................................................................................... 31

2 | P a g e

APRIL 2007 ...................................................................................................................................... 33

Question 1 ................................................................................................................................... 33

Question 2 ................................................................................................................................... 34

Question 3 ................................................................................................................................... 34

Question 4 ................................................................................................................................... 35

Question 5 ................................................................................................................................... 36

Question 6 ................................................................................................................................... 36

Question 7 ................................................................................................................................... 37

OCTOBER 2006 ................................................................................................................................ 39

Question 1 ................................................................................................................................... 39

Question 2 ................................................................................................................................... 40

Question 3 ................................................................................................................................... 42

Question 4 ................................................................................................................................... 43

Question 5 ................................................................................................................................... 44

Question 6 ................................................................................................................................... 44

Question 7 ................................................................................................................................... 45

APRIL 2006 ...................................................................................................................................... 46

Question 1 ................................................................................................................................... 46

Question 2 ................................................................................................................................... 46

Question 3 ................................................................................................................................... 46

Question 4 ................................................................................................................................... 46

Question 5 ................................................................................................................................... 47

Question 6 ................................................................................................................................... 47

Question 7 ................................................................................................................................... 47

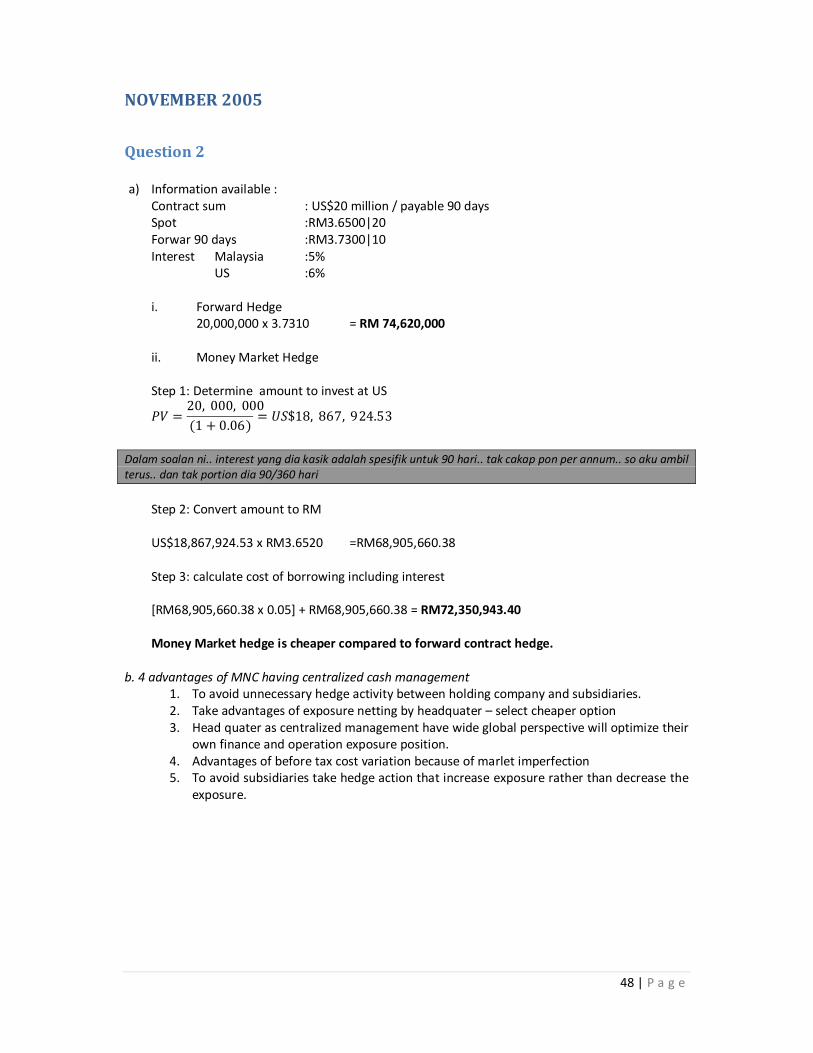

NOVEMBER 2005 ............................................................................................................................. 48

Question 2 ................................................................................................................................... 48

3 | P a g e

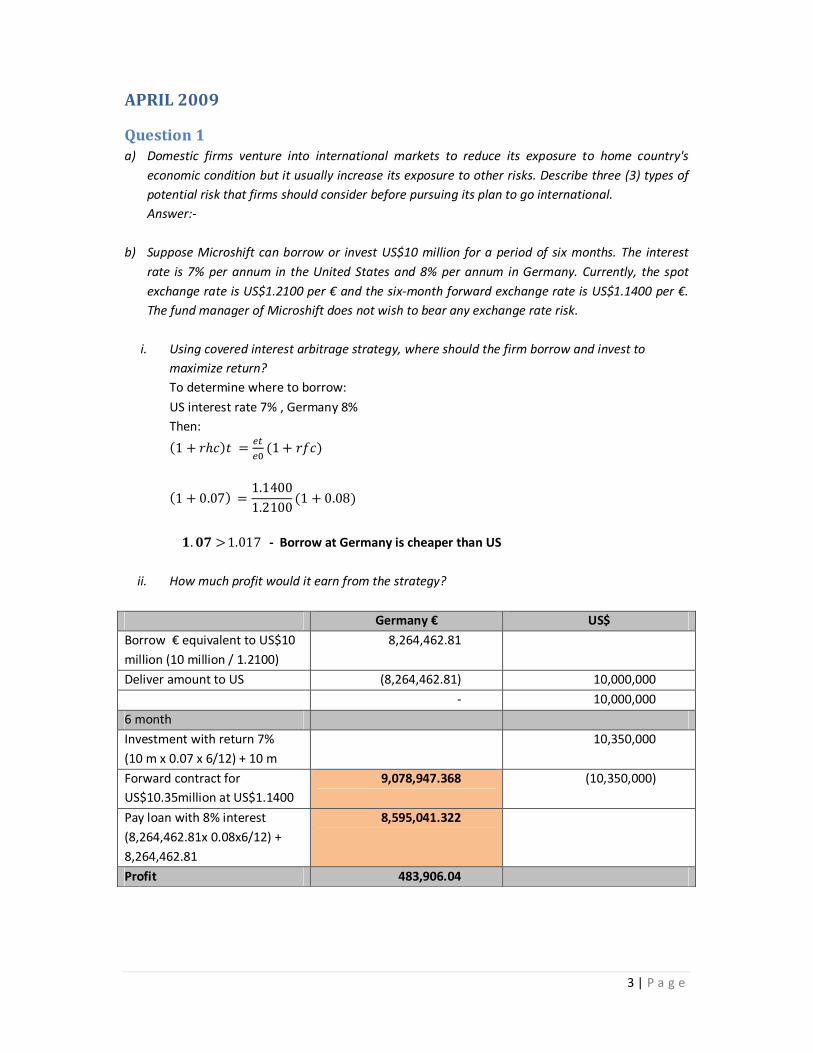

APRIL 2009

Question 1 a) Domestic firms venture into international markets to reduce its exposure to home country's

economic condition but it usually increase its exposure to other risks. Describe three (3) types of

potential risk that firms should consider before pursuing its plan to go international.

Answer:-

b) Suppose Microshift can borrow or invest US$10 million for a period of six months. The interest

rate is 7% per annum in the United States and 8% per annum in Germany. Currently, the spot

exchange rate is US$1.2100 per € and the six-month forward exchange rate is US$1.1400 per €.

The fund manager of Microshift does not wish to bear any exchange rate risk.

i. Using covered interest arbitrage strategy, where should the firm borrow and invest to

maximize return?

To determine where to borrow:

US interest rate 7% , Germany 8%

Then:

(1 + �ℎ�)� =��

��(1 + ���)

(1 + 0.07) =1.1400

1.2100(1 + 0.08)

�. �� > 1.017 - Borrow at Germany is cheaper than US

ii. How much profit would it earn from the strategy?

Germany € US$

Borrow € equivalent to US$10

million (10 million / 1.2100)

8,264,462.81

Deliver amount to US (8,264,462.81) 10,000,000

- 10,000,000

6 month

Investment with return 7%

(10 m x 0.07 x 6/12) + 10 m

10,350,000

Forward contract for

US$10.35million at US$1.1400

9,078,947.368 (10,350,000)

Pay loan with 8% interest

(8,264,462.81x 0.08x6/12) +

8,264,462.81

8,595,041.322

Profit 483,906.04

4 | P a g e

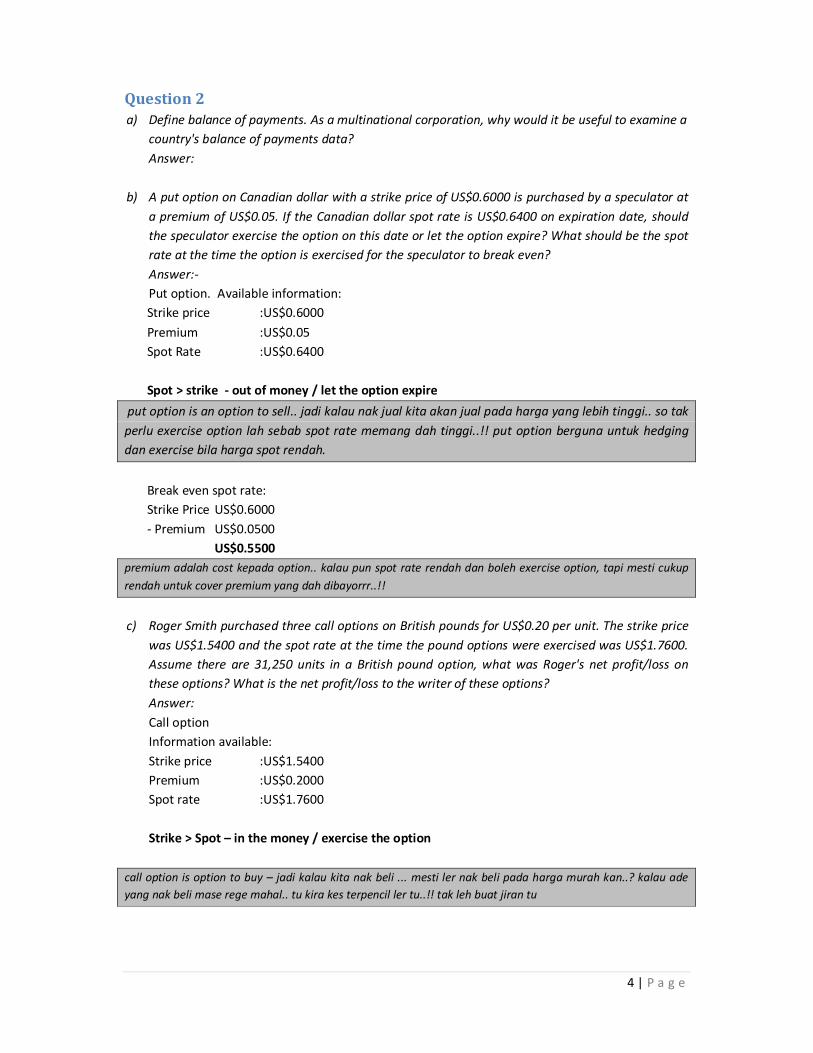

Question 2 a) Define balance of payments. As a multinational corporation, why would it be useful to examine a

country's balance of payments data?

Answer:

b) A put option on Canadian dollar with a strike price of US$0.6000 is purchased by a speculator at

a premium of US$0.05. If the Canadian dollar spot rate is US$0.6400 on expiration date, should

the speculator exercise the option on this date or let the option expire? What should be the spot

rate at the time the option is exercised for the speculator to break even?

Answer:-

Put option. Available information:

Strike price :US$0.6000

Premium :US$0.05

Spot Rate :US$0.6400

Spot > strike - out of money / let the option expire

put option is an option to sell.. jadi kalau nak jual kita akan jual pada harga yang lebih tinggi.. so tak

perlu exercise option lah sebab spot rate memang dah tinggi..!! put option berguna untuk hedging

dan exercise bila harga spot rendah.

Break even spot rate:

Strike Price US$0.6000

- Premium US$0.0500

US$0.5500

premium adalah cost kepada option.. kalau pun spot rate rendah dan boleh exercise option, tapi mesti cukup

rendah untuk cover premium yang dah dibayorrr..!!

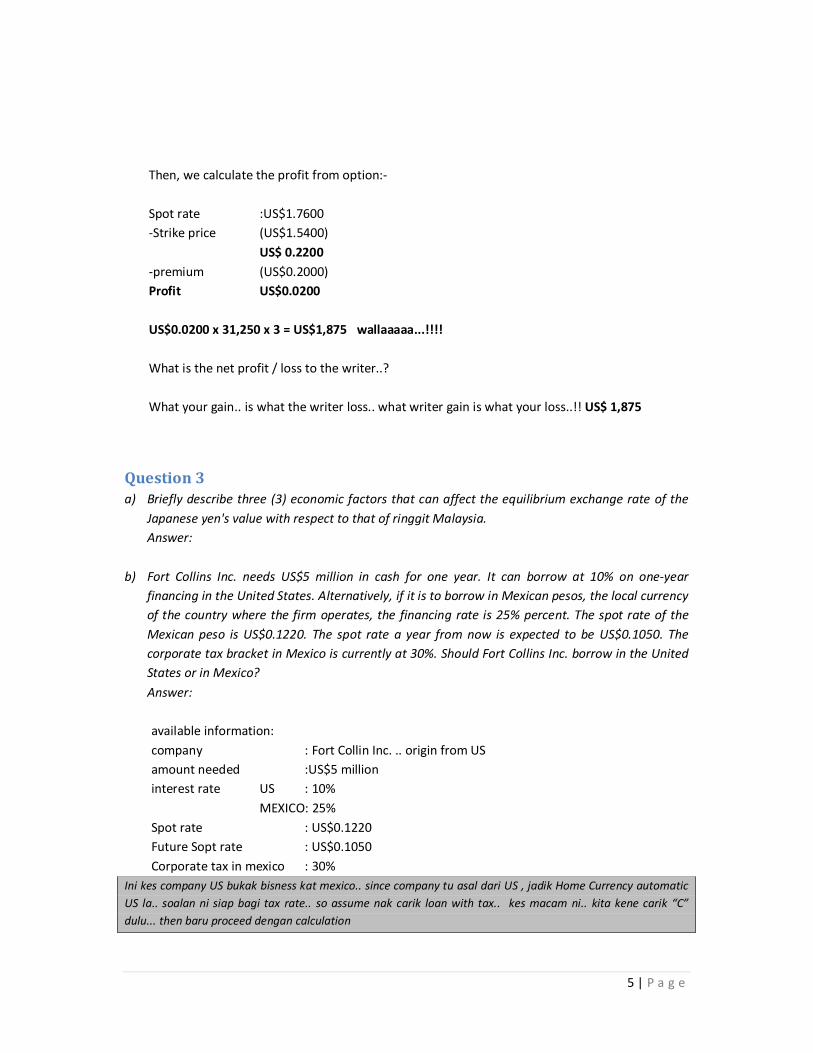

c) Roger Smith purchased three call options on British pounds for US$0.20 per unit. The strike price

was US$1.5400 and the spot rate at the time the pound options were exercised was US$1.7600.

Assume there are 31,250 units in a British pound option, what was Roger's net profit/loss on

these options? What is the net profit/loss to the writer of these options?

Answer:

Call option

Information available:

Strike price :US$1.5400

Premium :US$0.2000

Spot rate :US$1.7600

Strike > Spot – in the money / exercise the option

call option is option to buy – jadi kalau kita nak beli ... mesti ler nak beli pada harga murah kan..? kalau ade

yang nak beli mase rege mahal.. tu kira kes terpencil ler tu..!! tak leh buat jiran tu

5 | P a g e

Then, we calculate the profit from option:-

Spot rate :US$1.7600

-Strike price (US$1.5400)

US$ 0.2200

-premium (US$0.2000)

Profit US$0.0200

US$0.0200 x 31,250 x 3 = US$1,875 wallaaaaa...!!!!

What is the net profit / loss to the writer..?

What your gain.. is what the writer loss.. what writer gain is what your loss..!! US$ 1,875

Question 3 a) Briefly describe three (3) economic factors that can affect the equilibrium exchange rate of the

Japanese yen's value with respect to that of ringgit Malaysia.

Answer:

b) Fort Collins Inc. needs US$5 million in cash for one year. It can borrow at 10% on one-year

financing in the United States. Alternatively, if it is to borrow in Mexican pesos, the local currency

of the country where the firm operates, the financing rate is 25% percent. The spot rate of the

Mexican peso is US$0.1220. The spot rate a year from now is expected to be US$0.1050. The

corporate tax bracket in Mexico is currently at 30%. Should Fort Collins Inc. borrow in the United

States or in Mexico?

Answer:

available information:

company : Fort Collin Inc. .. origin from US

amount needed :US$5 million

interest rate US : 10%

MEXICO: 25%

Spot rate : US$0.1220

Future Sopt rate : US$0.1050

Corporate tax in mexico : 30%

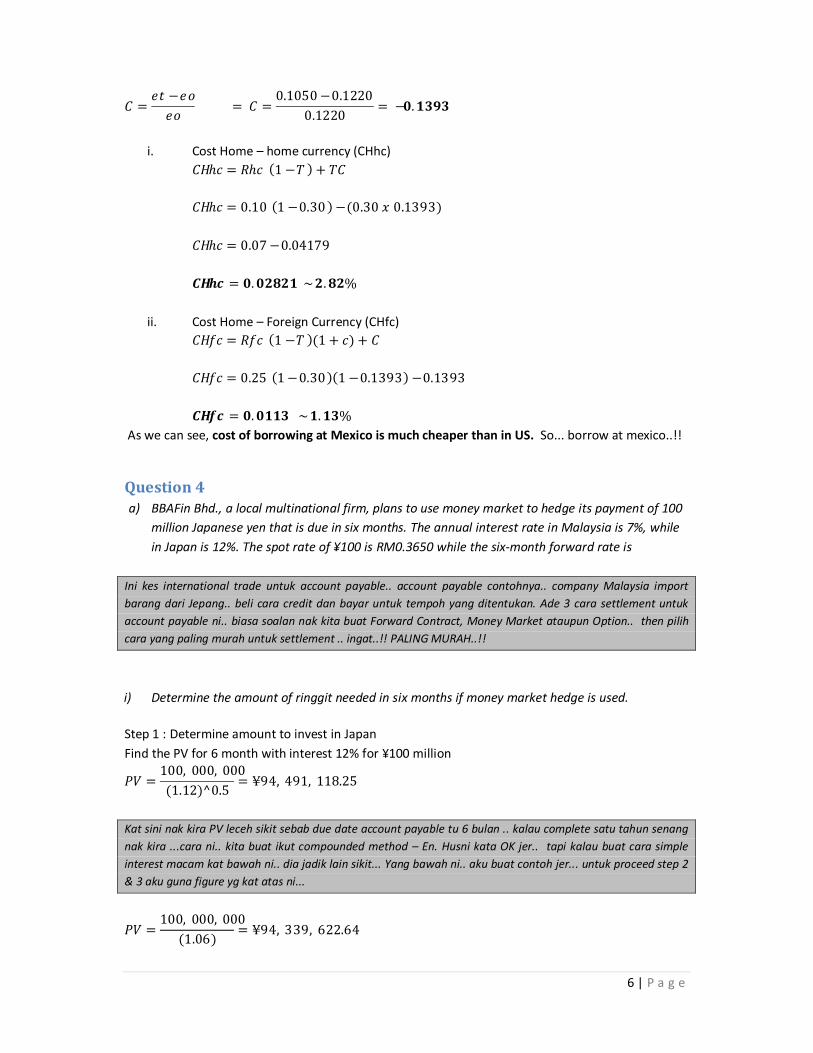

Ini kes company US bukak bisness kat mexico.. since company tu asal dari US , jadik Home Currency automatic

US la.. soalan ni siap bagi tax rate.. so assume nak carik loan with tax.. kes macam ni.. kita kene carik “C”

dulu... then baru proceed dengan calculation

6 | P a g e

� =�� − ��

�� = � =

0.1050 − 0.1220

0.1220= −�. ����

i. Cost Home – home currency (CHhc)

��ℎ� = �ℎ� (1 − � ) + ��

��ℎ� = 0.10 (1 − 0.30 ) − (0.30 � 0.1393)

��ℎ� = 0.07 − 0.04179

���� = �. ����� ~ �. ��%

ii. Cost Home – Foreign Currency (CHfc)

���� = ��� (1 − � )(1 + �) + �

���� = 0.25 (1 − 0.30)(1 − 0.1393) − 0.1393

���� = �. ���� ~ �. ��%

As we can see, cost of borrowing at Mexico is much cheaper than in US. So... borrow at mexico..!!

Question 4 a) BBAFin Bhd., a local multinational firm, plans to use money market to hedge its payment of 100

million Japanese yen that is due in six months. The annual interest rate in Malaysia is 7%, while

in Japan is 12%. The spot rate of ¥100 is RM0.3650 while the six-month forward rate is

Ini kes international trade untuk account payable.. account payable contohnya.. company Malaysia import

barang dari Jepang.. beli cara credit dan bayar untuk tempoh yang ditentukan. Ade 3 cara settlement untuk

account payable ni.. biasa soalan nak kita buat Forward Contract, Money Market ataupun Option.. then pilih

cara yang paling murah untuk settlement .. ingat..!! PALING MURAH..!!

i) Determine the amount of ringgit needed in six months if money market hedge is used.

Step 1 : Determine amount to invest in Japan

Find the PV for 6 month with interest 12% for ¥100 million

�� =100,000,000

(1.12)^0.5= ¥94,491,118.25

Kat sini nak kira PV leceh sikit sebab due date account payable tu 6 bulan .. kalau complete satu tahun senang

nak kira ...cara ni.. kita buat ikut compounded method – En. Husni kata OK jer.. tapi kalau buat cara simple

interest macam kat bawah ni.. dia jadik lain sikit... Yang bawah ni.. aku buat contoh jer... untuk proceed step 2

& 3 aku guna figure yg kat atas ni...

�� =100,000,000

(1.06)= ¥94,339,622.64

7 | P a g e

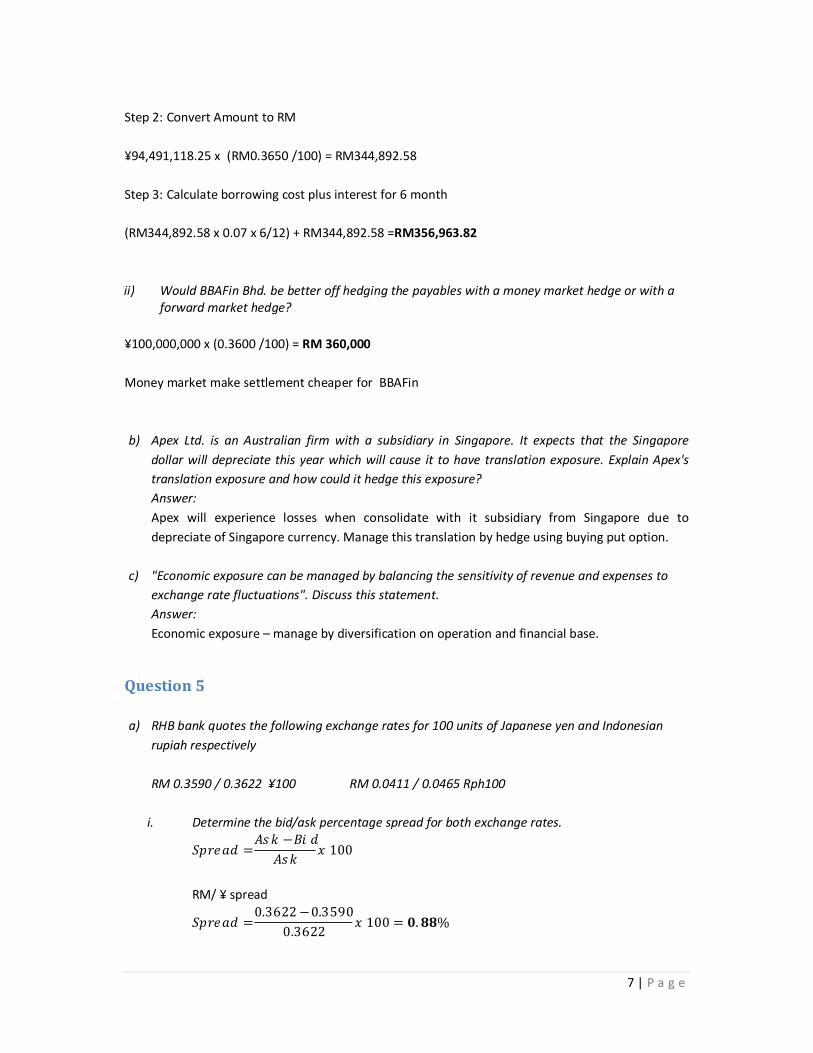

Step 2: Convert Amount to RM

¥94,491,118.25 x (RM0.3650 /100) = RM344,892.58

Step 3: Calculate borrowing cost plus interest for 6 month

(RM344,892.58 x 0.07 x 6/12) + RM344,892.58 =RM356,963.82

ii) Would BBAFin Bhd. be better off hedging the payables with a money market hedge or with a forward market hedge?

¥100,000,000 x (0.3600 /100) = RM 360,000

Money market make settlement cheaper for BBAFin

b) Apex Ltd. is an Australian firm with a subsidiary in Singapore. It expects that the Singapore

dollar will depreciate this year which will cause it to have translation exposure. Explain Apex's

translation exposure and how could it hedge this exposure?

Answer:

Apex will experience losses when consolidate with it subsidiary from Singapore due to

depreciate of Singapore currency. Manage this translation by hedge using buying put option.

c) "Economic exposure can be managed by balancing the sensitivity of revenue and expenses to

exchange rate fluctuations". Discuss this statement.

Answer:

Economic exposure – manage by diversification on operation and financial base.

Question 5

a) RHB bank quotes the following exchange rates for 100 units of Japanese yen and Indonesian

rupiah respectively

RM 0.3590 / 0.3622 ¥100 RM 0.0411 / 0.0465 Rph100

i. Determine the bid/ask percentage spread for both exchange rates.

������ =��� − ���

���� 100

RM/ ¥ spread

������ =0.3622 − 0.3590

0.3622� 100 = �. ��%

8 | P a g e

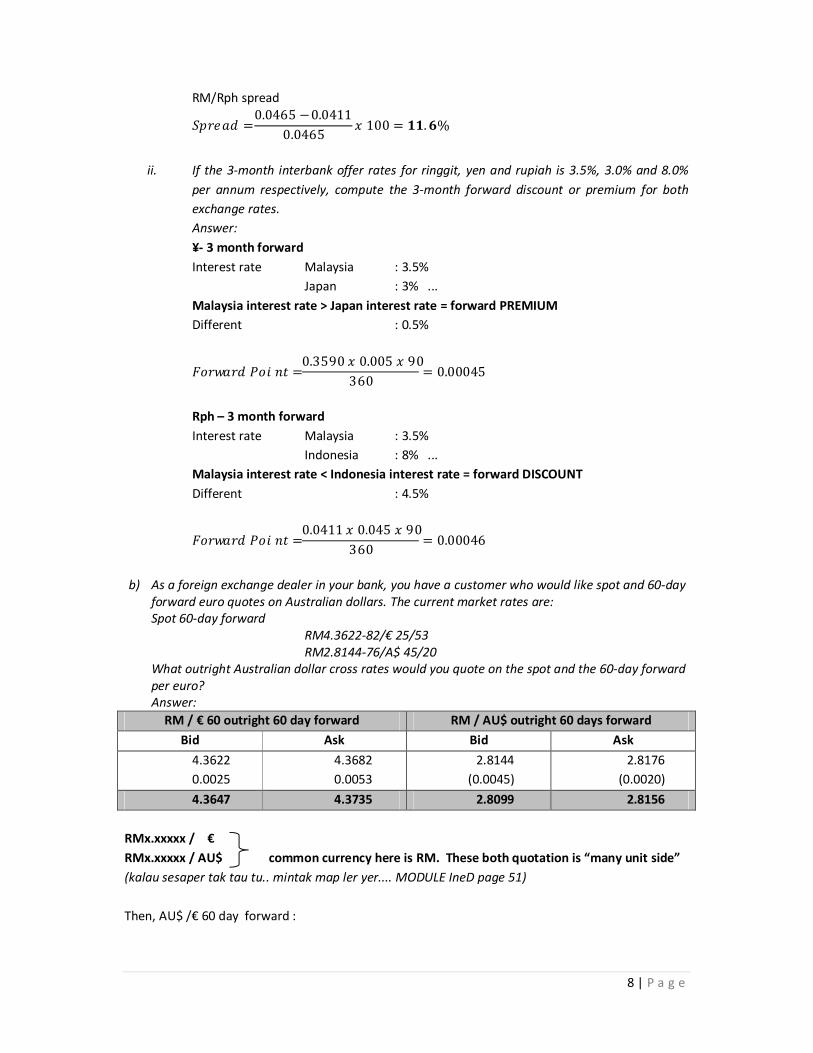

RM/Rph spread

������ =0.0465 − 0.0411

0.0465� 100 = ��. �%

ii. If the 3-month interbank offer rates for ringgit, yen and rupiah is 3.5%, 3.0% and 8.0%

per annum respectively, compute the 3-month forward discount or premium for both

exchange rates.

Answer:

¥- 3 month forward

Interest rate Malaysia : 3.5%

Japan : 3% ...

Malaysia interest rate > Japan interest rate = forward PREMIUM

Different : 0.5%

������� ����� =0.3590 � 0.005 � 90

360= 0.00045

Rph – 3 month forward

Interest rate Malaysia : 3.5%

Indonesia : 8% ...

Malaysia interest rate < Indonesia interest rate = forward DISCOUNT

Different : 4.5%

������� ����� =0.0411 � 0.045 � 90

360= 0.00046

b) As a foreign exchange dealer in your bank, you have a customer who would like spot and 60-day forward euro quotes on Australian dollars. The current market rates are: Spot 60-day forward

RM4.3622-82/€ 25/53 RM2.8144-76/A$ 45/20

What outright Australian dollar cross rates would you quote on the spot and the 60-day forward per euro? Answer:

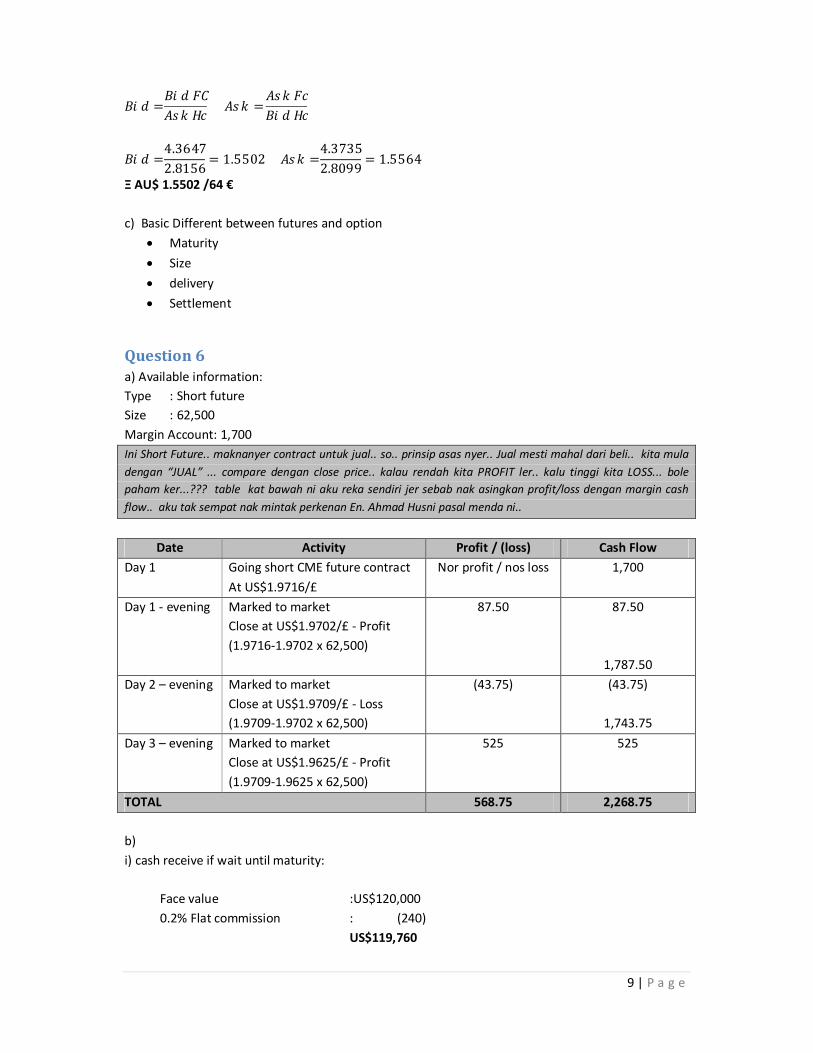

RM / € 60 outright 60 day forward RM / AU$ outright 60 days forward

Bid Ask Bid Ask

4.3622

0.0025

4.3682

0.0053

2.8144

(0.0045)

2.8176

(0.0020)

4.3647 4.3735 2.8099 2.8156

RMx.xxxxx / €

RMx.xxxxx / AU$ common currency here is RM. These both quotation is “many unit side”

(kalau sesaper tak tau tu.. mintak map ler yer.... MODULE IneD page 51)

Then, AU$ /€ 60 day forward :

9 | P a g e

��� =��� ��

��� �� ��� =

��� ��

��� ��

��� =4.3647

2.8156= 1.5502 ��� =

4.3735

2.8099= 1.5564

Ξ AU$ 1.5502 /64 €

c) Basic Different between futures and option

Maturity

Size

delivery

Settlement

Question 6 a) Available information:

Type : Short future

Size : 62,500

Margin Account: 1,700

Ini Short Future.. maknanyer contract untuk jual.. so.. prinsip asas nyer.. Jual mesti mahal dari beli.. kita mula

dengan “JUAL” ... compare dengan close price.. kalau rendah kita PROFIT ler.. kalu tinggi kita LOSS... bole

paham ker...??? table kat bawah ni aku reka sendiri jer sebab nak asingkan profit/loss dengan margin cash

flow.. aku tak sempat nak mintak perkenan En. Ahmad Husni pasal menda ni..

Date Activity Profit / (loss) Cash Flow

Day 1 Going short CME future contract

At US$1.9716/£

Nor profit / nos loss 1,700

Day 1 - evening Marked to market

Close at US$1.9702/£ - Profit

(1.9716-1.9702 x 62,500)

87.50 87.50

1,787.50

Day 2 – evening Marked to market

Close at US$1.9709/£ - Loss

(1.9709-1.9702 x 62,500)

(43.75) (43.75)

1,743.75

Day 3 – evening Marked to market

Close at US$1.9625/£ - Profit

(1.9709-1.9625 x 62,500)

525 525

TOTAL 568.75 2,268.75

b)

i) cash receive if wait until maturity:

Face value :US$120,000

0.2% Flat commission : (240)

US$119,760

10 | P a g e

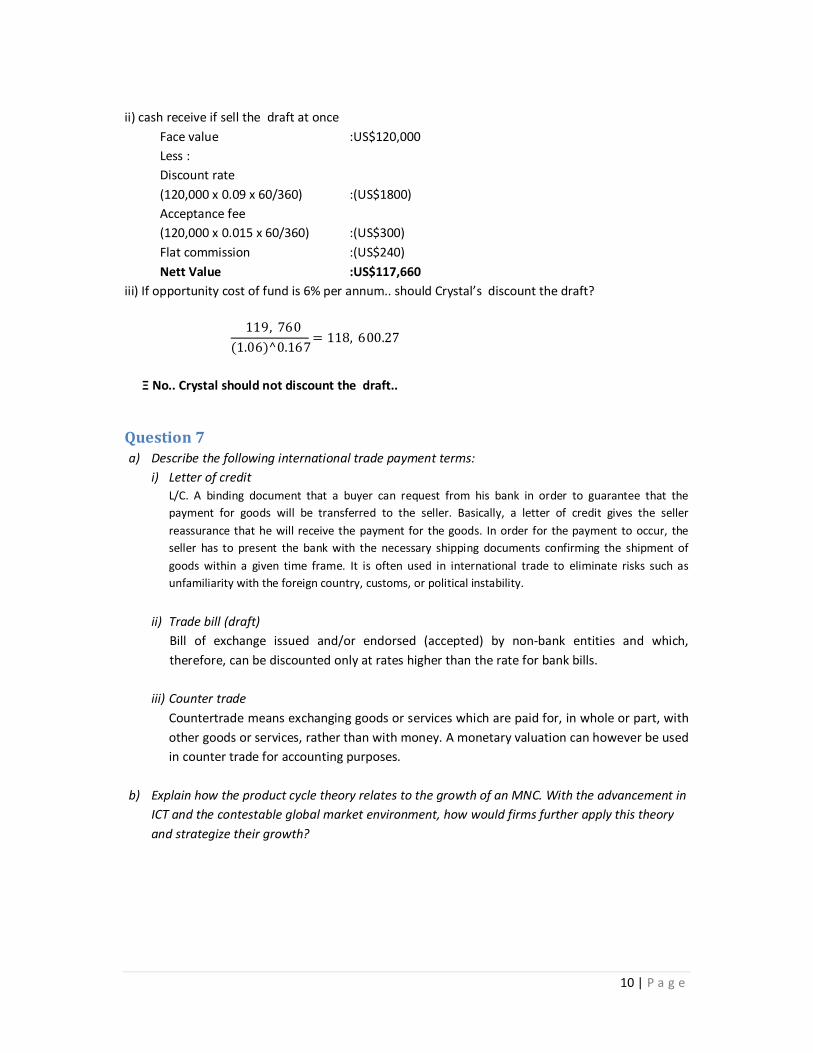

ii) cash receive if sell the draft at once

Face value :US$120,000

Less :

Discount rate

(120,000 x 0.09 x 60/360) :(US$1800)

Acceptance fee

(120,000 x 0.015 x 60/360) :(US$300)

Flat commission :(US$240)

Nett Value :US$117,660

iii) If opportunity cost of fund is 6% per annum.. should Crystal’s discount the draft?

119,760

(1.06)^0.167= 118,600.27

Ξ No.. Crystal should not discount the draft..

Question 7 a) Describe the following international trade payment terms:

i) Letter of credit

L/C. A binding document that a buyer can request from his bank in order to guarantee that the

payment for goods will be transferred to the seller. Basically, a letter of credit gives the seller

reassurance that he will receive the payment for the goods. In order for the payment to occur, the

seller has to present the bank with the necessary shipping documents confirming the shipment of

goods within a given time frame. It is often used in international trade to eliminate risks such as

unfamiliarity with the foreign country, customs, or political instability.

ii) Trade bill (draft)

Bill of exchange issued and/or endorsed (accepted) by non-bank entities and which,

therefore, can be discounted only at rates higher than the rate for bank bills.

iii) Counter trade

Countertrade means exchanging goods or services which are paid for, in whole or part, with

other goods or services, rather than with money. A monetary valuation can however be used

in counter trade for accounting purposes.

b) Explain how the product cycle theory relates to the growth of an MNC. With the advancement in

ICT and the contestable global market environment, how would firms further apply this theory

and strategize their growth?

11 | P a g e

OCTOBER 2008

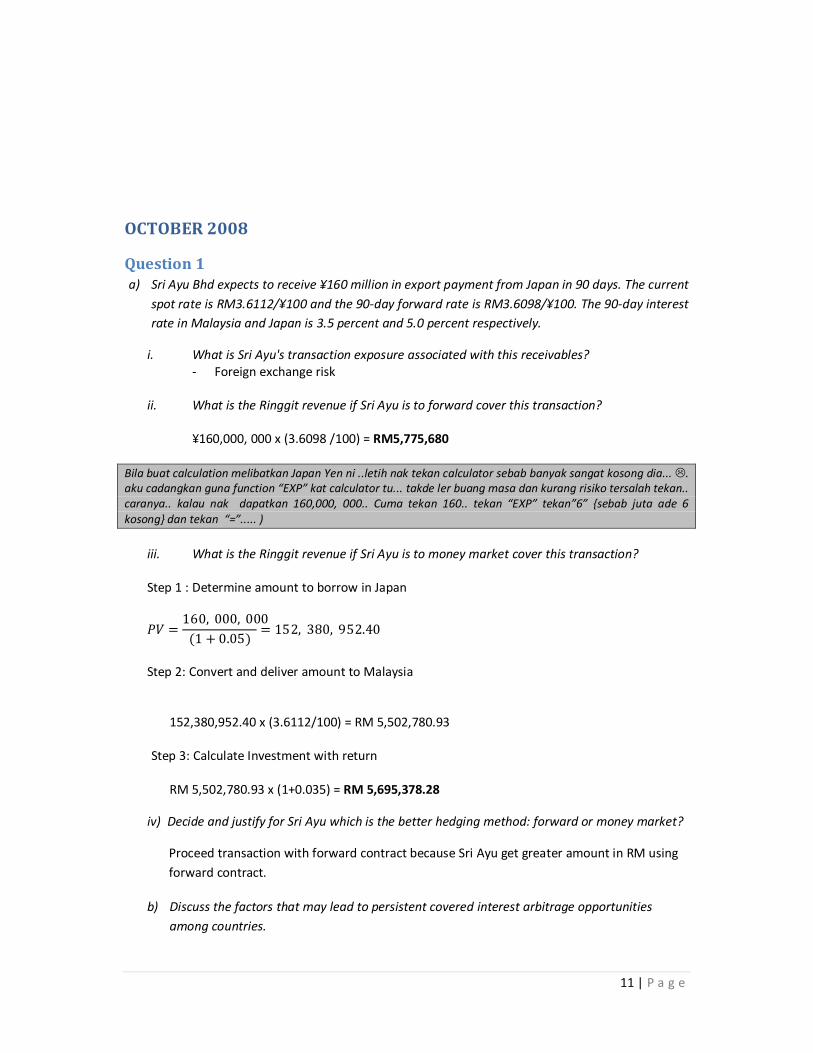

Question 1 a) Sri Ayu Bhd expects to receive ¥160 million in export payment from Japan in 90 days. The current

spot rate is RM3.6112/¥100 and the 90-day forward rate is RM3.6098/¥100. The 90-day interest

rate in Malaysia and Japan is 3.5 percent and 5.0 percent respectively.

i. What is Sri Ayu's transaction exposure associated with this receivables? - Foreign exchange risk

ii. What is the Ringgit revenue if Sri Ayu is to forward cover this transaction?

¥160,000, 000 x (3.6098 /100) = RM5,775,680

Bila buat calculation melibatkan Japan Yen ni ..letih nak tekan calculator sebab banyak sangat kosong dia... . aku cadangkan guna function “EXP” kat calculator tu... takde ler buang masa dan kurang risiko tersalah tekan.. caranya.. kalau nak dapatkan 160,000, 000.. Cuma tekan 160.. tekan “EXP” tekan”6” {sebab juta ade 6 kosong} dan tekan “=”..... )

iii. What is the Ringgit revenue if Sri Ayu is to money market cover this transaction? Step 1 : Determine amount to borrow in Japan

�� =160,000,000

(1 + 0.05)= 152,380,952.40

Step 2: Convert and deliver amount to Malaysia

152,380,952.40 x (3.6112/100) = RM 5,502,780.93

Step 3: Calculate Investment with return

RM 5,502,780.93 x (1+0.035) = RM 5,695,378.28

iv) Decide and justify for Sri Ayu which is the better hedging method: forward or money market?

Proceed transaction with forward contract because Sri Ayu get greater amount in RM using

forward contract.

b) Discuss the factors that may lead to persistent covered interest arbitrage opportunities

among countries.

12 | P a g e

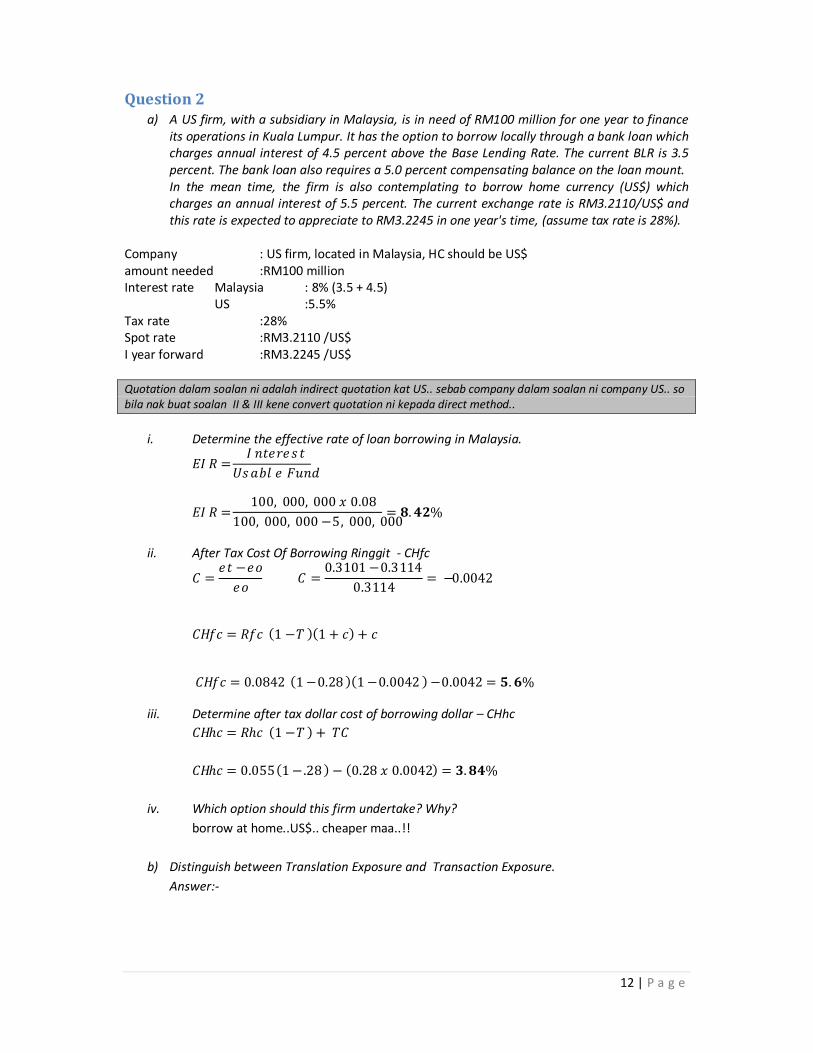

Question 2 a) A US firm, with a subsidiary in Malaysia, is in need of RM100 million for one year to finance

its operations in Kuala Lumpur. It has the option to borrow locally through a bank loan which charges annual interest of 4.5 percent above the Base Lending Rate. The current BLR is 3.5 percent. The bank loan also requires a 5.0 percent compensating balance on the loan mount. In the mean time, the firm is also contemplating to borrow home currency (US$) which charges an annual interest of 5.5 percent. The current exchange rate is RM3.2110/US$ and this rate is expected to appreciate to RM3.2245 in one year's time, (assume tax rate is 28%).

Company : US firm, located in Malaysia, HC should be US$ amount needed :RM100 million Interest rate Malaysia : 8% (3.5 + 4.5) US :5.5% Tax rate :28% Spot rate :RM3.2110 /US$ I year forward :RM3.2245 /US$ Quotation dalam soalan ni adalah indirect quotation kat US.. sebab company dalam soalan ni company US.. so bila nak buat soalan II & III kene convert quotation ni kepada direct method..

i. Determine the effective rate of loan borrowing in Malaysia.

��� =��������

������ ����

��� =100,000,000 � 0.08

100,000,000 − 5,000,000= �. ��%

ii. After Tax Cost Of Borrowing Ringgit - CHfc

� =�� − ��

�� � =

0.3101 − 0.3114

0.3114= −0.0042

���� = ��� (1 − � )(1 + �) + �

���� = 0.0842 (1 − 0.28 )(1 − 0.0042 ) − 0.0042 = �. �%

iii. Determine after tax dollar cost of borrowing dollar – CHhc

��ℎ� = �ℎ� (1 − � ) + ��

��ℎ� = 0.055(1 − .28 ) − (0.28 � 0.0042) = �. ��%

iv. Which option should this firm undertake? Why?

borrow at home..US$.. cheaper maa..!!

b) Distinguish between Translation Exposure and Transaction Exposure.

Answer:-

13 | P a g e

Question 3 a) Balance of Payment is considered one of the key indicators for a country's economic and

financial performance. Describe in detailed the three main accounts in a country's Balance of

Payment. Explain the factors that can directly affect these accounts.

Answer:-

b) Which is likely to be higher, a 120% Rupiah return in Indonesia or a 12% dollar return in the

United States?

Answer:-

c) The interest rate in Malaysia is 12.0 percent per annum and in the United States is 10.0 percent per annum. The spot rate for the US dollar (US$) is RM3.2250. If the interest rate parity holds, what is the 90-day forward rate? Answer:-

�� − ��

���

360

��100 = �ℎ� − ���

�� − 3.2250

3.2250�

360

90�100 = 2

�� = ���. ����

Question 4 a) Discuss the law of comparative advantage. Explain the opportunities that MNCs can tap by

going abroad. Answer:-

Law of comparative advantages Each country should specialise in the certain production and export of those goods that it can produce relatively more efficient and import those goods that it cannot produce with the highest relative efficiency. This will result in specialization in most countries and a greater output to be consumed by the world population.

Opportunities that MNC can tap by going abroad.

- Take advantages on labour market imperfection - Resources of production - Skill, knowledge and expertise - New market - Opportunities for cheaper cost of financing - Exploitation on market imperfection

14 | P a g e

b) TICK TOCK Sdn Bhd. wants to import 500 watches from a supplier in Switzerland at SFr200 each. The company has a choice of paying for the items immediately or in 3 months time. If the company settles the payment immediately, it will use its clean overdraft facility for 3 months, which charges a 15 percent interest rate per annum. If it settles the payment in 3 months time, the supplier will charge a flat rate of 10 percent on the total purchase price. The company can cover the exchange risk through a forward contract. Based on the exchange quotations below, determine the lowest cost settlement method. contract value : SFr 200 x 500 = SFr100,000 Spot :RM3.1820/86 SFr 3 month forward :RM3.1708/91 SFr - outright quotation Late charge :10% flat rate

Soalan ni pasal account payable.. berdasarkan information dan kehendak soalan.. ade dua cara untuk buat settlement.. 1) guna overdraft facilities 2) guna forward contract.. then kita pilih.. cara mana boleh buat settlement yang paling murah..

i. Forward Contract Settlement

[SFr100,000 x (1+ 0.10)] x RM3.1791 = RM349,701

ii. Settlement using overdraft facilities SFr 100,000 x RM3.1886 = RM318,860 (RM318,860 x 0.15 x 3/12) + RM318,860 = RM330,817.25

Settlement using overdraft facilities is much cheaper beb..!!

Question 5 a) The Letter of Credit (LC) is a commonly used method of trade settlement and financing. Discuss

various benefits that international traders can get from using LC. Answer:-

Against exporter explanation L/C eliminate credit risk Exporter only need to check credit reputation of

issuing bank

L/C reduce the danger payment will delay cause of exchange control or political act

Country always permit local bank to honor it LC. Fail to honour will cause coutry’s credit standing and credibility damage

L/C reduce uncertainty Requirement for payment clearly stipulated on L/C

L/C guard against pre shipment risk Protection against cancelation before shipment particularly with make to order equipment

Against Importer

L/C stipulated condition ensure goods are comply to importer requirement

Ensure quality, specification and delivery (L/C) require Bill Of Ladding for shipment)

Bank responsible for any oversight mistake Document will be check by experience clerk

L/C good as cash advance Importer can have credit term

Competetive advantage to importer who can provide L/C

Some importer only accept L/C

Prepayment through deposit Any default happen, importer easy to recover the deposit

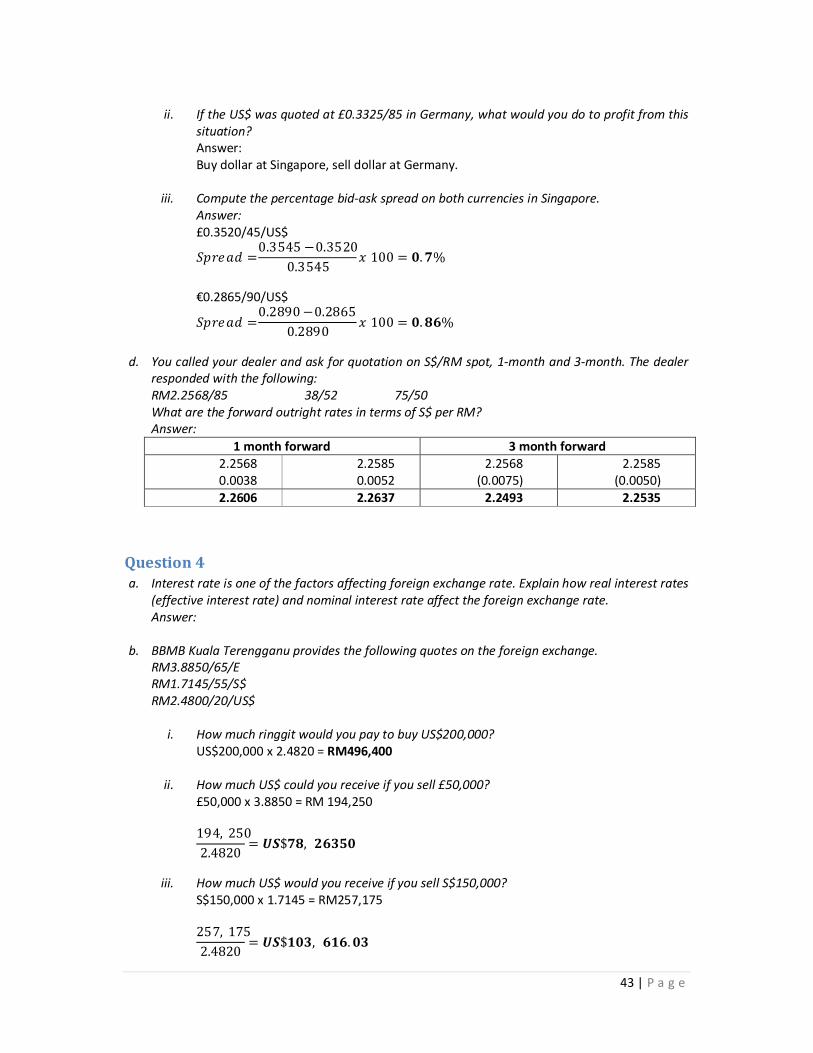

b) If the ¥/USD exchange rate and the C/¥ exchange rate are 108.6957/80 and 0.0053/57 respectively, what is the C/USD exchange rate? Determine the bid ask spread of C/USD.

15 | P a g e

Answer:- ¥108.6957 |80 /US$ €0.0053|57 /¥ What is €/US$ exchange rate? This is both side... then:- Bid FC x Bid HC Ask FC x Ask HC 108.6957 x 0.0053 =0.5760 108.6980 x 0.0057 = 0.6196 Ξ €0.5760 |0.6196 /US$

Determine spread of €/US$

������ =��� − ���

��� � ��� ������ =

�. ���� − �. ����

�. ���� � ��� = �%

c) i. When would hedging with a currency futures contract be more suitable than a currency

forward contract? Answer:- Currency future contract be more suitable than a currency forward contract when the trader / hedger not only want to minimize future transaction from the foreign exchange exposure but to gain benefit from the price movement. Using future, trader can maximize profit from the price movement because future trading activities using margin.

ii. When would hedging with a currency option contract be better than a currency futures contract? Answer:- Options can be very important, especially when it comes preserving the value of an existing fixed-income portfolio. Many people believe options are "insurance" against adverse price movements while offering the flexibility to benefit from possible favorable price movements. You could use options on futures based on the structure of an option contract. When you buy an option it gives you the right, not the obligation, to buy or sell a specific amount of a specific commodity at a specific price, within a specific period of time. By comparison, a futures contract requires a buyer or seller to perform under the terms of the contract if an open position is not offset before expiration. Second, the decision to exercise the option is entirely that of the buyer. Thirdly, the purchaser of the option can lose no more than the initial amount of money invested. This is called a premium. However, that is not the case for the buyer of a futures contract. Finally, an option buyer is never subject to margin calls. This enables the purchaser to maintain a market position, despite any adverse moves without putting up additional funds.

Gua sedut dari internet nih…. Dia tipu.. aku pon tipu ler..

16 | P a g e

Question 6 a) Dell Computer produces its machines in Asia with components largely imported from the United

States and sells its products in various Asian nations in local currencies. What is the likely impact on Dell's Asian profits of a weakened dollar? Explain. Answer:-

b) Assume a forex dealer contracted to buy five call options in Australian Dollars for USD0.034 per

unit. The strike price was USD0.4305 and the spot rate at the time the Australian Dollars was exercised was USD0.4359. If the dealer exercised the call option, what is the net profit (loss) of the call options? (assume the Australian Dollar option has 50,000 units) Answer:- Available information: Type : Call option Unit : 5 Volume /unit :50,000 Strike price :US$0.4305 Spot :US$0.4359 Premium :US$0.034

The dealer should exercise the option because Strike Price < Spot Rate – in the money The profit/loss calculation : Spot : US$0.4359 Strike price :(US$0.4305) US$0.0054 Premium : (US$0.034) Loss (US$0.0028) Ξ US$0.0028 x 50,000 x 5 =(US$7,150) LOSS...!!

Call option ni exercise bila spot rate tinggi... dalam soalan ni.. mula-mula Nampak macam nak untung... tapi bila tolak cost premium yang dah belanja untuk beli setiap unit option tu.. jadik rugi pulak.. kesimpulan yang aku buat sendiri... tak semestinya kita boleh exercise call option bila spot rate tinggi.. pastikan ia cukup tinggi untuk cover kita punyer premium cost..

c) BBAFin Sdn Bhd. has received an order for 200,000 units of ethnic porcelain vases from a

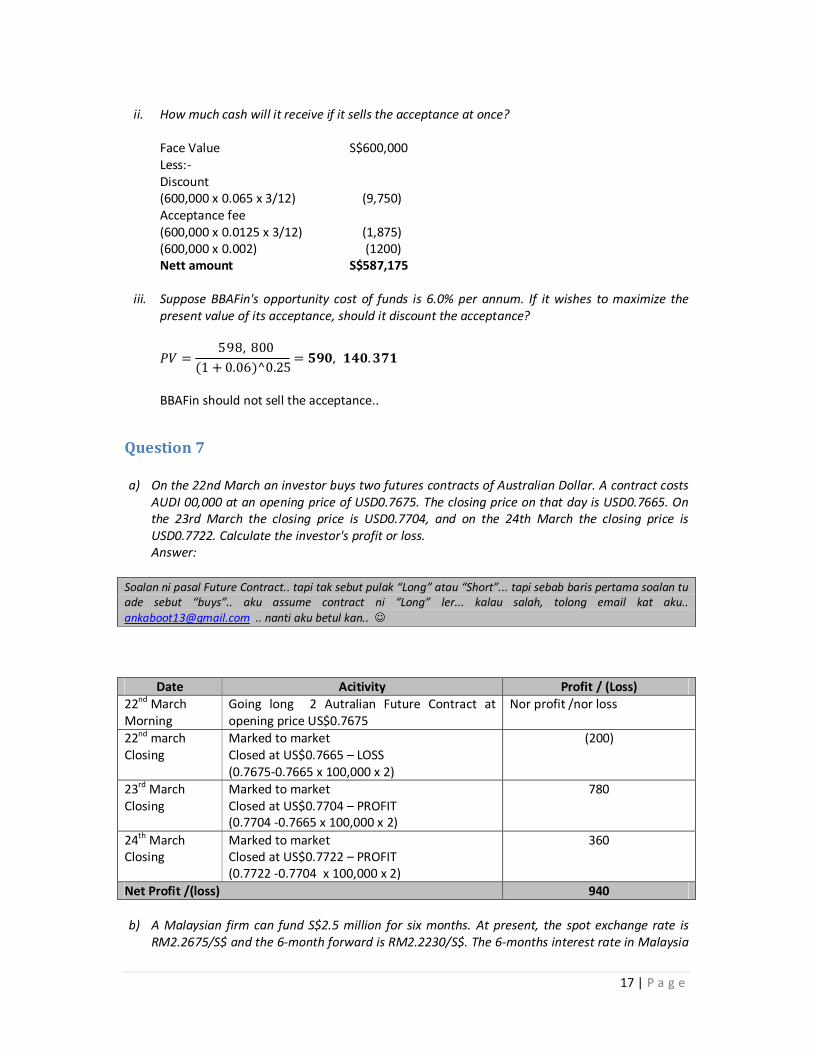

Singaporean distributor and payment is to be made in Singapore dollar, using 90 days usance credit. The letter of credit specifies that the face value of the shipment, S$600,000, will be paid 90 days after the Singapore Bank accepts a draft drawn by BBAFin. The current discount rate on 3-month acceptances is 6.5% per annum and the acceptance fee is 1.25% per annum. In addition, there is a flat commission, equal to 0.2% of the face amount of the accepted draft, which must be paid if it is sold. Answer:-

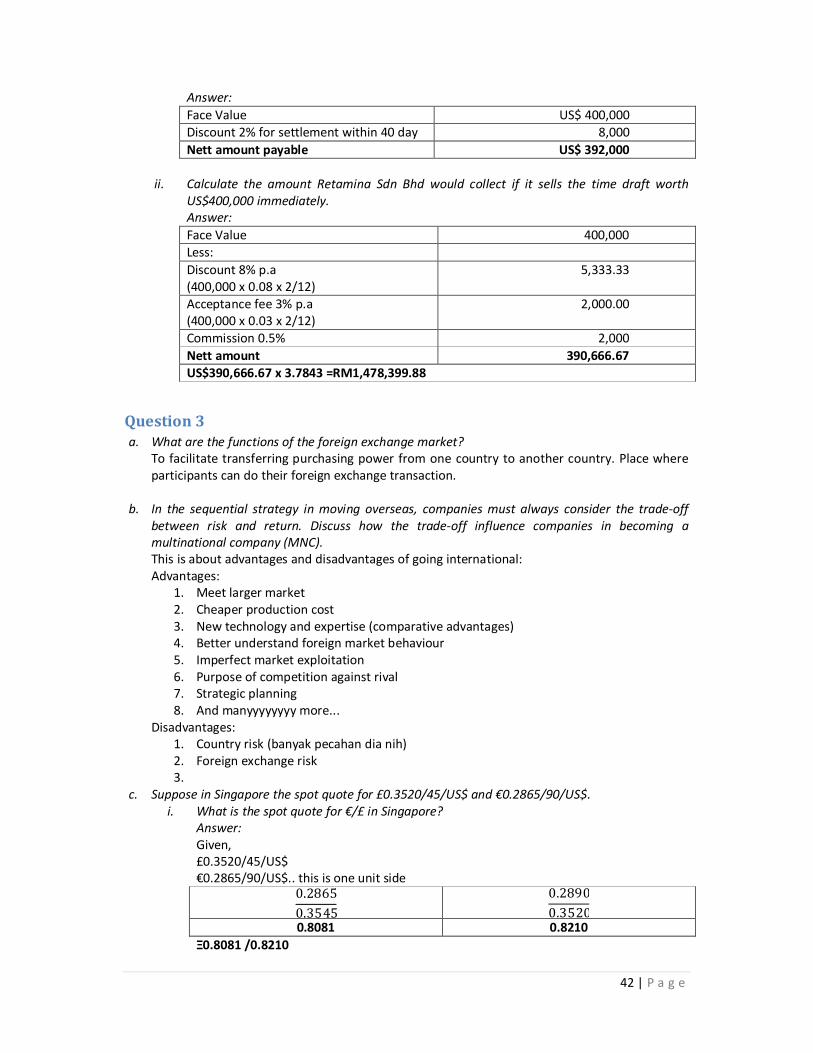

i. How much cash will BBAFin receive if it holds the acceptance until maturity?

Face Value S$600,000 Less; (600,000 x 0.002) (S$ 1200) S$598,800

17 | P a g e

ii. How much cash will it receive if it sells the acceptance at once?

Face Value S$600,000 Less:- Discount (600,000 x 0.065 x 3/12) (9,750) Acceptance fee (600,000 x 0.0125 x 3/12) (1,875) (600,000 x 0.002) (1200) Nett amount S$587,175

iii. Suppose BBAFin's opportunity cost of funds is 6.0% per annum. If it wishes to maximize the

present value of its acceptance, should it discount the acceptance?

�� =598,800

(1 + 0.06)^0.25= ���, ���. ���

BBAFin should not sell the acceptance..

Question 7 a) On the 22nd March an investor buys two futures contracts of Australian Dollar. A contract costs

AUDI 00,000 at an opening price of USD0.7675. The closing price on that day is USD0.7665. On the 23rd March the closing price is USD0.7704, and on the 24th March the closing price is USD0.7722. Calculate the investor's profit or loss. Answer:

Soalan ni pasal Future Contract.. tapi tak sebut pulak “Long” atau “Short”... tapi sebab baris pertama soalan tu ade sebut “buys”.. aku assume contract ni “Long” ler... kalau salah, tolong email kat aku.. [email protected] .. nanti aku betul kan..

Date Acitivity Profit / (Loss) 22nd March Morning

Going long 2 Autralian Future Contract at opening price US$0.7675

Nor profit /nor loss

22nd march Closing

Marked to market Closed at US$0.7665 – LOSS (0.7675-0.7665 x 100,000 x 2)

(200)

23rd March Closing

Marked to market Closed at US$0.7704 – PROFIT (0.7704 -0.7665 x 100,000 x 2)

780

24th March Closing

Marked to market Closed at US$0.7722 – PROFIT (0.7722 -0.7704 x 100,000 x 2)

360

Net Profit /(loss) 940

b) A Malaysian firm can fund S$2.5 million for six months. At present, the spot exchange rate is RM2.2675/S$ and the 6-month forward is RM2.2230/S$. The 6-months interest rate in Malaysia

18 | P a g e

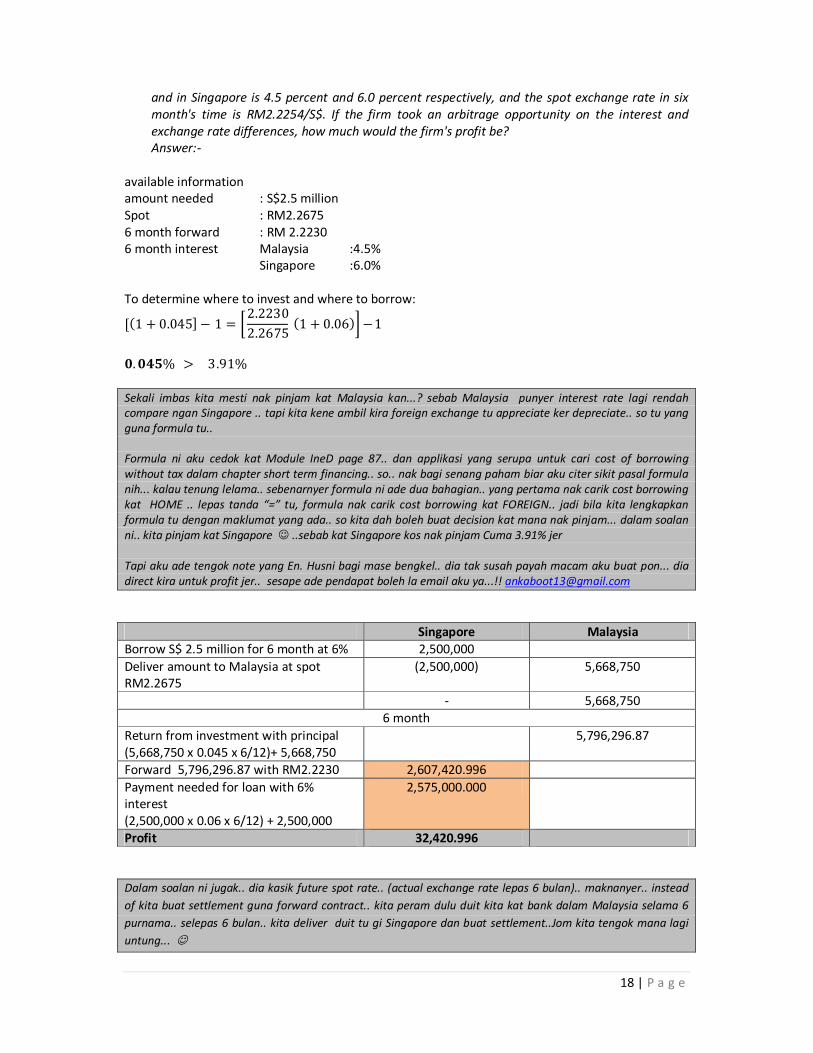

and in Singapore is 4.5 percent and 6.0 percent respectively, and the spot exchange rate in six month's time is RM2.2254/S$. If the firm took an arbitrage opportunity on the interest and exchange rate differences, how much would the firm's profit be? Answer:-

available information amount needed : S$2.5 million Spot : RM2.2675 6 month forward : RM 2.2230 6 month interest Malaysia :4.5% Singapore :6.0% To determine where to invest and where to borrow:

[(1 + 0.045] − 1 = �2.2230

2.2675 (1 + 0.06)� − 1

�. ���% > 3.91%

Sekali imbas kita mesti nak pinjam kat Malaysia kan...? sebab Malaysia punyer interest rate lagi rendah compare ngan Singapore .. tapi kita kene ambil kira foreign exchange tu appreciate ker depreciate.. so tu yang guna formula tu.. Formula ni aku cedok kat Module IneD page 87.. dan applikasi yang serupa untuk cari cost of borrowing without tax dalam chapter short term financing.. so.. nak bagi senang paham biar aku citer sikit pasal formula nih... kalau tenung lelama.. sebenarnyer formula ni ade dua bahagian.. yang pertama nak carik cost borrowing kat HOME .. lepas tanda “=” tu, formula nak carik cost borrowing kat FOREIGN.. jadi bila kita lengkapkan formula tu dengan maklumat yang ada.. so kita dah boleh buat decision kat mana nak pinjam... dalam soalan ni.. kita pinjam kat Singapore ..sebab kat Singapore kos nak pinjam Cuma 3.91% jer Tapi aku ade tengok note yang En. Husni bagi mase bengkel.. dia tak susah payah macam aku buat pon... dia direct kira untuk profit jer.. sesape ade pendapat boleh la email aku ya...!! [email protected]

Singapore Malaysia Borrow S$ 2.5 million for 6 month at 6% 2,500,000

Deliver amount to Malaysia at spot RM2.2675

(2,500,000) 5,668,750

- 5,668,750 6 month

Return from investment with principal (5,668,750 x 0.045 x 6/12)+ 5,668,750

5,796,296.87

Forward 5,796,296.87 with RM2.2230 2,607,420.996

Payment needed for loan with 6% interest (2,500,000 x 0.06 x 6/12) + 2,500,000

2,575,000.000

Profit 32,420.996

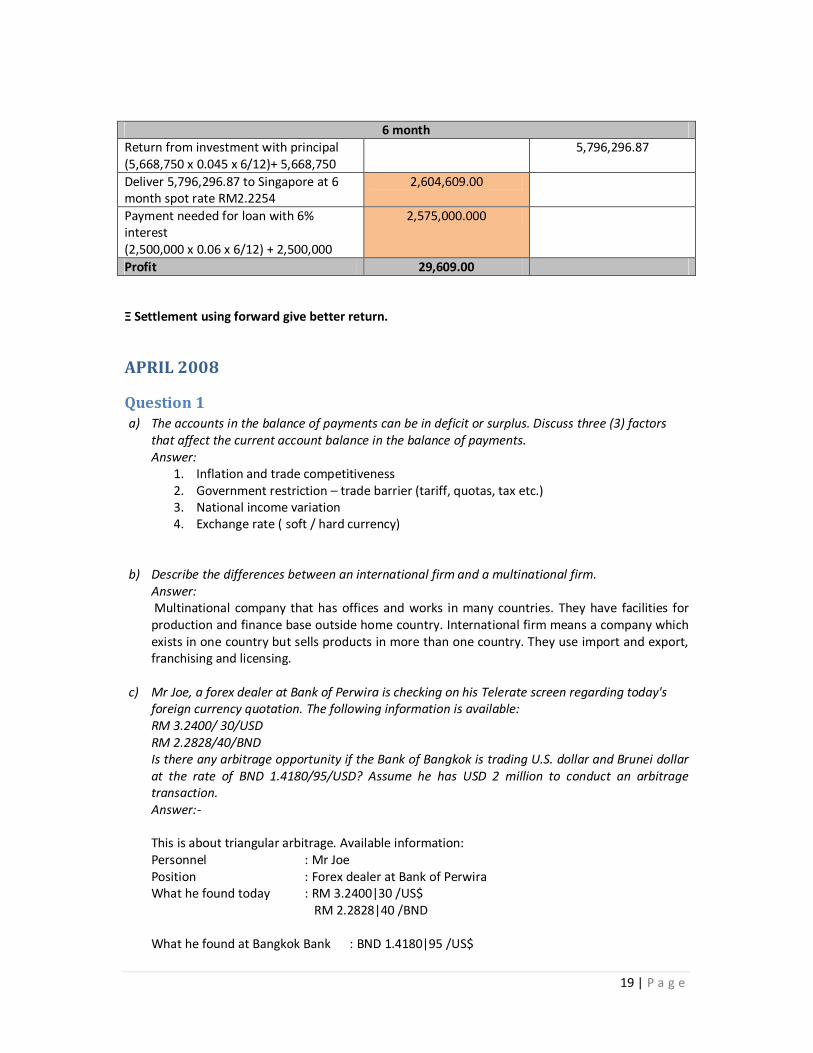

Dalam soalan ni jugak.. dia kasik future spot rate.. (actual exchange rate lepas 6 bulan).. maknanyer.. instead

of kita buat settlement guna forward contract.. kita peram dulu duit kita kat bank dalam Malaysia selama 6

purnama.. selepas 6 bulan.. kita deliver duit tu gi Singapore dan buat settlement..Jom kita tengok mana lagi

untung...

19 | P a g e

6 month Return from investment with principal (5,668,750 x 0.045 x 6/12)+ 5,668,750

5,796,296.87

Deliver 5,796,296.87 to Singapore at 6 month spot rate RM2.2254

2,604,609.00

Payment needed for loan with 6% interest (2,500,000 x 0.06 x 6/12) + 2,500,000

2,575,000.000

Profit 29,609.00

Ξ Settlement using forward give better return.

APRIL 2008

Question 1 a) The accounts in the balance of payments can be in deficit or surplus. Discuss three (3) factors

that affect the current account balance in the balance of payments. Answer:

1. Inflation and trade competitiveness 2. Government restriction – trade barrier (tariff, quotas, tax etc.) 3. National income variation 4. Exchange rate ( soft / hard currency)

b) Describe the differences between an international firm and a multinational firm. Answer: Multinational company that has offices and works in many countries. They have facilities for production and finance base outside home country. International firm means a company which exists in one country but sells products in more than one country. They use import and export, franchising and licensing.

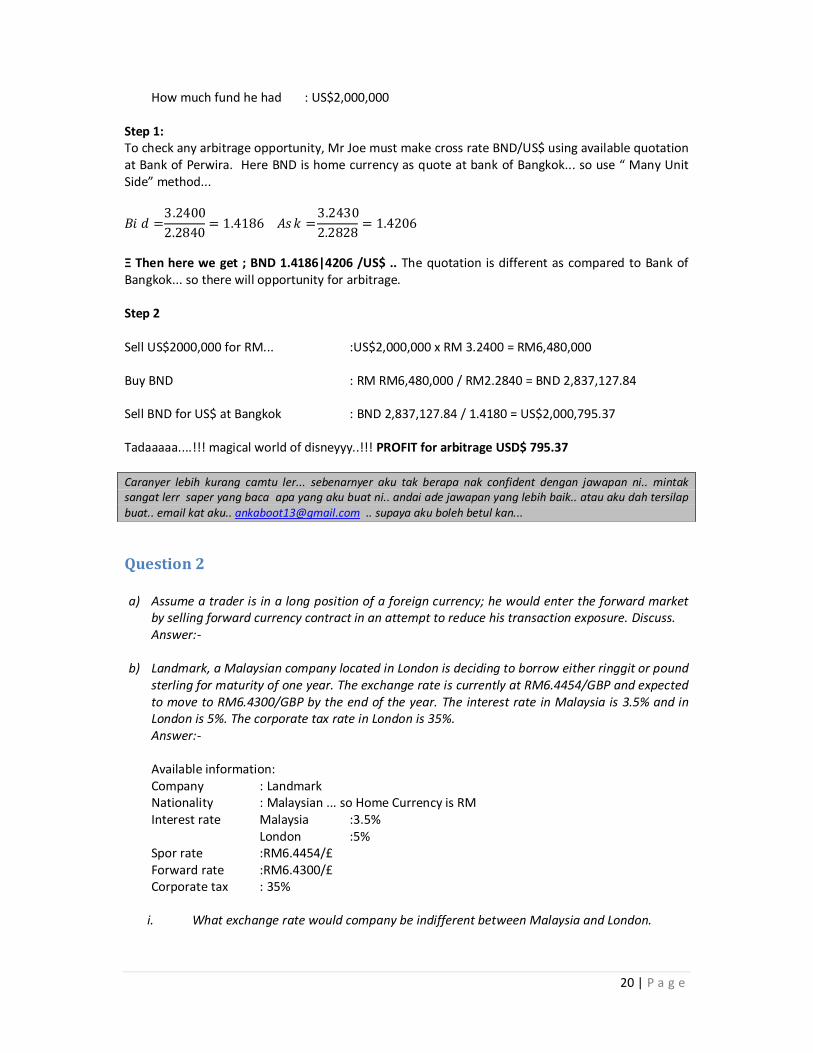

c) Mr Joe, a forex dealer at Bank of Perwira is checking on his Telerate screen regarding today's foreign currency quotation. The following information is available: RM 3.2400/ 30/USD RM 2.2828/40/BND Is there any arbitrage opportunity if the Bank of Bangkok is trading U.S. dollar and Brunei dollar at the rate of BND 1.4180/95/USD? Assume he has USD 2 million to conduct an arbitrage transaction. Answer:- This is about triangular arbitrage. Available information: Personnel : Mr Joe Position : Forex dealer at Bank of Perwira What he found today : RM 3.2400|30 /US$ RM 2.2828|40 /BND What he found at Bangkok Bank : BND 1.4180|95 /US$

20 | P a g e

How much fund he had : US$2,000,000 Step 1: To check any arbitrage opportunity, Mr Joe must make cross rate BND/US$ using available quotation at Bank of Perwira. Here BND is home currency as quote at bank of Bangkok... so use “ Many Unit Side” method...

��� =3.2400

2.2840= 1.4186 ��� =

3.2430

2.2828= 1.4206

Ξ Then here we get ; BND 1.4186|4206 /US$ .. The quotation is different as compared to Bank of Bangkok... so there will opportunity for arbitrage. Step 2 Sell US$2000,000 for RM... :US$2,000,000 x RM 3.2400 = RM6,480,000 Buy BND : RM RM6,480,000 / RM2.2840 = BND 2,837,127.84 Sell BND for US$ at Bangkok : BND 2,837,127.84 / 1.4180 = US$2,000,795.37 Tadaaaaa....!!! magical world of disneyyy..!!! PROFIT for arbitrage USD$ 795.37

Caranyer lebih kurang camtu ler... sebenarnyer aku tak berapa nak confident dengan jawapan ni.. mintak sangat lerr saper yang baca apa yang aku buat ni.. andai ade jawapan yang lebih baik.. atau aku dah tersilap buat.. email kat aku.. [email protected] .. supaya aku boleh betul kan...

Question 2 a) Assume a trader is in a long position of a foreign currency; he would enter the forward market

by selling forward currency contract in an attempt to reduce his transaction exposure. Discuss. Answer:-

b) Landmark, a Malaysian company located in London is deciding to borrow either ringgit or pound

sterling for maturity of one year. The exchange rate is currently at RM6.4454/GBP and expected to move to RM6.4300/GBP by the end of the year. The interest rate in Malaysia is 3.5% and in London is 5%. The corporate tax rate in London is 35%. Answer:- Available information: Company : Landmark Nationality : Malaysian ... so Home Currency is RM Interest rate Malaysia :3.5% London :5% Spor rate :RM6.4454/£ Forward rate :RM6.4300/£ Corporate tax : 35%

i. What exchange rate would company be indifferent between Malaysia and London.

21 | P a g e

(1 + �ℎ�)

(1 + ���)=

��

��

(1 + 0.035)

(1 + 0.05)=

��

6.4454

�� = ���. ����/£ .. at the exchange rate.. it would be indifferent either borrow in Malaysia or London...

Kat sini kita guna equation IFE (international Fisher Effect) .. sebabnyer IFE suggest.. aku cakap omputih sikit ehh.. ”The differences of interest rate between two countries’ currencies can be an unbiased predictor to the future change in the spot rate”.. tu sebab kita guna untuk carik future spot rate guna interest rate.. baca Module IneD page 85.

ii. Before Tax ringgit cot of pound loan.? – Cost Home Foreign Currency (CHfc)

���� = ���

��(1 + ���)� − 1

���� = �6.4300

6.4454(1 + 0.05)� − 1

���� =4.75%

iii. What is the after tax ringgit cost of pound loan? Cost Home Foreign Currency (CHfc)

Find “C” first...

� =�� − ��

�� � =

6.4300 − 6.4454

6.4454= −�. �����

Then, proceed with this formula

���� = ���(� − � )(� + �) + �

���� = �. ��(� − �. �� )(� − �. ����� ) − �. �����

���� = �%

iv. What is after tax ringgit cost of ringgit loan? Cost Home, Home currency (CHhc)

���� = ���(� − � ) + � �

���� = �. ��� (� − �. �� ) − (�. �� � �. �����)

���� = �. ��%

v. Borrow ringgit.. because it cheaper.

22 | P a g e

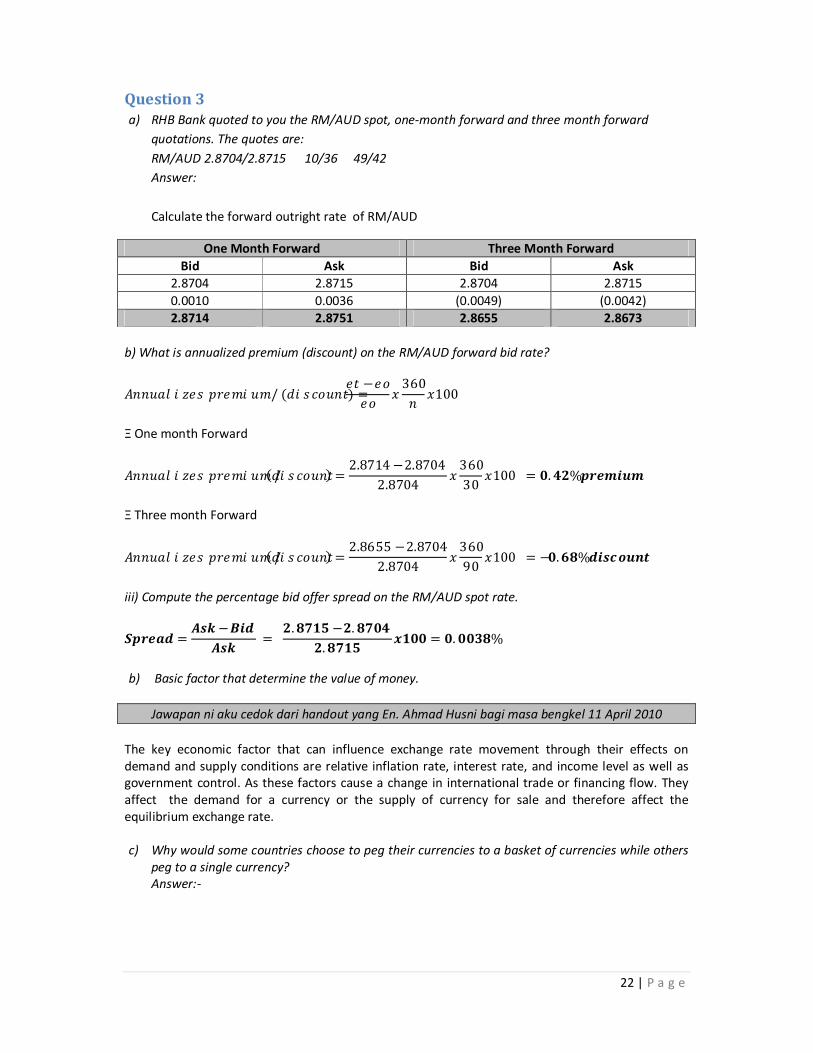

Question 3 a) RHB Bank quoted to you the RM/AUD spot, one-month forward and three month forward

quotations. The quotes are:

RM/AUD 2.8704/2.8715 10/36 49/42

Answer:

Calculate the forward outright rate of RM/AUD

One Month Forward Three Month Forward

Bid Ask Bid Ask 2.8704 2.8715 2.8704 2.8715

0.0010 0.0036 (0.0049) (0.0042) 2.8714 2.8751 2.8655 2.8673

b) What is annualized premium (discount) on the RM/AUD forward bid rate?

���������� �������/ (��������) =�� − ��

���

360

��100

Ξ One month Forward

���������� ������� / (��������) =2.8714 − 2.8704

2.8704�

360

30�100 = �. ��% �������

Ξ Three month Forward

���������� ������� / (��������) =2.8655 − 2.8704

2.8704�

360

90�100 = −�. ��% ��������

iii) Compute the percentage bid offer spread on the RM/AUD spot rate.

������ =��� − ���

��� =

�. ���� − �. ����

�. �������� = �. ����%

b) Basic factor that determine the value of money.

Jawapan ni aku cedok dari handout yang En. Ahmad Husni bagi masa bengkel 11 April 2010

The key economic factor that can influence exchange rate movement through their effects on demand and supply conditions are relative inflation rate, interest rate, and income level as well as government control. As these factors cause a change in international trade or financing flow. They affect the demand for a currency or the supply of currency for sale and therefore affect the equilibrium exchange rate. c) Why would some countries choose to peg their currencies to a basket of currencies while others

peg to a single currency? Answer:-

23 | P a g e

Question 4 a) Your customer who exports palm oil to Egypt for US$100,000 presents the bill of exchange for

the amount to your bank for collection and requests your bank to purchase the bill. Payment is by way of 90 days sight bill (D/A) CIF Port Said. Answer:-

i. If your bank purchases the bill from the customer, what are the risks involved to the

bank?

ii. What do you understand by the payment term 90 days sight bill (D/A) CIF Port Said?

b) What are bills of exchange (B/E) and why are they being used in international trade? Answer: An unconditional order issued by a person or business which directs the recipient to pay a fixed sum of money to a third party at a future date. The future date may be either fixed or negotiable. A bill of exchange must be in writing and signed and dated. Also called draft. Use in international trade because it characteristics and payment system safeguard the interest of exporter and importer.

Question 5 a) The East Asiatic Company (EAC), a Danish company with subsidiaries all over Asia, has been

funding its Bangkok subsidiary primarily with U.S. dollar debt because of the cost and availability of dollar capital as opposed to Thai baht (B) funds. The treasurer of EAC-Thailand is considering a one-year bank loan for US$350,000. The current spot exchange rate is B41.3580/US$, and the dollar-based interest is 8.885% for the one-year period. Answer: Available information : Spot :B41.3580 US interest :8.885% Expected inflation Thai : 4.50% US : 2.20%

i) Assuming expected inflation rates of 4.50% and 2.20% in Thailand and the United States respectively, for the coming year. According to purchasing power parity, what would the effective cost of funds be in Thai baht terms? Purchasing Power Parity (PPP) – currency with higher interest rate should depreciate to currencies with lower interest rate.

�� =(1 + �ℎ�)

(1 + ���)��

�� =(1 + 0.045)

(1 + 0.0220)� 41.3580

�� = �42.2887

[350,000 x 0.08885] + 350,000 = 381,097.50

24 | P a g e

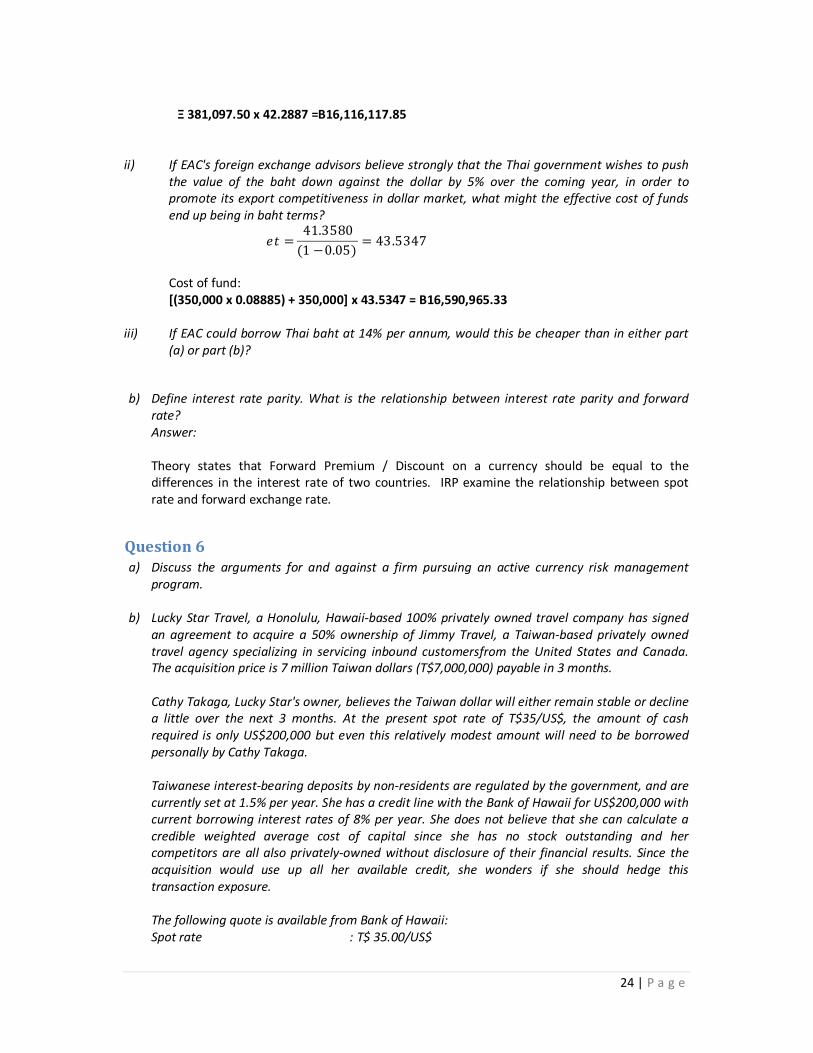

Ξ 381,097.50 x 42.2887 =B16,116,117.85

ii) If EAC's foreign exchange advisors believe strongly that the Thai government wishes to push

the value of the baht down against the dollar by 5% over the coming year, in order to promote its export competitiveness in dollar market, what might the effective cost of funds end up being in baht terms?

�� =41.3580

(1 − 0.05)= 43.5347

Cost of fund: [(350,000 x 0.08885) + 350,000] x 43.5347 = B16,590,965.33

iii) If EAC could borrow Thai baht at 14% per annum, would this be cheaper than in either part (a) or part (b)?

b) Define interest rate parity. What is the relationship between interest rate parity and forward rate? Answer: Theory states that Forward Premium / Discount on a currency should be equal to the differences in the interest rate of two countries. IRP examine the relationship between spot rate and forward exchange rate.

Question 6 a) Discuss the arguments for and against a firm pursuing an active currency risk management

program.

b) Lucky Star Travel, a Honolulu, Hawaii-based 100% privately owned travel company has signed an agreement to acquire a 50% ownership of Jimmy Travel, a Taiwan-based privately owned travel agency specializing in servicing inbound customersfrom the United States and Canada. The acquisition price is 7 million Taiwan dollars (T$7,000,000) payable in 3 months.

Cathy Takaga, Lucky Star's owner, believes the Taiwan dollar will either remain stable or decline a little over the next 3 months. At the present spot rate of T$35/US$, the amount of cash required is only US$200,000 but even this relatively modest amount will need to be borrowed personally by Cathy Takaga. Taiwanese interest-bearing deposits by non-residents are regulated by the government, and are currently set at 1.5% per year. She has a credit line with the Bank of Hawaii for US$200,000 with current borrowing interest rates of 8% per year. She does not believe that she can calculate a credible weighted average cost of capital since she has no stock outstanding and her competitors are all also privately-owned without disclosure of their financial results. Since the acquisition would use up all her available credit, she wonders if she should hedge this transaction exposure. The following quote is available from Bank of Hawaii: Spot rate : T$ 35.00/US$

25 | P a g e

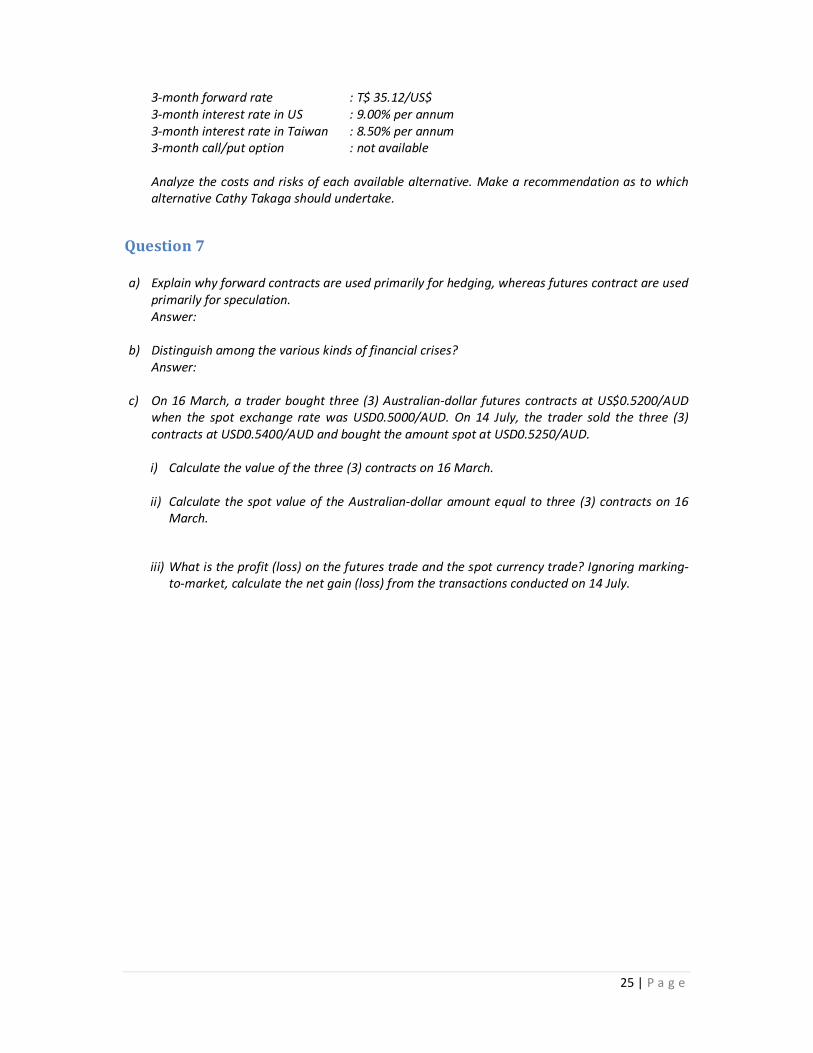

3-month forward rate : T$ 35.12/US$ 3-month interest rate in US : 9.00% per annum 3-month interest rate in Taiwan : 8.50% per annum 3-month call/put option : not available Analyze the costs and risks of each available alternative. Make a recommendation as to which alternative Cathy Takaga should undertake.

Question 7 a) Explain why forward contracts are used primarily for hedging, whereas futures contract are used

primarily for speculation. Answer:

b) Distinguish among the various kinds of financial crises? Answer:

c) On 16 March, a trader bought three (3) Australian-dollar futures contracts at US$0.5200/AUD when the spot exchange rate was USD0.5000/AUD. On 14 July, the trader sold the three (3) contracts at USD0.5400/AUD and bought the amount spot at USD0.5250/AUD. i) Calculate the value of the three (3) contracts on 16 March. ii) Calculate the spot value of the Australian-dollar amount equal to three (3) contracts on 16

March.

iii) What is the profit (loss) on the futures trade and the spot currency trade? Ignoring marking-to-market, calculate the net gain (loss) from the transactions conducted on 14 July.

26 | P a g e

OCTOBER 2007

Question 1 a) Foreign direct investment by multinational companies (MNC) is a major force driving

globalization of the world economy. Describe three (3) ways where MNCs may gain from their global presence.

b) An American firm has contracted to buy parts from Europe worth €15 million payable in one year. The firm has receivables for goods sold to a French firm valued at €5 million, also due in one year. The spot rate of the US dollar against the euro dollar is €0.7200, and the one year forward rate is €0.6300. The annual interest rates on the US dollar and the euro dollar are 13.2% and 9% respectively. What is the cost of the forward cover if the firm executes the desired hedge in the forward market? If the hedge is executed in the money market, what is the cost of this money market hedge? Answer:

Dalam soalan ni ade dua macam account,.. account payable €15 million dengan account receivable €5 million.. bila ade dua account macam ni... kita ambil nett jer... mana yang lagi besar.. tolak yang kecik.. so dalam soalan ni... €15 million - €5 million.. jadik nett amount dia Payable €10 million... aku confident dengan jawapan ni.. sebab buat dalam class En. Ahmad Husni yang terangkan.

i. Foward contract Cost

10,000,000

0.6300= ��$��, ���, ���. ��

ii. Money Market Hedge

Step 1: Determine Amount To Invest in Europe

�� =10,000,000

(1 + 0.09)= €9,174,311.98

Step 2: Covert amount to US$ €9,174,311.98

0.7200= ��$12,742,099.9

Step 3: Calculate Cost Of Borrowing US$12,742,099.9 x (1+0.132) =US$14,424,057.08

27 | P a g e

Question 2 a) As an investment officer of a world renown bank in Kuala Lumpur, you have been tracking the

exchange rate market and realized that there may exist opportunities to arbitrage. The exchange rate quotation on your computer shows the following: RM 3.5070/90 /US$ RM 0.4555/80 /HK$ Show all calculations and ignore transaction costs.

i. Investigate if there is any opportunity to arbitrage between the two markets if you noticed that the Bank of Indonesia in Jakarta is trading the U.S. dollar and the Hong Kong dollar at the current quote of HK$7.8240/60 /US$.

��� =3.5070

0.4580= 7.6572 ��� =

3.5090

0.4555= 7.7036

Ξ HK 7.6572 | 7.7036 /US$ The quotation is different. There is opportunity to arbitrage.

ii. Assume that you can source a sum of HK$ 20 million to perform this transaction, explain how you should go about transferring funds from one market to the next and how much can you gain? What HK$/US$ price will eliminate this triangular arbitrage opportunity?

Sell HK$ 20 million for RM

HK$20,000,000 x RM0.4555 = RM9,110,000

Buy US$ using RM

RM9,110,000 / RM 3.5090 =US$2,596,181.24

Sell US$ at Jakarta for HK$

US$2,596,181.24 x HK$7.8240 = HK$20,312,522.09

Profit from these transaction HK$312,522.09

Satu perkara yang aku rase boleh buat kenkawan dapat clue sikit macam mana nak buat triangular arbitrage

ni .. Mula- mula kita tengok currency yang first sekali dia kasi untuk conduct transaction ni.. dalam soalan ni..

dia kasik HK$... so kita kene pastikan.. setelah.. jual.. beli.. jual...beli.. jual ...beli... berpusing-pusing.. lassssttttt

sekali dia kene berakhir dengan HK$ jugak.... so baru kita tahu berapa untung dia... tak gitu...??? kalu aku

salah.. tolong sound aku yer... [email protected]

b) What is the difference between foreign direct investment and a foreign portfolio investment? What type of investment is an industrial multinational company more likely to make?

Foreign direct investment (FDI) is defined as a long-term investment by a foreign direct investor in an enterprise resident in an economy other than that in which the foreign direct investor is based. The FDI relationship consists of a parent enterprise and a foreign affiliate which together form a transnational corporation (TNC). In order to qualify as FDI the investment must afford the parent enterprise control over its foreign affiliate. The United Nations defines control in this case as owning 10 percent or more of the ordinary shares or voting power of an incorporated firm or its equivalent for an unincorporated firm.

28 | P a g e

Portfolio investment is investment made by investors who are not particularly interested in involvement in the management of a company. The purchase of stocks, bonds, and money market instruments by foreigners for the purpose of realizing a financial return, which does not result in foreign management, ownership, or legal control. Multinational Company most likely makes investment in form FDI.

Question 3 a) On October 10, a trader goes long one IMM yen futures contract at an opening price of $0.0088.

The settlement prices for October 10, 11, and 12 are $0.0079, $0.0083 and $0.0086, respectively. On October 13, you close out the contract at a price of $0.0084. Your roundtrip commission is $25 (Contract = Yen 12.5 million). Calculate the daily cash flows on your account.

Long Future Contract maknanyer .. contract untuk BELI.. beli mesti mau murah..!!! jual mesti MAHAL.. jadi.. if close rendah.. maknanyer jual rendah .. kita rugi.. kalau close tinggi.. mananyer jual tinggi... kita untung..? bole ker camtu..? hehehehe... suka korang la nak paham cara mana...

Date Activities Profit /(loss)

10 October Morning

Goes long Yen future contract at price $0.0088

Nor profit /nor loss

10 October Evening

Marked to Market Close at $0.0079 – LOSS [$0.0088 - $0.0079] x 12.5 million

(11,250)

11 October Evening

Marked to Market Close at $0.0083 – PROFIT [$0.0083 - $0.0079] x 12.5 million

5,000

12 October Evening

Marked to Market Close at $0.0086 – PROFIT [$0.0086 - $0.0083] x 12.5 million

3,750

13 October Evening

Marked to Market Close at $0.0084 – LOSS [$0.0086 - $0.0084] x 12.5 million

(2500)

Nett profit /(loss) (5000)

b) Briefly explain nominal and real exchange rate. Why is purchasing power parity not holding in

short-term?

Question 4 a) Prolon (Malaysia) could borrow ringgit at 4% or dollars at 6% for one year. The USD:ringgit

exchange is expected to move from USD/RM3.4240 currently to USD/RM3.3500 by the year's end. Chevrolet is paying 35% corporate tax.

i) What is the before-tax home currency equivalent cost?

���� = �3.3500

3.4240(1.06)� − 1 = 3.7%

29 | P a g e

ii) What is the after tax ringgit cost of dollar loan? - CHfc

� =3.3500 − 3.4240

3.4240= −�. ����

���� = ��� (1 − � )(1 + �) + � ���� = �. ��(� − �. �� )(� − �. ���� ) − �. ���� = �. ��%

iii) What is the after tax ringgit cost of ringgit loan? ��ℎ� = �ℎ� (1 − � ) + �� ���� = �. �� (� − �. �� ) − (�. �� � �. ����) = �. ��%

iv) Which currency loan has the lowest after-tax cost? DOLLARRRRRR... $$$$$$$...!!!

b) Discuss three (3) methods of financing international trade.

Question 5 a) Canterbury Chocolate of Singapore has received an export order of 60,000 cartons of chocolate

from Langkawi Chocolate Sdn Bhd in Malaysia. The chocolate will be exported under the terms of a letter of credit issued by Maybank Malaysia. The letter of credit specifies that the face value of the shipment, GBP 500,000 will be paid after Maybank accepts a draft drawn by Canterbury Chocolate. Langkawi Chocolate has two options: to pay on cash basis and receive a discount of 5% or a 180 day creditbasis with a 7% per annum late payment. The current discount rate on a 6-month bill is 8.5% per annum and the acceptance fee is 1.25% per annum. There is a flat commission of 0.5% on the face amount of the accepted draft that must be paid if it is sold. The following quotations are given:

Kuala Lumpur RM/£ London £/RM Spot rate 6.9530/7.0900 0.1471/0.1485 3 month forward 60/78 55/45 6 month forward 30/56 80/75 i) How much will Canterbury receive if it sold the banker's acceptance at once?

ii) How much cash will Canterbury receive if it holds the banker's acceptanceuntil maturity?

iii) If Langkawi Chocolate decides to take the 180-day credit basis and hedges in the forward

market, how much do they need to pay?

b) US speculator sold a put option on Canadian dollars for US$ 0.06 per unit. The strike price was US$ 0.60 and the spot rate at the time the Canadian dollars was exercised was US$ 0.65.

30 | P a g e

Assume the speculator immediately sold off the Canadian dollars received when the option was exercised. What was the net profit or loss to the seller of the put option? (C$ 50,000 units per contract)

Aku pon teragak-agak juga nak jawab soalan ni.. sebab kefahaman aku yang ala kadar ni... tapi setelah berdiskusi dengan MABAM, Amir TV3, Jeff, Fendi AmBank, Amir MARDI, Nazri PKA.. aku simpulkan kefahaman aku begini..... US speculator tu.. aku assume ( ASS U & ME) writer to the option... (orang yang jual option)..

At the put option buyer perspective Spot rate > Strike price - out of money.. buyer will let the option expire BUT.. in this question... the option was exercised (by the broken heart buyer perhaps ) the seller get profit as follow: Spot rate US$ 0.65 - Strike (US$ 0.60) US$ 0.05 Premium US$ 0.06 US$0.11 ΞUS$0.11 x 50,000 =US$5,500

Question 6 a) When a country faces economic problems, one of the steps that would be taken by the

government is to increase the interest rates. Do you think it is the right thing to do?

b) Mel Broke Sdn Bhd has to buy and sell currencies at different time periods. Loan Bank provides the following quote on the foreign currency. RM/US$ 3.4872/84 30/45 61/55 RM/£ 6.3145/65 65/80 23/19 i) How many RM would you pay to buy US$6,600,000 today?

��$6,600,000 � 3.4884 = ����, ���, ���. ��

ii) How many pounds sterling would you receive if you have RM820, 000 today? 820,000

6.3165= £���, ���. ��

iii) How many US dollars can you purchase for delivery in 1 month with RM2, 300,000?

2,300,000

(3.4884 + 0.0045)= ��$���, ���. ��

iv) How many ringgits would you receive if you sell £74,000 for delivery in three months?

£74,000 � (6.3154 + 0.0023) = �� ���, ���. ��

31 | P a g e

v) What is the bid-offer price of US dollar per £ today?

Ni soalan cross rate.. aku tengok kenkawan lain senang jer buat cross rate nih... tapi kepala aku susah bebenor nak terima natang nih..!!! saper yg tak berapa nak paham tu.. kira kita boleh geng ler... hehehehehe.. apa pun kesimpulan yg aku boleh buat... yg buat Nampak susah tu disebabkan cara soalan bagi quotation tu.. contohnya RM/US$ x.xxxx/xx ..ade pulak yg macam nih.. RM x.xxxx/xx |US$.... ade pulak dia sebut jer “ RM against US$”...”US$ per Pound”..adoii.. konpius jugak kepalo pakcik yang tak berapa nak bijak bahaso omputih nih... so.. PAHAM kan chapter 4 tu sebaik-baiknyer...!!

RM/US$ 3.4872/84 RM/£ 6.3145/65

��� =6.3145

3.4884= 1.8101 ��� =

6.3165

3.4872= 1.8113

ΞUS$1.8101 /13 |£

Question 7 a) If expected inflation is 150% and the real required return is 6%, what will the nominal interest be

according to the Fisher effect? According to fisher effect:-

� = � + � Where: r = Nominal rate a = real rate of return i = inflation rate

� = 0.06 + 1.50 � = �. �� ~ ���%

b) Assuming that last year the short-term interest rate in France was 4.2% and forecast inflation

was 1.8%. At the same time, the short-term German interest rate was 3.5% and forecast inflation was 1.6%. Based on these figures, what were the real interest rates in France and Germany according to the Fisher effect?

� = � + � Interest rate in france:

4.2 = � + 1.8 � = �. �%

Interest rate in Germany: 3.5 = � + 1.6 � = �. �%

Many unit side... formula selak buku ler yer..!!

32 | P a g e

c) i. Given that the one-year interest rate is 12% on British pounds and 9% on Malaysian

ringgit. If the current exchange rate is RM 6.8585/£, what is the expected future exchange rate in one year based on the international Fisher effect? (1 + �ℎ�)�

1 + ���)�=

��

��

(1 + 0.09)

(1 + 0.12)=

��

6.8585 �� = ��6.6748/£

Aku nak citer sikit pasal Fisher Effect nih... theory ni kata.. Negara yang interest rate dia rendah , mata wang dia akan appreciate.. berbanding Negara yang interest tinggi... Kenapa..? sebabnya idea fisher effect nih... real rate of return (interest rate) seluruh dunia ni almost serupa... Cuma interest rate berbeza-beza disebabkan rate tersebut telah di adjust dengan inflation rate.. statement ni relate dengan PPP theory (purchasing Power Parity).. matawang akan depreciate kalau Negara tu punyer inflasi tinggi.. kalau tengok soalan yang aku cuba buat kat atas nih... RM appreciate for the next 1 year .. sebabnyer interest rate British tinggi (mungkin di sebabkan inflasi) berbanding Malaysia.. (aku tau.. aku tak competent nak explain pasal theory nih.. tapi aku cuba nak share kefahaman aku sebagai seorang student jer... kalu silap maaf ler yer.)

ii. Suppose a change in expectations regarding future inflation in Malaysia causes the

expected future spot rate to decline to RM6.8400/£. What should happen to interest rate in Malaysia?

�

(1 + 0.12)=

6.8400

6.8585 � = �. ��� ~��. �%

d) What are the advantages and disadvantages of fixed exchange rates?

Answer:- The main advantages of fixed exchange rate is bacalah ler sendiri...!! kui..kui..kuii....

33 | P a g e

APRIL 2007

Question 1 i. Describe the Bretton Woods agreement. How long did the agreement last? What forces it to

collapse? Answer: Fact about bretton woods agreement:

1. 1944 2. 44 countries 3. Last for 27 years.. until 1973 4. Only US$ can convert to gold at US$35 per ounce 5. Other countries pegged their US$

Why this collapse: 1. America involved in Vietnam war.. diaorang cetak dollar bebanyak so susah nak

maintain US$ to gold at US$35 per ounce. 2. Orther countries like Japan and France refuse to maintain the system. Ade ler cerita

dia.. panjang jugak.. nak pinjam buku aku boleh gak.. The following information is given to you: RM/US$ spot rate :3.5312 / 24 RM/€ spot rate :4.4956 / 78 One month interest rate in Malaysia is 8.50%, in United States is 6.50% and in Germany is 9.20%.

ii. If you need US$ 57,400, today, how much ringgit would you exchange with? US$57,000 x 3.5324= RM201,346.80

iii. If you have €83,500 today, how much ringgit would you exchange with? €83,500 x 4.4956 =RM375,382.60

iv. How many ringgit would you receive if you sell US$ 71,301 for delivery in one month? �. ���� � (�. ��� − �. ��� )� ��

���= �. ���� �������

US$71,301 x (3.5312 + 0.0059) = RM 252,198.77

v. How many Euro would you exchange with RM95,219 for delivery in one month? 4.4978 � (0.085 − 0.092)� 30

360= − 0.0026 ��������

��, ���

(�. ���� − �. ����)= €��, ���. ��

vi. What is the bid and offer price of US$/€ exchange today?

4.4956

3.5324= 1.2727 − ���

34 | P a g e

4.4978

3.5312= 1.2737 − ���

Ξ US$ 1.2727|37 /€

vii. What is the annualized premium (discount) on the one month ask forward RM / US$ rate? viii. What is the percentage spread of the RM /€ quotation?

Question 2 a) How can MNC reduce the operating expenses relative to domestic firms?

b) Dearborn Inc. (based in US) could borrow a one-year loan in New Zealand at the quoted interest

rate of 8% or 9.5% in US. The exchange rate at that time is US$0.5000 per New Zealand dollar and it is expected to move to US$0.4500. Assume that currently the company is paying 33% corporate tax to the New Zealand government.

i. Compute the before-tax home currency equivalent cost.

���� =��

��(1 + ���)

���� = �0.4500

0.5000(1.08)� − 1 =

?

ii. Compute the after-tax home currency equivalent cost

iii. In which currency would it be cheaper to borrow? Why?

Question 3 a) Malaysian palm oil producers export more than 90% of their product for sale in dollars. Virtually

all their costs, however, are in Malaysian ringgit. i. How would the 30% fall in the value of the ringgit during 1997 affect the ringgit

profitability of these producers? Explain. ii. How would the ringgit's depreciation affect the dollar profits of these producers?

Explain. b) Simon Lee has obtained several forward contract quotations for the Thai baht to determine

whether covered interest arbitrage may be possible. He was quoted a forward rate of US$0.0225 per Thai baht for a 90-day forward contract. The current spot rate is US$0.0229. Ninety-day interest rates available to him in the United States are 2.5% while ninety-day interest rates in Thailand are 6.75%. Determine the dollar profit he could generate by withdrawing TB300,000 from his checking account.

35 | P a g e

Question 4 a) What are the long term and short-term consequences for a nation running balance of payments

deficits?

b) DKNY owes Mex Peso 7 million in 30 days for a recent shipment from Mexico. It faces the following interest and exchange rates: Spot rate : Mex Peso 13.0/$ Forward rate (30 days) Mex Peso 13.1/$ 30-day put option on dollars at Mex Peso 12.9/$ 1% premium 30-day call option on dollars at Mex Peso 13.1/$ 3% premium U.S. dollar 30-day interest rate (annualized) : 7.5% Mex Peso 30-day interest rate (annualized) : 15%

i. What hedging alternatives are available to DKNY? Forward Contract, Money Market, Option

ii. What is the hedged cost of DKNY's payable using a forward market hedge? Using money market hedge? Using put option? Using Forward contract : Peso 7,000,000 / 13.1 =US$534,351.15 Using Money Market: Step 1: Determine to invest in Mexico

7,000,000

(1 + [0.15�1/12))= 6,913,580.25

Step 2: Covert amount US$ 6,913,580.25

13= 531,813.86

Step 3: Calculate cost of borrowing [531,813,86 x 0.075 x 1/12 ]+ 531,813.86= US$535,137.70 Using Option: Call Option 7,000,000 / 13.1 + premium 3 % = USD$550,381.68

iii. Which is the preferred alternative? Forward contract is cheaper option

iv. Suppose that DKNY expects the 30-day spot rate to be Mex$ 13.4/$. Should it hedge this payable? What other factors should go into DKNY's hedging decision? Yes... DKNY should hedge.

36 | P a g e

Question 5 a) As a foreign exchange officer at MayBank, the exchange quotation you checked on your

computer screen is as follows: RM 3.5015/25/US$ RM 6.8755/65/£

You learned that DBS Singapore is making a market between the pound sterling and the U.S. dollar with the current quote of US$1.8288/90/£. Is there an opportunity to arbitrage between the two markets? Show all workings ignoring transaction costs. Assume that you can fund US$ 5 million to conduct this transaction. What US$/£ price will eliminate this triangular arbitrage opportunity? Answer: Step 1: find cross rate US$ /£ at Maybank

Bid Ask 6.8755

3.5025= 1.9630

6.8765

3.5015= 1.9639

ΞUS$ 1.9630|39 /£ The quotation is different. There opportunity for arbitrage. Step 2: Buy £ at DBS Singapore :US$5,000,000 / 1.8290 = £2,733,734.28 Sell £ at Malaysia : £2,733,734.28 x RM6.8755 = RM18,795,790.05 Buy Dollar at Malaysia : RM18,795,790.05 / 3.5025 =US$5,366,392.60 Gain from transaction: US$366,392.60

Anda rasa keliru...??? aku pon keliru... hehehe... aku rase.. dia punyer method dah ok dah.. Cuma yang tak conform mana nak amik.. bid ker ask... kalau aku salah.. tolong bagi tau yer... [email protected]

b) Under what circumstances might multinational firms be less subject to exchange rate risk than

purely domestic firms in the same industry?

Question 6 a. Given that the Australian dollar's spot rate is US$0.9000 and that the Australian and US one

year interest rates are initially 6%. Assume that the Australian one-year interest rate increases by 5%, while the US one-year interest rate remains unchanged.

i. Using the information and the International Fisher effect (IFE) theory, forecast the spot rate for one year ahead. (1 + �ℎ�)

(1 + ���)=

��

��

(1 + 0.06)

(1 + 0.11)=

��

0.9000

�� = �. ����

ii. According to the IFE, what is the underlying factor that would cause such a change? Answer: International Fisher Effect states that an estimated change in the current exchange rate between any two currencies is directly proportional to the difference between the two countries' nominal interest rates at a particular time

37 | P a g e

iii. If US investors believe in the IFE, will they attempt to capitalize on the higher Australian

interest rates? Explain. No. Because any extra gain in respect to higher interest rate as return from investment will be eliminate by Australian weaker currency and lower purchasing power.

b. Discuss why a MNC parent would consider foreign financing. Answer: 1. To offset account receivable from international trading 2. To take advantage on lower financing abroad (interest rate differ) 3. Lower financing cost

Question 7 a) Assume that a call option on Euro is written with a strike price of US$1.25/Euro at premium of

US$0,038 /Euro and with an expiration date three months from now. The option is for Euro 100,000. Calculate your profit or loss at maturity when the Euro is traded spot at:

ix. US$1.10/Euro Spot < Strike – out of Money let the option expire Loss on premium paid = 100,000 x US$0.038 = US$3,800

iii) US$1.30/Euro Spot > Strike Price – In the Money – exercise the option Spot Price US$1.3000 Strike US$1.2500 Gross US$0.0500 Premium US$0.0380 Nett US$0.0120 Ξ US$0.0120 x 100,000= US$1,200

b) Maria Sharapona works in the currency trading unit of Maybank in New York. Her latest speculative position is to profit from her expectation that the U.S. dollar will rise significantly against the Japanese yen. The current spot rate is US$0.9092/100¥. She must choose between the following 90-day option on the Japanese Yen: Option Strike Price Premium Put US$0.9050/100¥ US$0.003/100¥ Call US$0.9050/100¥ US$0.004/100¥

i. Should Maria buy a put on yen or a call on yen? Put Option

Dalam buku Jeff Madura – “ Put Option appropriate when currency expected to depreciate and Call Option when currency expected to appreciate”- jadi kat sini yang aku paham.. Dollar akan appreciate against Yen.. so. Yen relatively akan depreciate against Dollar. Position Maria sekarang nak beli option Yen kan..? wat per beli dollar.. sebab dia memang dah kat New York... tu yang aku paham ler... kalau aku salah paham.. tolong betul kan aku.. email ke [email protected]

ii. Using the answer in (a), what is the profit/loss Maria Sharapona faces if the spot rate at the end of the 90-day is 0.8820/100¥.

38 | P a g e

Strike :US$0.9050 -Spot :US$0.8820 Gross :US$0.0230 -premium :US$0.0040 Profit :US$0.0190

c) Describe the basic differences between futures, forward and options contracts.

To answer this question we look at area as follow: 1. Contract size 2. Maturity date 3. Delivery 4. Actual amount / cost involve in transaction (actual amount/ margin/ premium) 5. Purpose of enter into contract.

39 | P a g e

OCTOBER 2006

Question 1 a. What is the meaning of "immediate delivery" in foreign exchange transaction?

Answer: Immediate delivery is transaction (foreign exchange transaction) that must be delivered in two good business day at the spot rate.

b. In July the one-year interest rate is 10% on the British pound and 8% on US dollar. i. If the current exchange rate is US$1.5625/£. What is the expected future exchange rate in

one year? (1 + �ℎ�)�

(1 + ���)�=

��

��

1.08

1.10=

��

1.6525

�� = ��$1.6224

Soalan ni pasal Fisher Effect dalam chapter forecasting..

ii. Suppose a change in expectation regarding future US inflation causes the expected future spot rate to decline from US$1.5625 to US$1.5572. What should happen to US interest rate in one year's time? 1 + �ℎ�

1.10=

1.5572

1.6525

� + ��� = �. ��� ~ �. �%

c. Currently the spot exchange rate of is RM7.6220/£ and the one year forward rate is RM7.6550/£. Interest rate in UK is 7% per annum and in Malaysia is 9.5% per annum. Assume that you can borrow as much as £1.5 million or RM10,000,000 for your coming project: i. Determine whether interest rate parity is currently holding.

Annualize premium/discount = rhc-rfc 7.6550 − 7.6220

7.6220�

360

360�100 = 0.095 − 0.07

0.43 ≠ 2.5 Ξ interest rate parity not holding. There opportunity for arbitrage

ii. If the IRP were not holding, how would you carry out covered interest arbitrage? Show all

the steps and determine the arbitrage profit. Step 1: where to borrow? Where to invest?

[1.095] − 1 = ��7.6550

7.6220� �1.07� − 1

9.5% > 7.46%

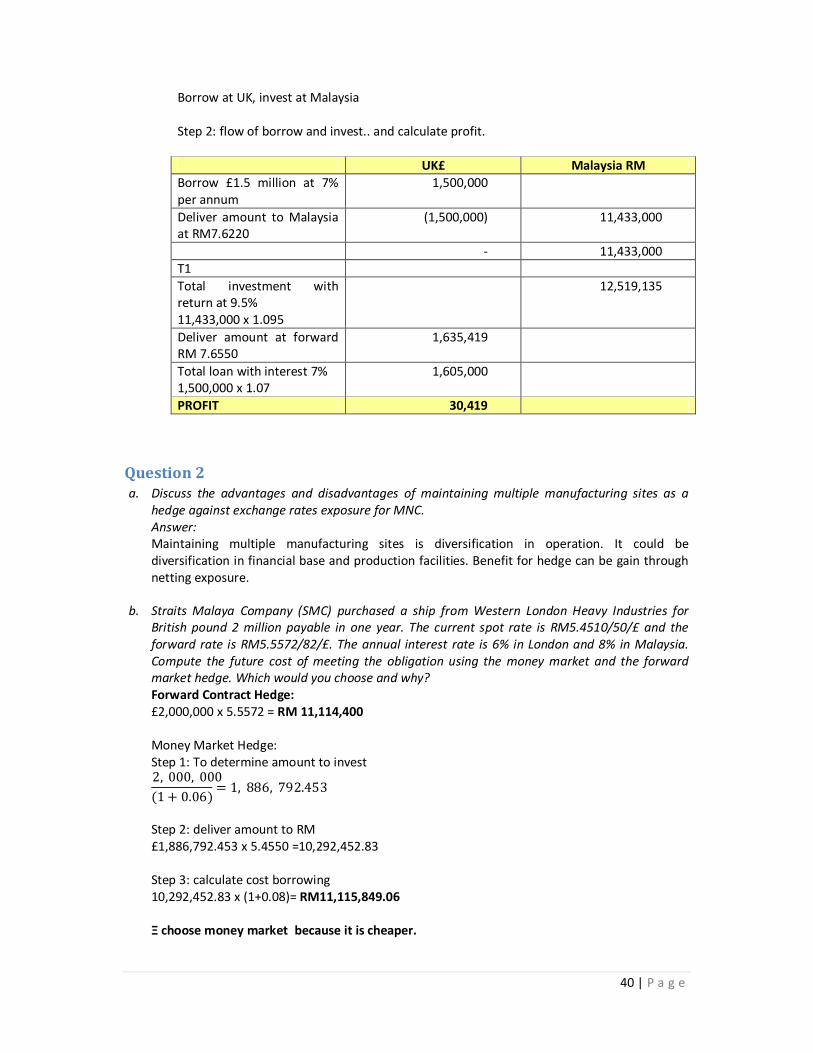

40 | P a g e

Borrow at UK, invest at Malaysia Step 2: flow of borrow and invest.. and calculate profit.

UK£ Malaysia RM Borrow £1.5 million at 7% per annum

1,500,000

Deliver amount to Malaysia at RM7.6220

(1,500,000) 11,433,000

- 11,433,000 T1

Total investment with return at 9.5% 11,433,000 x 1.095

12,519,135

Deliver amount at forward RM 7.6550

1,635,419

Total loan with interest 7% 1,500,000 x 1.07

1,605,000

PROFIT 30,419

Question 2 a. Discuss the advantages and disadvantages of maintaining multiple manufacturing sites as a

hedge against exchange rates exposure for MNC. Answer: Maintaining multiple manufacturing sites is diversification in operation. It could be diversification in financial base and production facilities. Benefit for hedge can be gain through netting exposure.

b. Straits Malaya Company (SMC) purchased a ship from Western London Heavy Industries for

British pound 2 million payable in one year. The current spot rate is RM5.4510/50/£ and the forward rate is RM5.5572/82/£. The annual interest rate is 6% in London and 8% in Malaysia. Compute the future cost of meeting the obligation using the money market and the forward market hedge. Which would you choose and why? Forward Contract Hedge: £2,000,000 x 5.5572 = RM 11,114,400 Money Market Hedge: Step 1: To determine amount to invest 2,000,000

(1 + 0.06)= 1,886,792.453

Step 2: deliver amount to RM £1,886,792.453 x 5.4550 =10,292,452.83 Step 3: calculate cost borrowing 10,292,452.83 x (1+0.08)= RM11,115,849.06 Ξ choose money market because it is cheaper.

41 | P a g e

Ni aku nak share apa yang aku faham tentang payable account. Payable account ni maksudnya company Malaysia (home country) berhutang dengan company luar Negara. Stategy settlement dia ada macam-macam, antaranya cash, credit term, forward contract, option, money market. a. Forward contract: Foward contract maksudnya kita berhutang, dan akan buat settlement katakan dalam tempoh satu

tahun. Tapi sebab risau exchange fluctuate, kita ikat ngan forward contract dengan bank kat Malaysia pada kadar tukaran yang dah ditetapkan awal-awal. Bila nak buat payabale account, kita mesti ambil rate “ask”.. sebab kita beli matawang lain untuk buat bayaran.

b. Money Market: dalam money market, strategy dia mudah tapi nak faham kene banyak berimiginasi sikit .Tapi secara