stock returns and the weekend effect: the malaysian experience papers/pert vol. 11 (1) apr... ·...

TRANSCRIPT

Pertanika 11(1), 107-114 (1988)

Stock Returns and the Weekend Effect:the Malaysian Experience

ANNUAR BIN MD. NASIR, SHAMSHER MOHAMAD and MOHAMAD ALI ABDUL HAMID

Department of Management StudiesFaculty of Economics and Management

Universiti Pertanian Malaysia43400 Serdang, Selangor, Malaysia

ABSTRAK

Gelagat pasaran pulangan saham dan kesan mingguan telah dikaji Kajian kami mengesahkanwujudnya kesan mingguan dipasaran saham Malaysia. Secara khususnya, dalam tempoh masa 1975-85,pulangan purata terendah berlaku pada hari Selasa dan kedua-dua pulangan purata pada hari Isnin danSelasa adalah negatif

ABSTRACT

Market behaviour of stock returns and the weekend effect were investigated. Our study confirmsthe presence of the day of the week effect or Monday effect in the Malaysian Stock Market In particular,over the 1975-1985 periods, the lowest mean return occurred on Tuesday and both Monday and Tuesdayreturns were negative.

INTRODUCTION

One of the most important areas of academicresearch in finance over the past twenty years hasbeen on efficient capital markets. An efficientcapital market is one in which security pricesadjust rapidly to the infusion of new informationand current stock prices fully reflect all availableinformation, An efficient market is also one inwhich prices provide accurate signals for resourceallocation, providing a rendezvous in which firmscan make production-investment decisions andinvestors can choose among securities that repre-sent ownership of a firm's activities.

An initial and very important assumption ofan efficient market is that a large number of profitmaximising participants are concerned with theanalysis and valuation of securities and that theseparticipants operate independently of each other.Another assumption is that new information re-garding securities comes to the market in a randomfashion and independent of one another. A finalassumption is that investors adjust security prices

rapidly to reflect the effect of new information.Although the price adjustment mechanism

may not be perfect, it is normally assumed to beunbiased (sometimes there is an over-adjustment,sometimes an under-adjustment but we don'tknow for sure what it will be). Furthermoresecurity prices that prevail at any time should bean unbiased reflection of all currently availableinformation. The previous price of a securityshould be an unbiased estimate of the currenttrue instrinsic value of the security ai that time,given all the information available. Hence thereturn implicit in the price should reflect the riskinvolved so that expected return is a function of risk.Although a preponderance of evidence supportsthe efficient market hypothesis, several studieshave provided evidence that is inconsistent withthe efficient capital market hypothesis.

Empirical research on capital market docu-menting size, weekend, January and recentlymonthly effects on stock returns represent in-teresting and puzzling empirical evidence on capi-

ANNUAR BIN MD. NASIR, SHAMSHER MOHAMAD AND MOHAMAD ALI ABDUL HAMID

tal market anomalies. One of the earliest evidenceon the capital market anomalies is the Monday orweekend effect.

Stock markets in developed countries likeUnited States, Japan, Australia, United Kingdomand Canada exhibit a strong tendency of seasonaleffects: Cross (1973), French(1980), Gibbon andHess (1981), Keim and Stambaugh (1984), Jaffeand Westerfield (1985a & 1985b), Harris (1986),Smirlock and Starks (1986), Wong and Ho (1986),Condoyanni et al (1987) and Penman (1987)provide interesting empirical evidence that theaverage return on Friday is abnormaly high whilethe average return on Monday is abnormaly low.Notably the average return for Monday (closeFriday to close Monday) is significantly negative.This so-called day of the week effect or weekendeffect is an empirical regularity for which notheoretical explanation has been found.

This paper intends to extend some empiricalresults found in developed stock markets to a newmarket place. In particular the paper provides anexamination of the day-to-day behaviour of stockmarket returns for Malaysia.

Review of Literature

Evidence of the day of the week effect or weekendeffect on stock prices has generally been obtainedfrom studies of daily close to close returns inbroad market indices. These studies have con-clusively identified systematic returns pattern —in particular the average return for Monday (closeFriday to close Monday) to be significantly negative.

French (1980) studied daily return on theStandard and Poor's Composite portfolio of the500 largest firms on the NYSE over the period1953-1977. He concluded that the average re-turns on Monday was significantly negative overalland during each of the five year sub-periods.

Keim and Stambaugh (1984) doubled thelength of period as examined by French (1980).Their results indicated consistently negative Mon-day returns (close Monday to close Friday)throughout the 55-year period. They found nega-tive Monday returns as early as 1928. They alsoreported that in periods with Saturday trading,Friday's return was generally lower than that ofSaturday,

Rogalski (1984) found the presence of week-end effect using Friday's close to Monday's open.

He discovered that all the average negative re-turns from Friday close to Monday close occurredduring the non trading period from Friday close toMonday open. In addition, average trading dayreturns (open to close) were identical for all daysof the week. He also showed that the size-Januaryeffect was interrelated with the weekend effect.

In another paper, Jaffe and Westerfield(1985a) found weekly seasonal effects on theJapanese stock markets. They found that thelowest means return in the Japanese stock marketoccurred on Tuesday and not Monday as in theUnited States. However, their results were consis-tent with Keim and Stambaugh's (1984) sugges-tion that in periods with Saturday trading, Fri-day's return is generally lower than Saturday'sreturn.

In providing international evidence on theweekend effect, Jaffe & Westerfield (1985b)tabulated similar behaviour of stock returnspattern in the United Kingdom, Japanese, Cana-dian, and Australian stock markets. In particularthey found the lowest means return for theJapanese and Australian stock markets ocurringon Tuesday.

Smirlock and Starks (1986) examined day ofthe week effect using hourly data of the DowJones Industrial Average. They confirmed theresults found by Rogalski (1984) which indicatedthat the weekend effect was due to the negativeaverage returns from Friday close to Mondayopen.

Harris (1986) found that for large firms,negative Monday returns accrued between Fridayclose and Monday open; for smaller firms theyaccrued primarily during the Monday's tradingday.

Wong and Ho (1986) examined the SingaporeStock Exchange All Share Index and six sectorialindexes. They found a weekly seasonal patternsimilar to those in U.K., U.S. and Canada.

Condoyanni et al (1987) examined the week-end effect on seven stock exchanges namely, NewYork, Sydney, Toronto, London, Tokyo, Parisand Singapore. They tentatively suggest that theweekend effect which was documented on theseven stock exchanges appear to be the normrather than the exception in a range of capitalmarkets around the world.

Penman (1987) found that firms tend to

108 PERTANIKA VOL. 11 NO. 1, 1988

STOCK RETURNS AND THE WEEKEND EFFECT

publish bad news earning reports on Mondays,coincident with the negative Monday effect instock returns.

Suggested Explanation

Previous authors have mentioned settlement proce-dures and measurement errors as plausible reasonsfor such behaviour. Settlement procedures refer todelay of cash payment for stock purchase andcash receipt for selling before stock certificatesexchange hands. For example,according to Lakoni-shok and Levi (1981), since 1968 it has been theestablished practice in the U.S for the settlementon stocks to take place five business days aftertrading. In an ordinary week that does not containany holidays, this means that payment is due onthe same day of the week as the trade, but in thefollowing week. Cheques normally take one busi-ness day to clear from the time they are deliveredto the commercial banks to the time that usablefunds are debited and credited. This clearing delaymeans that in weeks without a holiday, stocks pur-chased on business days other than Friday givesthe buyer eight calender days before losing fundsfor stock purchases. These eight days are the fivebusiness days for settlement, the two weekenddays and the cheque clearing day. However, pay-ment for stock purchased on Friday will notoccur until the second following Monday, tencalendar days after the trade. These ten days arethe five business days for settlement, the twoweekends and the cheque clearing day. Buyersshould therefore be prepared to pay more on aFriday than any other by the amount of the twodays interest. The sellers of stock should also re-quire a higher price for stocks sold on a Fridaybecause of the two extra day delay before beingpaid. Hence the equilibrium expected rate ofreturn on Friday should be higher than on otherdays. As such, the equilibrium expected rate ofreturn on Monday should be lower by two daysof interest than the return expected.

Measurement errors could be caused by up-wardly biased quotes at Friday closing price. Forexample, Keim and Stambaugh (1984) suggest thatFriday's closing price might be affected by random

errors which are generally positive and Monday'sclosing price might be affected by generally nega-tive random errors. They found a higher thanaverage negative correlation between returns onthese two days for U.S data, thus suggesting apossibility of random type of measurement errors.

Another immediate natural reaction to ex-plain this phenomenon is that firms wait untilafter the close of the market on Friday to an-nounce bad news. The news is then reflected inthe stock price on Monday. The problem is that ifthe market is efficient, it would anticipate suchbehaviour and discount Friday prices to accountfor the bad news.

MATERIALS AND METHODS

Previous studies on the Malaysian capital marketsfocus on the market efficiency and risk return rela-tionship. These include those of Othman Yong(1987), Neoh (1986), Khoo and Tan (1986),Nassir(1983), Dawson (1981), Cheng (1978), Lim(1980), Laurence (1986) and Barnes (1986). Mostof these studies documented weak form efficiencyand inefficiency of the Malaysian stock market1

Little has been done or known on the stock mar-ket anomalies particularly the Monday effect.Studies (see Cootner, 1964 and Fama 1965) indaily stock market prices have shown that thebehaviour of stock prices closely follow a multi-plicative random walk where

= Pt _ j [exp

where Pt is the price at the end of period t, D.the dividend paid during period t, E(Rt) the ex-pected return in period t and et a serially indepen-dent random variable whose expected value iszero. This model is equivalent to

Rt =

where Rt is the continuously compounded returnobserved in period t.

To test the hypothesis about daily returnbehaviour, it is assumed that, for any particularday of the week, .the expected return is constant

1/ A survey of empirical studies on market efficiency of the KLSE is summarised in Annuar et. al (1987)

PERTANIKA VOL. 11 NO. 1, 1988 109

ANNUAR BIN MD. NASIR, SHAMSHER M O H A M A D AND MOHAMAD ALI ABDUL HAMID

and that the error term is drawn from a stationarynormal distribution. This assumption implies thatthe expected return for every Friday is the sameand that every Friday error term is drawn from*the same distribution. This can be summarized asfollows:

Rt

where subscript d indicates the day of the weekin which the return i observed.

Following the model of daily stock returns,two measures of returns are suggested

100 (1)

R t = ( V t " V t - 1 / V t - 1 > *

where V. indicates common stock market index atthe end of day t.

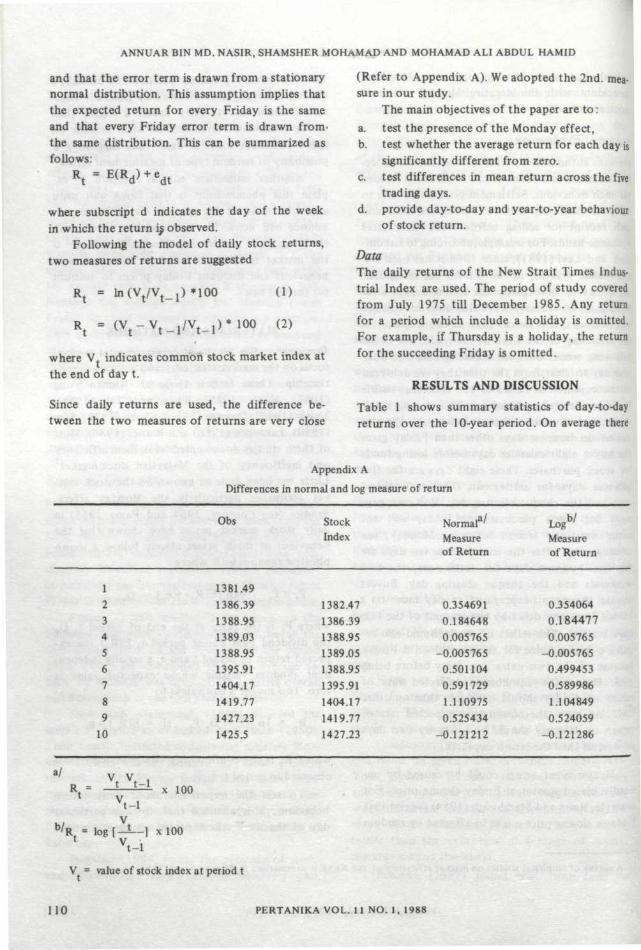

Since daily returns are used, the difference be-tween the two measures of returns are very close

(Refer to Appendix A). We adopted the 2nd. mea-sure in our study.

The main objectives of the paper are to:

a. test the presence of the Monday effect,b. test whether the average return for each day is

significantly different from zero.c. test differences in mean return across the five

trading days.d. provide day-to-day and year-to-year behaviour

of stock return.

DataThe daily returns of the New Strait Times Indus-trial Index are used. The period of study coveredfrom July 1975 till December 1985. Any returnfor a period which include a holiday is omitted.For example, if Thursday is a holiday, the returnfor the succeeding Friday is omitted.

RESULTS AND DISCUSSION

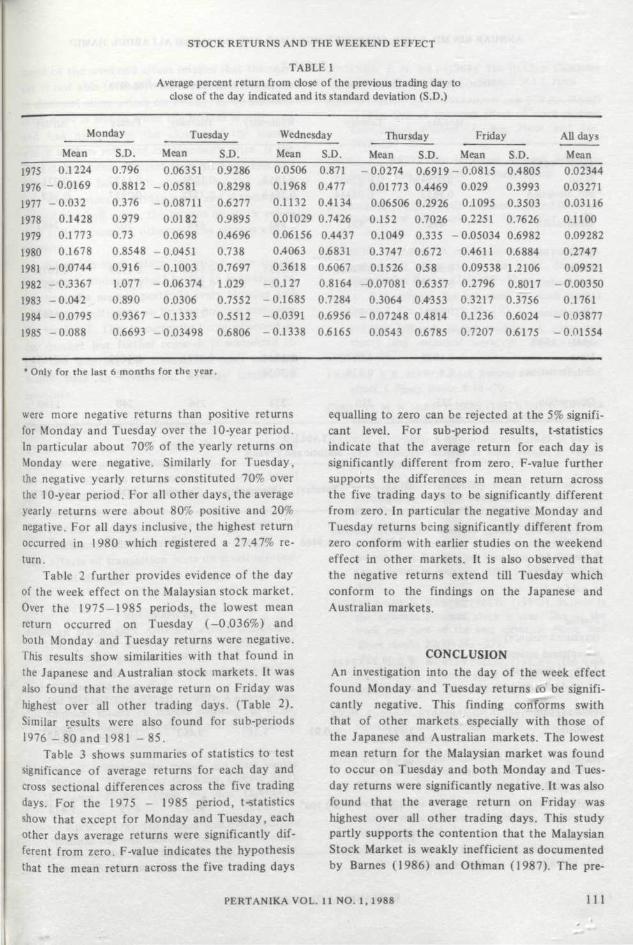

Table 1 shows summary statistics of day-to-dayreturns over the 10-year period. On average there

Appendix A

Differences in normal and log measure of return

1

2

3

4

5

6

7

8

9

10

Obs

1381.49

1386.39

1388.95

1389.03

1388.95

1395.91

1404.17

1419.77

1427.23

1425.5

StockIndex

1382.47

1386.39

1388.95

1389.05

1388.95

1395.91

1404.17

1419.77

1427.23

Normal^Measureof Return

0.354691

0.184648

0.005765

-0.005765

0.501104

0.591729

M10975

0.525434

-0.121212

Logb/

Measureof Return

0.354064

0.1844770.005765

-0.0057650.4994530.5899861.1048490.524059

-0.121286

a /

VV V

v t - lv

b /R. = l og [— L - ] xlOOt v

v t - l

V = value of stock index at period t

110 PERTANIKA VOL. 11 NO. 1, 1988

STOCK RETURNS AND THE WEEKEND EFFECT

TABLE 1

Average percent return from close of the previous trading day toclose of the day indicated and its standard deviation (S.D.)

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

Monday

Mean

0.1224

- 0.0169

- 0 . 0 3 2

0.1428

0.1773

0.1678

- 0 . 0 7 4 4

- 0 . 3 3 6 7

- 0 . 0 4 2

-0 .0795

- 0 . 0 8 8

S.D.

0.796

0.8812

0.376

0.979

0.73

0.8548

0.916

1.077

0.890

0.9367

0.6693

Tuesday

Mean

0.06351

- 0 . 0 5 8 1

-0 .08711

0.0182

0.0698

- 0 . 0 4 5 1

- 0 . 1 0 0 3

-0 .06374

0.0306

- 0 . 1 3 3 3

- 0 . 0 3 4 9 8

S.D.

0.9286

0,8298

0.6277

0.9895

0.4696

0.7380.76971.0290.75520.55120.6806

Wednesday

Mean0.05060.19680.11320.010290.061560.40630.3618

-0.127-0.1685-0.0391-0.1338

S.D.0.8710.4770.41340.74260.44370.68310.60670.81640.72840.69560.6165

Thursday

Mean-0.0274

0.017730.065060.1520.10490.37470.1526

-0.07081

0.3064

- 0.07248

0.0543

S.D.

0.6919

0.4469

0.2926

0.7026

0.335

0.672

OJ58

0.6357

0.4*353

0.4814

0.6785

Friday

Mean

- 0 . 0 8 1 5

0.029

0.1095

0.2251

- 0.05034

0.4611

0,09538

0.2796

0.3217

0.1236

0.7207

S.D.

0.4805

0.3993

0.3503

0.7626

0.6982

0.6884

1.2106

0.8017

0.3756

0.6024

0.6175

All days

Mean

0.02344

0.03271

0.03116

0.1100

0.09282

0.2747

0.09521

- 0.00350

0.1761

-0 .03877

-0 .01554

* Only for the last 6 months for the year.

were more negative returns than positive returnsfor Monday and Tuesday over the 10-year period.In particular about 70% of the yearly returns onMonday were negative. Similarly for Tuesday,the negative yearly returns constituted 70% overthe 10-year period. For all other days, the averageyearly returns were about 80% positive and 20%negative. For all days inclusive, the highest returnoccurred in 1980 which registered a 27.47% re-turn.

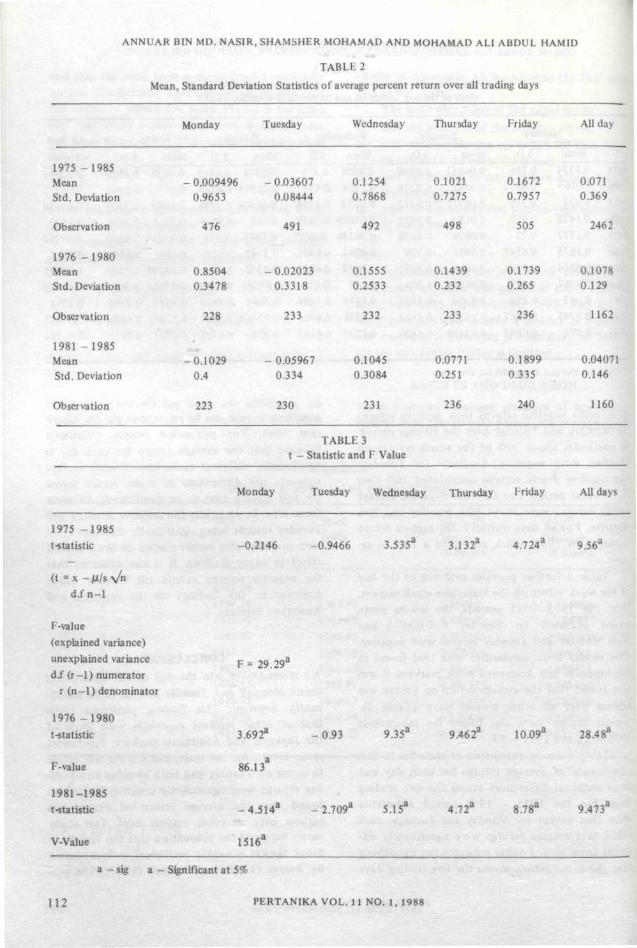

Table 2 further provides evidence of the dayof the week effect on the Malaysian stock market.Over the 1975-1985 periods, the lowest meanreturn occurred on Tuesday (-0.036%) andboth Monday and Tuesday returns were negative.This results show similarities with that found inthe Japanese and Australian stock markets. It wasalso found that the average return on Friday washighest over all other trading days. (Table 2).Similar results were also found for sub-periods1976 - 8 0 and 1981 - 8 5 .

Table 3 shows summaries of statistics to testsignificance of average returns for each day andcross sectional differences across the five tradingdays. For the 1975 - 1985 period, tstatisticsshow that except for Monday and Tuesday, eachother days average returns were significantly dif-ferent from zero, F-value indicates the hypothesisthat the mean return across the five trading days

equalling to zero can be rejected at the 5% signifi-cant level. For sub-period results, t-statisticsindicate that the average return for each day issignificantly different from zero. F-value furthersupports the differences in mean return acrossthe five trading days to be significantly differentfrom zero. In particular the negative Monday andTuesday returns being significantly different fromzero conform with earlier studies on the weekendeffect in other markets. It is also observed thatthe negative returns extend till Tuesday whichconform to the findings on the Japanese andAustralian markets.

CONCLUSIONAn investigation into the day of the week effectfound Monday and Tuesday returns LO be signifi-cantly negative. This finding conforms swiththat of other markets especially with those ofthe Japanese and Australian markets. The lowestmean return for the Malaysian market was foundto occur on Tuesday and both Monday and Tues-day returns were significantly negative. It was alsofound that the average return on Friday washighest over all other trading days. This studypartly supports the contention that the MalaysianStock Market is weakly inefficient as documentedby Barnes (1986) and Othman (1987). The pre-

PERTANIKA VOL. 11 NO. 1, 1988 111

ANNUAR BIN MD. NASIR, SHAMSHER MOHAMAD AND MOHAMAD ALI ABDUL HAMID

TABLE 2

Mean, Standard Deviation Statistics of average percent return over all trading days

1975 -1985MeanStd. Deviation

Observation

1976 -1980MeanStd. Deviation

Observation

1981 -1985MeanStd. Deviation

Observation

Monday

- 0.0094960.9653

476

0.85040.3478

228

-0.10290.4

223

Tuesday

- 0.036070.08444

491

-0.020230.3318

233

- 0.059670.334

230

Wednesday

0.12540.7868

492

0.15550.2533

232

0.10450.3084

231

TABLE 3t - Statistic and F Value

Thursday

0.10210.7275

498

0.14390.232

233

0.07710.251

236

Friday

0.16720.7957

505

0.17390.265

236

0.18990.335

240

All day

0.0710.369

2462

0.10780.129

1162

0.040710.146

1160

Monday Tuesday Wednesday Thur sday Friday All days

1975 -1985t-statistic -0.2146 -0.9466 3.535d 3.132* 4.724d 9.56*

(t =x -d.fn-1

F-value(explained variance)unexplained varianced.f (r-1) numerator

r (n-1) denominator

1976 -1980t-statistic

F= 29.29d

3.692a -0 .93 9.35a 9.462* 10.09d 28.48d

F-value

1981-1985t-statistic

86.13

-4.514 a -2.709 a 5.15a 4.72d 8.78* 9.473a

V-Value 1516*

a - sig a - Significant at 5%

112 PERTANIKA VOL. 11 NO. 1, 1988

STOCK RETURNS AND THE WEEKEND EFFECT

sence of the weekend effect implies that the mar-ket is not able to absorb all available informationto discount share prices on Friday, as we assumedgood news is leaked while the market is still openand bad news after the closure of the marketwhich is then reflected on Monday's price. If themarket had been efficient then all good and badnews should have been absorbed by the marketinto stock prices on Friday itself, and if good newsexceed the bad news, the returns on stock pricesmay still be positive; otherwise the returns will benegative.

Based on such return behaviour, one simpleinvestment strategy would be for an individual topurchase the market portfolio every Monday andsell these investments on Friday, holding cash overthe weekend. This is currently being observed inour market but further research is warranted tofind out whether the transaction costs incurredmakes such an investment strategy feasible toinvestors.

Suggestion for Further Research

Further research on the day of the week effect in

the following areas are suggested:(i) comprehensive examination for other broad

market indexes and stock returns of individual

companies,

(ii) further evidence on measurement errors and

settlement procedures,

(iii) effects of transaction costs on investor invest-

ment strategy.

REFERENCESANNUAR MD NASSIR AND SHAMSHER MOHAMAD

(1987a): What weekend does to KLSE. InvestorDigest, Mid-August issue, 3-4.(1987b): Cheers for the new year, Investor Digiest,

1 Mid-November issue, 4-5 .and SHAMSUDIN ISMAIL, (1987): A survey of em-empirical studies on market efficiency of KLSE.Unpublished report, Faculty of Economics and Mana-gement, UPM.

BARNES, P. (1986): Thin trading and stock marketefficiency: The case of the Kuala Lumpur StockExchange. /. Bus. Finan. and Ace. 13(4):609-617.

CHENG KIEW, (1978): The random walk hypothesis: Anempirical test with Malaysian shareprices. Occasionalpaper, Faculty of Economics and Management,Universiti Kebangsaan Malaysia.

COOTNER, P. H. (ed.) (1964): The Random Characterof Stock Market Prices. Cambridge: M.I.T. Press

CONDOYANNI, L., J. O'HANLON and C.W.R. WARD(1987): Day of the week effect on stock returns:International evidence. /. Bus. Finan. and Ace.14(2):159-75.

CROSS, F. (1973): The behaviour of stock prices onFridays and Mondays. Finan. Analy. / . 28:67-^69.

D'AMBROSIO, C.A. (1980): Random walk and the stockexchange of Singapore. The Finan. Rev. 15(2):1-9.

DAWSON, S. (1981): A test of stock recommendationand market efficiency for the KLSE, SingaporeManagement Review. (July):69-72.

FAMA, E.F. (1965): The behaviour of stock marketprices./. Bus. (January): 34-105.

(1970): Efficient capital markets: A review oftheory and empirical work, / . Finan. (May):383-417.

FRENCH, K.R. (1980): Stock Returns and the weekendeffect./. Finan. Econs. 8:55-70.

GIBBONS, M. R. and P. J. HESS (1981): Day of the weekeffects and assets return./. Bus. 54:579-596.

HARRIS, L. (1986): A transaction data study of weeklyand intradaily patterns in stock return. / . Finan.Econs. 16:99-117.

HONG, H. (1978): Predictability of price trends on stockexchange: A study of some far eastern countries.Rev. Econs. andStat. 60(4): 619-621.

ISMAIL ZAKRI MD. KHALID (1986): The developmentof a sound securities market in Malaysia. Paperpresented at Seminar on Securities and Commodi-ties Industry in Malaysia, April 5, 1986 ITM, ShahAlam.

JAFFE, J. and R. WESTERFIELD, (1985a): Pattern inthe Japanese common stock returns: Day of theweek and turn of the year effect. / . Finan. andQuart Analy. 20(2): 261-272.

JAFFE, J. and R. WESTERFIELD, (1985b): The weekend effect in common stock returns: The interna-tional evidence./. Finan. 40:432-453.

KEIM, D. and R. STAMBAUGH (1984): A further inves-tigation of the week end effect in stock return.J. Finan. 39:819-834.

LIM, T.L, (1980): The efficient market hypotesis andweak form tests on the KLSE, MBA Dissertation,Sheffield U. Library, University of Sheffield.

KHONG, T.S. and T.K. HOW, (1986): The KLSE: To-wards a more efficient stock market. Bankers Jour-nal Malaysia. 35:9-14.

LAKONISHOK J. and M. LEVI, (1982): Weekend effectson stock returns: A note. /. Finan. 37:883-889.

PERTANIKA VOL. 11 NO. 1, 1988 113

ANNUAR BIN MD. NASIR, SHAMSHER MOHAMAD AND MOHAMAD ALI ABDUL HAMID

LAURENCE, M.M. (1986): Weak form efficiency in theKuala Lumpur and Singapore Stock .Exchange./. Bus., Finan. and Ace. 10:431-445.

MOHD NASSIR LANJONG (1983): Efficiency of theMalaysian stock market and risk-return relation-ship." Unpublished Ph.D thesis. Katholieke Universi-tiet Leuven, Belgium.

NEOH, SOON KEAN (1986): Stock Market Investmentin Malaysia and Singapore, Berita Publishing Sdn.Bhd.

OTHMAN YONG (1987): A study of the weak formefficient market hypothesis of the Kuala LumpurStock Exchange. Unpublished Ph. D. Dissertation,Mississippi State University.

PENMAN, S.H. (1987): The distribution of earning newsover time and seasonalities in aggregate stock re-turn. / . Finan. Econs. (in print)

ROGALSKI, RICHARD, (1984): New findings regardingday of the week returns over trading and non tradingperiods./. Finan. 39:1603-1614.

SMIRLOCK, M. and LAURA STARKS, (1986): Day ofthe week and intra day effects in stock returns,J. Finan. Econs. 17:197-210.

WONG, K.A. and HlN-DONG D. HO (1986): The week-end effect on stock returns in Singapore, Hong KongJournal Business Management. 4:51-66.

(Received 27 March, 1987)

114 PERTANIKA VOL. 11 NO. 1, 1988