session 1 datuk wan selamah

DESCRIPTION

caseTRANSCRIPT

1

By:By:By:By:

Datuk Wan Selamah binti Wan SulaimanDatuk Wan Selamah binti Wan SulaimanDatuk Wan Selamah binti Wan SulaimanDatuk Wan Selamah binti Wan Sulaiman

Accountant General of MalaysiaAccountant General of MalaysiaAccountant General of MalaysiaAccountant General of Malaysia

CURRENT STATUS OF PUBLIC SECTOR CURRENT STATUS OF PUBLIC SECTOR CURRENT STATUS OF PUBLIC SECTOR CURRENT STATUS OF PUBLIC SECTOR ACCOUNTING IN MALAYSIA AND THE WAY ACCOUNTING IN MALAYSIA AND THE WAY ACCOUNTING IN MALAYSIA AND THE WAY ACCOUNTING IN MALAYSIA AND THE WAY

FORWARDFORWARDFORWARDFORWARD

2

OVERVIEWOVERVIEWOVERVIEWOVERVIEW

• IntroductionIntroductionIntroductionIntroduction

• Where Are We NowWhere Are We NowWhere Are We NowWhere Are We Now

• The Way ForwardThe Way ForwardThe Way ForwardThe Way Forward

• ConclusionConclusionConclusionConclusion

INTRODUCTION

Components of Public Sector

• Federal Government

• State Government

• Federal Statutory Bodies

• State Statutory Bodies

• Local Government, Town, District Councils &

City Halls

• Islamic Council of Malaysia

Governing Laws & Regulations

4

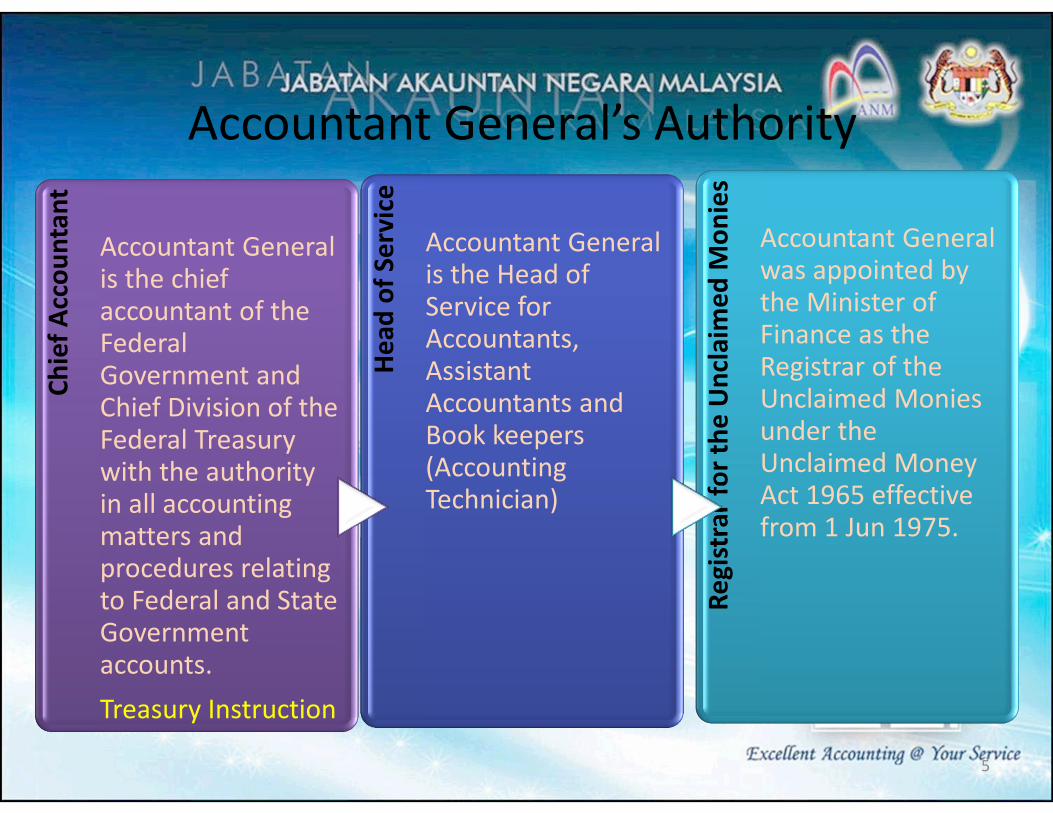

Accountant General’s Authority

Ch

ief

Acc

ou

nta

nt

Accountant General is the chief accountant of the Federal Government and Chief Division of the Federal Treasury with the authority in all accounting matters and procedures relating to Federal and State Government accounts.

Treasury Instruction

He

ad

of

Se

rvic

e

Accountant General is the Head of Service for Accountants, Assistant Accountants and Book keepers (Accounting Technician)

Re

gis

tra

r fo

r th

e U

ncl

aim

ed

Mo

nie

s

Accountant General was appointed by the Minister of Finance as the Registrar of the Unclaimed Monies under the Unclaimed Money Act 1965 effective from 1 Jun 1975.

5

Where Are We Now?

• Current Basis of Accounting

• Current Accounting Standards

• Financial Statement Performance

• Timeliness

• Quality

• Current Accounting System

6

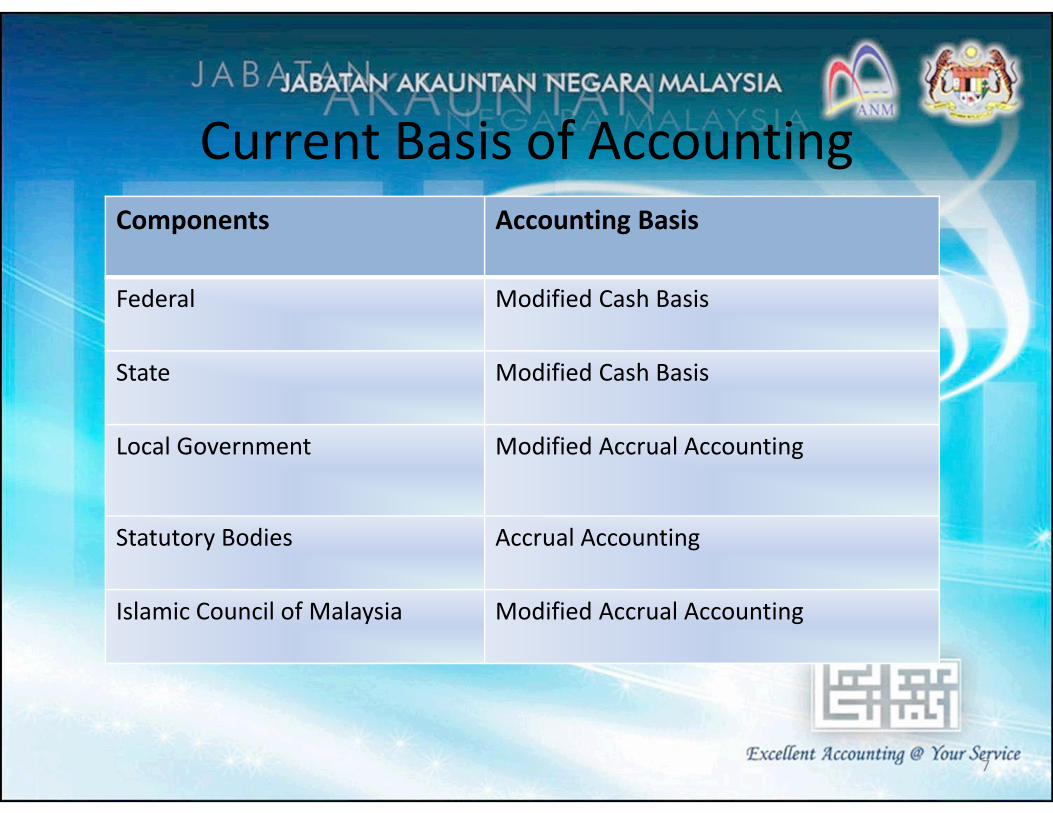

Current Basis of Accounting

Components Accounting Basis

Federal Modified Cash Basis

State Modified Cash Basis

Local Government Modified Accrual Accounting

Statutory Bodies Accrual Accounting

Islamic Council of Malaysia Modified Accrual Accounting

7

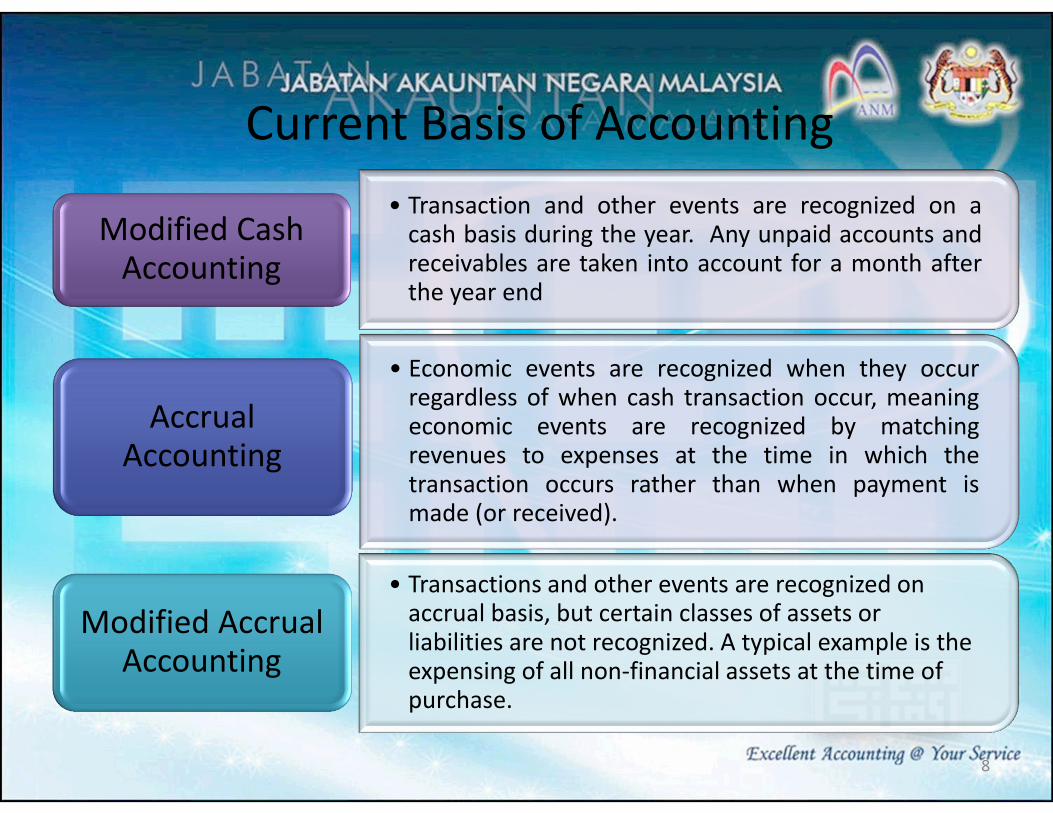

Current Basis of Accounting

• Transaction and other events are recognized on acash basis during the year. Any unpaid accounts andreceivables are taken into account for a month afterthe year end

Modified Cash Accounting

• Economic events are recognized when they occurregardless of when cash transaction occur, meaningeconomic events are recognized by matchingrevenues to expenses at the time in which thetransaction occurs rather than when payment ismade (or received).

Accrual Accounting

• Transactions and other events are recognized on accrual basis, but certain classes of assets or liabilities are not recognized. A typical example is the expensing of all non-financial assets at the time of purchase.

Modified Accrual Accounting

8

Limitation of Modified Cash Basis

• Simpler but the concept is

unfamiliar

• Ease of manipulation

• Less comprehensive – cash

information only

• Provides only basic information –

commitment information are not

available

• Higher implementation cost –

because of customization and

limited availability

• No information provided for non

financial asset management

• Limited credibility and

accountability (especially by

Rating Agency)

• Limited basis for determining

fiscal strategy

• Limited product/service pricing

• Limited disincentives for fraud

and corruption

9

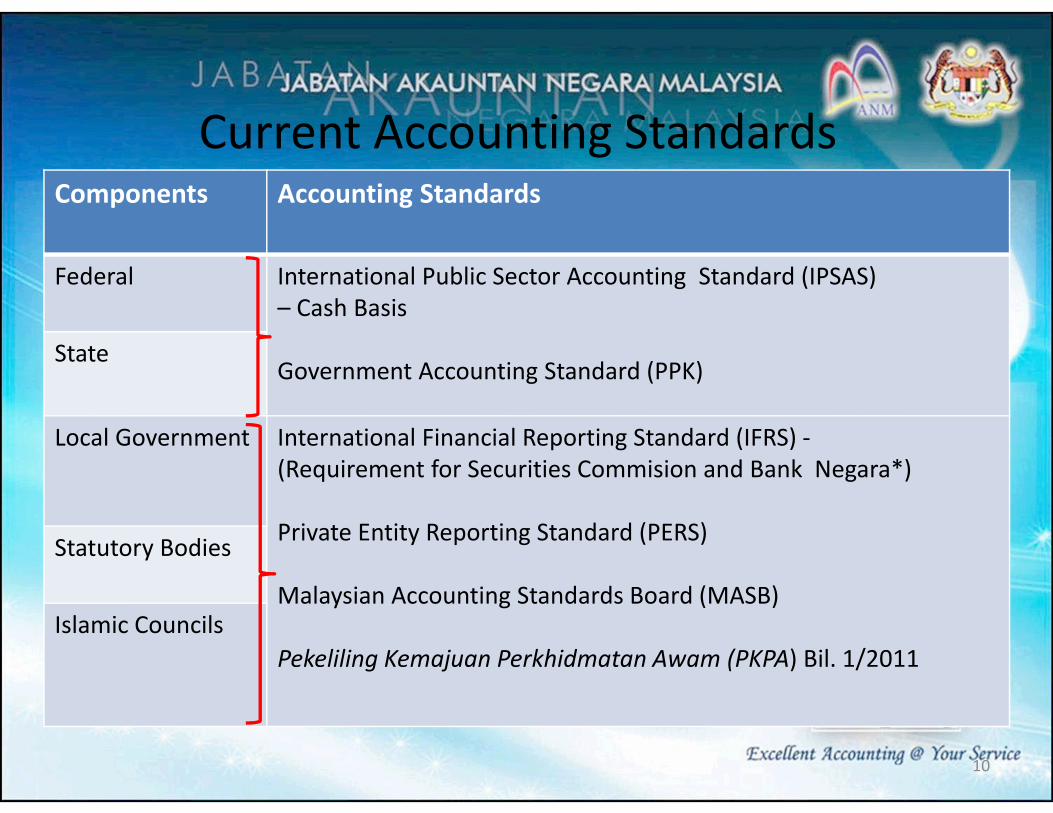

Current Accounting StandardsComponents Accounting Standards

Federal International Public Sector Accounting Standard (IPSAS)

– Cash Basis

Government Accounting Standard (PPK)State

Local Government International Financial Reporting Standard (IFRS) -

(Requirement for Securities Commision and Bank Negara*)

Private Entity Reporting Standard (PERS)

Malaysian Accounting Standards Board (MASB)

Pekeliling Kemajuan Perkhidmatan Awam (PKPA) Bil. 1/2011

Statutory Bodies

Islamic Councils

10

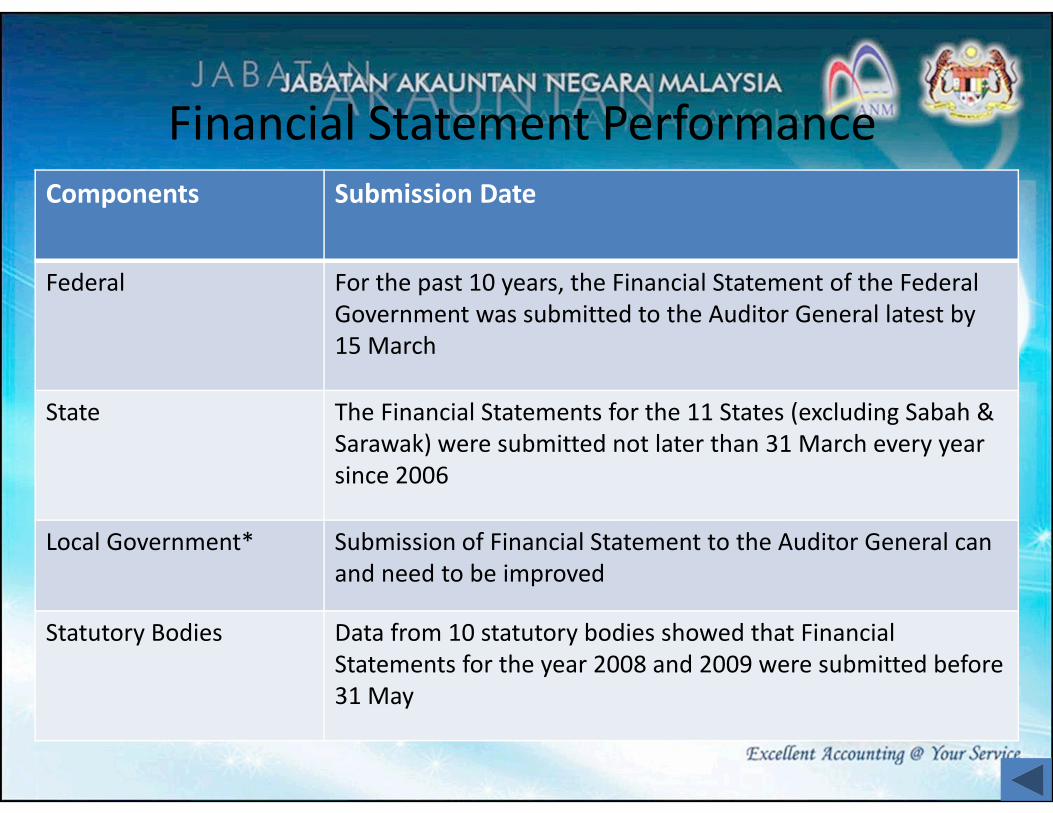

Financial Statement Performance

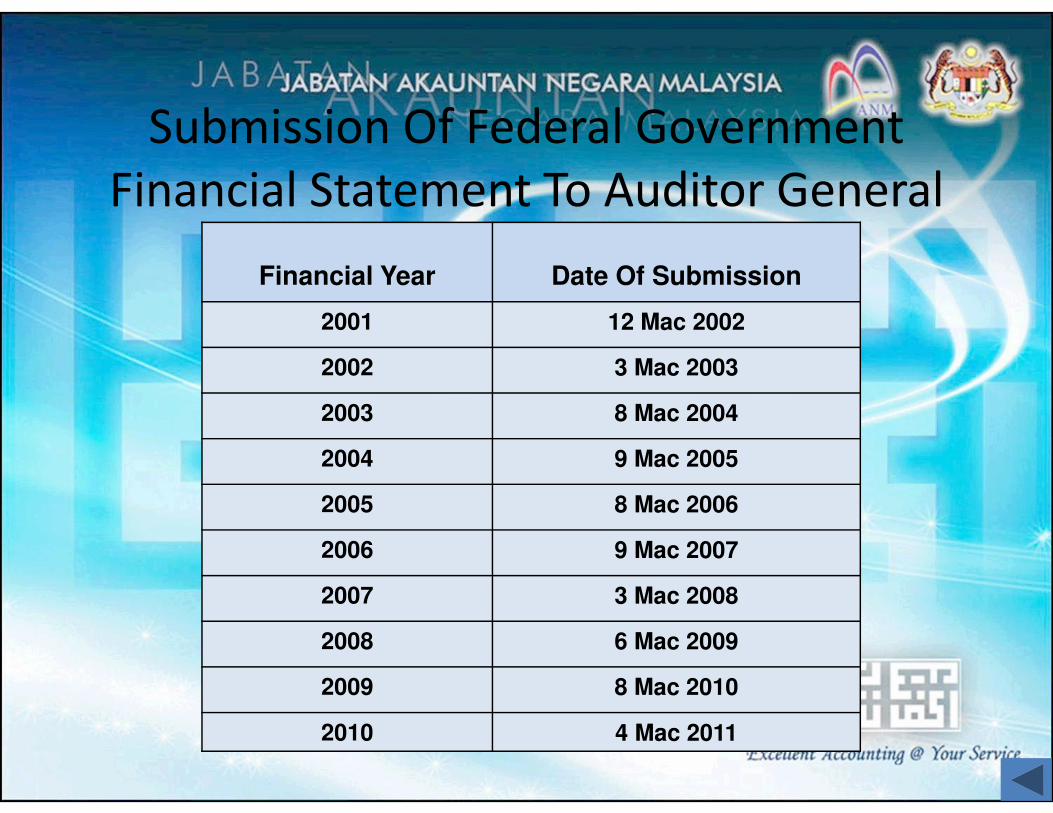

Components Submission Date

Federal For the past 10 years, the Financial Statement of the Federal

Government was submitted to the Auditor General latest by

15 March

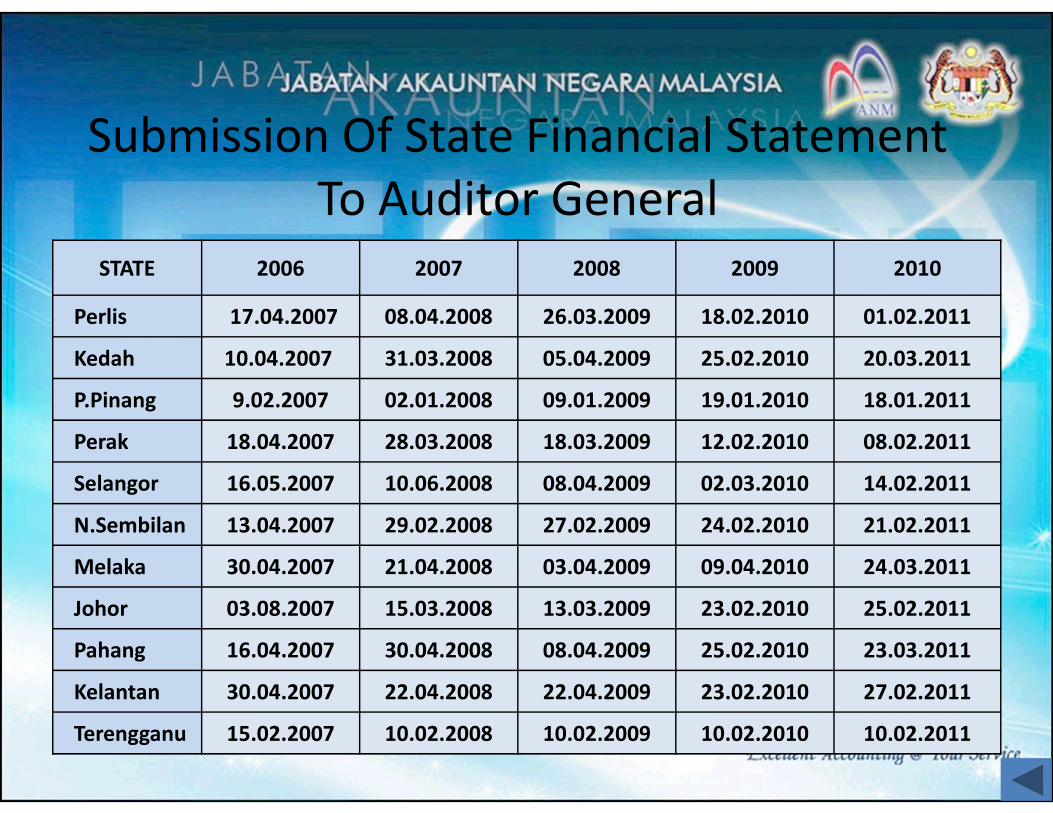

State The Financial Statements for the 11 States (excluding Sabah &

Sarawak) were submitted not later than 31 March every year

since 2006

Local Government* Submission of Financial Statement to the Auditor General can

and need to be improved

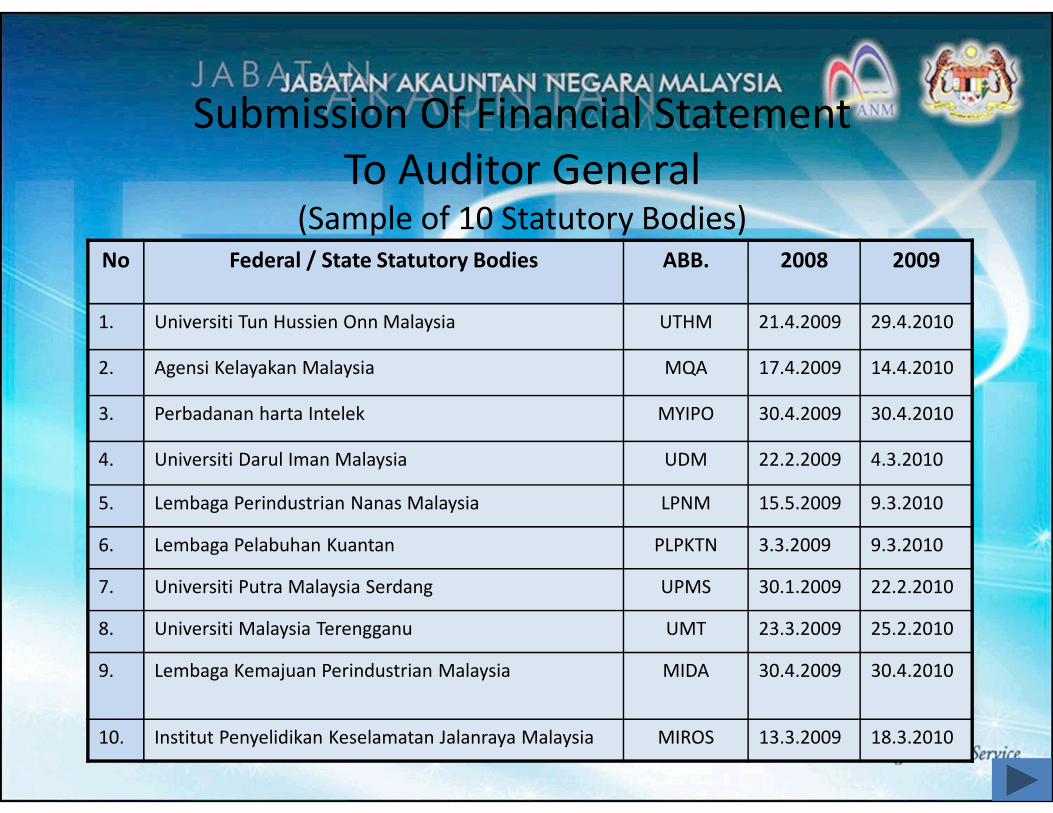

Statutory Bodies Data from 10 statutory bodies showed that Financial

Statements for the year 2008 and 2009 were submitted before

31 May

Financial Year Date Of Submission

2001 12 Mac 2002

2002 3 Mac 2003

2003 8 Mac 2004

2004 9 Mac 2005

2005 8 Mac 2006

2006 9 Mac 2007

2007 3 Mac 2008

2008 6 Mac 2009

2009 8 Mac 2010

2010 4 Mac 2011

Submission Of Federal Government

Financial Statement To Auditor General

Submission Of State Financial Statement

To Auditor General

STATE 2006 2007 2008 2009 2010

Perlis 17.04.2007 08.04.2008 26.03.2009 18.02.2010 01.02.2011

Kedah 10.04.2007 31.03.2008 05.04.2009 25.02.2010 20.03.2011

P.Pinang 9.02.2007 02.01.2008 09.01.2009 19.01.2010 18.01.2011

Perak 18.04.2007 28.03.2008 18.03.2009 12.02.2010 08.02.2011

Selangor 16.05.2007 10.06.2008 08.04.2009 02.03.2010 14.02.2011

N.Sembilan 13.04.2007 29.02.2008 27.02.2009 24.02.2010 21.02.2011

Melaka 30.04.2007 21.04.2008 03.04.2009 09.04.2010 24.03.2011

Johor 03.08.2007 15.03.2008 13.03.2009 23.02.2010 25.02.2011

Pahang 16.04.2007 30.04.2008 08.04.2009 25.02.2010 23.03.2011

Kelantan 30.04.2007 22.04.2008 22.04.2009 23.02.2010 27.02.2011

Terengganu 15.02.2007 10.02.2008 10.02.2009 10.02.2010 10.02.2011

Submission Of Financial Statement

To Auditor General (Sample of 10 Statutory Bodies)

No Federal / State Statutory Bodies ABB. 2008 2009

1. Universiti Tun Hussien Onn Malaysia UTHM 21.4.2009 29.4.2010

2. Agensi Kelayakan Malaysia MQA 17.4.2009 14.4.2010

3. Perbadanan harta Intelek MYIPO 30.4.2009 30.4.2010

4. Universiti Darul Iman Malaysia UDM 22.2.2009 4.3.2010

5. Lembaga Perindustrian Nanas Malaysia LPNM 15.5.2009 9.3.2010

6. Lembaga Pelabuhan Kuantan PLPKTN 3.3.2009 9.3.2010

7. Universiti Putra Malaysia Serdang UPMS 30.1.2009 22.2.2010

8. Universiti Malaysia Terengganu UMT 23.3.2009 25.2.2010

9. Lembaga Kemajuan Perindustrian Malaysia MIDA 30.4.2009 30.4.2010

10. Institut Penyelidikan Keselamatan Jalanraya Malaysia MIROS 13.3.2009 18.3.2010

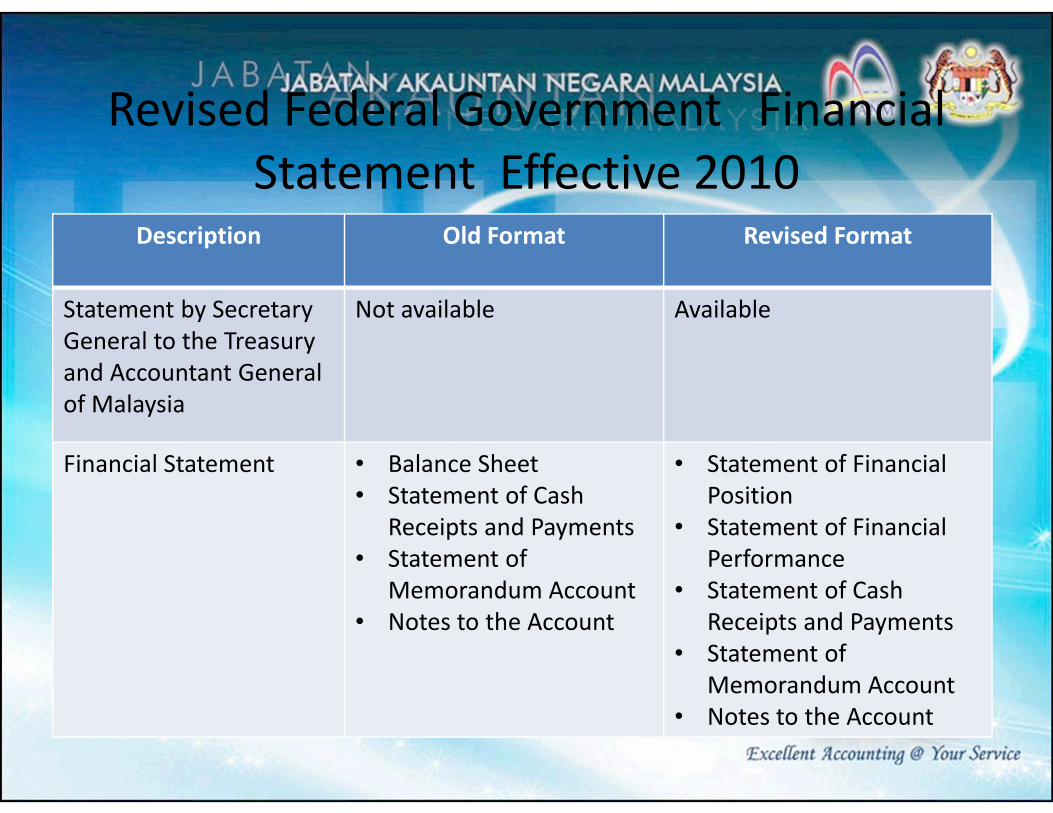

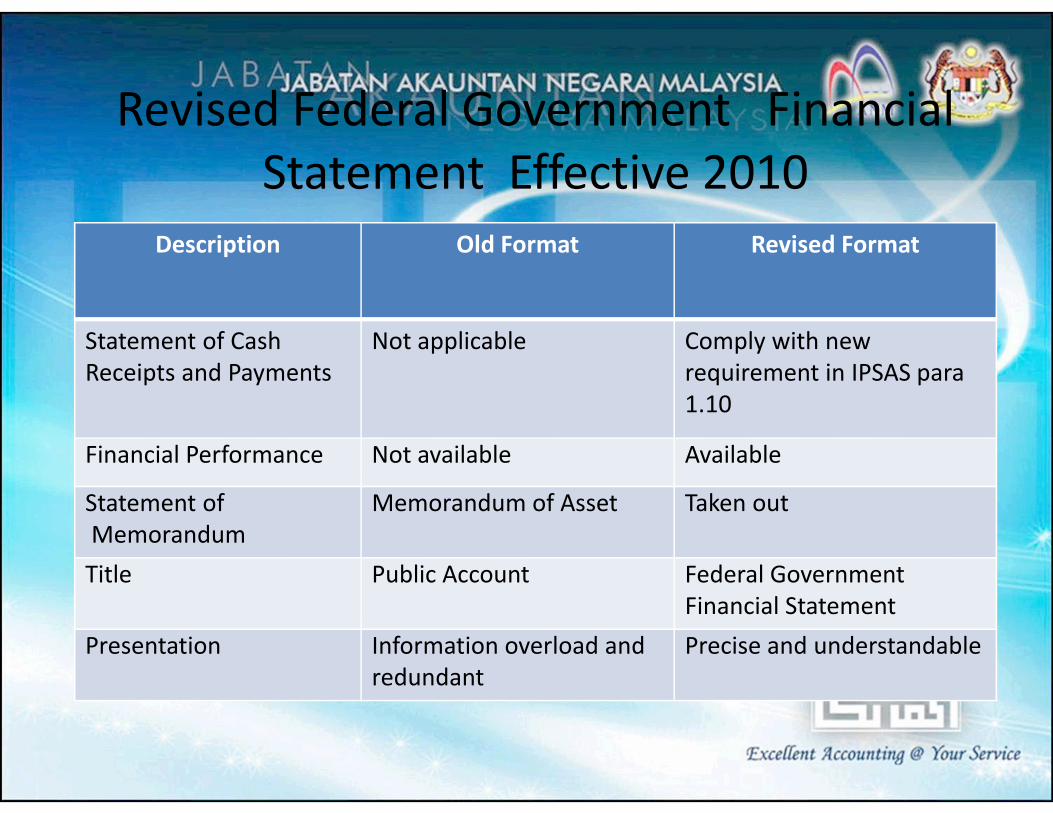

Revised Federal Government Financial

Statement Effective 2010Description Old Format Revised Format

Statement by Secretary

General to the Treasury

and Accountant General

of Malaysia

Not available Available

Financial Statement • Balance Sheet

• Statement of Cash

Receipts and Payments

• Statement of

Memorandum Account

• Notes to the Account

• Statement of Financial

Position

• Statement of Financial

Performance

• Statement of Cash

Receipts and Payments

• Statement of

Memorandum Account

• Notes to the Account

Description Old Format Revised Format

Statement of Cash

Receipts and Payments

Not applicable Comply with new

requirement in IPSAS para

1.10

Financial Performance Not available Available

Statement of

Memorandum

Memorandum of Asset Taken out

Title Public Account Federal Government

Financial Statement

Presentation Information overload and

redundant

Precise and understandable

Revised Federal Government Financial

Statement Effective 2010

Research By IPN And ARI On Local Authority Issues

17

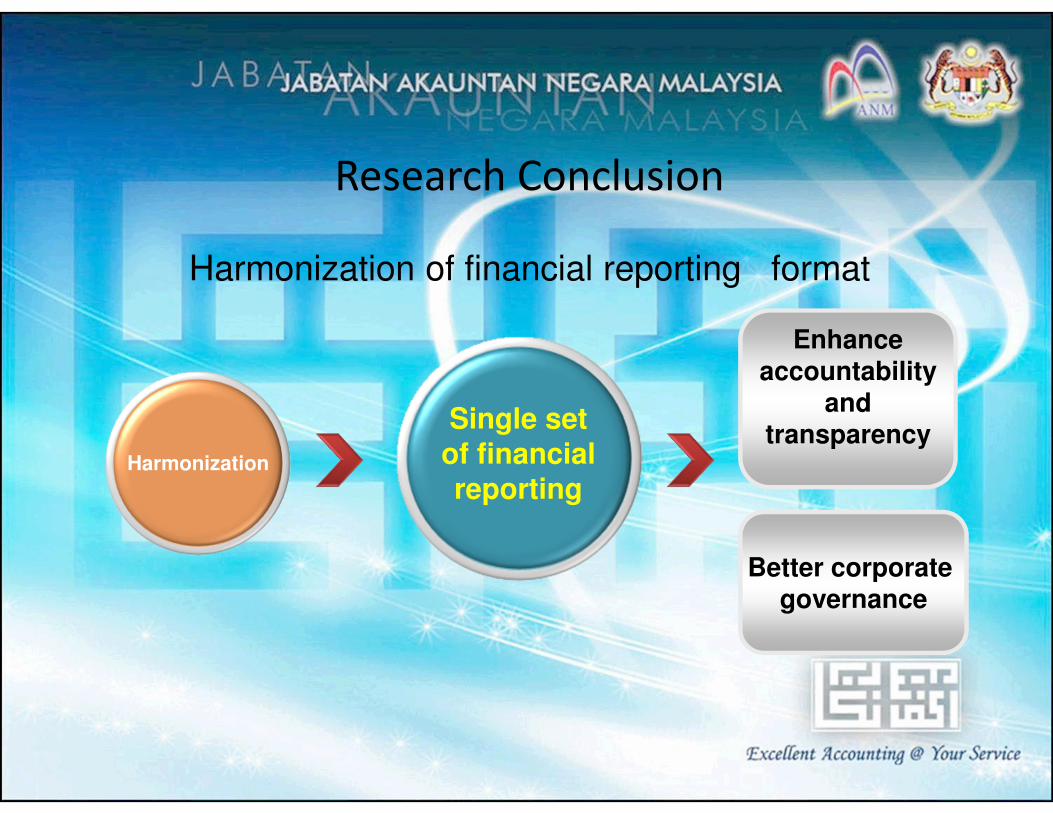

Research Conclusion

Single set

of financial

reportingHarmonization

Harmonization of financial reporting format

Enhance

accountability

and transparency

Better corporate

governance

19

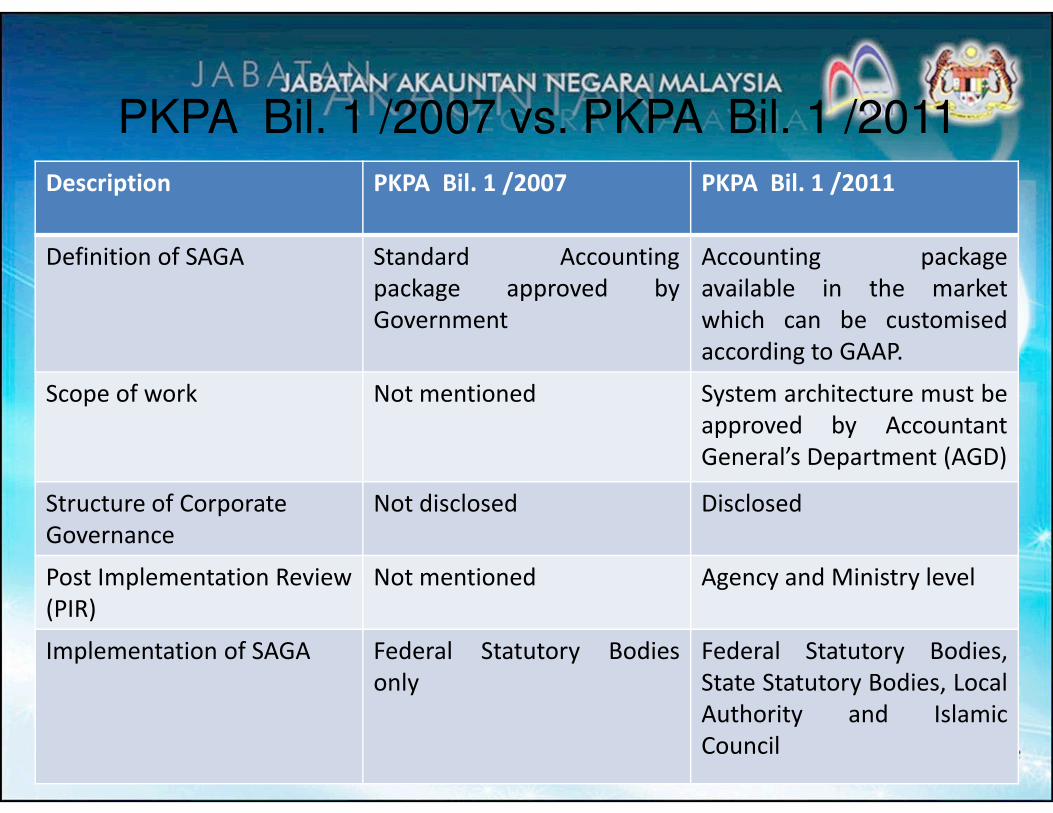

Description PKPA Bil. 1 /2007 PKPA Bil. 1 /2011

Definition of SAGA Standard Accounting

package approved by

Government

Accounting package

available in the market

which can be customised

according to GAAP.

Scope of work Not mentioned System architecture must be

approved by Accountant

General’s Department (AGD)

Structure of Corporate

Governance

Not disclosed Disclosed

Post Implementation Review

(PIR)

Not mentioned Agency and Ministry level

Implementation of SAGA Federal Statutory Bodies

only

Federal Statutory Bodies,

State Statutory Bodies, Local

Authority and Islamic

Council

PKPA Bil. 1 /2007 vs. PKPA Bil. 1 /2011

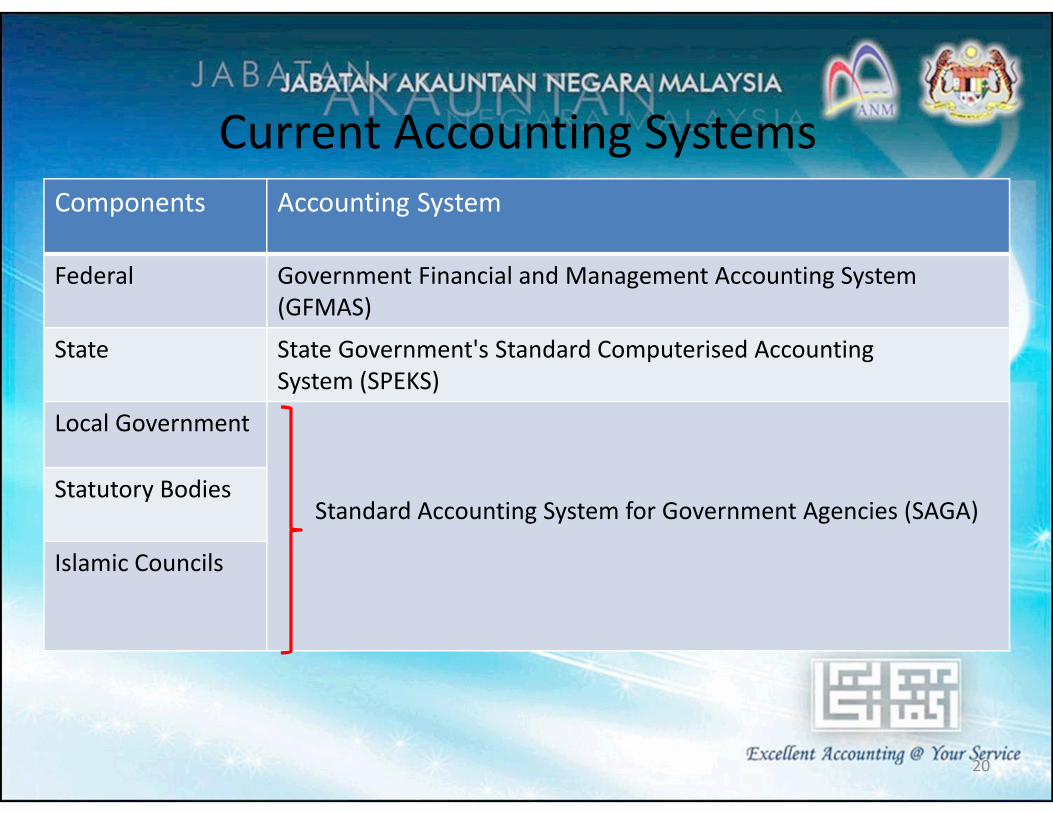

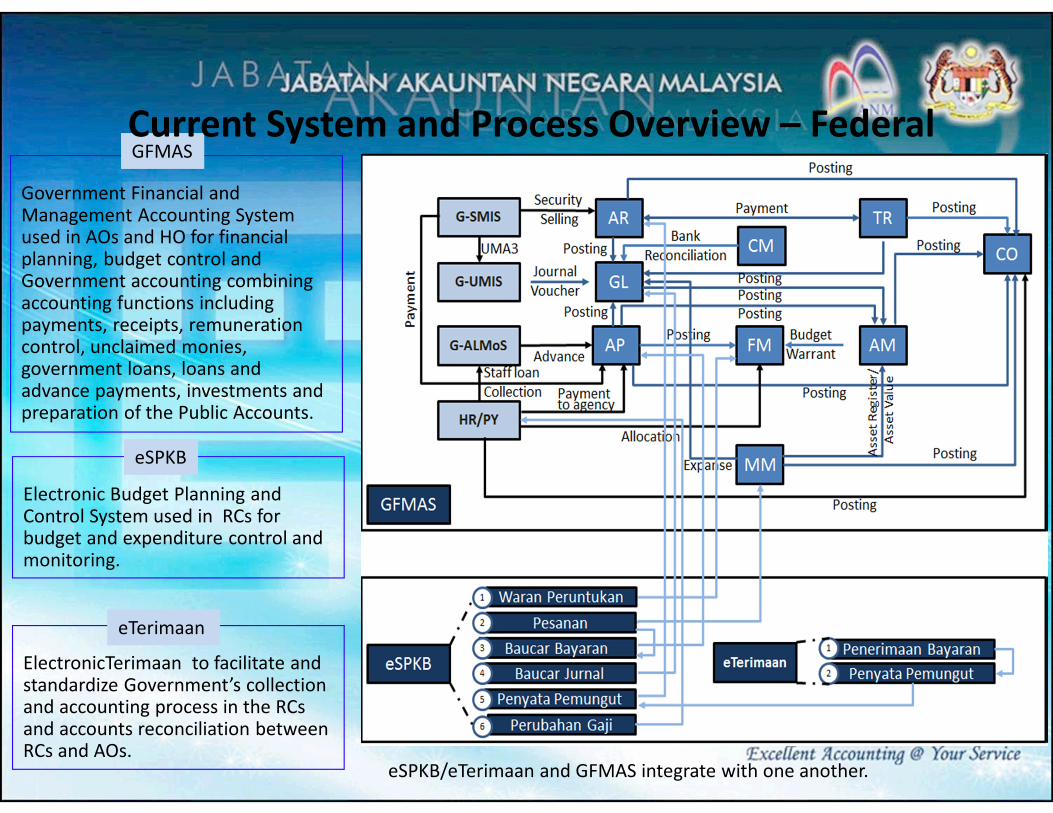

Current Accounting Systems

Components Accounting System

Federal Government Financial and Management Accounting System

(GFMAS)

State State Government's Standard Computerised Accounting

System (SPEKS)

Local Government

Standard Accounting System for Government Agencies (SAGA)Statutory Bodies

Islamic Councils

20

Government Financial and Management Accounting System used in AOs and HO for financial planning, budget control and Government accounting combining accounting functions including payments, receipts, remuneration control, unclaimed monies, government loans, loans and advance payments, investments and preparation of the Public Accounts.

GFMASGFMAS

Electronic Budget Planning and Control System used in RCs for budget and expenditure control and monitoring.

eSPKBeSPKB

ElectronicTerimaan to facilitate and standardize Government’s collection and accounting process in the RCs and accounts reconciliation between RCs and AOs.

eTerimaaneTerimaan

eSPKB/eTerimaan and GFMAS integrate with one another.

Current System and Process Overview – Federal

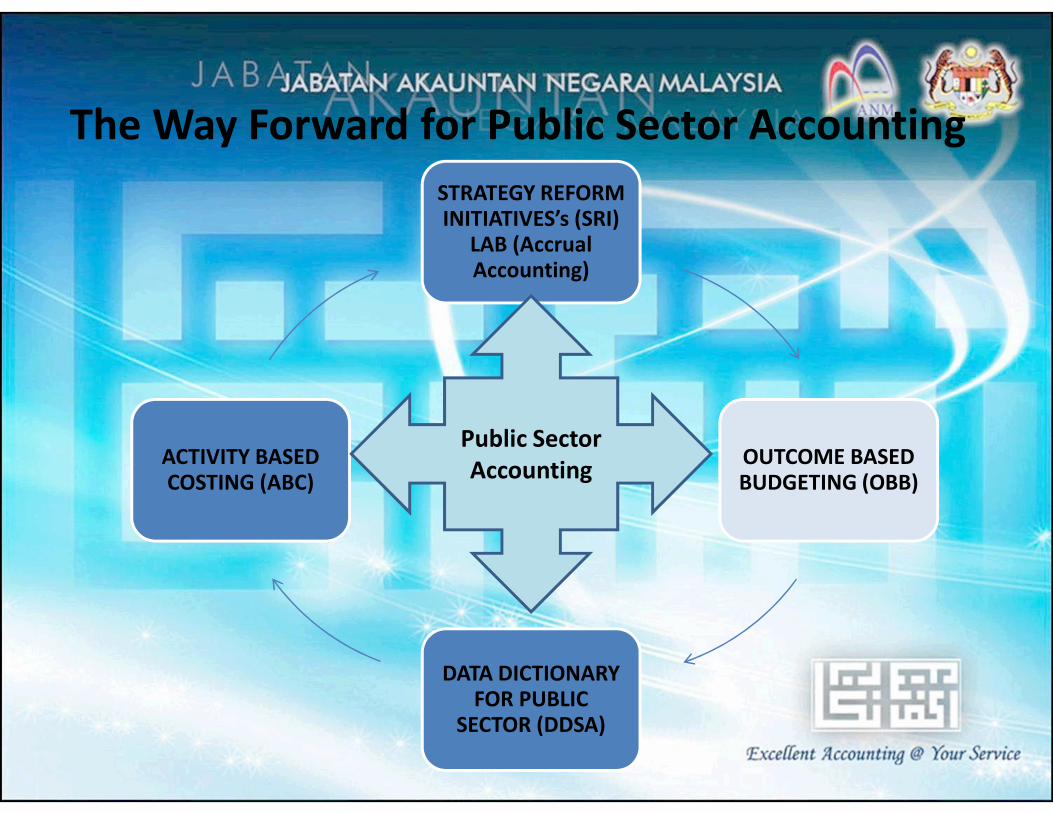

The Way Forward for Public Sector Accounting

STRATEGY REFORM INITIATIVES’s (SRI)

LAB (Accrual Accounting)

OUTCOME BASED BUDGETING (OBB)

DATA DICTIONARY FOR PUBLIC

SECTOR (DDSA)

ACTIVITY BASED COSTING (ABC)

Public Sector

Accounting

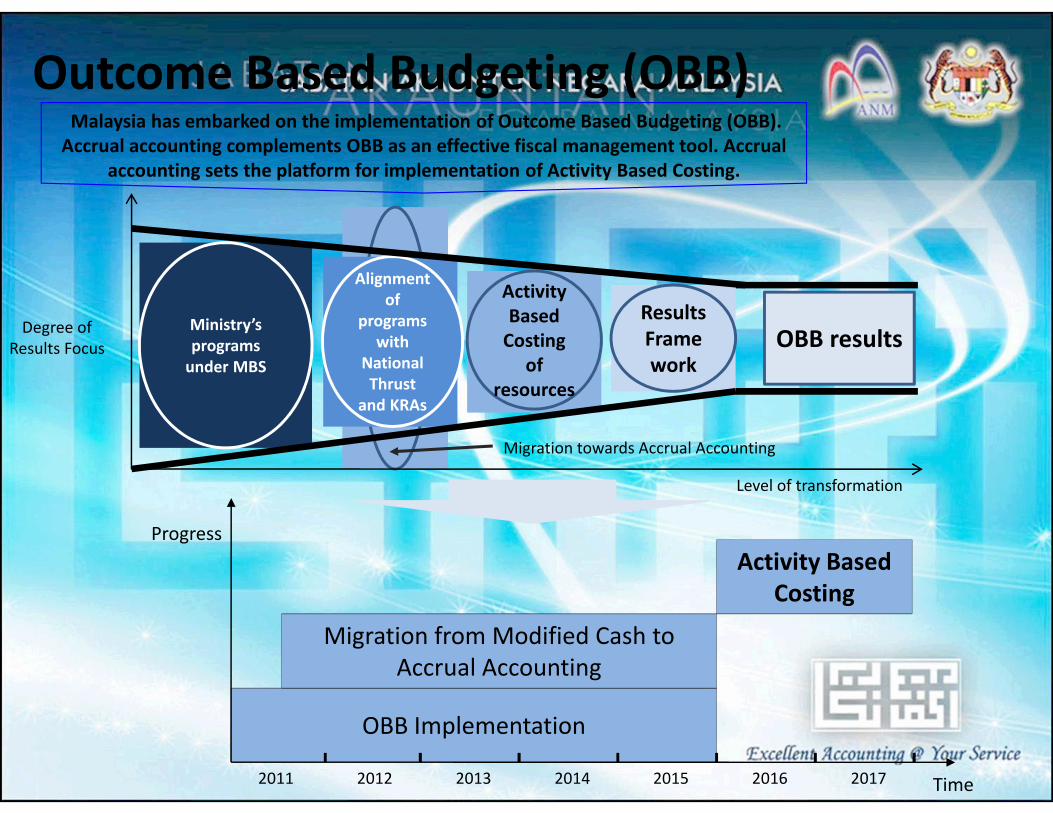

Outcome Based Budgeting (OBB)

Time

Progress

2011 2012 2013 2014 2015 2016 2017

OBB Implementation

Migration from Modified Cash to

Accrual Accounting

Activity Based

Costing

Ministry’s

programs

under MBS

Alignment

of

programs

with

National

Thrust

and KRAs

Activity

Based

Costing

of

resources

Results

Frame

work

OBB results

Migration towards Accrual Accounting

Level of transformation

Degree of

Results Focus

Malaysia has embarked on the implementation of Outcome Based Budgeting (OBB).

Accrual accounting complements OBB as an effective fiscal management tool. Accrual

accounting sets the platform for implementation of Activity Based Costing.

SRI Lab - Accrual Accounting

• Aspiration of the Malaysian Government of

attaining developed nation status with the drive

for “People first, Performance now”.

• Migration to accrual accounting has been

stipulated as a policy measure in the NEM Report.

• The adoption will put the Malaysian public sector

finance practice to be in line with the developed

countries.

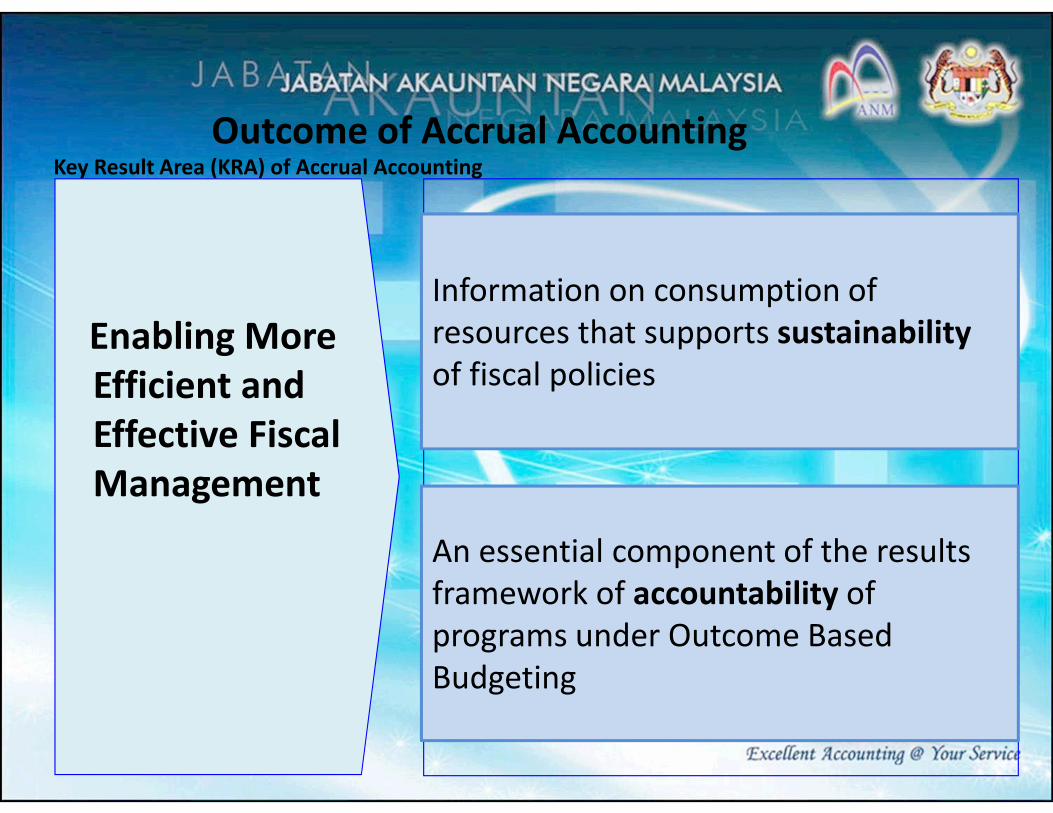

Outcome of Accrual AccountingKey Result Area (KRA) of Accrual Accounting

Enabling More

Efficient and

Effective Fiscal

Management

Information on consumption of

resources that supports sustainability

of fiscal policies

An essential component of the results

framework of accountability of

programs under Outcome Based

Budgeting

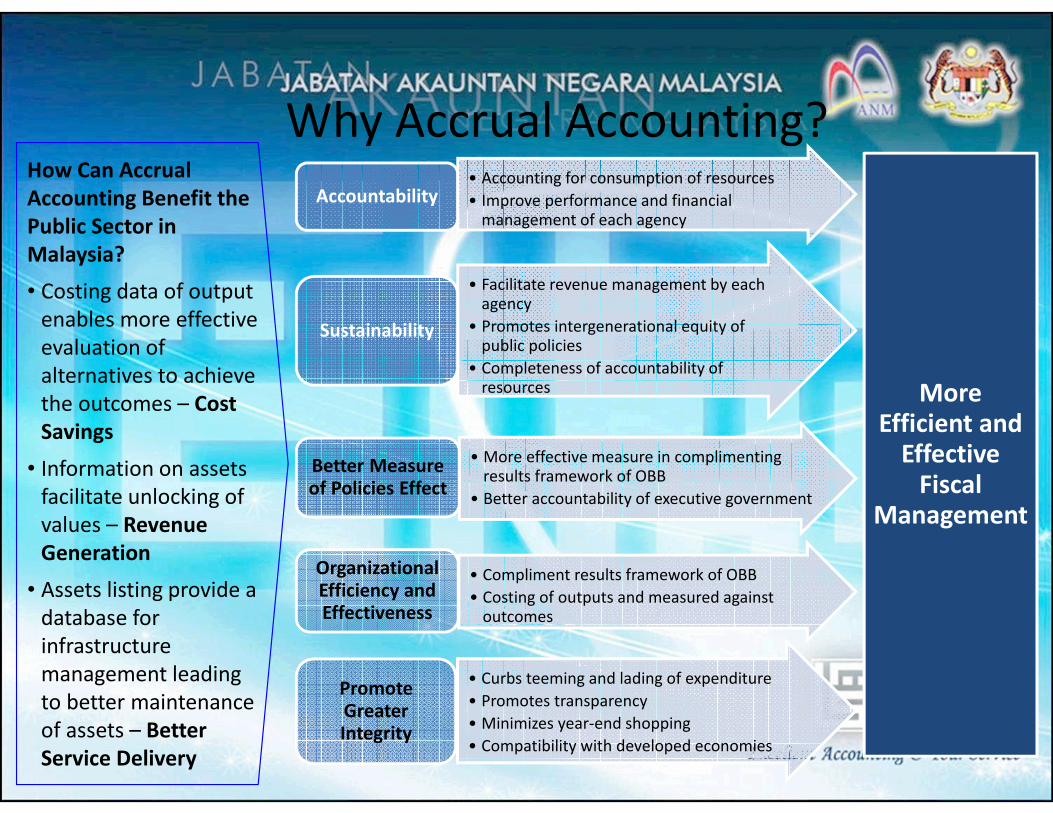

• Accounting for consumption of resources

• Improve performance and financial management of each agency

Accountability

• Facilitate revenue management by each agency

• Promotes intergenerational equity of public policies

• Completeness of accountability of resources

Sustainability

• More effective measure in complimenting results framework of OBB

• Better accountability of executive government

Better Measure of Policies Effect

• Curbs teeming and lading of expenditure

• Promotes transparency

• Minimizes year-end shopping

• Compatibility with developed economies

Promote Greater Integrity

• Compliment results framework of OBB

• Costing of outputs and measured against outcomes

Organizational Efficiency and Effectiveness

More Efficient and

Effective Fiscal

Management

Why Accrual Accounting?How Can Accrual

Accounting Benefit the

Public Sector in

Malaysia?

• Costing data of output

enables more effective

evaluation of

alternatives to achieve

the outcomes – Cost

Savings

• Information on assets

facilitate unlocking of

values – Revenue

Generation

• Assets listing provide a

database for

infrastructure

management leading

to better maintenance

of assets – Better

Service Delivery

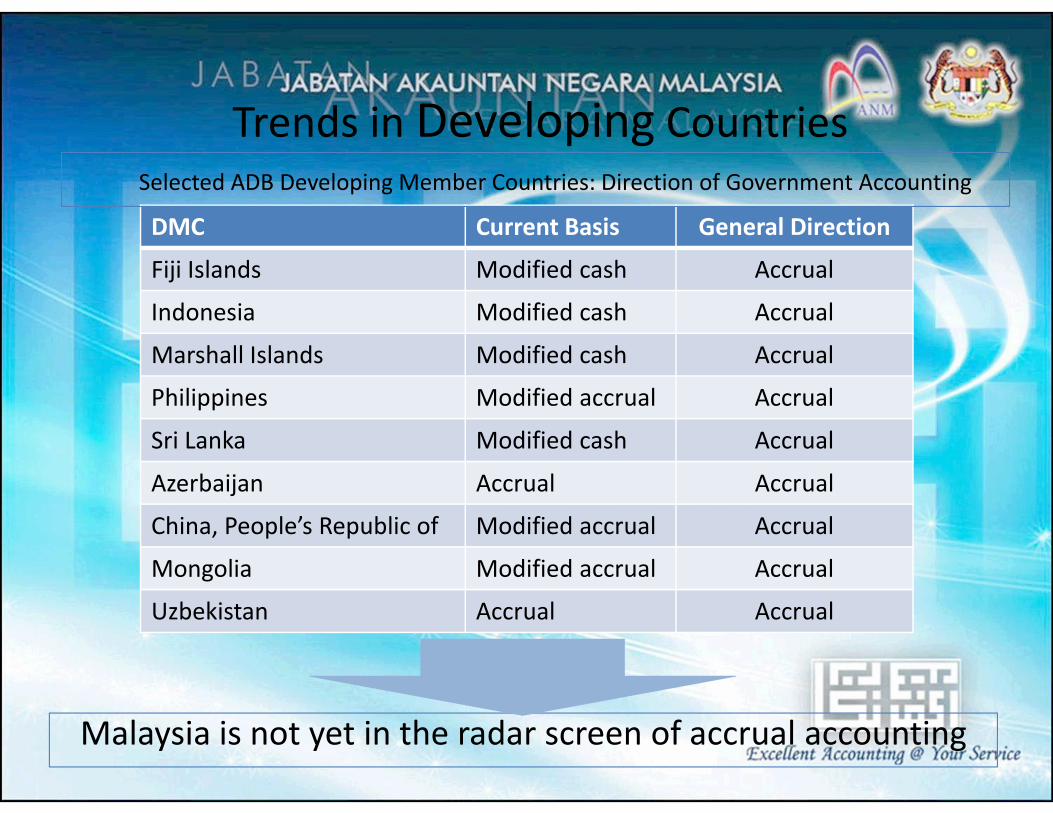

Trends in Developing Countries

DMC Current Basis General Direction

Fiji Islands Modified cash Accrual

Indonesia Modified cash Accrual

Marshall Islands Modified cash Accrual

Philippines Modified accrual Accrual

Sri Lanka Modified cash Accrual

Azerbaijan Accrual Accrual

China, People’s Republic of Modified accrual Accrual

Mongolia Modified accrual Accrual

Uzbekistan Accrual Accrual

Selected ADB Developing Member Countries: Direction of Government Accounting

Malaysia is not yet in the radar screen of accrual accounting

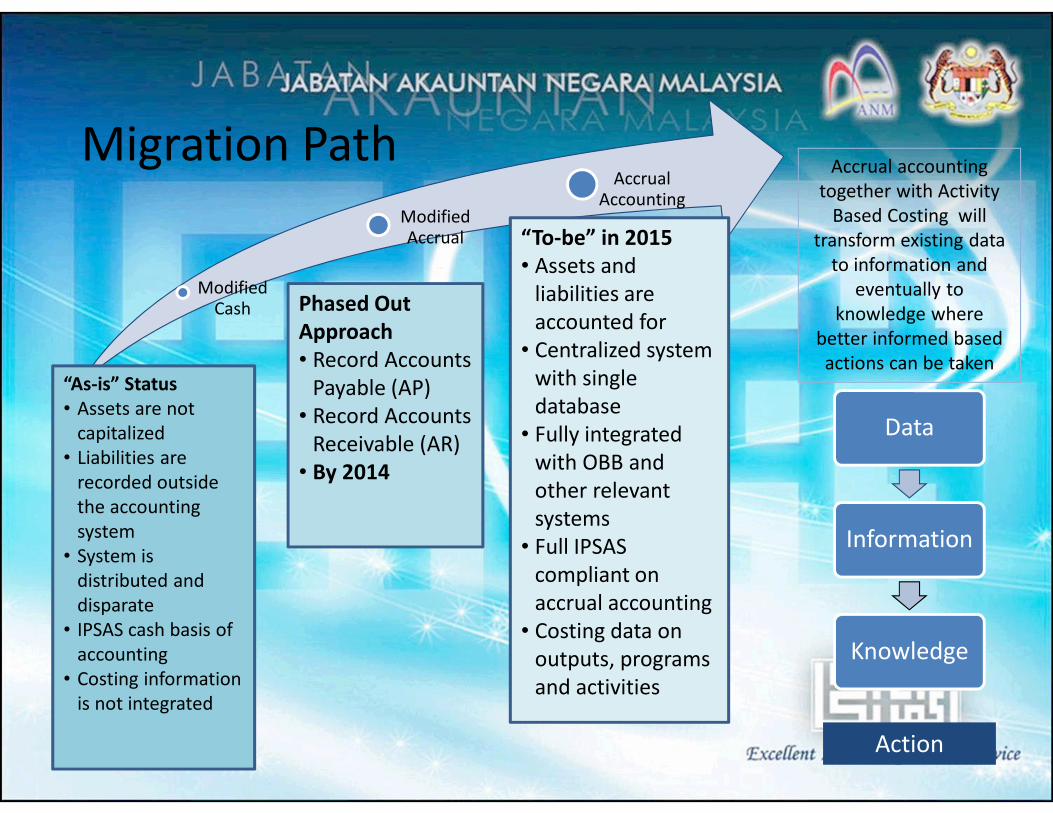

Migration Path

Modified Cash

Modified Accrual

Accrual Accounting

“As-is” Status

• Assets are not

capitalized

• Liabilities are

recorded outside

the accounting

system

• System is

distributed and

disparate

• IPSAS cash basis of

accounting

• Costing information

is not integrated

Phased Out

Approach

• Record Accounts

Payable (AP)

• Record Accounts

Receivable (AR)

• By 2014

“To-be” in 2015

• Assets and

liabilities are

accounted for

• Centralized system

with single

database

• Fully integrated

with OBB and

other relevant

systems

• Full IPSAS

compliant on

accrual accounting

• Costing data on

outputs, programs

and activities

Accrual accounting

together with Activity

Based Costing will

transform existing data

to information and

eventually to

knowledge where

better informed based

actions can be taken

Data

Information

Knowledge

Action

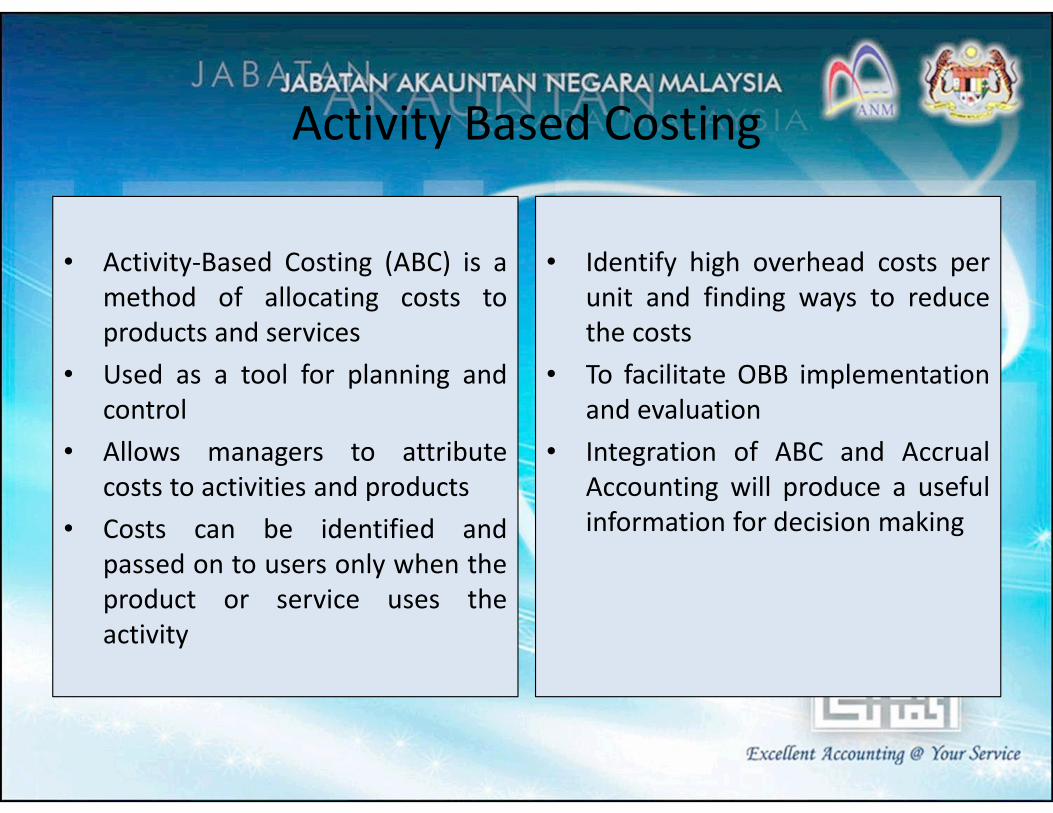

Activity Based Costing

• Activity-Based Costing (ABC) is a

method of allocating costs to

products and services

• Used as a tool for planning and

control

• Allows managers to attribute

costs to activities and products

• Costs can be identified and

passed on to users only when the

product or service uses the

activity

• Identify high overhead costs per

unit and finding ways to reduce

the costs

• To facilitate OBB implementation

and evaluation

• Integration of ABC and Accrual

Accounting will produce a useful

information for decision making

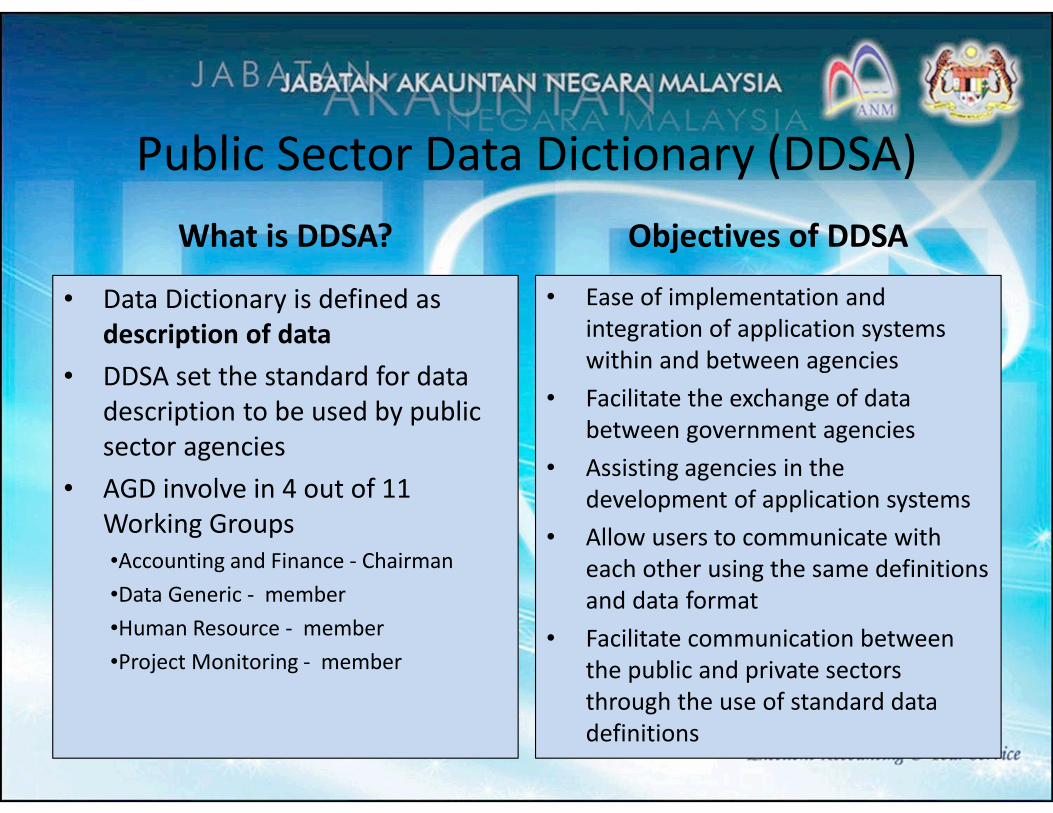

Public Sector Data Dictionary (DDSA)

What is DDSA?

• Data Dictionary is defined as

description of data

• DDSA set the standard for data

description to be used by public

sector agencies

• AGD involve in 4 out of 11

Working Groups

•Accounting and Finance - Chairman

•Data Generic - member

•Human Resource - member

•Project Monitoring - member

Objectives of DDSA

• Ease of implementation and

integration of application systems

within and between agencies

• Facilitate the exchange of data

between government agencies

• Assisting agencies in the

development of application systems

• Allow users to communicate with

each other using the same definitions

and data format

• Facilitate communication between

the public and private sectors

through the use of standard data

definitions

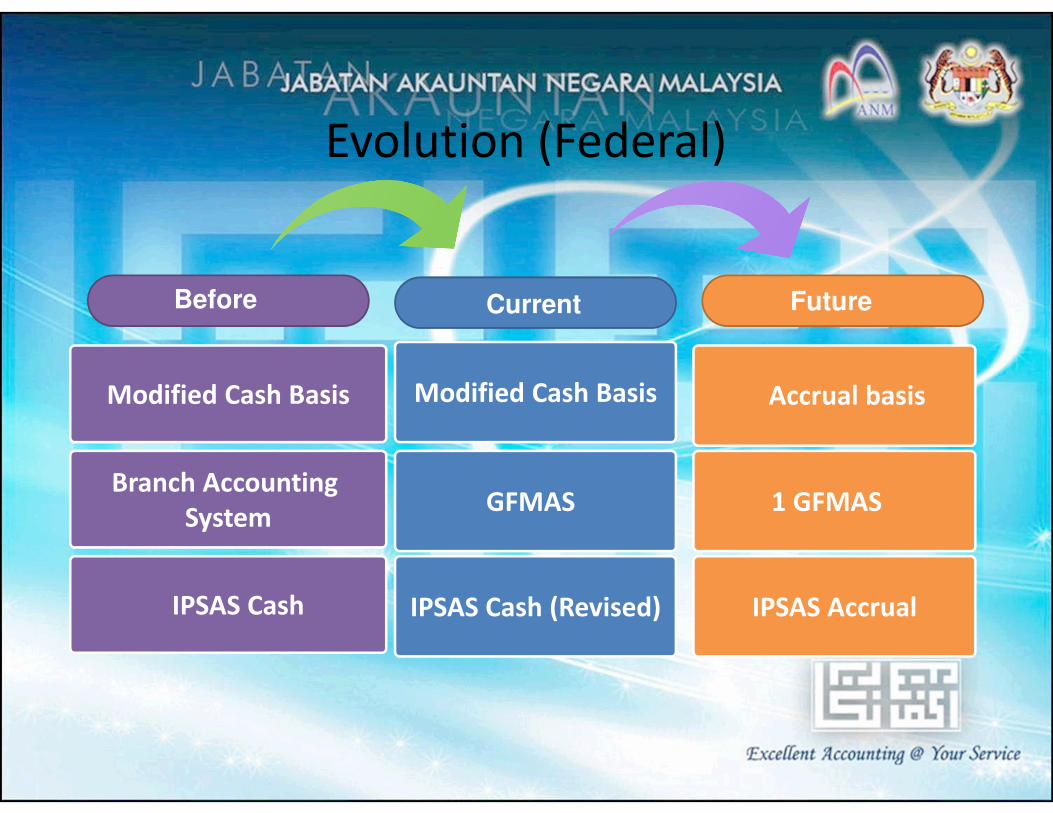

Evolution (Federal)

Modified Cash Basis Modified Cash Basis

Before

Accrual basis

Current Future

Branch Accounting

SystemGFMAS 1 GFMAS

IPSAS AccrualIPSAS Cash (Revised)IPSAS Cash

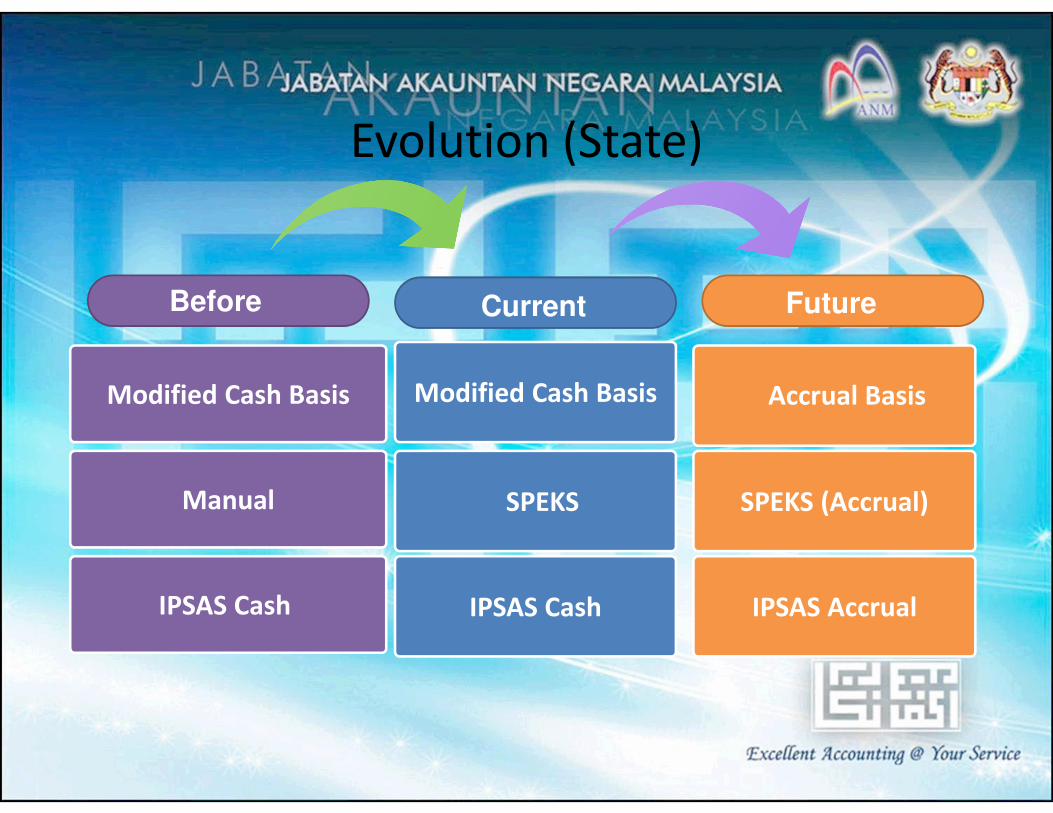

Evolution (State)

Modified Cash Basis Modified Cash Basis

Before

Accrual Basis

Current Future

Manual SPEKS SPEKS (Accrual)

IPSAS AccrualIPSAS CashIPSAS Cash

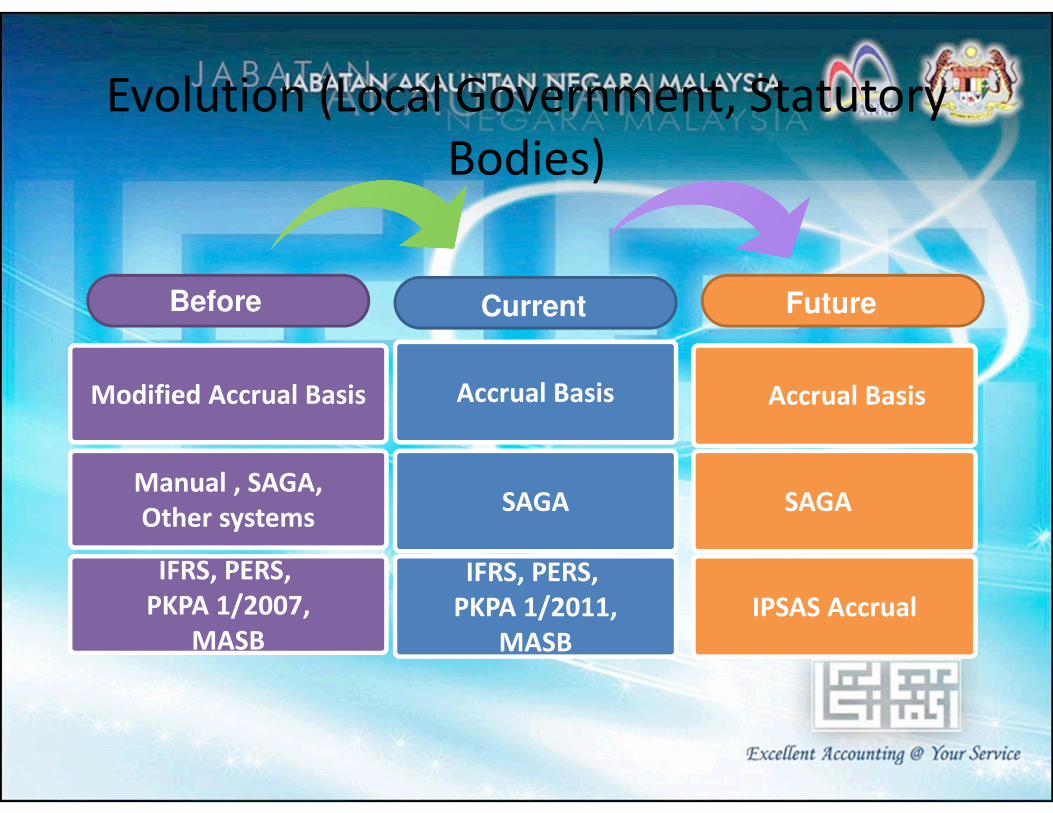

Evolution (Local Government, Statutory

Bodies)

Modified Accrual Basis Accrual Basis

Before

Accrual Basis

Current Future

Manual , SAGA,

Other systemsSAGA SAGA

IPSAS Accrual

IFRS, PERS,

MASB

IFRS, PERS,

PKPA 1/2011,

MASB

IFRS, PERS,

MASB

IFRS, PERS,

PKPA 1/2007,

MASB

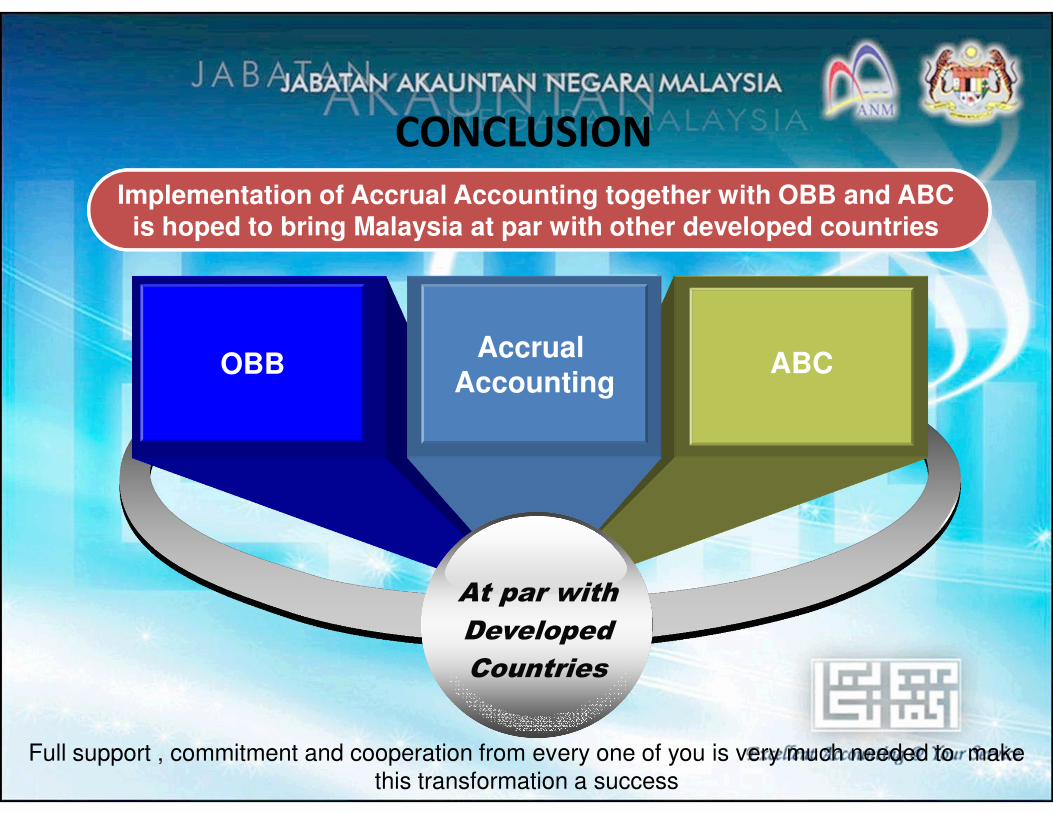

CONCLUSION

Implementation of Accrual Accounting together with OBB and ABC

is hoped to bring Malaysia at par with other developed countries

OBBAccrual

AccountingABC

At par with

Developed

Countries

Full support , commitment and cooperation from every one of you is very much needed to make

this transformation a success

35

Thank You For Your

Attention

Together we make this happen……