hua yang berhad (“hua yang” or the “company”)...

TRANSCRIPT

HUA YANG BERHAD (“HUA YANG” OR THE “COMPANY”) PROPOSED ACQUISITION OF A PIECE OF LEASEHOLD LAND M EASURING APPROXIMATELY 32,740 SQUARE METRES HELD UNDER PN 51166 LOT 80646 IN MUKIM BATU, DAERAH KUALA LUMPUR, STATE OF WILAYAH PERSEKUTUAN KUALA LU MPUR BY PRISMA PELANGI SDN BHD, A WHOLLY-OWNED SUBSIDIARY OF HUA Y ANG, FOR A TOTAL CASH CONSIDERATION OF RM120.0 MILLION ONLY (“PROPOSED AC QUISITION”) 1. INTRODUCTION

On behalf of the Board of Directors of Hua Yang (“Board ”), Kenanga Investment Bank Berhad (“Kenanga IB ”) is pleased to announce that Prisma Pelangi Sdn Bhd (Company No. 228268-A) (“PPSB” or the “Purchaser ”), a wholly-owned subsidiary of Hua Yang, had on 30 January 2015 entered into a conditional sale and purchase agreement (“SPA”) with Nation Holdings Sdn Bhd (Company No. 80501-H) (“Nation Holdings ” or the “Vendor ”) for the acquisition of a piece of leasehold land measuring approximately 32,740 square metres or 352,410 square feet held under PN 51166 Lot 80646 in Mukim Batu, Daerah Kuala Lumpur, State of Wilayah Persekutuan Kuala Lumpur (“Land ”) for a total cash consideration of RM120.0 million only (“Purchase Price ”) (“Proposed Acquisition ”). Further details of the Proposed Acquisition are set out below.

2. DETAILS OF THE PROPOSED ACQUISITION

The Proposed Acquisition involves the acquisition of the Land by PPSB for a total cash consideration of RM120.0 million. Pursuant to the SPA, in consideration of the earnest deposit of RM2.4 million only paid to the Vendor prior to the signing of the SPA (“Earnest Deposit ”) and the balance deposit of RM9.6 million only (“Balance Deposit ”) (the aggregate of the Earnest Deposit and the Balance Deposit shall be known collectively as “Deposit ”) paid to the Vendor upon the execution of the SPA, the Vendor agreed to sell and the Purchaser agreed to purchase the Land on an “as is where is” basis free from all encumbrances and in the state and condition as at the date of the SPA and with vacant possession at the Purchase Price and subject to the terms and conditions as contained in the SPA. Further to the above payments, the Purchaser shall pay the balance of the Purchase Price of RM108.0 million only (“Balance Purchase Price ”) to the Vendor’s solicitors as stakeholders on or before three (3) months from the date all Conditions Precedents (as defined herein) under the SPA are fulfilled (“Payment Due Date ”) with an automatic extension of one (1) month from the Payment Due Date (“Extended Payment Due Date ”) subject to interest at the rate of eight per centum (8%) per annum (“Extension Interest ”) payable by the Purchaser to the Vendor, and the Vendor shall deliver vacant possession of the Land following the full payment of the same (“Completion Date ”). The Balance Purchase Price shall be released to the Vendor upon the expiry of fourteen (14) days from the presentation of the Transfer (as defined herein) or upon registration thereof, whichever is earlier, subject to the Vendor having delivered vacant possession of the Land.

2.1 Details of the Land

Descriptions of the Land are set out below: Location : PN 51166 Lot 80646 in Mukim Batu, Daerah Kuala Lumpur, State

of Wilayah Persekutuan Kuala Lumpur Size : Approximately 32,740 square metres (352,410 square feet) Tenure : Leasehold land with a tenure of 99 years expiring on 24 May 2111

Description : The Land is generally flat and earmarked as commercial zone. Category of Land use : “Bangunan” Registered proprietor : Nation Holdings

Existing and proposed development

: The Land is currently vacant. Following the completion of the Proposed Acquisition, the Land will be developed by PPSB.

Net book value : Not available(1) Express Condition : “Tanah ini hendaklah digunakan untuk bangunan perdagangan

bagi tujuan kedai pejabat sahaja.” Restriction in interest : “Tanah ini tidak boleh dipindahmilik, dipajak, dicagar atau digadai

tanpa kebenaran Jawatankuasa Kerja Tanah Wilayah Persekutuan Kuala Lumpur.”

Encumbrances : The Land is charged to Ambank (M) Berhad (“Existing Chargee ”)

vide Presentation Nos. 39949/2013 and 49223/2013(2)

Notes:

(1) The Purchaser is not privy to such information which belongs to the Vendor.

(2) The Land is to be purchased free from all encumbrances. Pursuant to the terms of the SPA, the Vendor undertakes to cause the Existing Chargee to deliver the discharge documents to the Purchaser’s solicitors.

The Proposed Acquisition is subject to the terms and conditions of the SPA, the salient terms of which are set out in Section 2.2 of this announcement.

2.2 Salient terms and conditions of the SPA

The salient terms and conditions of the SPA include, amongst others, the following: (a) Conditions precedent

The SPA is conditional upon and subject to the fulfilment of the following conditions precedent on or before the date falling four (4) months and ten (10) Business Days* from the date of the SPA with extension to be mutually agreed between the Vendor and the Purchaser (“Conditions Precedent Fulfilment Due Date ”): (i) The Vendor having obtained, at their own costs and expenses, the following:

(aa) the consent of the Wilayah Persekutuan Kuala Lumpur State

Authority to transfer the Land to the Purchaser due to the restriction in interest contained in the document of title (“State Approval To Transfer ”);

(bb) the approval from the appropriate authorities for the development

order zoned for commercial with a plot ratio of 1:5 for development of the Land (“DO”) in accordance with the approval in principle of the Dewan Bandaraya Kuala Lumpur (“DBKL ”) as per its letter dated 13 June 2014, and which shall include the approval of DBKL for the Kuala Lumpur Middle Ring Road 2 (“MRR2”) Access (“DO Approval ”); and

(cc) the approval of Jabatan Kerja Raya for access, ingress and egress, to and from the MRR2 from and to the Land (“MRR2 Access ”) upon terms satisfactory to the Purchaser (“MRR2 Approval ”).

(collectively known as “Vendor’s Approvals ”) (ii) The Purchaser having obtained, at their own costs and expenses, the

approval of the shareholders of Hua Yang for the acquisition of the Land subject to the terms and conditions of the SPA (“Hua Yang’s Shareholders Approval ”).

* any day excluding Saturdays, Sundays and public holidays on which financial

institutions licensed under the Financial Services Act 2013 are open for business in Kuala Lumpur and Selangor (“Business Day”)

(b) Vendor’s fulfilment of Conditions Precedent

The Vendor shall at its own costs and expenses apply for the Vendor’s Approvals within ten (10) Business Days from the date of the SPA and shall execute all forms, instruments and documents and do all such acts and things as required to obtain the Vendor’s Approvals on or before the Conditions Precedent Fulfilment Due Date provided that the Purchaser shall provide the information and execute the form(s)/document(s) required to be submitted with the Vendor’s application for the State Approval To Transfer. The Vendor shall pay all costs, expenses, levies, premiums, fees, charges and all other payments payable, imposed and incurred pertaining to the obtaining of the Vendor’s Approvals.

(c) Purchaser’s fulfilment of Conditions Precedent

The Purchaser shall at its own costs and expenses use its reasonable endeavour procure Hua Yang to issue its shareholders circular and convene a shareholders’ meeting for the purpose of obtaining its shareholders’ approval prior to the Conditions Precedent Fulfilment Date.

(d) Appeal

(i) If any of the Vendor’s Approvals is granted but with conditions which materially and adversely affect a party (“Affected Party ”) imposed with the Vendor’s Approvals (“Adverse Condition” ), the Affected Party shall be entitled to within fourteen (14) days of its receipt of notification in writing of the Vendor’s Approvals by notice in writing to the other party:

(aa) request the Vendor (in the case where the Affected Party is the

Purchaser) to appeal or where the Affected Party is the Vendor, the Vendor shall be entitled to appeal against the imposition of the Adverse Condition by the appropriate authorities and the Vendor shall within fourteen (14) days upon the receipt or issuance of the notice, as the case may be, submit an appeal to the appropriate authorities (“Condition Appeal ”); or

(bb) accept the Adverse Condition in which event the Condition Precedent

shall be deemed to have been fulfilled,

and in the event that the Purchaser or the Vendor shall fail to give any notice within the aforesaid fourteen (14) days’ period, the Purchaser or the Vendor shall be deemed to have accepted the Adverse Condition, in which event the Condition Precedent shall be deemed to have been fulfilled.

(ii) The Purchaser shall not be entitled to deem any conditions imposed by the

appropriate authorities as an Adverse Condition unless the same shall materially and adversely affect:

(aa) the plot ratio of 1:5 for development of the Land based on the area of the Land stated in the document of title; or

(bb) the MRR2 Access.

(iii) The Vendor shall not be entitled to deem any conditions imposed by the

appropriate authorities as an Adverse Condition save and except if the charges (including the Improvement Service Funds) imposed by DBKL in granting the DO Approval exceeds the amount stipulated in the SPA.

(iv) If any of the Vendor’s Approvals is rejected by the appropriate authorities

before the Conditions Precedent Fulfilment Due Date the Vendor shall within fourteen (14) days of its receipt of the rejection, appeal against the rejection to the appropriate authorities (“Rejection Appeal ”), with a copy of the appeal letter forwarded to the Purchaser.

(v) If the Condition Appeal shall be rejected by the appropriate authorities, the

Affected Party shall within fourteen (14) days of its receipt of the reply by written notice to the Purchaser, appeal again or as the case may be, request for appeal again against the imposition of the Adverse Condition, if permissible, or the Affected Party shall be entitled to, within fourteen (14) days of its receipt of the reply, elect to accept the Adverse Condition, in which event the Condition Precedent shall be deemed to have been fulfilled, or to reject the Adverse Condition, in which event the relevant Vendor’s Approval shall be deemed not granted.

(vi) If the appropriate authorities fails to notify the Vendor of its decision whether

to grant the Vendor’s Approval or regarding the Rejection Appeal or the Condition Appeal, or the Rejection Appeal is rejected by the appropriate authorities, on or before the Conditions Precedent Fulfilment Due Date, then the Vendor’s Approval is deemed to be not obtained.

(e) Non-fulfilment of the Conditions Precedent

(i) If any of the Conditions Precedent are not fulfilled by the Conditions

Precedent Fulfilment Due Date, either the Vendor or the Purchaser shall have the option, at its discretion, by notice in writing to the other party to terminate the SPA.

(ii) Upon termination of the SPA, the Vendor shall within fourteen (14) days upon

receipt of the written notice of termination refund to the Purchaser the Deposit, in exchange for the returning to the Vendor of the Transfer Documents (as defined herein) and thereafter all obligations and liabilities of the parties under the SPA shall cease to have effect and, none of the parties shall have any claim against the other for costs, damages, compensation or otherwise save for any antecedent breaches.

(f) Memorandum of Transfer and Documents

Simultaneously with the execution of the SPA, the Vendor shall deliver or cause to be delivered the following documents (collectively, the “Transfer Documents ”) to the Purchaser’s solicitors:

i) a valid and registrable Memorandum of Transfer in Form 14A of the National

Land Code, 1965 in respect of the Land duly executed by the Vendor in favour of the Purchaser ("Transfer ");

ii) a certified true copy of the document of title;

iii) certified true copy of the quit rent receipt to the Land for year 2014 (if the quit rent bill for year 2015 has not been issued by the appropriate authorities) and certified true copy of the quit rent receipt to the Land for year 2015 shall be furnished to the Purchaser’s solicitors as and when they are available and in any event no later than two (2) months from the execution of the SPA;

iv) the Vendors’ income tax file reference number and the branch where the tax

file is located at; and

v) any other document or documents which are necessary to enable the Transfer to be registered at the relevant land office or registry.

(g) Redemption of the Land

(i) The Vendor shall cause the Existing Chargee to deliver the redemption

statement cum undertaking to the Purchaser’s solicitors within ten (10) Business Days of a written request being made to the Vendor for the same.

(ii) If the redemption amount exceeds the Balance Purchase Price, the Vendor

shall within five (5) Business Days of receipt of a written request from the Vendor's solicitors or the Purchaser’s solicitors, deposit the difference between the redemption amount and the Balance Purchase Price ("Shortfall ") with the Vendor’s solicitors and the Vendor’s solicitors are hereby authorized to forthwith pay the Shortfall to the Existing Chargee to redeem the Land from the Existing Chargee and inform the Purchaser’s solicitors of the same.

(iii) The Vendor undertakes to cause the Existing Chargee to deliver the

discharge documents to the Purchaser’s solicitors within ten (10) Business Days from the date of receipt of the redemption amount by the Existing Chargee.

(iv) The whole or such portion of the Balance Purchase Price shall be utilised to

pay to the Existing Chargee the redemption amount in order to redeem the Land and to obtain the discharge documents.

(v) If there is a delay for any reason by the Vendor, the Vendor’s solicitors or the

Existing Chargee, as the case may be, in delivering or releasing the redemption statement cum undertaking, the Shortfall or the discharge documents, the Payment Due Date shall be deemed extended free of interest by a period of time corresponding to the aforesaid delay until the relevant documents are received by the person who requested for the same.

(h) Events of default

(i) Default by the Vendor

In the event that:

• the Vendor shall fail neglect and/or refuse to sell and/or transfer the Land to the Purchaser in accordance with the SPA; or

• the Vendor shall be in breach in any material respect of any of the

covenants, undertakings, terms, conditions or provisions of the SPA which is not capable of remedy, or capable of remedy but is not remedied within thirty (30) days from receipt of written notice by the Purchaser; or

• the Vendor shall become insolvent, or any petition for winding up has been filed against the Vendor and such petition has not been stayed or set aside within sixty (60) days from receipt of written notice by the Purchaser,

the Purchaser shall be entitled:

• to the remedy of specific performance against the Vendor and to all

reliefs flowing therefrom at the costs and expenses of the Vendor; or • to, by notice in writing to the Vendor terminate the SPA and upon such

termination, the Vendor shall refund and/or pay all monies or consideration paid or provided by the Purchaser or its financier towards the Purchase Price (including the Deposit) within fourteen (14) days from the date of the Purchaser’s termination notice, and the Vendor shall pay a further sum equivalent to the Deposit to the Purchaser as agreed liquidated damages whereupon the Purchaser shall, simultaneous with the abovementioned refund:

� re-deliver vacant possession of the Land to the Vendor (if same

has been delivered to the Purchaser) in substantially the same state and condition as it was delivered to the Purchaser (fair wear and tear excepted);

� remove the Purchaser’s and/or its financier’s caveat and any

encumbrances over the Land attributable to the Purchaser or its financier at the sole cost and expense of the Purchaser;

� return to the Vendor or the Vendor’s solicitors the Transfer

documents (provided that the Purchaser shall be entitled to retain the Transfer for refund of the stamp duty paid to and only return the same upon receipt of the said refund) and the discharge documents forwarded to the Purchaser or its financier (if any),

and thereafter the SPA shall become null and void and of no further effect and the Parties shall have no further claims against the other in respect of or arising out of the SPA and the Vendor shall be at liberty to deal with the Land as the Vendor deems fit.

(i) Default by the Purchaser

In the event that:

• the Purchaser shall fail to make the payment of the Balance Purchase Price or any part thereof on or before the Payment Due Date or Extended Payment Due Date, or the Extension Interest (if any) within three (3) Business Days; or

• the Purchaser shall be in breach in any material respect of any of the

covenants, undertakings, terms, conditions or provisions of the SPA which is not capable of remedy, or capable of remedy but is not remedied within thirty (30) days from receipt of written notice by the Vendor; or

• the Purchaser shall become insolvent,

the Vendor shall be entitled to terminate the SPA by notice in writing to the Purchaser and upon such termination, the Deposit shall be forfeited to the Vendor as agreed liquidated damages, and all other monies paid by the Purchaser or its financier towards account of the Purchase Price shall be refunded within fourteen (14) days from the date of the Vendor’s termination notice to the Purchaser or its financier (as the case may be) whereupon the Purchaser shall, simultaneous with the abovementioned refund:

• re-deliver vacant possession of the Land to the Vendor (if the same

has been delivered to the Purchaser) in substantially the same state and condition as it was delivered to the Purchaser (fair wear and tear excepted);

• remove the Purchaser’s and/or its financier’s caveat and any

encumbrances over the Land attributable to the Purchaser at the sole cost and expense of the Purchaser;

• return to the Vendor or the Vendor’s solicitors the Transfer

documents (provided that the Purchaser shall be entitled to retain the Transfer for refund of the stamp duty paid to and only return the same upon receipt of the said refund) and the discharge documents forwarded to the Purchaser or its financier,

and thereafter the SPA shall become null and void and be of no further effect and the Vendor and Purchaser shall have no further claims against the other in respect of or arising out of the SPA and the Vendor shall be at liberty to deal with the Land as the Vendor deems fit.

(i) Delivery of vacant possession

Vacant possession of the Land shall be deemed delivered to the Purchaser on the Completion Date.

2.3 Proposed Development of the Land

Based on preliminary plans, the proposed development of the Land shall comprise of four (4) blocks of serviced apartments and two (2) levels of retail lots (“Proposed Development ”). Currently, the Vendor will be obtaining a planning approval from DBKL for a high-rise mixed commercial development. Upon completion of the Proposed Acquisition, the Group intends to amend the development component to meet the Company’s market segment. Therefore, it is too preliminary at this stage to ascertain the total development cost and the expected profits to be derived from the Proposed Development. The Proposed Development is estimated to have a potential gross development value (“GDV”) of approximately RM800.0 million. Subject to the conditions precedent being fulfilled, the Proposed Development is expected to commence in the fourth (4th) quarter of 2016.

The Proposed Development is expected to be developed over a span of between five (5) to seven (7) years.

2.4 Basis and justification of the Purchase Price

The Purchase Price for the Land was arrived at based on a willing buyer-willing seller basis after taking into consideration the indicative market value of the Land by an independent firm registered with the Board of Valuers, Appraisers & Estate Agents Malaysia, Henry Butcher Malaysia Sdn Bhd (“Henry Butcher ” or the “Valuer ”) and the development potential of the Land.

The Valuer had determined the indicative market value of the Land to be RM121.0 million as set out in the indicative valuation letter from the Vendor to the Company dated 29 January 2015. As such, the Purchase Price represents a discount of approximately 0.83% or RM1.0 million to the market value of the Land.

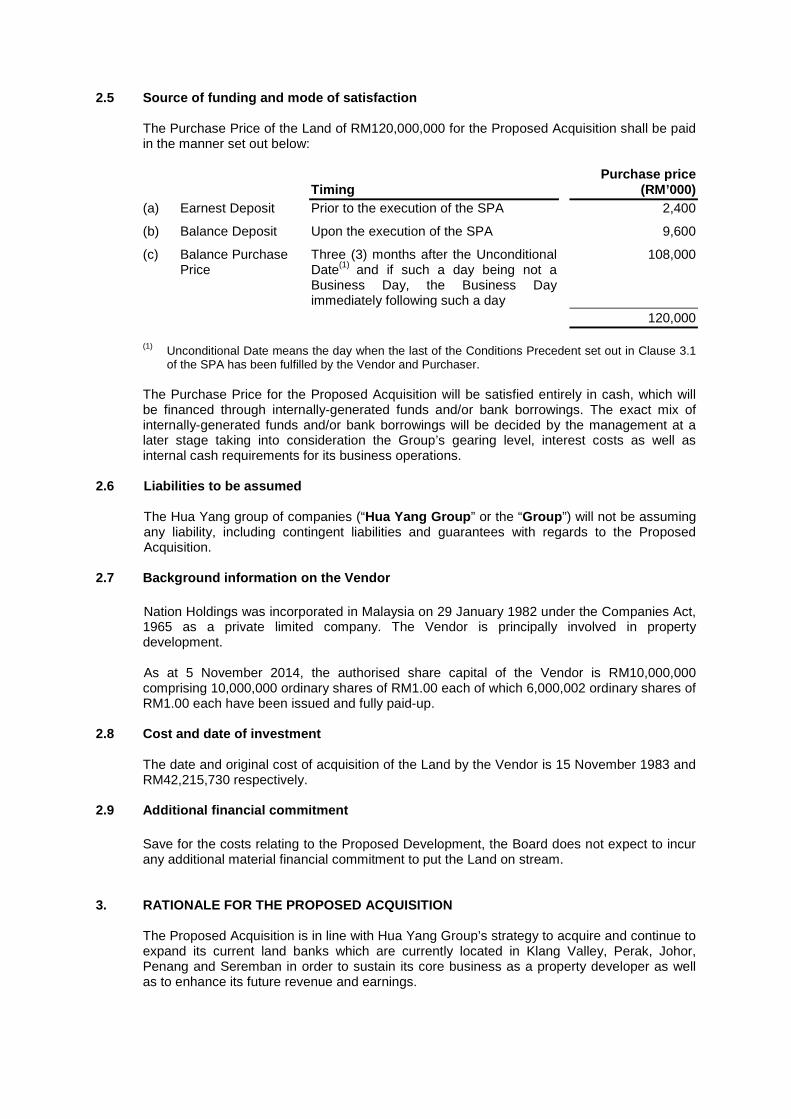

2.5 Source of funding and mode of satisfaction

The Purchase Price of the Land of RM120,000,000 for the Proposed Acquisition shall be paid in the manner set out below:

Timing Purchase price

(RM’000) (a) Earnest Deposit Prior to the execution of the SPA 2,400

(b) Balance Deposit Upon the execution of the SPA 9,600

(c) Balance Purchase Price

Three (3) months after the Unconditional Date(1) and if such a day being not a Business Day, the Business Day immediately following such a day

108,000

120,000 (1) Unconditional Date means the day when the last of the Conditions Precedent set out in Clause 3.1

of the SPA has been fulfilled by the Vendor and Purchaser. The Purchase Price for the Proposed Acquisition will be satisfied entirely in cash, which will be financed through internally-generated funds and/or bank borrowings. The exact mix of internally-generated funds and/or bank borrowings will be decided by the management at a later stage taking into consideration the Group’s gearing level, interest costs as well as internal cash requirements for its business operations.

2.6 Liabilities to be assumed The Hua Yang group of companies (“Hua Yang Group ” or the “Group ”) will not be assuming any liability, including contingent liabilities and guarantees with regards to the Proposed Acquisition.

2.7 Background information on the Vendor

Nation Holdings was incorporated in Malaysia on 29 January 1982 under the Companies Act, 1965 as a private limited company. The Vendor is principally involved in property development. As at 5 November 2014, the authorised share capital of the Vendor is RM10,000,000 comprising 10,000,000 ordinary shares of RM1.00 each of which 6,000,002 ordinary shares of RM1.00 each have been issued and fully paid-up.

2.8 Cost and date of investment

The date and original cost of acquisition of the Land by the Vendor is 15 November 1983 and RM42,215,730 respectively.

2.9 Additional financial commitment

Save for the costs relating to the Proposed Development, the Board does not expect to incur any additional material financial commitment to put the Land on stream.

3. RATIONALE FOR THE PROPOSED ACQUISITION

The Proposed Acquisition is in line with Hua Yang Group’s strategy to acquire and continue to expand its current land banks which are currently located in Klang Valley, Perak, Johor, Penang and Seremban in order to sustain its core business as a property developer as well as to enhance its future revenue and earnings.

The Land will be developed for sale to meet the increasing demand for affordable priced properties while maintaining the modern and city lifestyle concept to attract the younger generation of the surrounding residential areas of Selayang, Kepong and Gombak due to population growth in these areas. The development will be centered on building vertical communities in the form of serviced apartments. The Proposed Development (as elaborated in Section 2.3) is expected to contribute positively to the Group’s future revenue stream and profitability.

4. PROSPECTS OF THE PROPOSED ACQUISITION 4.1 Overview and Outlook of the Malaysian economy

Growth of the Malaysian economy accelerated to 6.4% in the second (2nd) quarter of 2014 from 6.2% in the first (1st) quarter, thus bringing the first half growth to 6.3%. Growth was supported by resilient domestic demand and reinforced by higher exports. The faster pace of recovery, particularly in the United States, United Kingdom and selected euro area economies as well as moderate growth in the emerging economies provided strong support to the Malaysian export-oriented industries and trade-related services. Meanwhile, the Malaysian economy has benefited from several initiatives and reforms taken over the years to enhance its resilience and competitiveness. Consequently, Malaysia is now well placed to gain further from the gradual global recovery with a more broad-based growth. The economic growth momentum in 2014 is expected to continue in 2015 with a projected growth of 5% to 6% driven by improving external demand and resilient domestic economic activity. (Source: Economic Report 2014/2015, Ministry of Finance Malaysia) The Malaysian economy registered a growth of 5.6% in the third (3rd) quarter of 2014 (2Q 2014: 6.5%), supported by private sector demand and continued positive growth in net exports of goods and services. On the supply side, growth in the major economic sectors was sustained, supported by trade and domestic activities. On a quarter-on-quarter seasonally adjusted basis, the economy grew by 0.9% (2Q 2014: 1.9%). (Source: Economic and Financial Developments in Malaysia in the Third Quarter of 2014, Bank Negara Malaysia)

4.2 Overview and Outlook of the Malaysian Property Market

Growth in the non-residential subsector turned around sharply by 14% (January – June 2013: -1%) in line with healthy business activities during the first half of 2014. This was reflected by increased construction activities especially for commercial buildings with the incoming supply of shops increasing to 72,117 units (January – June 2013: 66,167 units). Meanwhile, construction starts for purpose-built offices (“PBO”) decreased substantially to 2,965 square metres (January – June 2013: 263,284 square metres), after experiencing a strong growth of 61.2% in PBO starts in 2013. However, the national occupancy rate of office buildings remained stable at 83.4% (end-June 2013: 82%) despite an additional 194,798 square metres space. Meanwhile, the incoming supply of shopping complexes declined by 22%, while construction starts dropped 64.2% during the first half of 2014. However, the overall occupancy rate remained high at 81.3% (end-June 2013:79.6%), reflecting strong retail activities supported by resilient private consumption. As at end-June 2014, the stock of shopping complexes and PBO stood at 12.39 million square metres and 19.20 million square metres, respectively (end-June 2013: 12.18 million square metres; 18.87 million square metres).

The residential subsector expanded strongly by 22.1% during the first half of 2014 (January to June 2013: 15.7%) supported by higher growth in incoming supply at 9.5% (January – June 2013: 15.3%). Meanwhile, new housing approvals increased significantly by 32.6% to 96,115 units (January – June 2013: 6.8%; 72,461 units). Despite the decline in housing starts at 5.3% to 70,346 units (January – June 2013: 21.1%; 74,270 units), residential activity is expected to remain stable. Meanwhile, the value of total property transactions increased to RM82 billion (January – June 2013: RM68.8 billion), with volume expanding 3.3% to 193,405 transactions during the first six months of 2014. Residential property transactions formed the bulk with a share of 63.5%. However, following several cooling measures imposed to curb speculative activity in the property sector, the number of residential property transactions decreased 2.7% in the first half of 2014 (July – December 2013: 5.1%). During the same period, residential transactions declined in Kuala Lumpur (-4.8%) and Selangor (-2.1%), while Johor and Pulau Pinang registered positive growth of 17.5% and 2.7%, respectively. Meanwhile, the residential overhang declined 11.5% to 12,105 units during the first half of 2014 (January – June 2013: 15.1%; 13,673 units), with a total value of RM4.5 billion (January – June 2013: RM5 billion). House prices in Malaysia continue to rise, albeit at a slower pace, amid several measures to curb rising house prices since 2010. The increase in house prices was driven by strong demand following favourable labour market conditions and growing household income. The Malaysian House Price Index, which measures the change in prices paid for an average house, increased moderately by 6.6%, in the second quarter of 2014, compared with 11.3% in the corresponding period in 2013. This was the lowest quarterly rate of increase since the third quarter of 2010. However, higher-than-average prices were recorded in Selangor (10.1%), Pulau Pinang (9.6%) and Kuala Lumpur (9.1%). The highest price increase was recorded for terrace houses, which grew 8.2% followed by high-rise units (7.9%), detached houses (2.5%) and semi-detached houses (2.4%). The residential subsector is expected to remain strong in view of the increased demand, particularly from the middle-income group. The demand for affordable housing will remain favourable amid government initiatives such as the PR1MA housing project. Moreover, the non-residential subsector is also expected to remain stable supported by encouraging demand for industrial and commercial buildings. Major commercial buildings such as the 118-storey Menara Warisan and Bukit Bintang city centre are expected to contribute to the growth of the sector. (Source: Economic Report 2014/2015, Ministry of Finance Malaysia)

4.3 Prospects of the Land

Greater Kuala Lumpur/ Klang Valley region is taken from the Economic Transformation Plan. The region comprises Kuala Lumpur, Putrajaya and all districts in Selangor with the exception of Kuala Langat, Kuala Selangor, Sabak Bernam and Hulu Selangor. The region is defined as being of key economic importance for Malaysia as a whole. Over 37% of the nation’s GDP is identified as being related to Kuala Lumpur and Selangor. (Source: Greater KL/Klang Valley Land Public Transport Master Plan) The Greater Kuala Lumpur/ Klang Valley National Key Economic Area (“NKEA”) is unique from other NKEAs, in that its initiatives are anchored geographically under a goal to develop the region as the centre of Malaysia’s commercial activities. To this end, this NKEA seeks to transform the country’s capital into a world-class city and globally competitive economic hub, focussing on nurturing the elements which support economic growth and improve the region’s liveability.

Among the NKEA’s key achievements in 2013 include Invest KL’s success in attracting fifteen (15) multinational companies from North America, Europe and Asia to set up regional offices in Greater Kuala Lumpur, exceeding the ten (10) MNCs targeted for the year. The MRT project also surpassed targets with the completion of its elevated guide way foundation and underground station excavation, while the River of Life project saw all thirteen (13) key activities under the river cleaning initiative remain on track. A further highlight for the NKEA during the year includes the planting of 36,246 trees under the Greener KL Entry Point Project, which aims to increase green space in the city. With the population of Greater Kuala Lumpur/ Klang Valley expected to grow to 10 million by 2020, the development of an integrated public transport network is necessary to improve the region’s connectivity. The MRT network was proposed to ease congestion and provide commuters to the city centre with an efficient and environmentally sustainable mode of public transportation. (Source: Economic Transformation Programme Annual Report 2013) The Land is located in the northern part of Kuala Lumpur nestled in Klang Valley, within a busy and well-established area with a healthy population growth. In view of that, the Board envisages that the Land has favourable development potential. Its strategic location provides easy access via various highways that links the Land to Petaling Jaya, Selayang, Kepong, Ampang and the Kuala Lumpur city centre, with nearby amenities including shopping malls, wholesale markets, a hospital as well as other recreational areas.

5. RISK FACTORS IN RELATION TO THE PROPOSED ACQUISI TION 5.1 Business Risk

The business activities of the Group are subject to the risks inherent in the property market industry. These risks include, but are not limited to, changes in the economic condition and demand for properties in Malaysia. Factors that may affect demand for property includes labour supply, volatility in construction material prices and changes in regulatory framework of the construction and/or property development industries, which are beyond the control of the Group. The Group faces competition from other property developers. Generally, brand name and reputation, established customer bases, competent personnel and competitive pricing are major factors in maintaining the Group’s market position and securing new sales.

The demand for properties is dependent on the general economic, business and credit conditions, as well as the availability of supply in the market. Whilst the Board believes that it is possible to address any fluctuations in the demand for properties by meticulous planning in terms of innovative design, timing of launch, right type of products/segment and pricing points relative to competitors, there can be no assurance that the Proposed Development will be shielded from any adverse downturn in the economy. Hua Yang will leverage on its strength and experience as a property development manager to manage these risks closely.

5.2 Funding Risk

The Purchase Price is expected to be fully/partially financed via external bank borrowings to be procured by the Group. As such, the Group may incur an interest expense on the bank borrowings. In view that the interest charged on bank borrowings is dependent on prevailing interest rates, future fluctuation of interest rates could have an effect on the Group’s cash flows and profitability. The management of Hua Yang believes that its prudent cash flow management will be able to address the financing risk.

5.3 Non-Completion risk of the Proposed Acquisition

The completion of the Proposed Acquisition is conditional upon the fulfilment of all necessary conditions as set out in Section 2.2(a) above, which includes, among others, the approval from the shareholders of Hua Yang and fulfilment of the conditions precedent by the Vendor and Purchaser. In the event that such approvals and/or conditions are not obtained and/or satisfied, the Proposed Acquisition will not be completed and the Group will not be able to meet its objective as stated in Section 3 of this announcement. However, the Board will take reasonable steps to ensure the fulfilment of the conditions precedent in the SPA to ensure the completion of the Proposed Acquisition.

5.4 Delays in commencement and completion

There are many external factors which are beyond the control of the Group that could affect the timely completion of property development projects such as getting the necessary approvals from relevant authorities, the availability of construction materials in reasonable amounts and satisfactory performance of the appointed building contractors. However, the Group will seek to mitigate such risks by closely monitoring the progress of the development projects and endeavour to promptly come up with solutions to any setbacks in order to ensure the timely completion of the Proposed Development.

6. EFFECTS OF THE PROPOSED ACQUISITION 6.1 Issued and paid-up share capital and substantia l shareholders’ shareholdings

The Proposed Acquisition will not have any effect on the issued and paid-up share capital of Hua Yang as well as Hua Yang’s substantial shareholders’ shareholdings, as the Purchase Price is to be satisfied wholly by cash and does not involve any issuance of shares.

6.2 NA and gearing The Proposed Acquisition is expected to be completed by the second (2nd) half of 2015 and would not have any effect on the consolidated NA of the Group for the financial year ending 31 March 2015. However, the Proposed Acquisition is expected to enhance the consolidated NA of the Group and NA per share of Hua Yang in the future in view of the potential future profit contribution arising from the Proposed Development. As the Purchase Price is to be satisfied by internally-generated funds and bank borrowings and the exact manner in which the Purchase Price will be satisfied has not been finalised at this juncture, the effect of the Proposed Acquisition on the gearing cannot be ascertained at this juncture.

6.3 Earnings and earnings per share

The Proposed Acquisition is not expected to have any material effect on the earnings of the Group for the financial year ending 31 March 2015 in view that the Proposed Acquisition is expected to be completed in the second half of 2015. However, the proposed development of the Land is expected to contribute positively to the Group’s future earnings and earnings per share.

7. APPROVALS REQUIRED The Proposed Acquisition is conditional upon the following approvals being obtained:

(a) approval from the shareholders of Hua Yang at an extraordinary general meeting (“EGM”) to be convened;

(b) the shareholders of the Vendor in respect of the Vendor’s disposal of the Land to the Purchaser;

(c) Approval from Jawatankuasa Kerja Tanah Wilayah Persekutuan Kuala Lumpur for the transfer of ownership to the Purchaser; and

(d) any other relevant parties and/or authorities, if required. The Proposed Acquisition is not conditional upon any other corporate exercise/scheme of Hua Yang.

8. INTEREST OF DIRECTORS, MAJOR SHAREHOLDERS AND/OR PERSONS CONNECTED TO THEM

None of the directors, major shareholders of Hua Yang and/or persons connected to them have any interest, whether direct or indirect, in the Proposed Acquisition.

9. DIRECTORS’ STATEMENT

The Board, after having considered all aspects of the Proposed Acquisition is of the opinion that the Proposed Acquisition is in the best interest of the Company.

10. HIGHEST PERCENTAGE RATIO

The highest percentage ratio applicable to the Proposed Acquisition pursuant to Paragraph 10.02(g) of the Main Market Listing Requirements of Bursa Malaysia Securities Berhad (“Bursa Securities ”) is 31.01%.

11. ADVISER Kenanga IB has been appointed as the adviser to Hua Yang for the Proposed Acquisition.

12. ESTIMATED TIMEFRAME FOR COMPLETION The draft circular to shareholders pertaining to the Proposed Acquisition shall be submitted to Bursa Securities within two (2) months from the date of this announcement. Barring any unforeseen circumstances, subject to the fulfilment of all conditions as set out in the SPA and subject to all required approvals being obtained, the Proposed Acquisition is expected to be completed by the second half of 2015.

13. DOCUMENTS FOR INSPECTION The SPA and the indicative valuation letter by the Valuer dated 29 January 2015 will be made available for inspection during normal business hours at the registered office of Hua Yang at 123A, Jalan Raja Permaisuri Bainun (Jalan Kampar) 30250 Ipoh, Perak Darul Ridzuan, from Mondays to Fridays (except public holidays) from the date of this announcement up to and including the date of the EGM of Hua Yang to be convened in relation to the Proposed Acquisition.

This announcement is dated 30 January 2015.