sijil tinggi muamalat 2 - pengenalan kepada sistem kewangan islam : haji mohd nazri chik (bimb)

TRANSCRIPT

PENGENALAN KEPADA SISTEM

KEWANGAN ISLAM

HAJI MOHD NAZRI CHIK PENGURUS BESAR/ KETUA BAHAGIAN SYARIAH

Strictly Private & Confidential

OBJEKTIF PEMBELAJARAN HARI INI

Shariah Division Page 2

Di akhir kursus subjek ini, peserta

akan dapat:

1. Memahami maksud ekonomi,

kewangan dan perbankan.

2. Memahami sistem kewangan

Islam dan cakupannya.

Page 3

o What Exactly Is Islamic Finance?

o Shariah: The Bedrock of Islamic Finance

o Takaful: Protection in Islamic Ways

o Islamic Capital Market

Sukuk Market

Equity Market

AGENDA

Shariah Division

WHAT IS ISLAMIC FINANCE?

Shariah Division Page 4

Is it all about money?

Is it concerns resource allocation, management,

acquisition and investment?

SUMMARY – a broad term and takes into

account many aspects of the economy and

financial system since its deals with matters

related to money.

Islamic finance is built upon distinctive and unique characteristics which are based upon certain principles underlined by the Shariah (Islamic law).

STRATEGIC OVERVIEW OF ISLAMIC FINANCE

Shariah Division Page 5

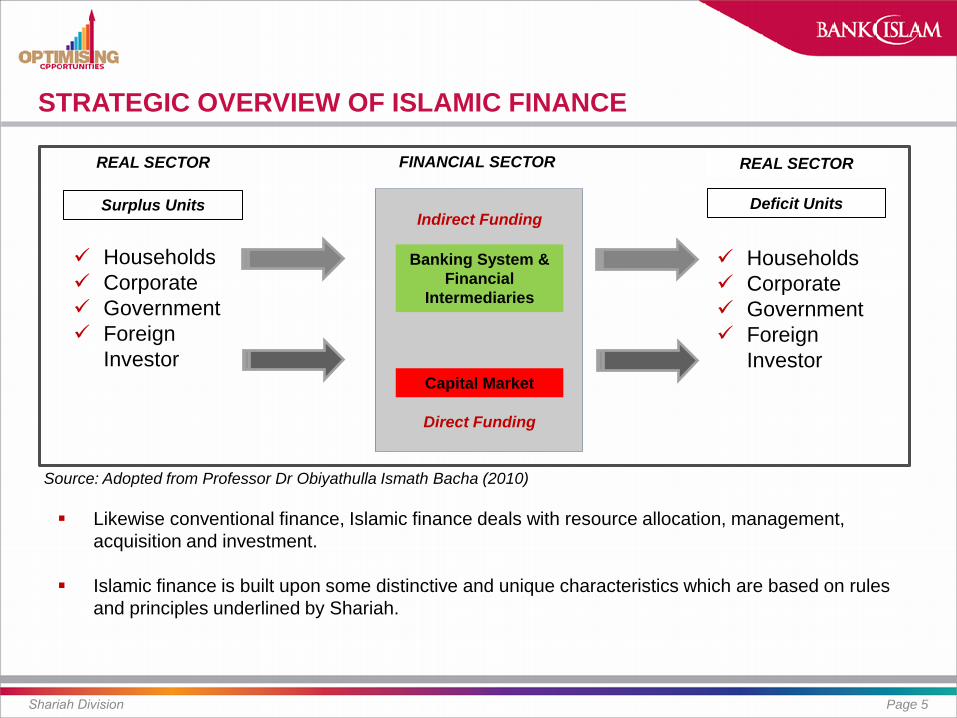

Likewise conventional finance, Islamic finance deals with resource allocation, management,

acquisition and investment.

Islamic finance is built upon some distinctive and unique characteristics which are based on rules

and principles underlined by Shariah.

Banking System &

Financial

Intermediaries

Capital Market

Indirect Funding

Direct Funding

REAL SECTOR FINANCIAL SECTOR REAL SECTOR

Surplus Units Deficit Units

Households

Corporate

Government

Foreign

Investor

Households

Corporate

Government

Foreign

Investor

Source: Adopted from Professor Dr Obiyathulla Ismath Bacha (2010)

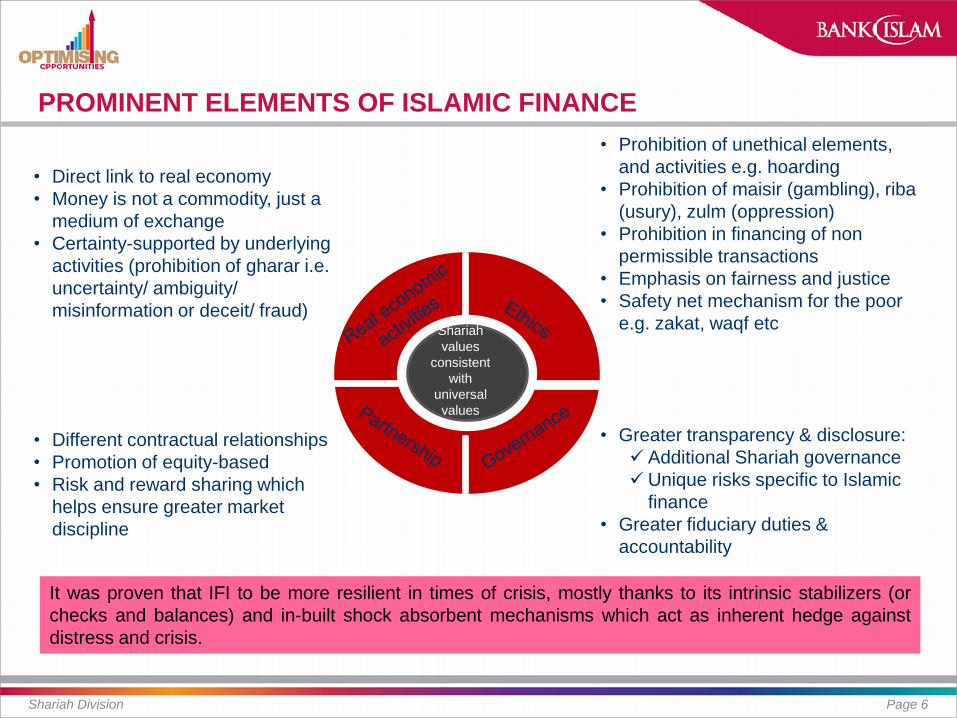

PROMINENT ELEMENTS OF ISLAMIC FINANCE

Shariah Division Page 6

• Direct link to real economy

• Money is not a commodity, just a

medium of exchange

• Certainty-supported by underlying

activities (prohibition of gharar i.e.

uncertainty/ ambiguity/

misinformation or deceit/ fraud)

• Different contractual relationships

• Promotion of equity-based

• Risk and reward sharing which

helps ensure greater market

discipline

• Prohibition of unethical elements,

and activities e.g. hoarding

• Prohibition of maisir (gambling), riba

(usury), zulm (oppression)

• Prohibition in financing of non

permissible transactions

• Emphasis on fairness and justice

• Safety net mechanism for the poor

e.g. zakat, waqf etc

• Greater transparency & disclosure:

Additional Shariah governance

Unique risks specific to Islamic

finance

• Greater fiduciary duties &

accountability

Shariah

values

consistent

with

universal

values

It was proven that IFI to be more resilient in times of crisis, mostly thanks to its intrinsic stabilizers (or

checks and balances) and in-built shock absorbent mechanisms which act as inherent hedge against

distress and crisis.

VATICAN SAYS…

Shariah Division Page 7

EVOLUTION OF ISLAMIC FINANCE

Shariah Division Page 8

First references to interest-free finance appeared in 1940s and more serious discussions and debates on fundamentals of Islamic finance took place in 1950s and 1960s

Modern forms of Islamic financial institutions can be traced back to:

1962 - Tabung Haji

1963 - a small banking experiment set up “under cover” in Mit Ghamr, Egypt, based on a German savings bank model but modified to comply with Shariah in particular profit-sharing (lasted 1967)

The institutional development of Islamic finance in particular its banking segment began to gather speed with the establishment of:

Dubai Islamic Bank in 1973 (first commercial Islamic bank)

Islamic Development Bank in 1974 (in the world)

Bank Islam Malaysia Berhad in 1983 (in Malaysia level)

End 2009 – Islamic assets of the global IFI are worth about US$1 trillion and more than 600 Islamic financial institutions operating in at least 75 countries in the Muslim and the Western world.

EVOLUTION: BEYOND NATION WITH MUSLIM POPULATION

Shariah Division Page 9

Burgeoning interest in Islamic finance over the past decade among:

– the so-called non-Muslim nations such as Australia, China, Germany, France, Holland, Italy,

Hong Kong, Japan, Luxembourg, New Zealand, Russia, Singapore, South Africa, South Korea,

the UK and the US

– the so-called non-traditional key Islamic finance markets in particular countries in Central

Asia such as Kazakhstan, Kyrgystan, Tajikistan, Turkmenistan and Uzbekistan; in Eurasia such

as Azerbaijan and in Africa such as the Comoros, Gambia, Kenya, Mali, Nigeria, Senegal,

TanzaniA

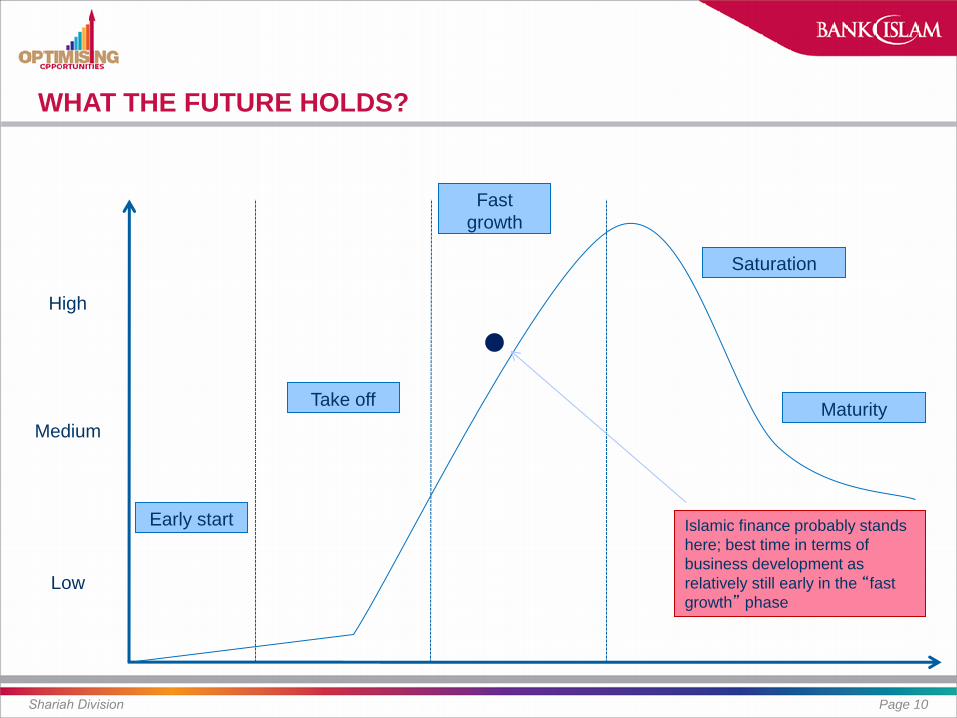

WHAT THE FUTURE HOLDS?

Shariah Division Page 10

Early start

Take off

Fast

growth

Maturity

Islamic finance probably stands

here; best time in terms of

business development as

relatively still early in the “fast

growth” phase

High

Medium

Low

Saturation

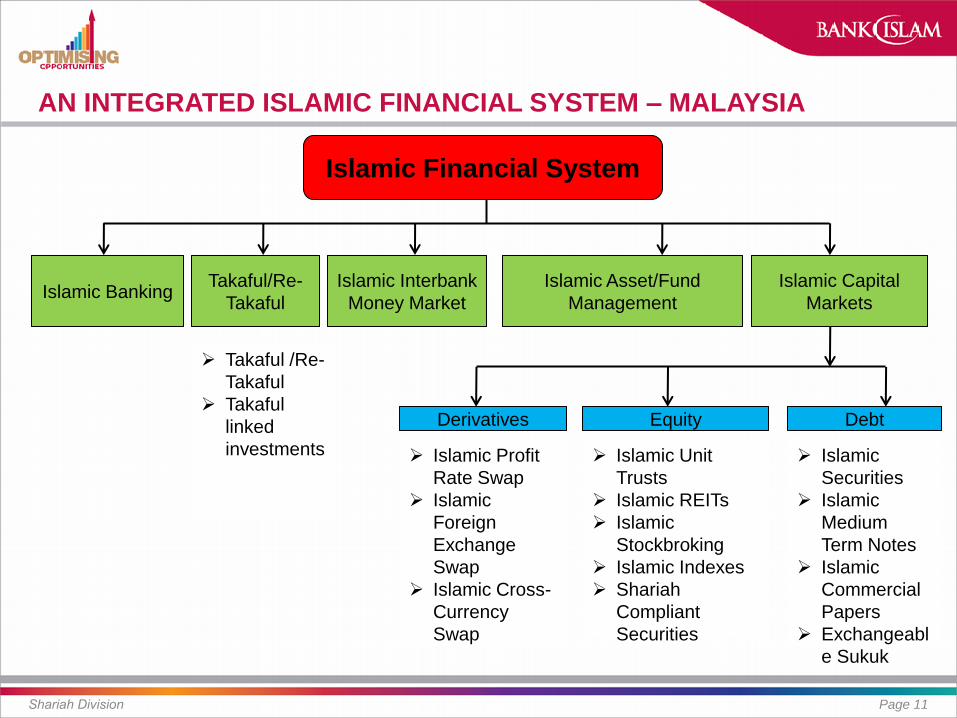

AN INTEGRATED ISLAMIC FINANCIAL SYSTEM – MALAYSIA

Shariah Division Page 11

Islamic Financial System

Islamic Banking Islamic Capital

Markets

Equity Debt Derivatives

Islamic Profit

Rate Swap

Islamic

Foreign

Exchange

Swap

Islamic Cross-

Currency

Swap

Islamic Unit

Trusts

Islamic REITs

Islamic

Stockbroking

Islamic Indexes

Shariah

Compliant

Securities

Islamic

Securities

Islamic

Medium

Term Notes

Islamic

Commercial

Papers

Exchangeabl

e Sukuk

Islamic Interbank

Money Market

Takaful/Re-

Takaful

Islamic Asset/Fund

Management

Takaful /Re-

Takaful

Takaful

linked

investments

Page 12

o What Exactly Is Islamic Finance?

o Shariah: The Bedrock of Islamic Finance

o Takaful: Protection in Islamic Ways

o Islamic Capital Market

Sukuk Market

Equity Market

AGENDA

Shariah Division

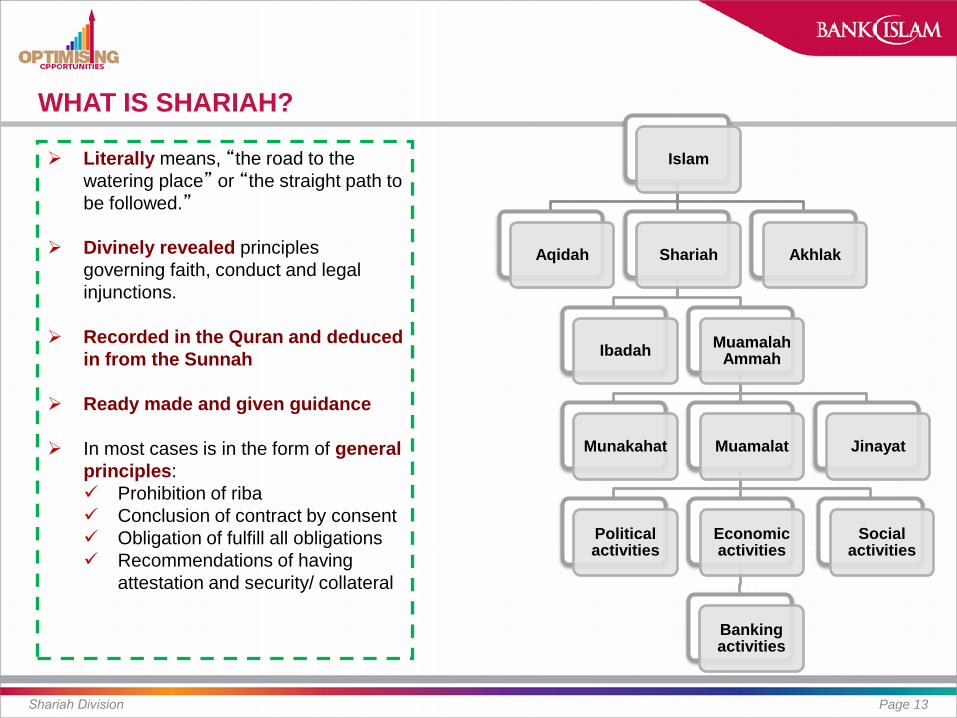

WHAT IS SHARIAH?

Shariah Division Page 13

Literally means, “the road to the

watering place” or “the straight path to

be followed.”

Divinely revealed principles

governing faith, conduct and legal

injunctions.

Recorded in the Quran and deduced

in from the Sunnah

Ready made and given guidance

In most cases is in the form of general

principles:

Prohibition of riba

Conclusion of contract by consent

Obligation of fulfill all obligations

Recommendations of having

attestation and security/ collateral

Islam

Aqidah Shariah

Ibadah Muamalah

Ammah

Munakahat Muamalat

Political activities

Economic activities

Banking activities

Social activities

Jinayat

Akhlak

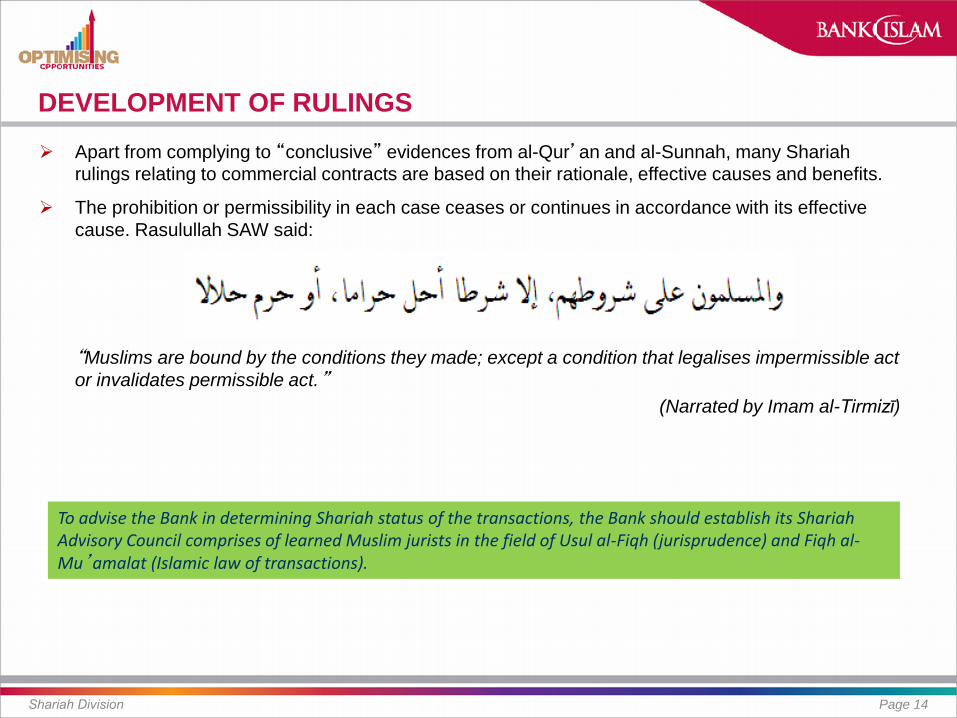

DEVELOPMENT OF RULINGS

Shariah Division Page 14

Apart from complying to “conclusive” evidences from al-Qur’an and al-Sunnah, many Shariah

rulings relating to commercial contracts are based on their rationale, effective causes and benefits.

The prohibition or permissibility in each case ceases or continues in accordance with its effective

cause. Rasulullah SAW said:

“Muslims are bound by the conditions they made; except a condition that legalises impermissible act

or invalidates permissible act.”

(Narrated by Imam al-Tirmizī)

To advise the Bank in determining Shariah status of the transactions, the Bank should establish its Shariah Advisory Council comprises of learned Muslim jurists in the field of Usul al-Fiqh (jurisprudence) and Fiqh al-Mu’amalat (Islamic law of transactions).

FUNDAMENTALS PROHIBITED ELEMENTS

Shariah Division Page 15

Shariah compliant transactions, structurally,

means;

Abstinence of the prohibited elements which

must be first removed and cut off:

o Riba,

o Gharar,

o Maisir

Observe that every contract possesses all the

essential elements (arkan) of contracts and

that every essential element meet the

necessary conditions (shurut).

Does not involve illegal commodities e.g. pork

and liqour

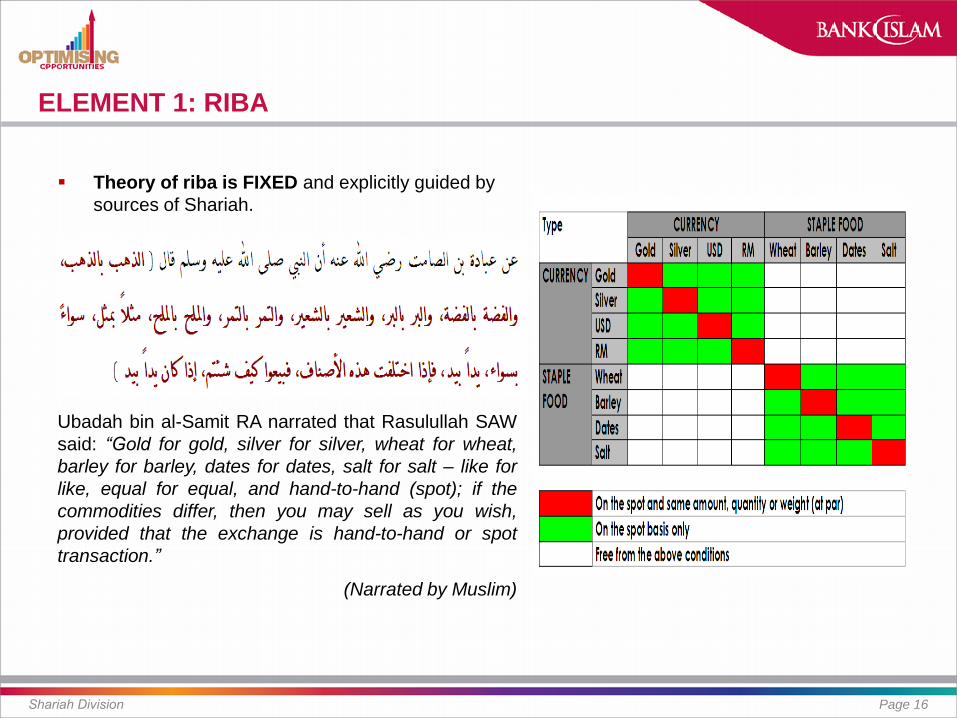

ELEMENT 1: RIBA

Shariah Division Page 16

Theory of riba is FIXED and explicitly guided by

sources of Shariah.

Ubadah bin al-Samit RA narrated that Rasulullah SAW

said: “Gold for gold, silver for silver, wheat for wheat,

barley for barley, dates for dates, salt for salt – like for

like, equal for equal, and hand-to-hand (spot); if the

commodities differ, then you may sell as you wish,

provided that the exchange is hand-to-hand or spot

transaction.”

(Narrated by Muslim)

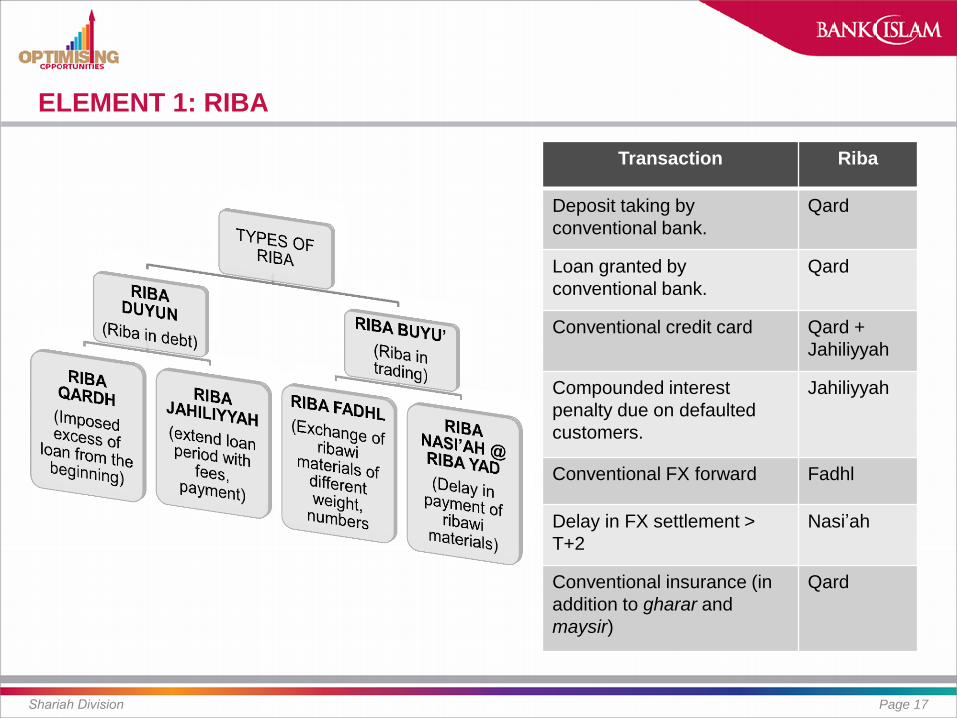

ELEMENT 1: RIBA

Shariah Division Page 17

Transaction Riba

Deposit taking by

conventional bank.

Qard

Loan granted by

conventional bank.

Qard

Conventional credit card Qard +

Jahiliyyah

Compounded interest

penalty due on defaulted

customers.

Jahiliyyah

Conventional FX forward Fadhl

Delay in FX settlement >

T+2

Nasi’ah

Conventional insurance (in

addition to gharar and

maysir)

Qard

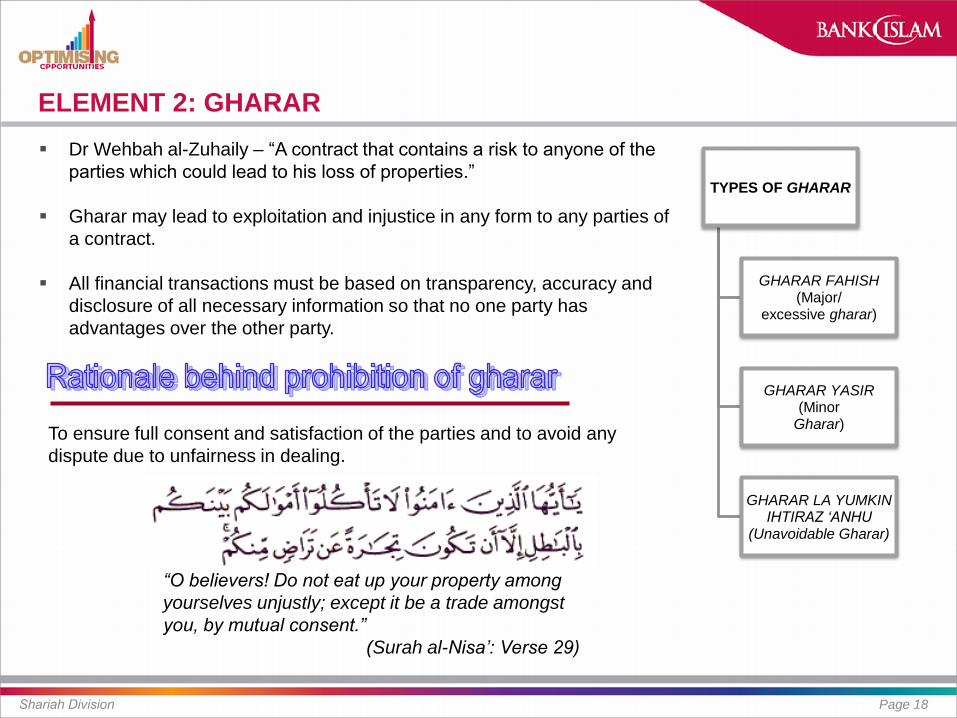

ELEMENT 2: GHARAR

Shariah Division Page 18

Dr Wehbah al-Zuhaily – “A contract that contains a risk to anyone of the

parties which could lead to his loss of properties.”

Gharar may lead to exploitation and injustice in any form to any parties of

a contract.

All financial transactions must be based on transparency, accuracy and

disclosure of all necessary information so that no one party has

advantages over the other party.

TYPES OF GHARAR

GHARAR FAHISH (Major/

excessive gharar)

GHARAR YASIR (Minor

Gharar)

GHARAR LA YUMKIN IHTIRAZ ‘ANHU

(Unavoidable Gharar)

To ensure full consent and satisfaction of the parties and to avoid any

dispute due to unfairness in dealing.

“O believers! Do not eat up your property among

yourselves unjustly; except it be a trade amongst

you, by mutual consent.”

(Surah al-Nisa’: Verse 29)

ELEMENT 2: GHARAR

Shariah Division Page 19

• Example: The seller is not in a position to hand over the subject matter to the buyer

• Example: Characteristics of the exchange counter-value, its species, quantities, date of delivery

etc.

• Prohibited because there exists the possibility of deceit or fraud in such a contract.

• Example: Seller says: “I sell to you this item at RM100 in cash today and RM110 to be paid in

one year.” Then buyer said: “I accept” without specifying at which price he buys the item.

1. Gharar due to non-existence of the exchange counter-values (settlement risk or counter

party risk)

2. Gharar due to inadequacy or inaccuracy of information (non-disclosure of material

information of the subject matter

3. Gharar due to the undue complexity of the contract (combining two sales in one

interdependent contract).

ELEMENT 3: MAISIR

Shariah Division Page 20

Allah SWT says: “O believers! Alcoholic drinks

(khamr), gambling (maisir), slaughtering animals for

the idols (ansab) and looking for luck using arrows

(azlam) are practices of Satan. So avoid (strictly all)

that practices) in order for you to be successful.”

Surah al-Mā’idah [5]: 90

• Any activity which involves betting whereby the winner will take the entire bet and the loser will lose his bet.

• Means games of pure chance where any party might gain at the expense of the loss of the other party.

• Also known as qimar.

Page 21

o What Exactly Is Islamic Finance?

o Shariah: The Bedrock of Islamic Finance

o Takaful: Protection in Islamic Ways

o Islamic Capital Market

Sukuk Market

Equity Market

AGENDA

Shariah Division

Shariah Division Page 22

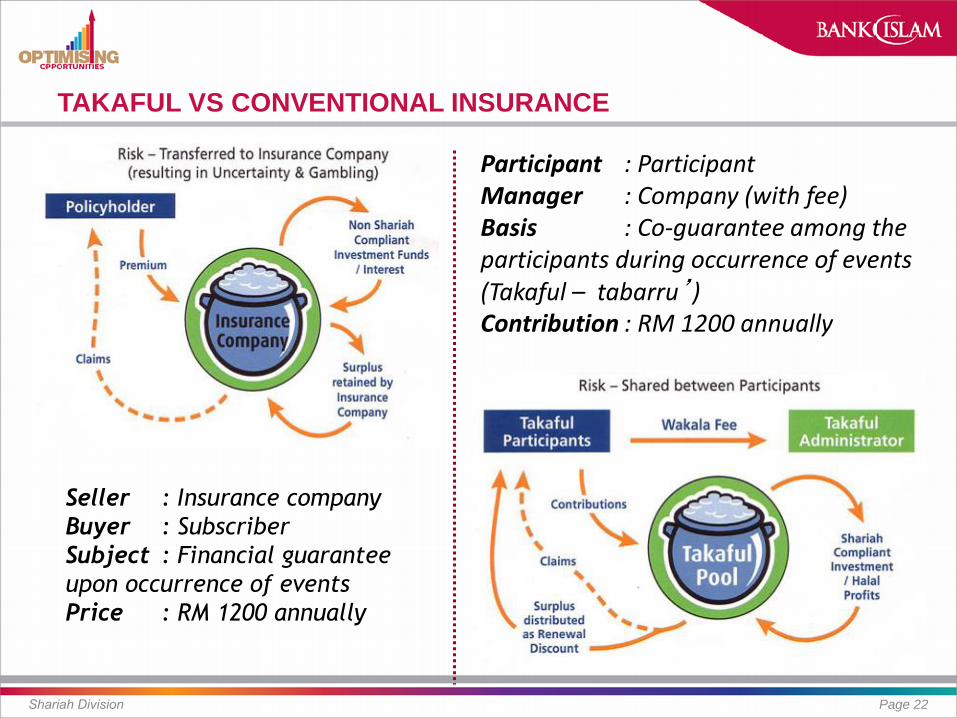

TAKAFUL VS CONVENTIONAL INSURANCE

Seller : Insurance company

Buyer : Subscriber

Subject : Financial guarantee

upon occurrence of events

Price : RM 1200 annually

Participant : Participant Manager : Company (with fee) Basis : Co-guarantee among the participants during occurrence of events (Takaful – tabarru’) Contribution : RM 1200 annually

Page 23

o What Exactly Is Islamic Finance?

o Shariah: The Bedrock of Islamic Finance

o Takaful: Protection in Islamic Ways

o Islamic Capital Market

Sukuk Market

Equity Market

AGENDA

Shariah Division

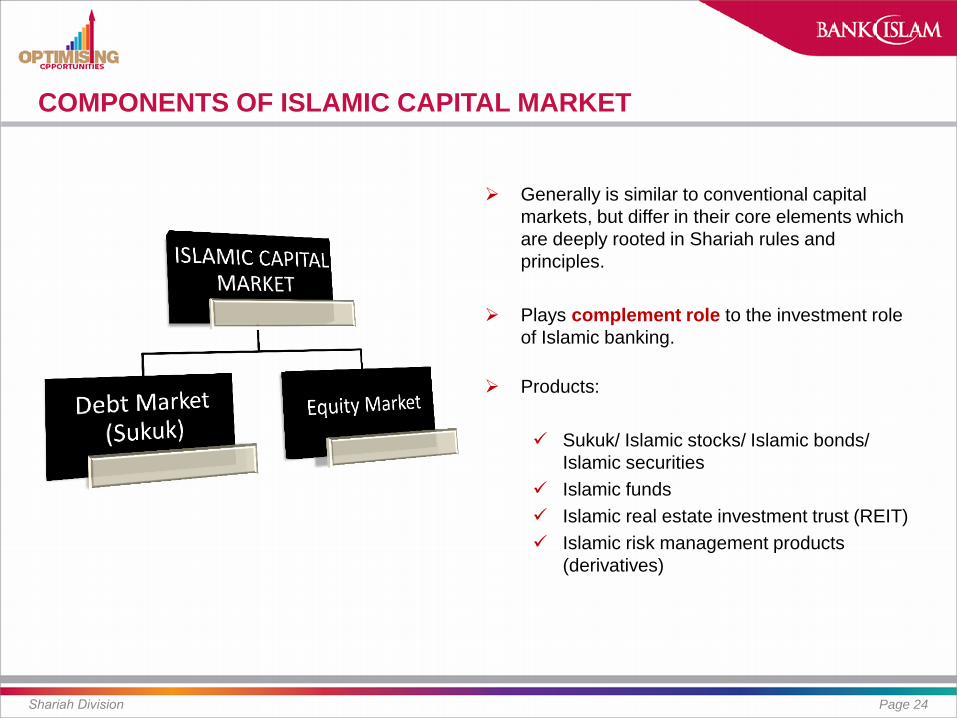

COMPONENTS OF ISLAMIC CAPITAL MARKET

Shariah Division Page 24

Generally is similar to conventional capital

markets, but differ in their core elements which

are deeply rooted in Shariah rules and

principles.

Plays complement role to the investment role

of Islamic banking.

Products:

Sukuk/ Islamic stocks/ Islamic bonds/

Islamic securities

Islamic funds

Islamic real estate investment trust (REIT)

Islamic risk management products

(derivatives)

Page 25

o What Exactly Is Islamic Finance?

o Shariah: The Bedrock of Islamic Finance

o Takaful: Protection in Islamic Ways

o Islamic Capital Market

Sukuk Market

Equity Market

AGENDA

Shariah Division

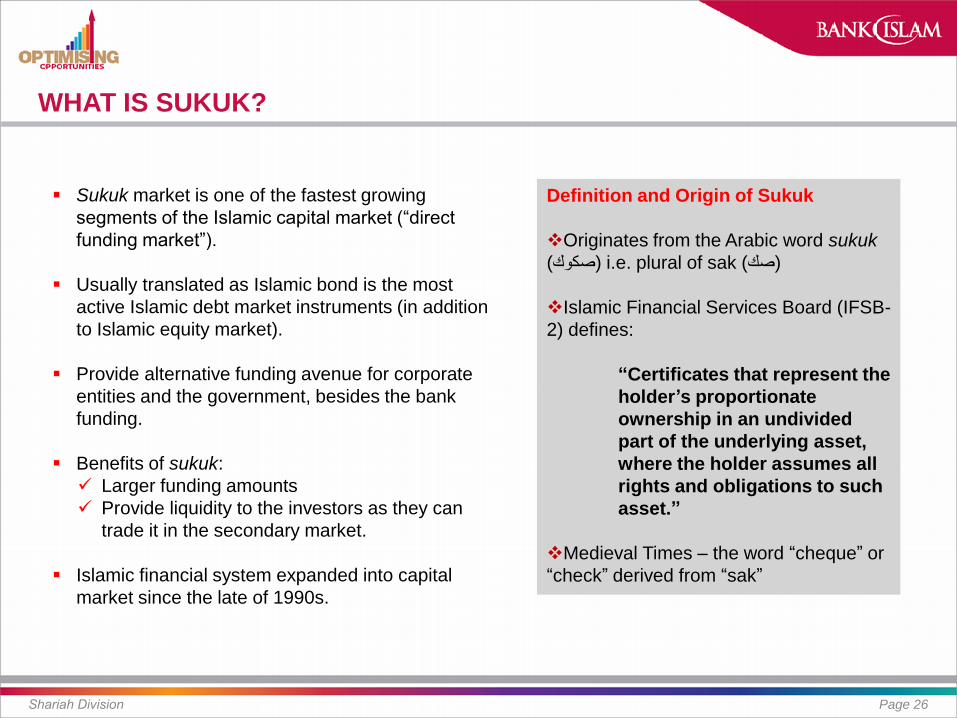

WHAT IS SUKUK?

Shariah Division Page 26

Sukuk market is one of the fastest growing

segments of the Islamic capital market (“direct

funding market”).

Usually translated as Islamic bond is the most

active Islamic debt market instruments (in addition

to Islamic equity market).

Provide alternative funding avenue for corporate

entities and the government, besides the bank

funding.

Benefits of sukuk:

Larger funding amounts

Provide liquidity to the investors as they can

trade it in the secondary market.

Islamic financial system expanded into capital

market since the late of 1990s.

Definition and Origin of Sukuk

Originates from the Arabic word sukuk

(صك) i.e. plural of sak (صكوك)

Islamic Financial Services Board (IFSB-

2) defines:

“Certificates that represent the

holder’s proportionate

ownership in an undivided

part of the underlying asset,

where the holder assumes all

rights and obligations to such

asset.”

Medieval Times – the word “cheque” or

“check” derived from “sak”

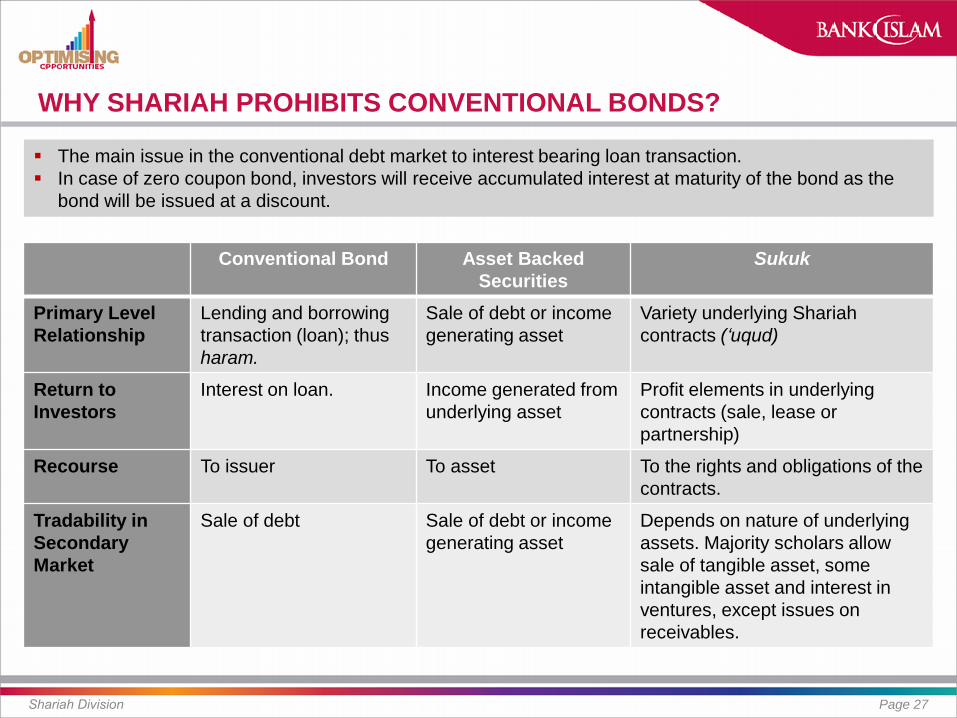

WHY SHARIAH PROHIBITS CONVENTIONAL BONDS?

Shariah Division Page 27

Conventional Bond Asset Backed

Securities

Sukuk

Primary Level

Relationship

Lending and borrowing

transaction (loan); thus

haram.

Sale of debt or income

generating asset

Variety underlying Shariah

contracts (‘uqud)

Return to

Investors

Interest on loan. Income generated from

underlying asset

Profit elements in underlying

contracts (sale, lease or

partnership)

Recourse To issuer To asset To the rights and obligations of the

contracts.

Tradability in

Secondary

Market

Sale of debt Sale of debt or income

generating asset

Depends on nature of underlying

assets. Majority scholars allow

sale of tangible asset, some

intangible asset and interest in

ventures, except issues on

receivables.

The main issue in the conventional debt market to interest bearing loan transaction.

In case of zero coupon bond, investors will receive accumulated interest at maturity of the bond as the

bond will be issued at a discount.

FUNDAMENTALS SHARIAH REQUIREMENT

Shariah Division Page 28

1. Funds raised must be used for Shariah compliant (halal)

activities.

2. Fund raised may be used to finance needed tangible assets.

Specificity of assets is important, since Sukuk unlike conventional

bonds cannot be used for general financial needs of the issuer.

3. Income received by sukukholders (investors) must be derived

from the cash flows generated by the underlying.

4. Sukukholders have a right to the ownership of the underlying

asset and its cash-flows.

5. Clear and transparent specification of rights and obligations of

all parties to the transaction, in particular the originator (customer)

and sukukholders.

6. No fixity in returns.

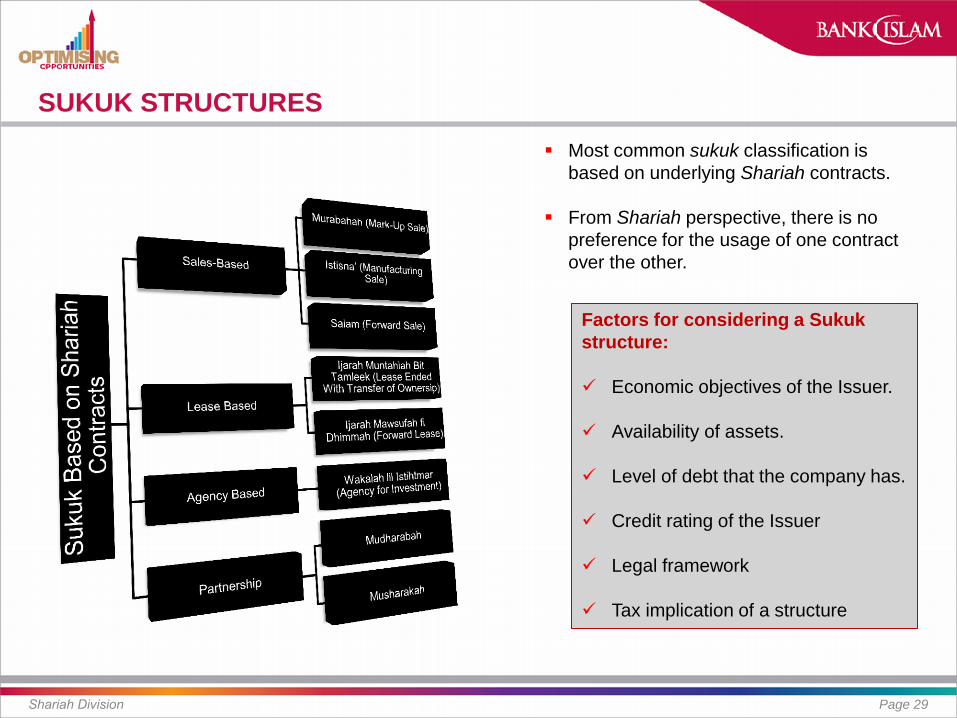

SUKUK STRUCTURES

Shariah Division Page 29

Most common sukuk classification is

based on underlying Shariah contracts.

From Shariah perspective, there is no

preference for the usage of one contract

over the other.

Factors for considering a Sukuk

structure:

Economic objectives of the Issuer.

Availability of assets.

Level of debt that the company has.

Credit rating of the Issuer

Legal framework

Tax implication of a structure

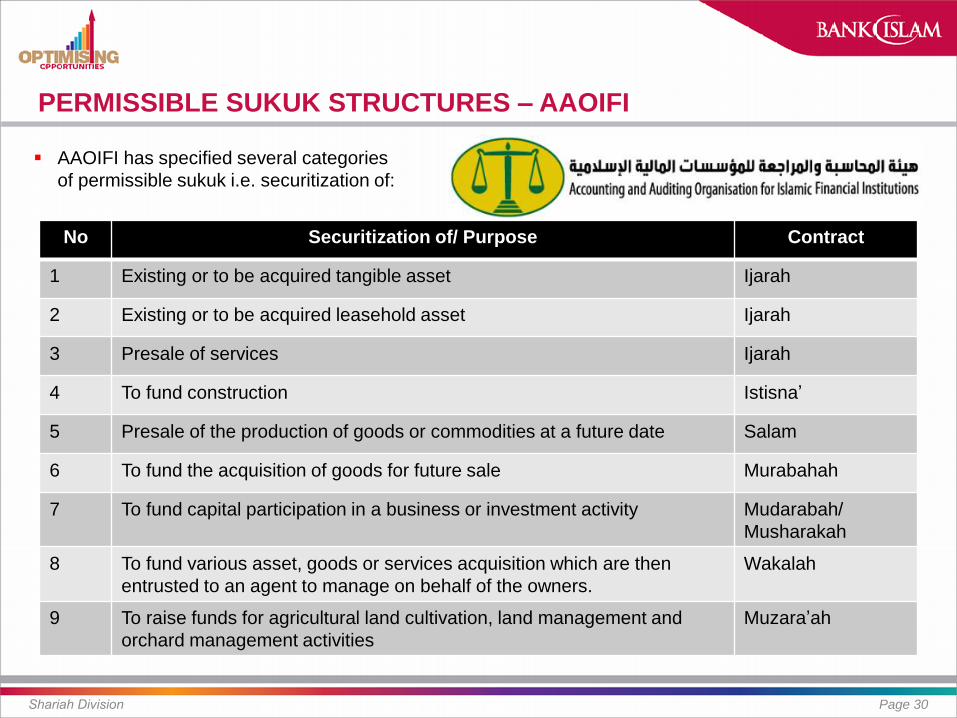

PERMISSIBLE SUKUK STRUCTURES – AAOIFI

Shariah Division Page 30

AAOIFI has specified several categories

of permissible sukuk i.e. securitization of:

No Securitization of/ Purpose Contract

1 Existing or to be acquired tangible asset Ijarah

2 Existing or to be acquired leasehold asset Ijarah

3 Presale of services Ijarah

4 To fund construction Istisna’

5 Presale of the production of goods or commodities at a future date Salam

6 To fund the acquisition of goods for future sale Murabahah

7 To fund capital participation in a business or investment activity Mudarabah/

Musharakah

8 To fund various asset, goods or services acquisition which are then

entrusted to an agent to manage on behalf of the owners.

Wakalah

9 To raise funds for agricultural land cultivation, land management and

orchard management activities

Muzara’ah

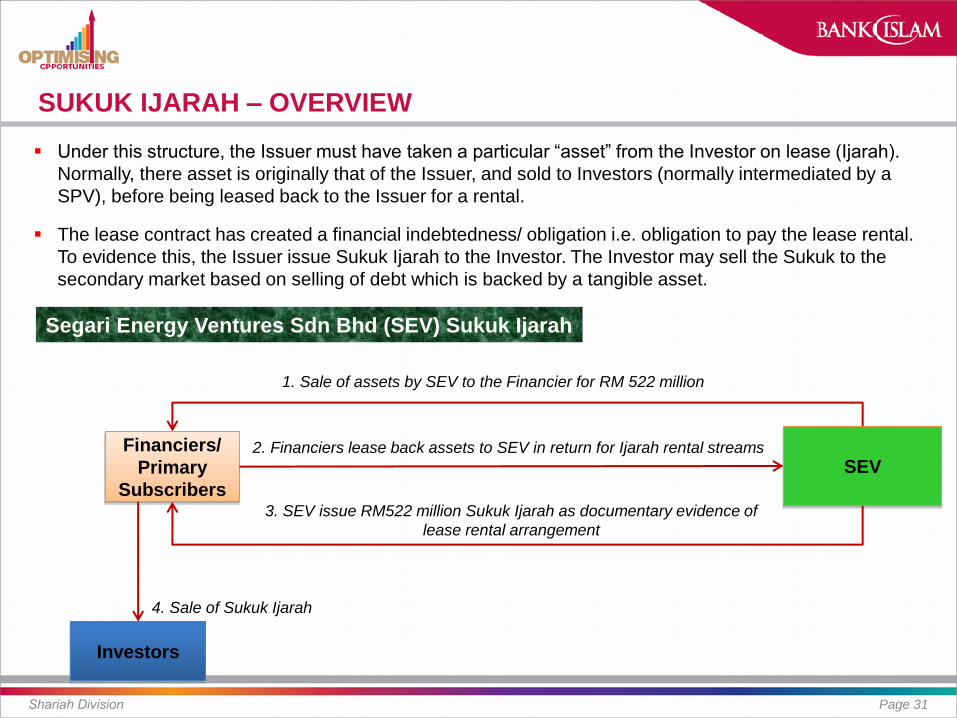

SUKUK IJARAH – OVERVIEW

Shariah Division Page 31

Under this structure, the Issuer must have taken a particular “asset” from the Investor on lease (Ijarah).

Normally, there asset is originally that of the Issuer, and sold to Investors (normally intermediated by a

SPV), before being leased back to the Issuer for a rental.

The lease contract has created a financial indebtedness/ obligation i.e. obligation to pay the lease rental.

To evidence this, the Issuer issue Sukuk Ijarah to the Investor. The Investor may sell the Sukuk to the

secondary market based on selling of debt which is backed by a tangible asset.

Segari Energy Ventures Sdn Bhd (SEV) Sukuk Ijarah

Investors

SEV

1. Sale of assets by SEV to the Financier for RM 522 million

Financiers/

Primary

Subscribers

2. Financiers lease back assets to SEV in return for Ijarah rental streams

3. SEV issue RM522 million Sukuk Ijarah as documentary evidence of

lease rental arrangement

4. Sale of Sukuk Ijarah

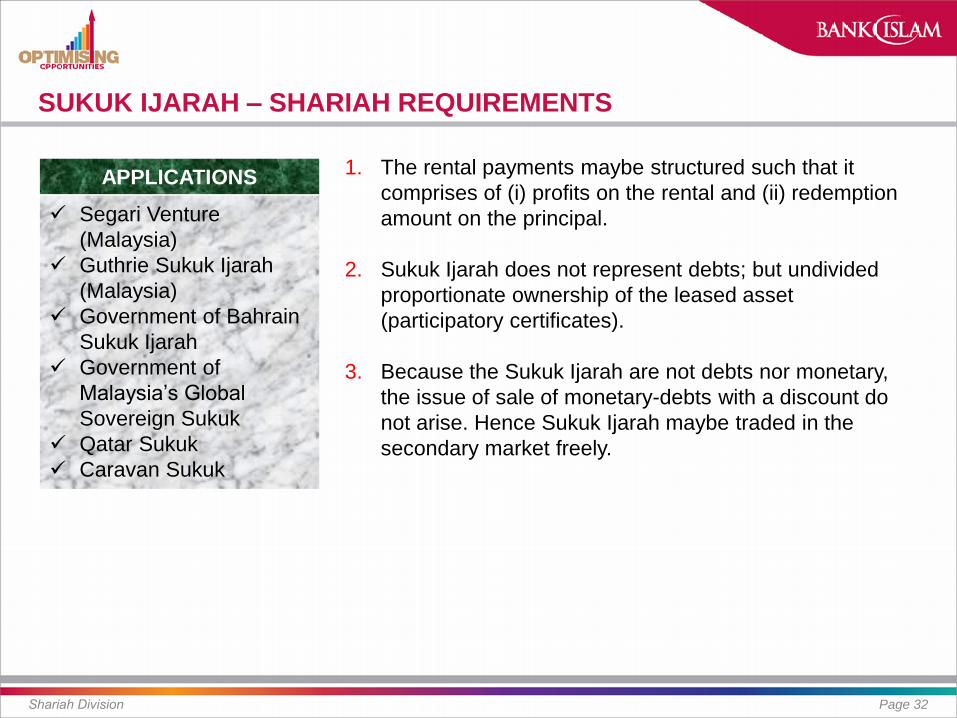

SUKUK IJARAH – SHARIAH REQUIREMENTS

Shariah Division Page 32

1. The rental payments maybe structured such that it

comprises of (i) profits on the rental and (ii) redemption

amount on the principal.

2. Sukuk Ijarah does not represent debts; but undivided

proportionate ownership of the leased asset

(participatory certificates).

3. Because the Sukuk Ijarah are not debts nor monetary,

the issue of sale of monetary-debts with a discount do

not arise. Hence Sukuk Ijarah maybe traded in the

secondary market freely.

APPLICATIONS

Segari Venture

(Malaysia)

Guthrie Sukuk Ijarah

(Malaysia)

Government of Bahrain

Sukuk Ijarah

Government of

Malaysia’s Global

Sovereign Sukuk

Qatar Sukuk

Caravan Sukuk

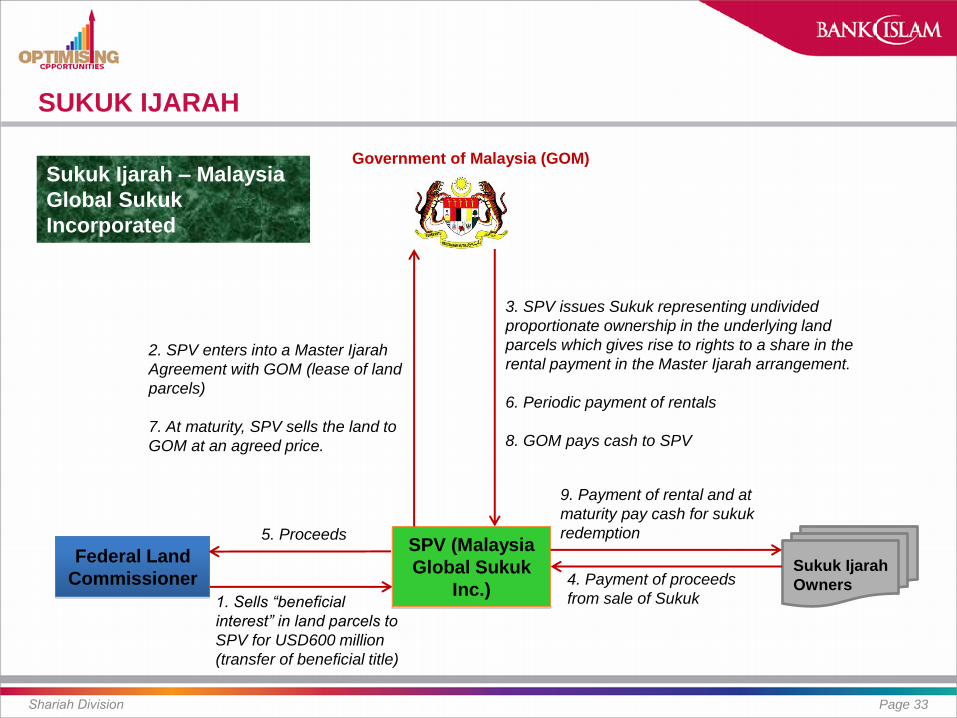

SUKUK IJARAH

Shariah Division Page 33

Sukuk Ijarah – Malaysia

Global Sukuk

Incorporated

Federal Land

Commissioner

SPV (Malaysia

Global Sukuk

Inc.)

Government of Malaysia (GOM)

2. SPV enters into a Master Ijarah

Agreement with GOM (lease of land

parcels)

7. At maturity, SPV sells the land to

GOM at an agreed price.

1. Sells “beneficial

interest” in land parcels to

SPV for USD600 million

(transfer of beneficial title)

Sukuk Ijarah

Owners

5. Proceeds

3. SPV issues Sukuk representing undivided

proportionate ownership in the underlying land

parcels which gives rise to rights to a share in the

rental payment in the Master Ijarah arrangement.

6. Periodic payment of rentals

8. GOM pays cash to SPV

4. Payment of proceeds

from sale of Sukuk

9. Payment of rental and at

maturity pay cash for sukuk

redemption

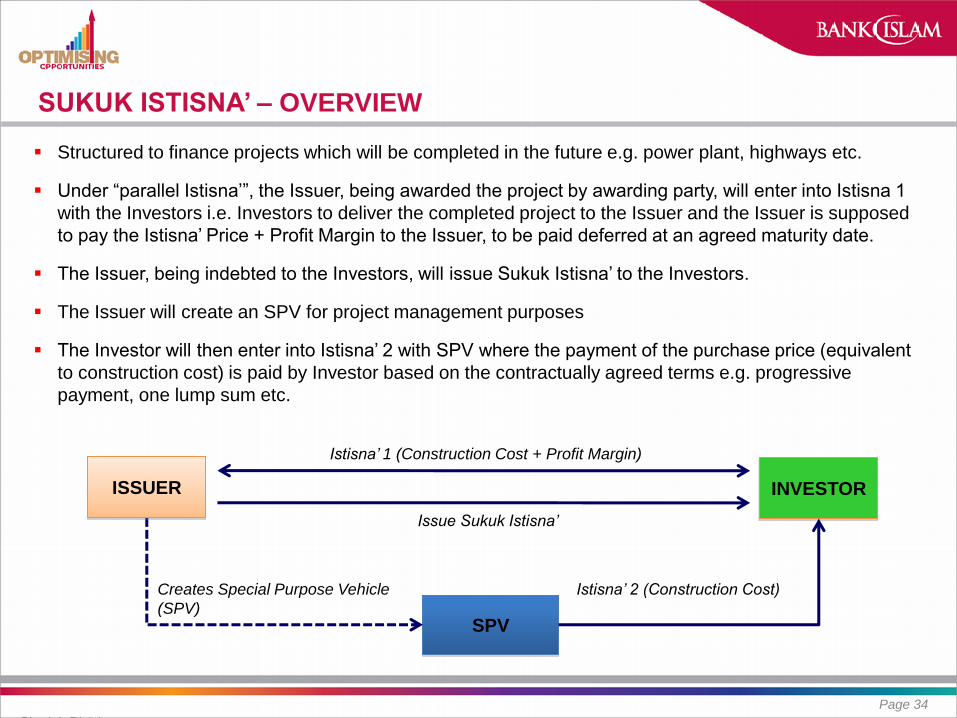

SUKUK ISTISNA’ – OVERVIEW

Shariah Division

Page 34

Structured to finance projects which will be completed in the future e.g. power plant, highways etc.

Under “parallel Istisna’”, the Issuer, being awarded the project by awarding party, will enter into Istisna 1

with the Investors i.e. Investors to deliver the completed project to the Issuer and the Issuer is supposed

to pay the Istisna’ Price + Profit Margin to the Issuer, to be paid deferred at an agreed maturity date.

The Issuer, being indebted to the Investors, will issue Sukuk Istisna’ to the Investors.

The Issuer will create an SPV for project management purposes

The Investor will then enter into Istisna’ 2 with SPV where the payment of the purchase price (equivalent

to construction cost) is paid by Investor based on the contractually agreed terms e.g. progressive

payment, one lump sum etc.

SPV

INVESTOR

Creates Special Purpose Vehicle

(SPV)

Istisna’ 1 (Construction Cost + Profit Margin)

ISSUER

Istisna’ 2 (Construction Cost)

Issue Sukuk Istisna’

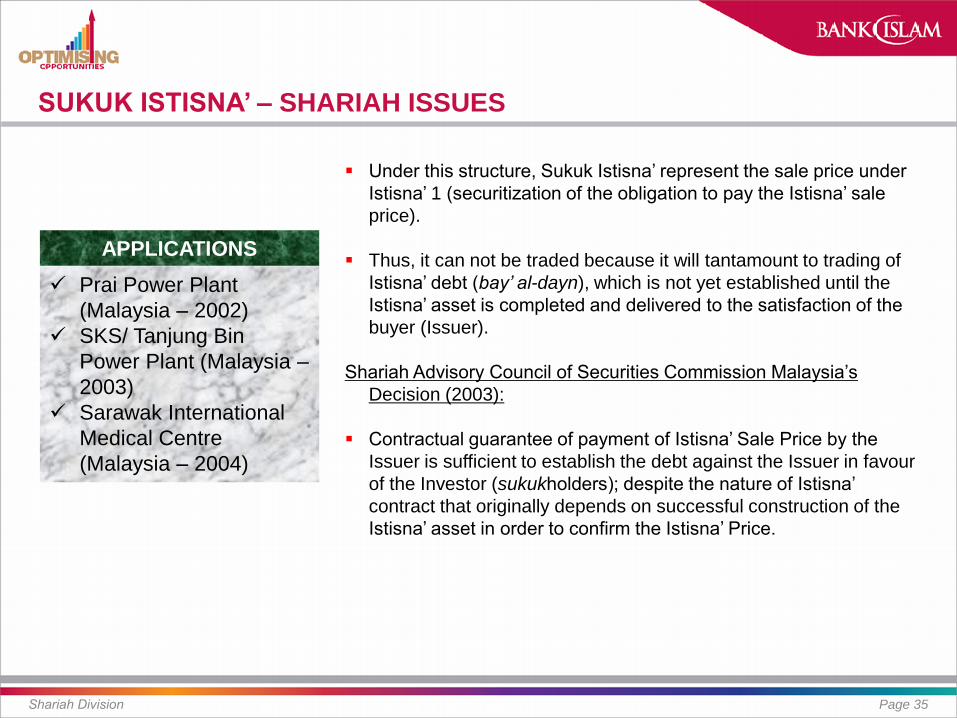

SUKUK ISTISNA’ – SHARIAH ISSUES

Shariah Division Page 35

Under this structure, Sukuk Istisna’ represent the sale price under

Istisna’ 1 (securitization of the obligation to pay the Istisna’ sale

price).

Thus, it can not be traded because it will tantamount to trading of

Istisna’ debt (bay’ al-dayn), which is not yet established until the

Istisna’ asset is completed and delivered to the satisfaction of the

buyer (Issuer).

Shariah Advisory Council of Securities Commission Malaysia’s

Decision (2003):

Contractual guarantee of payment of Istisna’ Sale Price by the

Issuer is sufficient to establish the debt against the Issuer in favour

of the Investor (sukukholders); despite the nature of Istisna’

contract that originally depends on successful construction of the

Istisna’ asset in order to confirm the Istisna’ Price.

APPLICATIONS

Prai Power Plant

(Malaysia – 2002)

SKS/ Tanjung Bin

Power Plant (Malaysia –

2003)

Sarawak International

Medical Centre

(Malaysia – 2004)

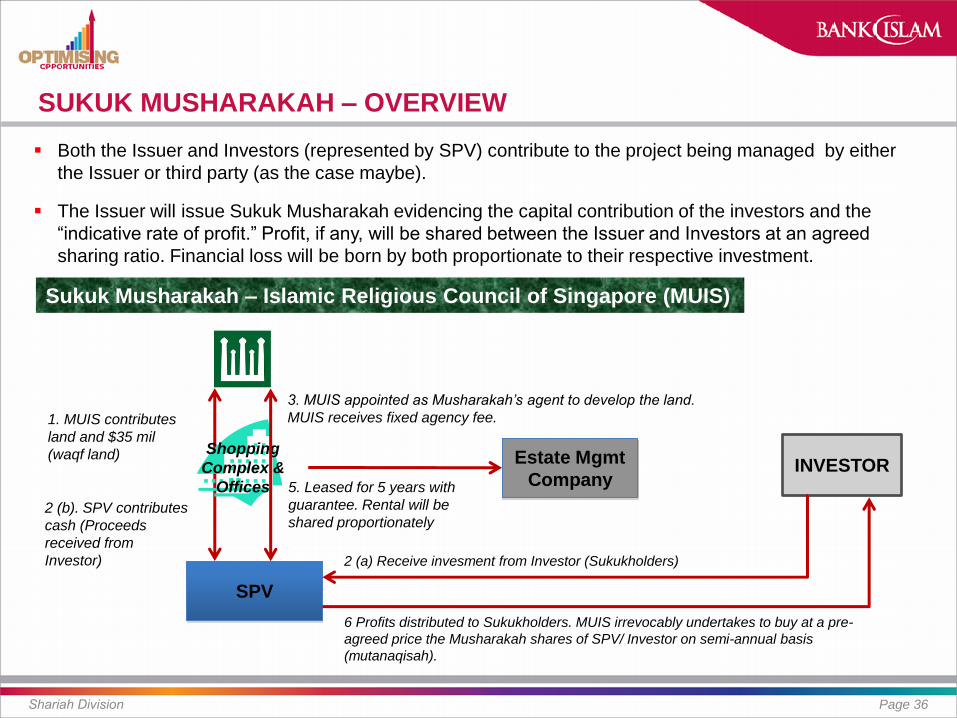

SUKUK MUSHARAKAH – OVERVIEW

Shariah Division Page 36

Both the Issuer and Investors (represented by SPV) contribute to the project being managed by either

the Issuer or third party (as the case maybe).

The Issuer will issue Sukuk Musharakah evidencing the capital contribution of the investors and the

“indicative rate of profit.” Profit, if any, will be shared between the Issuer and Investors at an agreed

sharing ratio. Financial loss will be born by both proportionate to their respective investment.

Sukuk Musharakah – Islamic Religious Council of Singapore (MUIS)

SPV

INVESTOR

1. MUIS contributes

land and $35 mil

(waqf land) Shopping

Complex &

Offices

2 (b). SPV contributes

cash (Proceeds

received from

Investor) 2 (a) Receive invesment from Investor (Sukukholders)

3. MUIS appointed as Musharakah’s agent to develop the land.

MUIS receives fixed agency fee.

Estate Mgmt

Company 5. Leased for 5 years with

guarantee. Rental will be

shared proportionately

6 Profits distributed to Sukukholders. MUIS irrevocably undertakes to buy at a pre-

agreed price the Musharakah shares of SPV/ Investor on semi-annual basis

(mutanaqisah).

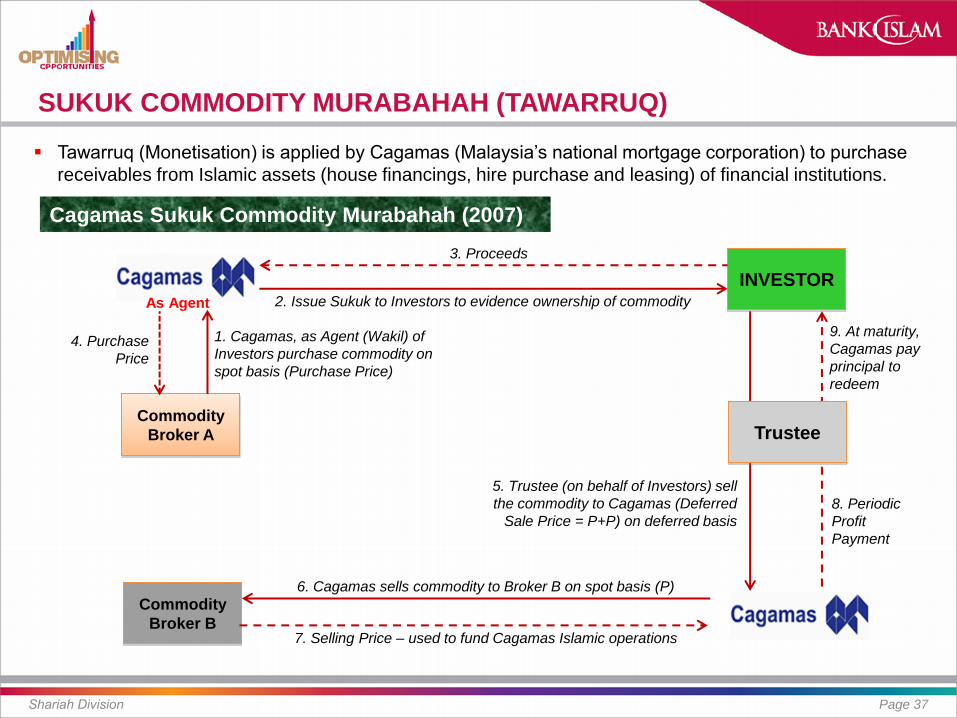

SUKUK COMMODITY MURABAHAH (TAWARRUQ)

Shariah Division Page 37

Tawarruq (Monetisation) is applied by Cagamas (Malaysia’s national mortgage corporation) to purchase

receivables from Islamic assets (house financings, hire purchase and leasing) of financial institutions.

Trustee Commodity

Broker A

1. Cagamas, as Agent (Wakil) of

Investors purchase commodity on

spot basis (Purchase Price)

INVESTOR

Commodity

Broker B

As Agent 2. Issue Sukuk to Investors to evidence ownership of commodity

3. Proceeds

4. Purchase

Price

5. Trustee (on behalf of Investors) sell

the commodity to Cagamas (Deferred

Sale Price = P+P) on deferred basis

6. Cagamas sells commodity to Broker B on spot basis (P)

7. Selling Price – used to fund Cagamas Islamic operations

8. Periodic

Profit

Payment

9. At maturity,

Cagamas pay

principal to

redeem

Cagamas Sukuk Commodity Murabahah (2007)

Shariah Division Page 38

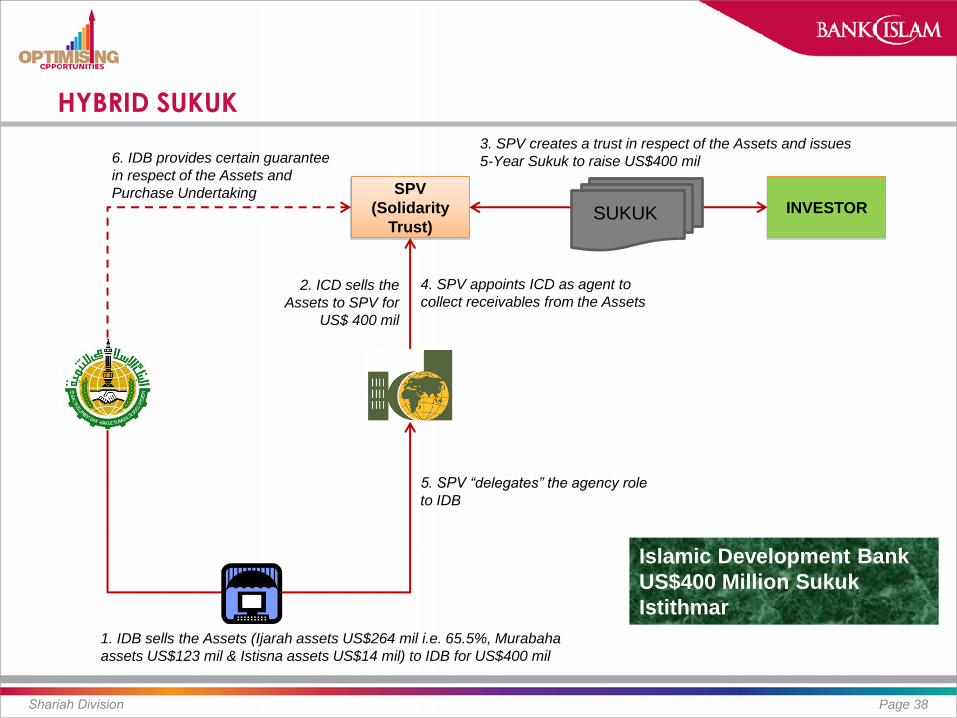

SPV

(Solidarity

Trust)

1. IDB sells the Assets (Ijarah assets US$264 mil i.e. 65.5%, Murabaha

assets US$123 mil & Istisna assets US$14 mil) to IDB for US$400 mil

Islamic Development Bank

US$400 Million Sukuk

Istithmar

2. ICD sells the

Assets to SPV for

US$ 400 mil

INVESTOR SUKUK

3. SPV creates a trust in respect of the Assets and issues

5-Year Sukuk to raise US$400 mil

4. SPV appoints ICD as agent to

collect receivables from the Assets

5. SPV “delegates” the agency role

to IDB

6. IDB provides certain guarantee

in respect of the Assets and

Purchase Undertaking

HYBRID SUKUK

HYBRID SUKUK IDB – SHARIAH REQUIREMENTS

Shariah Division Page 39

1. Shariah Board of IDB viewed that IDB can sell a

mixed portfolio of tangible assets (Ijarah properties)

and receivables (murabahah and istisna’) given that

the Ijarah properties are at least 51%.

2. IDB undertook that the Ijarah contract proportion in the

sukuk asset will not fall below 25%.

3. Based on the above, the sukuk can be freely tradable

in the secondary market.

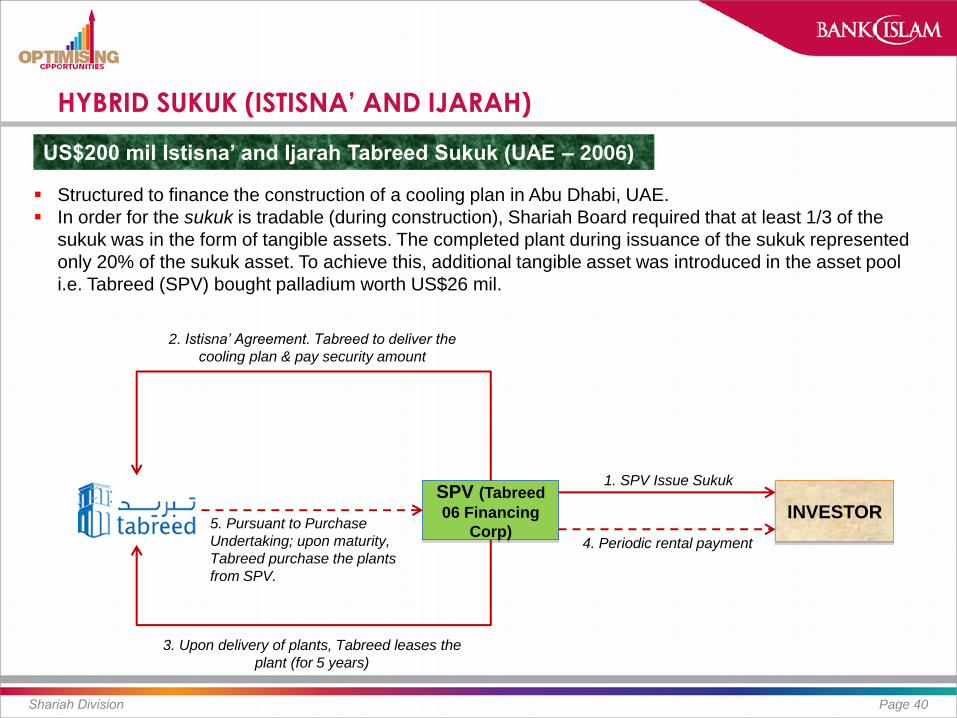

HYBRID SUKUK (ISTISNA’ AND IJARAH)

Shariah Division Page 40

Structured to finance the construction of a cooling plan in Abu Dhabi, UAE.

In order for the sukuk is tradable (during construction), Shariah Board required that at least 1/3 of the

sukuk was in the form of tangible assets. The completed plant during issuance of the sukuk represented

only 20% of the sukuk asset. To achieve this, additional tangible asset was introduced in the asset pool

i.e. Tabreed (SPV) bought palladium worth US$26 mil.

US$200 mil Istisna’ and Ijarah Tabreed Sukuk (UAE – 2006)

SPV (Tabreed

06 Financing

Corp) INVESTOR

1. SPV Issue Sukuk

2. Istisna’ Agreement. Tabreed to deliver the

cooling plan & pay security amount

3. Upon delivery of plants, Tabreed leases the

plant (for 5 years)

4. Periodic rental payment

5. Pursuant to Purchase

Undertaking; upon maturity,

Tabreed purchase the plants

from SPV.

Page 41

o What Exactly Is Islamic Finance?

o Shariah: The Bedrock of Islamic Finance

o Takaful: Protection in Islamic Ways

o Islamic Capital Market

Sukuk Market

Equity Market

AGENDA

Shariah Division

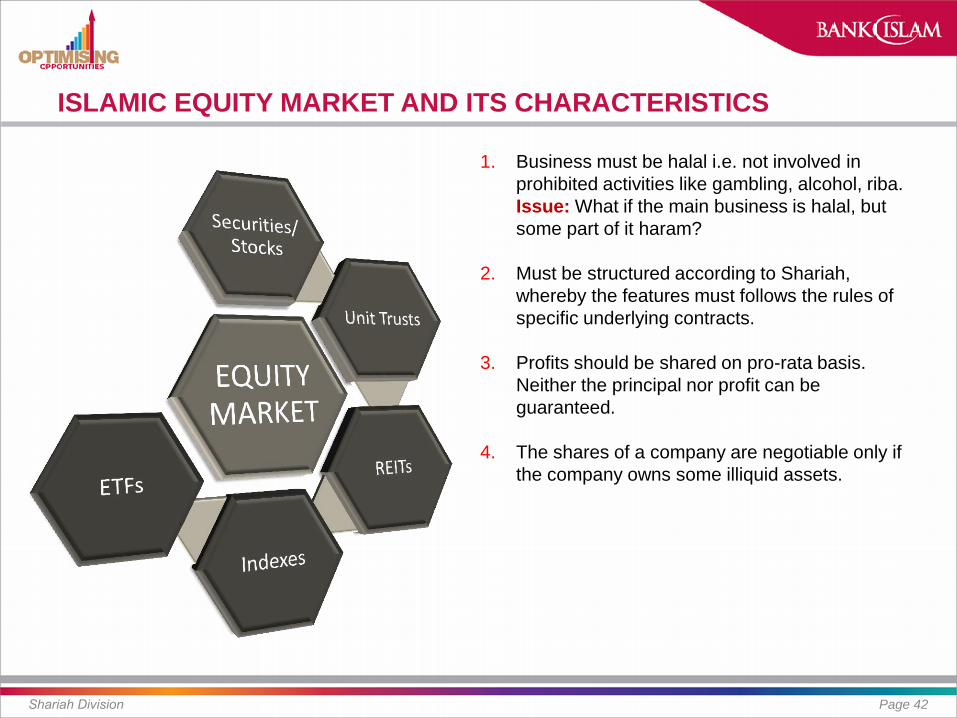

ISLAMIC EQUITY MARKET AND ITS CHARACTERISTICS

Shariah Division Page 42

1. Business must be halal i.e. not involved in

prohibited activities like gambling, alcohol, riba.

Issue: What if the main business is halal, but

some part of it haram?

2. Must be structured according to Shariah,

whereby the features must follows the rules of

specific underlying contracts.

3. Profits should be shared on pro-rata basis.

Neither the principal nor profit can be

guaranteed.

4. The shares of a company are negotiable only if

the company owns some illiquid assets.

1/ SECURITIES - SHARIAH PRINCIPLES IN SHAREHOLDING

Shariah Division Page 43

The share certificate evidences a form of capital

contribution in a company.

The investment in the shares can be in the form of

mudarabah or musharakah.

The shares can be sold at any price as it

represents the assets owned by the company.

The profit for investors can be in the form of

capital profits or dividends or both.

Shariah stock selection must be done to ensure

that companies invested in are only conducting

Shariah compliant activities.

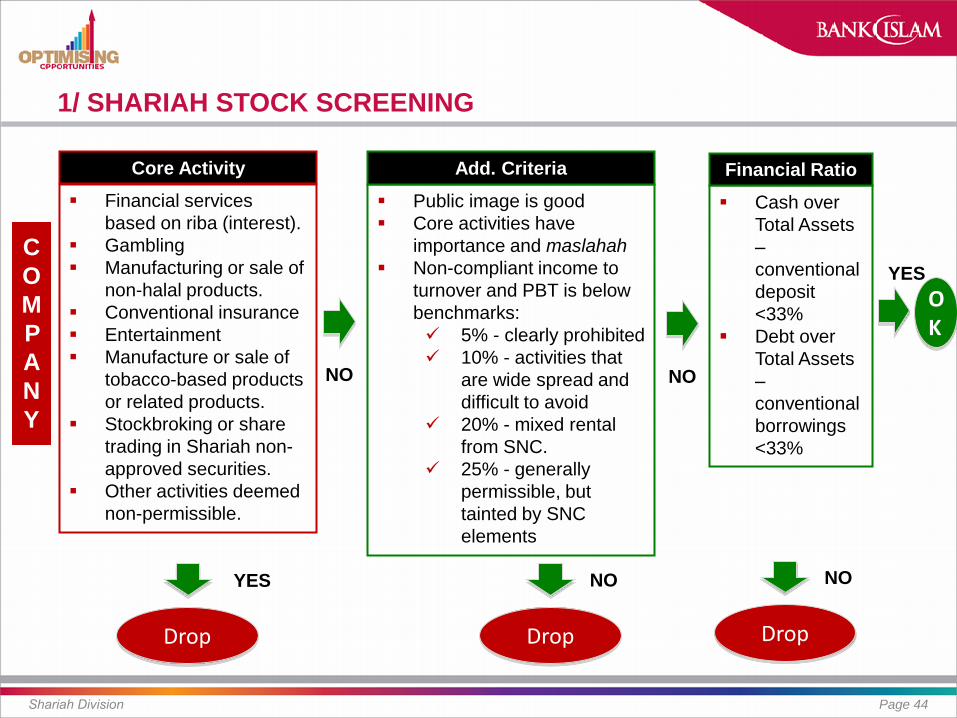

1/ SHARIAH STOCK SCREENING

Shariah Division Page 44

Financial services

based on riba (interest).

Gambling

Manufacturing or sale of

non-halal products.

Conventional insurance

Entertainment

Manufacture or sale of

tobacco-based products

or related products.

Stockbroking or share

trading in Shariah non-

approved securities.

Other activities deemed

non-permissible.

Public image is good

Core activities have

importance and maslahah

Non-compliant income to

turnover and PBT is below

benchmarks:

5% - clearly prohibited

10% - activities that

are wide spread and

difficult to avoid

20% - mixed rental

from SNC.

25% - generally

permissible, but

tainted by SNC

elements

Core Activity Add. Criteria

C

O

M

P

A

N

Y

OK

Drop Drop

YES

NO

NO

YES

Cash over

Total Assets

–

conventional

deposit

<33%

Debt over

Total Assets

–

conventional

borrowings

<33%

Financial Ratio

NO

Drop

NO

Shariah Division Page 45

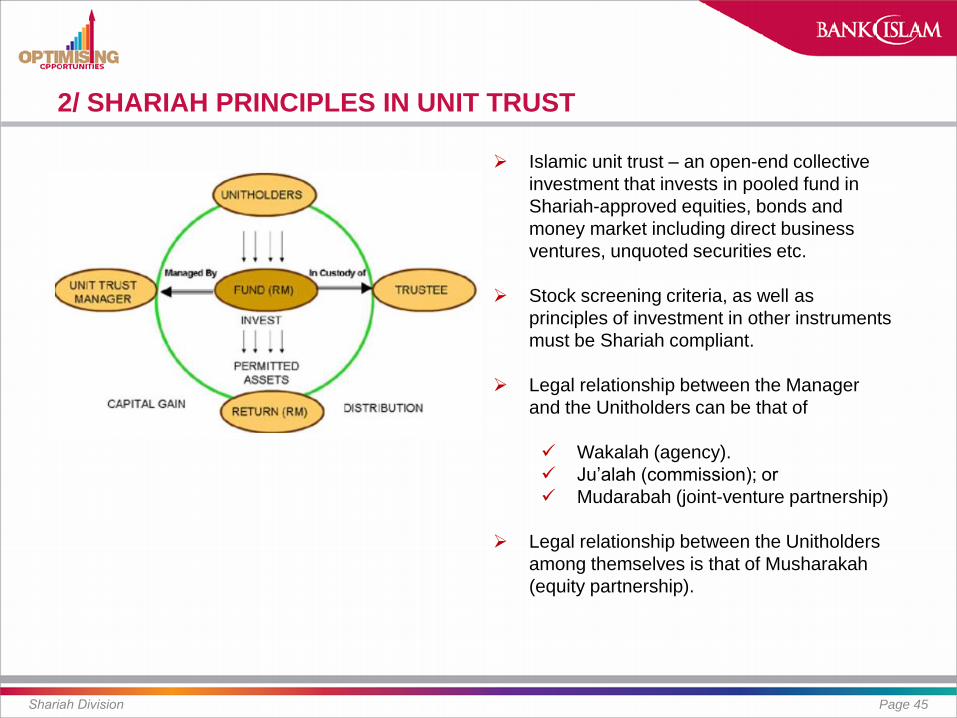

2/ SHARIAH PRINCIPLES IN UNIT TRUST

Islamic unit trust – an open-end collective

investment that invests in pooled fund in

Shariah-approved equities, bonds and

money market including direct business

ventures, unquoted securities etc.

Stock screening criteria, as well as

principles of investment in other instruments

must be Shariah compliant.

Legal relationship between the Manager

and the Unitholders can be that of

Wakalah (agency).

Ju’alah (commission); or

Mudarabah (joint-venture partnership)

Legal relationship between the Unitholders

among themselves is that of Musharakah

(equity partnership).

01/2014 MRCC MEETING Page 46

HAJI MOHD NAZRI CHIK

Pengurus Besar/ Ketua Bahagian Syariah,

Bank Islam Malaysia Berhad

Email: [email protected]

Direct Line: +603-20888052

Mobile: +6019-3380047