abf malaysia bond index fund - malaysiastock.biz name abf malaysia bond index fund (“fund”) ......

TRANSCRIPT

Annual Report for

31 December 2016

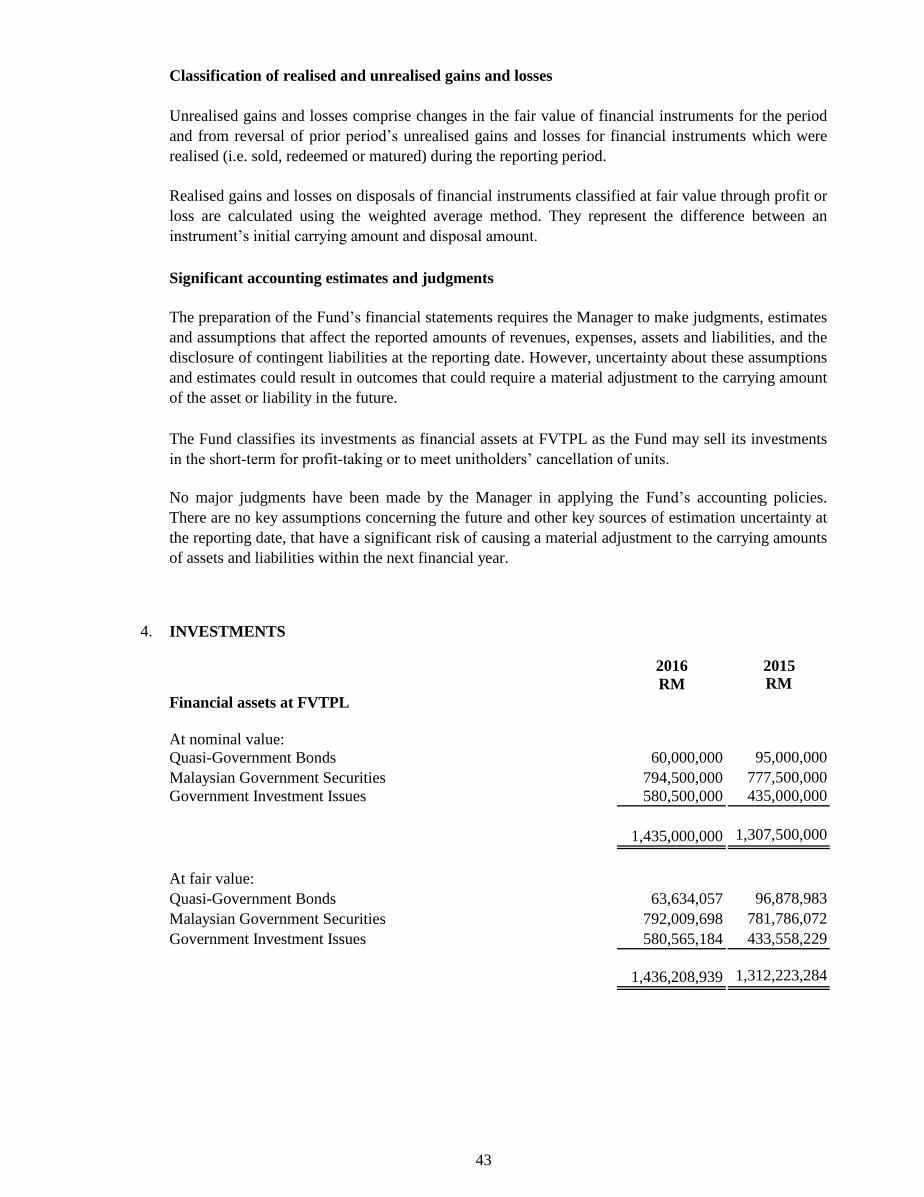

ABF Malaysia Bond Index Fund

ABF Malaysia Bond Index Fund

ABF Malaysia Bond Index Fund

Annual Report

31 December 2016

ABF Malaysia Bond Index Fund

TRUST DIRECTORY

Manager

AmFunds Management Berhad

9th & 10

th Floor, Bangunan AmBank Group

55 Jalan Raja Chulan

50200 Kuala Lumpur

Board of Directors

Pushparani a/p Moothathamby

Mustafa Mohd Nor

Tai Terk Lin

Datin Maznah Mahbob

Sum Leng Kuang

Investment Committee

Sum Leng Kuang

Tai Terk Lin

Mustafa Mohd Nor

Zainal Abidin Mohd Kassim

Datin Maznah Mahbob

Trustee

HSBC (Malaysia) Trustee Berhad

Auditors and Reporting Accountants

Ernst & Young

Taxation Adviser

Deloitte Tax Services Sdn Bhd

ABF Malaysia Bond Index Fund

CORPORATE DIRECTORY

AmFunds Management Berhad

Registered Office

22nd

Floor, Bangunan AmBank Group

55, Jalan Raja Chulan, 50200 Kuala Lumpur

Tel:03-2036 2633 Fax: 03-2032 1914

Head Office

9th & 10

th Floor, Bangunan AmBank Group

55, Jalan Raja Chulan, 50200 Kuala Lumpur

Tel:03-2036 2888 Fax: 03-2031 5210

Secretary

Koh Suet Peng (MAICSA 7019861)

Hafidzah Binti Zakaria (MAICSA 7052802)

22nd

Floor, Bangunan AmBank Group

55, Jalan Raja Chulan, 50200 Kuala Lumpur

HSBC (Malaysia) Trustee Berhad

Business/Registered Office/Head Office

Fund Services, Bangunan HSBC, 13th Floor, South Tower

No.2, Leboh Ampang, 50100 Kuala Lumpur

Tel: 03-2075 7800 Fax: 03-2026 1273

ABF Malaysia Bond Index Fund

CONTENTS

1 Manager’s Report

21 Additional Information

31 Independent Auditor’s Report to the Unitholders

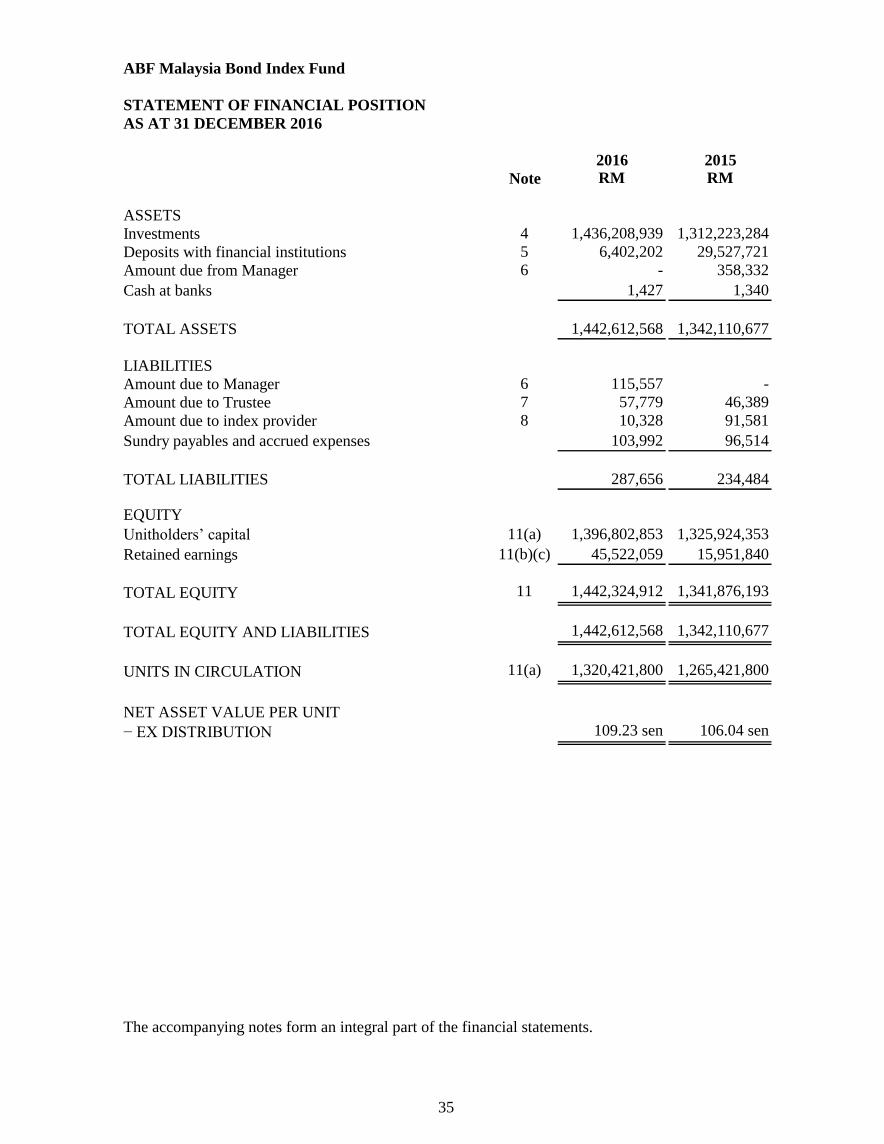

35 Statement of Financial Position

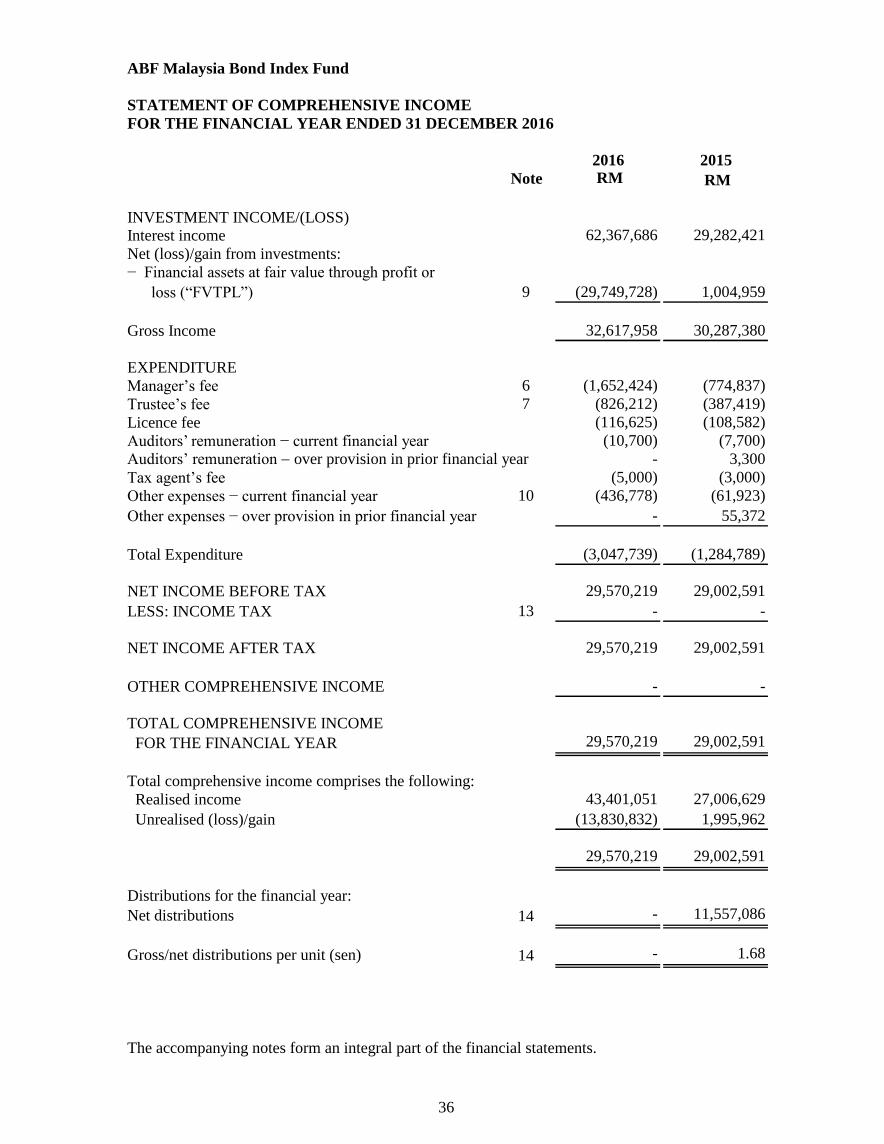

36 Statement of Comprehensive Income

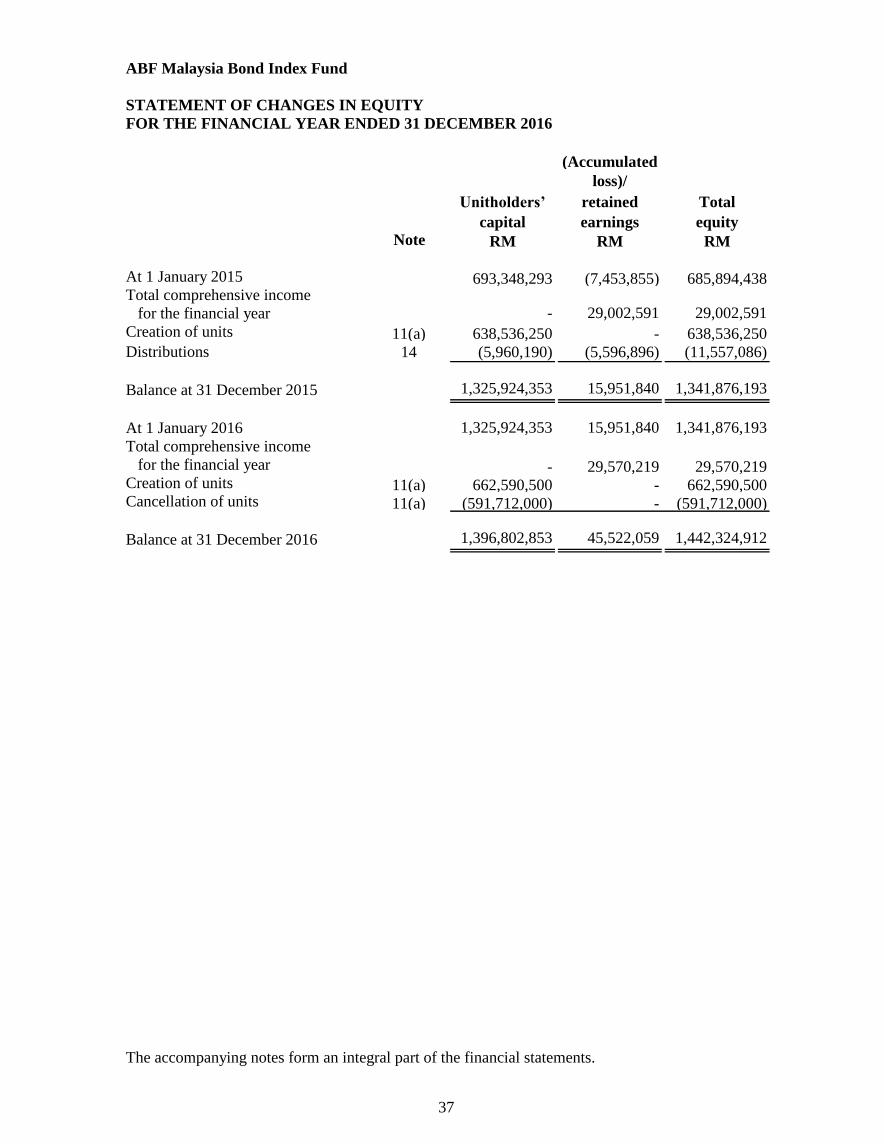

37 Statement of Changes in Equity

38 Statement of Cash Flows

39 Notes to the Financial Statements

59 Statement by the Manager

60 Trustee’s Report

61 Directory

1

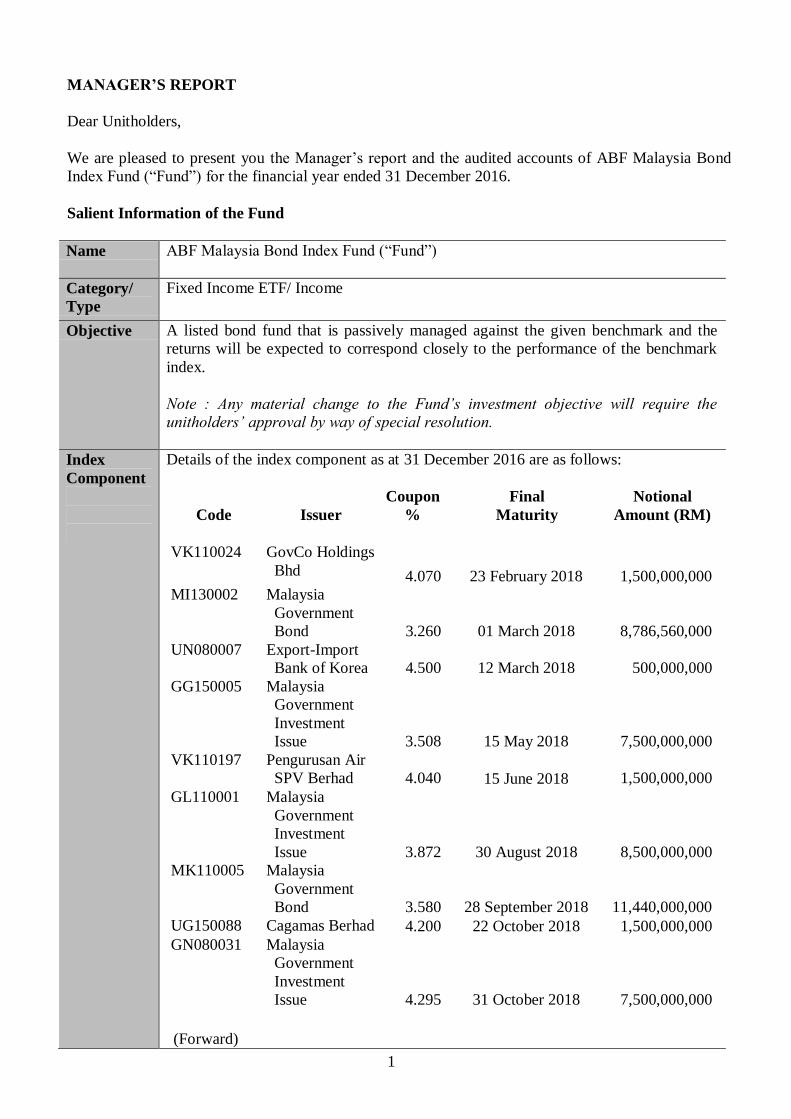

MANAGER’S REPORT

Dear Unitholders,

We are pleased to present you the Manager’s report and the audited accounts of ABF Malaysia Bond

Index Fund (“Fund”) for the financial year ended 31 December 2016.

Salient Information of the Fund

Name ABF Malaysia Bond Index Fund (“Fund”)

Category/

Type

Fixed Income ETF/ Income

Objective A listed bond fund that is passively managed against the given benchmark and the

returns will be expected to correspond closely to the performance of the benchmark

index.

Note : Any material change to the Fund’s investment objective will require the

unitholders’ approval by way of special resolution.

Index

Component

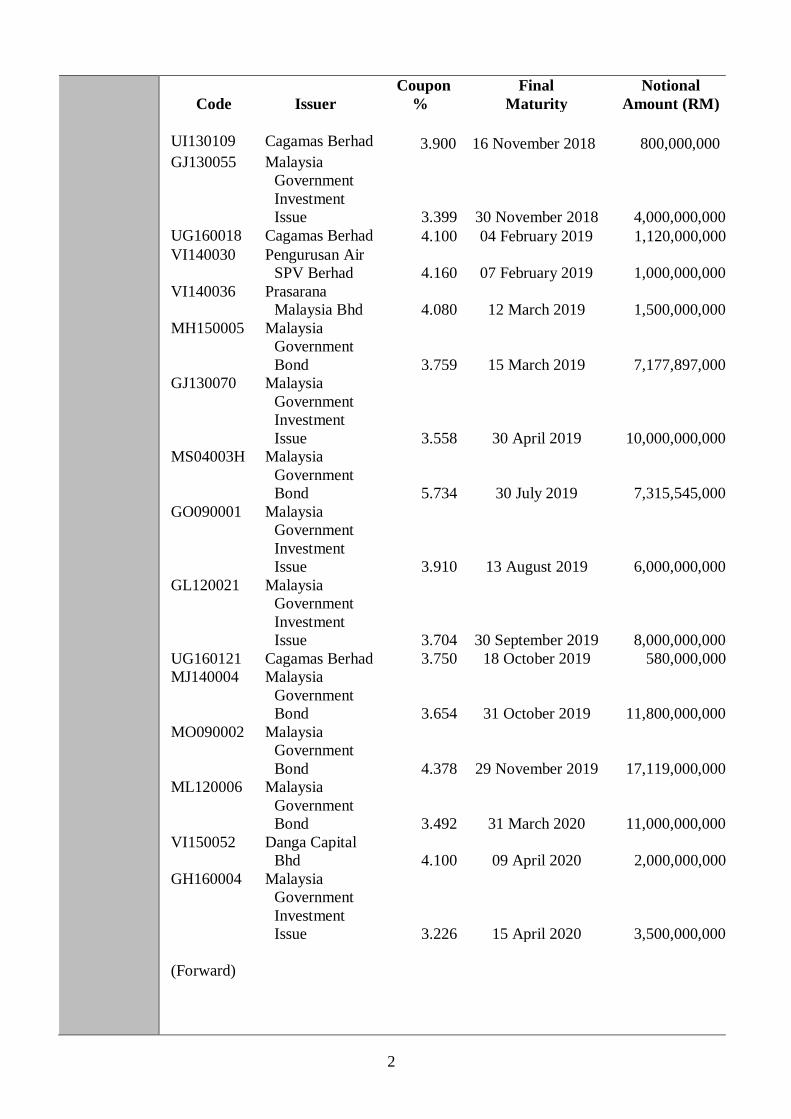

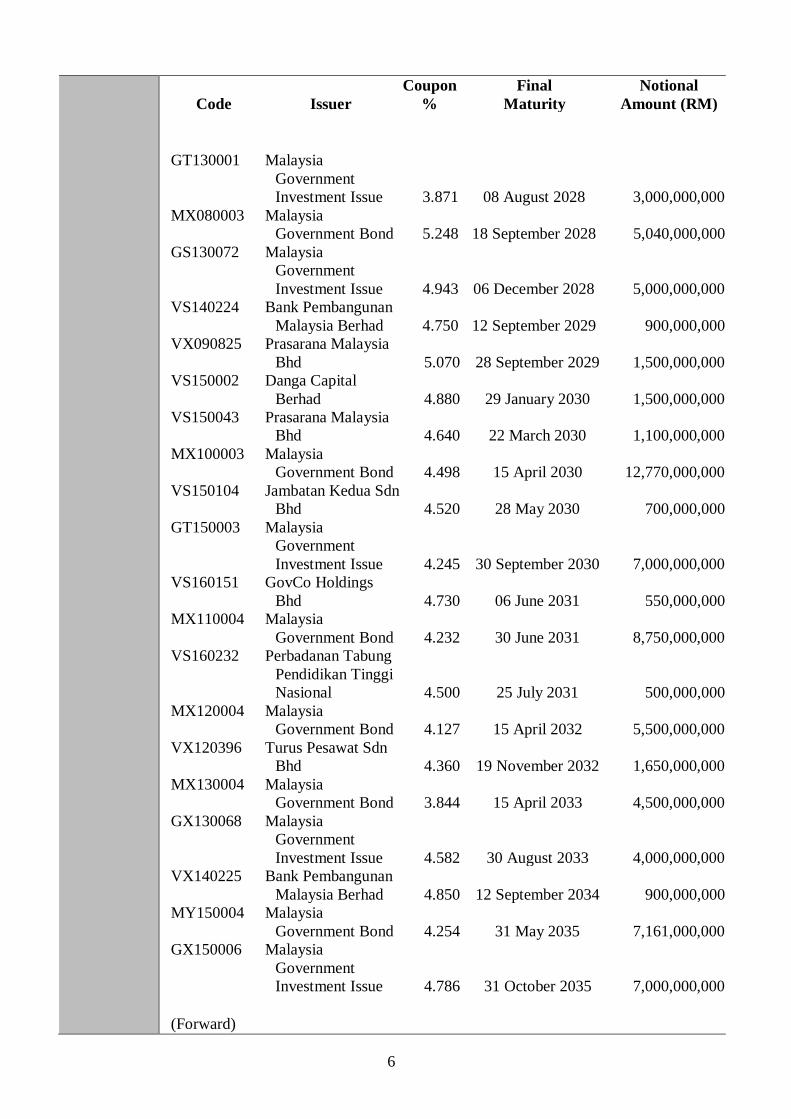

Details of the index component as at 31 December 2016 are as follows:

Code Issuer

Coupon

%

Final

Maturity

Notional

Amount (RM)

VK110024 GovCo Holdings

Bhd 4.070 23 February 2018

1,500,000,000

MI130002 Malaysia

Government

Bond 3.260 01 March 2018

8,786,560,000

UN080007 Export-Import

Bank of Korea 4.500 12 March 2018 500,000,000

GG150005 Malaysia

Government

Investment

Issue

3.508 15 May 2018

7,500,000,000

VK110197 Pengurusan Air

SPV Berhad

4.040 15 June 2018

1,500,000,000

GL110001 Malaysia

Government

Investment

Issue

3.872 30 August 2018

8,500,000,000

MK110005 Malaysia

Government

Bond

3.580 28 September 2018

11,440,000,000

UG150088 Cagamas Berhad 4.200 22 October 2018 1,500,000,000

GN080031 Malaysia

Government

Investment

Issue

4.295

31 October 2018

7,500,000,000

(Forward)

2

Code

Issuer

Coupon

%

Final

Maturity

Notional

Amount (RM)

UI130109 Cagamas Berhad 3.900 16 November 2018 800,000,000

GJ130055 Malaysia

Government

Investment

Issue 3.399 30 November 2018

4,000,000,000

UG160018 Cagamas Berhad 4.100 04 February 2019 1,120,000,000

VI140030 Pengurusan Air

SPV Berhad 4.160 07 February 2019

1,000,000,000

VI140036 Prasarana

Malaysia Bhd 4.080 12 March 2019

1,500,000,000

MH150005 Malaysia

Government

Bond 3.759 15 March 2019

7,177,897,000

GJ130070 Malaysia

Government

Investment

Issue 3.558 30 April 2019

10,000,000,000

MS04003H Malaysia

Government

Bond 5.734 30 July 2019

7,315,545,000

GO090001 Malaysia

Government

Investment

Issue 3.910 13 August 2019

6,000,000,000

GL120021 Malaysia

Government

Investment

Issue 3.704 30 September 2019

8,000,000,000

UG160121 Cagamas Berhad 3.750 18 October 2019 580,000,000

MJ140004 Malaysia

Government

Bond 3.654 31 October 2019

11,800,000,000

MO090002 Malaysia

Government

Bond 4.378 29 November 2019

17,119,000,000

ML120006 Malaysia

Government

Bond 3.492 31 March 2020

11,000,000,000

VI150052 Danga Capital

Bhd 4.100 09 April 2020 2,000,000,000

GH160004 Malaysia

Government

Investment

Issue 3.226 15 April 2020

3,500,000,000

(Forward)

3

Code

Issuer

Coupon

%

Final

Maturity

Notional

Amount (RM)

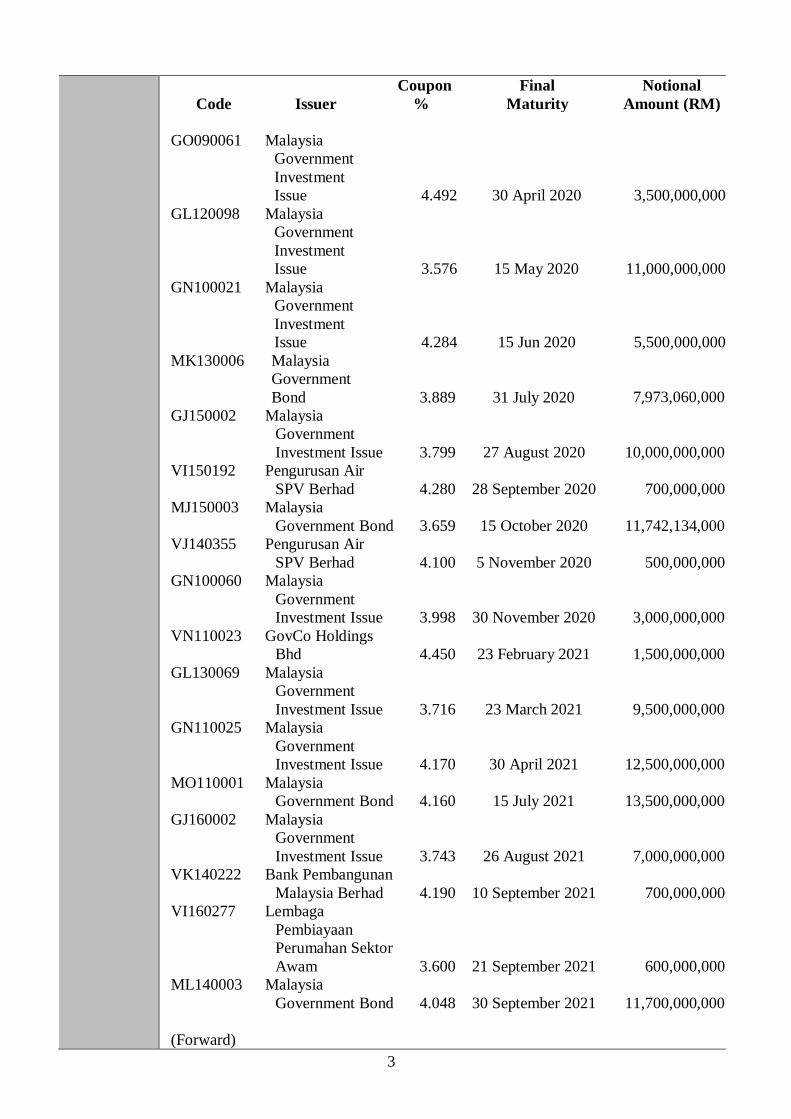

GO090061 Malaysia

Government

Investment

Issue 4.492 30 April 2020

3,500,000,000

GL120098 Malaysia

Government

Investment

Issue 3.576 15 May 2020

11,000,000,000

GN100021 Malaysia

Government

Investment

Issue 4.284 15 Jun 2020

5,500,000,000

MK130006

Malaysia Government

Bond 3.889 31 July 2020

7,973,060,000

GJ150002

Malaysia

Government

Investment Issue 3.799 27 August 2020

10,000,000,000

VI150192

Pengurusan Air

SPV Berhad 4.280 28 September 2020

700,000,000

MJ150003

Malaysia

Government Bond 3.659 15 October 2020

11,742,134,000

VJ140355

Pengurusan Air

SPV Berhad 4.100 5 November 2020

500,000,000

GN100060

Malaysia

Government

Investment Issue 3.998 30 November 2020

3,000,000,000

VN110023

GovCo Holdings

Bhd 4.450 23 February 2021

1,500,000,000

GL130069

Malaysia

Government

Investment Issue 3.716 23 March 2021

9,500,000,000

GN110025

Malaysia

Government

Investment Issue 4.170 30 April 2021

12,500,000,000

MO110001 Malaysia

Government Bond 4.160 15 July 2021

13,500,000,000

GJ160002

Malaysia

Government

Investment Issue 3.743 26 August 2021

7,000,000,000

VK140222

Bank Pembangunan

Malaysia Berhad 4.190 10 September 2021

700,000,000

VI160277

Lembaga

Pembiayaan

Perumahan Sektor

Awam 3.600 21 September 2021

600,000,000

ML140003

Malaysia

Government Bond 4.048 30 September 2021

11,700,000,000

(Forward)

4

Code

Issuer

Coupon

%

Final

Maturity

Notional

Amount (RM)

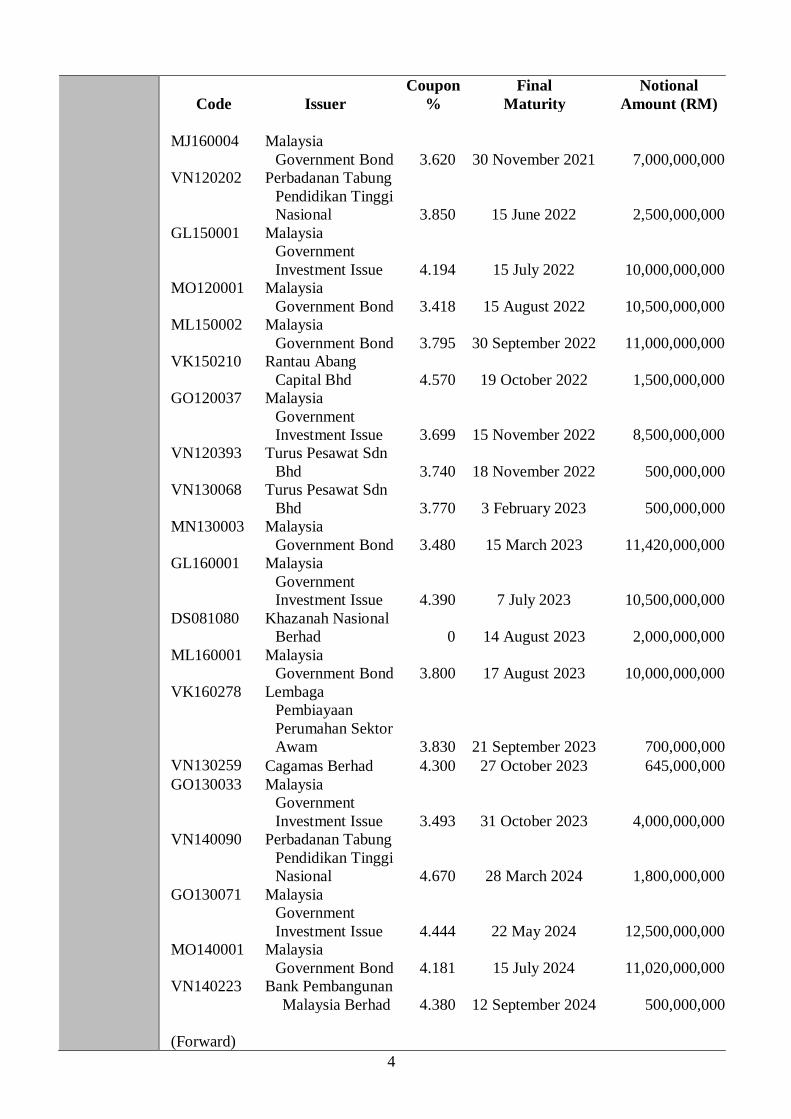

MJ160004 Malaysia

Government Bond 3.620 30 November 2021

7,000,000,000

VN120202

Perbadanan Tabung

Pendidikan Tinggi

Nasional 3.850 15 June 2022

2,500,000,000

GL150001

Malaysia

Government

Investment Issue 4.194 15 July 2022

10,000,000,000

MO120001 Malaysia

Government Bond 3.418 15 August 2022

10,500,000,000

ML150002

Malaysia

Government Bond 3.795 30 September 2022

11,000,000,000

VK150210

Rantau Abang

Capital Bhd 4.570 19 October 2022

1,500,000,000

GO120037

Malaysia

Government

Investment Issue 3.699 15 November 2022

8,500,000,000

VN120393

Turus Pesawat Sdn

Bhd 3.740 18 November 2022

500,000,000

VN130068

Turus Pesawat Sdn

Bhd 3.770 3 February 2023

500,000,000

MN130003

Malaysia

Government Bond 3.480 15 March 2023

11,420,000,000

GL160001

Malaysia

Government

Investment Issue 4.390 7 July 2023

10,500,000,000

DS081080

Khazanah Nasional

Berhad 0 14 August 2023

2,000,000,000

ML160001

Malaysia

Government Bond 3.800 17 August 2023

10,000,000,000

VK160278

Lembaga

Pembiayaan

Perumahan Sektor

Awam 3.830 21 September 2023

700,000,000

VN130259 Cagamas Berhad 4.300 27 October 2023 645,000,000

GO130033

Malaysia

Government

Investment Issue 3.493 31 October 2023

4,000,000,000

VN140090

Perbadanan Tabung

Pendidikan Tinggi

Nasional 4.670 28 March 2024

1,800,000,000

GO130071

Malaysia

Government

Investment Issue 4.444 22 May 2024

12,500,000,000

MO140001

Malaysia

Government Bond 4.181 15 July 2024

11,020,000,000

VN140223

Bank Pembangunan

Malaysia Berhad 4.380 12 September 2024

500,000,000

(Forward)

5

Code Issuer

Coupon

% Final Maturity

Notional

Amount (RM)

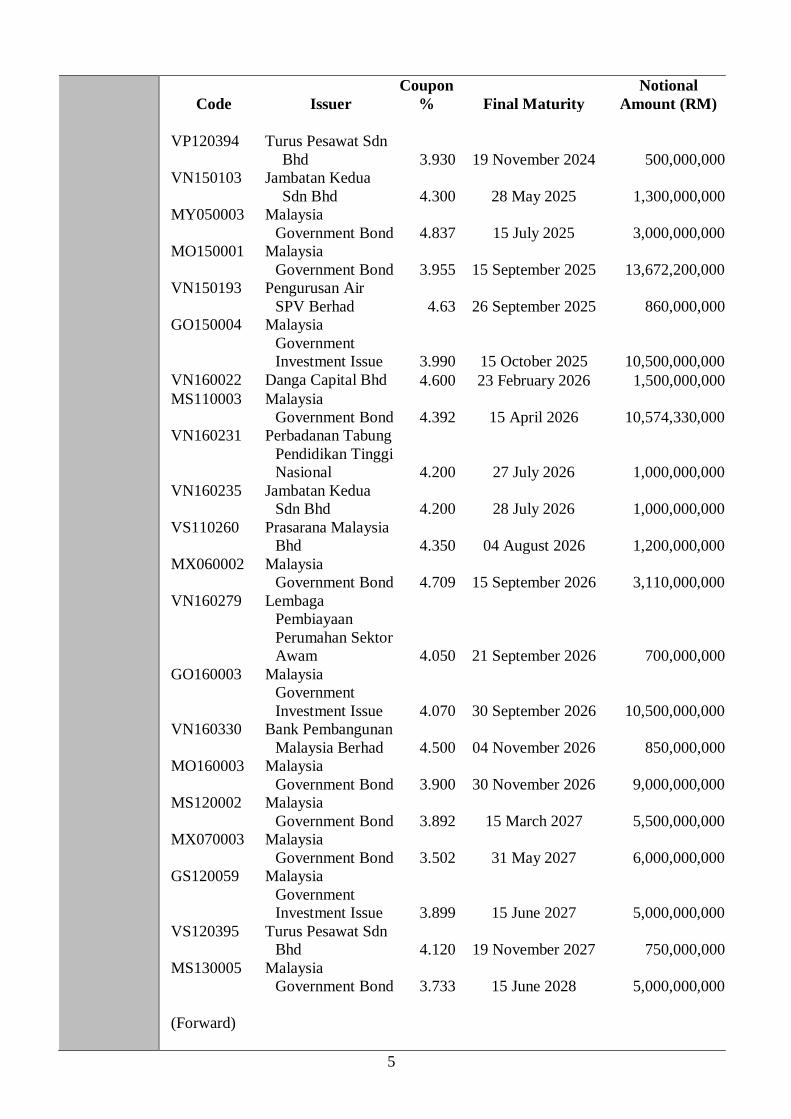

VP120394

Turus Pesawat Sdn

Bhd 3.930 19 November 2024

500,000,000

VN150103 Jambatan Kedua

Sdn Bhd 4.300 28 May 2025 1,300,000,000

MY050003

Malaysia

Government Bond 4.837 15 July 2025

3,000,000,000

MO150001 Malaysia

Government Bond 3.955 15 September 2025

13,672,200,000

VN150193 Pengurusan Air

SPV Berhad 4.63 26 September 2025

860,000,000

GO150004 Malaysia

Government

Investment Issue 3.990 15 October 2025

10,500,000,000

VN160022 Danga Capital Bhd 4.600 23 February 2026 1,500,000,000

MS110003 Malaysia

Government Bond 4.392 15 April 2026

10,574,330,000

VN160231 Perbadanan Tabung

Pendidikan Tinggi

Nasional 4.200 27 July 2026

1,000,000,000

VN160235 Jambatan Kedua

Sdn Bhd 4.200 28 July 2026

1,000,000,000

VS110260 Prasarana Malaysia

Bhd 4.350 04 August 2026

1,200,000,000

MX060002 Malaysia

Government Bond 4.709 15 September 2026

3,110,000,000

VN160279 Lembaga

Pembiayaan

Perumahan Sektor

Awam 4.050 21 September 2026

700,000,000

GO160003 Malaysia

Government

Investment Issue 4.070 30 September 2026

10,500,000,000

VN160330 Bank Pembangunan

Malaysia Berhad 4.500 04 November 2026

850,000,000

MO160003 Malaysia

Government Bond 3.900 30 November 2026

9,000,000,000

MS120002 Malaysia

Government Bond 3.892 15 March 2027

5,500,000,000

MX070003 Malaysia

Government Bond 3.502 31 May 2027

6,000,000,000

GS120059 Malaysia

Government

Investment Issue 3.899 15 June 2027

5,000,000,000

VS120395 Turus Pesawat Sdn

Bhd 4.120 19 November 2027

750,000,000

MS130005 Malaysia

Government Bond 3.733 15 June 2028

5,000,000,000

(Forward)

6

Code Issuer

Coupon

%

Final

Maturity

Notional

Amount (RM)

GT130001 Malaysia

Government

Investment Issue 3.871 08 August 2028

3,000,000,000

MX080003 Malaysia

Government Bond 5.248 18 September 2028 5,040,000,000

GS130072 Malaysia

Government

Investment Issue 4.943 06 December 2028

5,000,000,000

VS140224 Bank Pembangunan

Malaysia Berhad 4.750 12 September 2029

900,000,000

VX090825 Prasarana Malaysia

Bhd 5.070 28 September 2029

1,500,000,000

VS150002 Danga Capital

Berhad 4.880 29 January 2030

1,500,000,000

VS150043 Prasarana Malaysia

Bhd 4.640 22 March 2030

1,100,000,000

MX100003 Malaysia

Government Bond 4.498 15 April 2030

12,770,000,000

VS150104 Jambatan Kedua Sdn

Bhd 4.520 28 May 2030

700,000,000

GT150003 Malaysia

Government

Investment Issue 4.245 30 September 2030

7,000,000,000

VS160151 GovCo Holdings

Bhd 4.730 06 June 2031

550,000,000

MX110004 Malaysia

Government Bond 4.232 30 June 2031

8,750,000,000

VS160232 Perbadanan Tabung

Pendidikan Tinggi

Nasional 4.500 25 July 2031

500,000,000

MX120004 Malaysia

Government Bond 4.127 15 April 2032

5,500,000,000

VX120396 Turus Pesawat Sdn

Bhd 4.360 19 November 2032

1,650,000,000

MX130004 Malaysia

Government Bond 3.844 15 April 2033

4,500,000,000

GX130068 Malaysia

Government

Investment Issue 4.582 30 August 2033

4,000,000,000

VX140225 Bank Pembangunan

Malaysia Berhad 4.850 12 September 2034

900,000,000

MY150004 Malaysia

Government Bond 4.254 31 May 2035

7,161,000,000

GX150006 Malaysia

Government

Investment Issue 4.786 31 October 2035

7,000,000,000

(Forward)

7

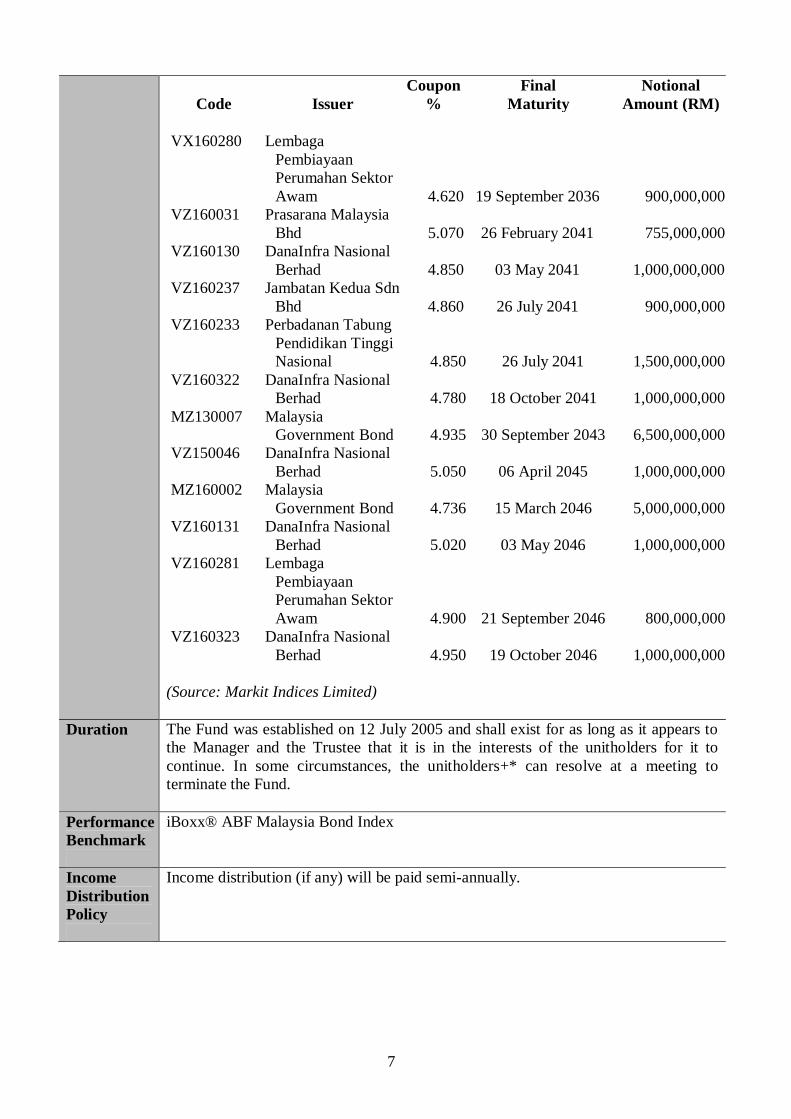

Code Issuer

Coupon

%

Final

Maturity

Notional

Amount (RM)

VX160280 Lembaga

Pembiayaan

Perumahan Sektor

Awam 4.620 19 September 2036

900,000,000

VZ160031 Prasarana Malaysia

Bhd 5.070 26 February 2041

755,000,000

VZ160130 DanaInfra Nasional

Berhad 4.850 03 May 2041

1,000,000,000

VZ160237 Jambatan Kedua Sdn

Bhd 4.860 26 July 2041

900,000,000

VZ160233 Perbadanan Tabung

Pendidikan Tinggi

Nasional 4.850 26 July 2041

1,500,000,000

VZ160322 DanaInfra Nasional

Berhad 4.780 18 October 2041

1,000,000,000

MZ130007 Malaysia

Government Bond 4.935 30 September 2043

6,500,000,000

VZ150046 DanaInfra Nasional

Berhad 5.050 06 April 2045

1,000,000,000

MZ160002 Malaysia

Government Bond 4.736 15 March 2046

5,000,000,000

VZ160131 DanaInfra Nasional

Berhad 5.020 03 May 2046

1,000,000,000

VZ160281 Lembaga

Pembiayaan

Perumahan Sektor

Awam 4.900 21 September 2046

800,000,000

VZ160323 DanaInfra Nasional

Berhad 4.950 19 October 2046

1,000,000,000

(Source: Markit Indices Limited)

Duration The Fund was established on 12 July 2005 and shall exist for as long as it appears to

the Manager and the Trustee that it is in the interests of the unitholders for it to

continue. In some circumstances, the unitholders+* can resolve at a meeting to

terminate the Fund.

Performance

Benchmark

iBoxx® ABF Malaysia Bond Index

Income

Distribution

Policy

Income distribution (if any) will be paid semi-annually.

8

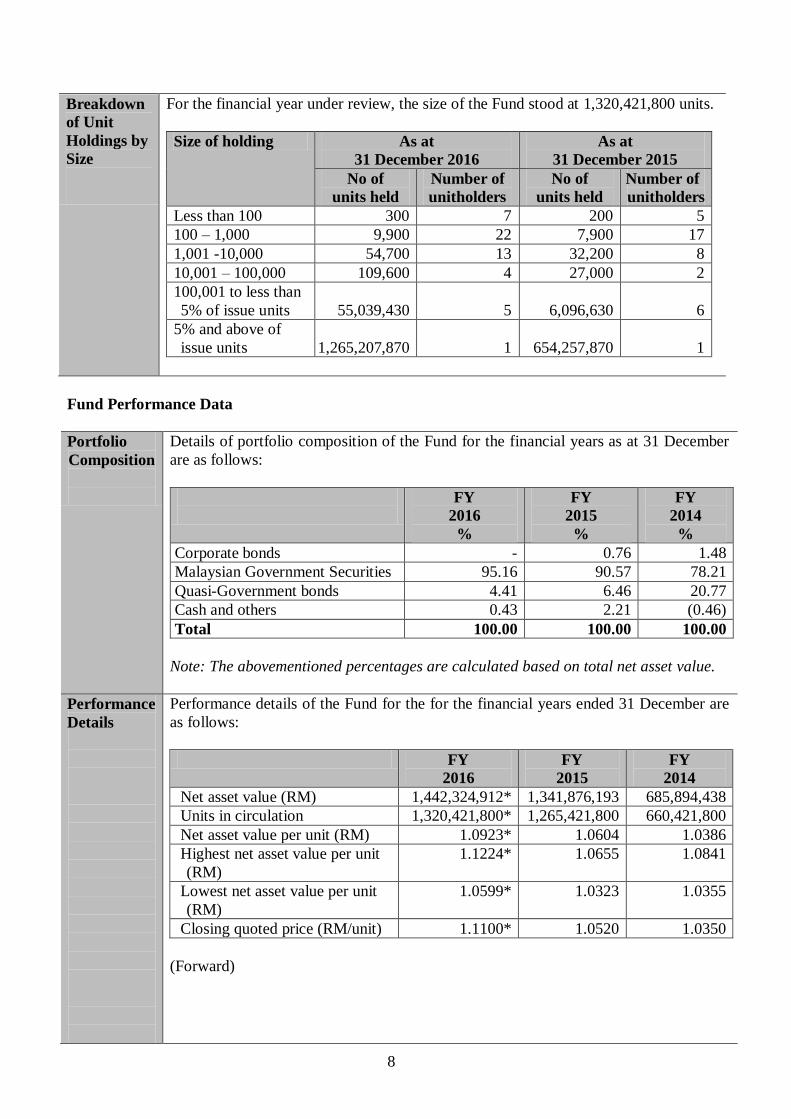

Breakdown

of Unit

Holdings by

Size

For the financial year under review, the size of the Fund stood at 1,320,421,800 units.

Size of holding As at

31 December 2016

As at

31 December 2015

No of

units held

Number of

unitholders

No of

units held

Number of

unitholders

Less than 100 300 7 200 5

100 – 1,000 9,900 22 7,900 17

1,001 -10,000 54,700 13 32,200 8

10,001 – 100,000 109,600 4 27,000 2

100,001 to less than

5% of issue units 55,039,430 5 6,096,630 6

5% and above of

issue units 1,265,207,870 1 654,257,870 1

Fund Performance Data

Portfolio

Composition

Details of portfolio composition of the Fund for the financial years as at 31 December

are as follows:

FY

2016

%

FY

2015

%

FY

2014

%

Corporate bonds - 0.76 1.48

Malaysian Government Securities 95.16 90.57 78.21

Quasi-Government bonds 4.41 6.46 20.77

Cash and others 0.43 2.21 (0.46)

Total 100.00 100.00 100.00

Note: The abovementioned percentages are calculated based on total net asset value.

Performance

Details

Performance details of the Fund for the for the financial years ended 31 December are

as follows:

FY

2016

FY

2015

FY

2014

Net asset value (RM) 1,442,324,912* 1,341,876,193 685,894,438

Units in circulation 1,320,421,800* 1,265,421,800 660,421,800

Net asset value per unit (RM) 1.0923* 1.0604 1.0386

Highest net asset value per unit

(RM)

1.1224* 1.0655 1.0841

Lowest net asset value per unit

(RM)

1.0599* 1.0323 1.0355

Closing quoted price (RM/unit) 1.1100* 1.0520 1.0350

(Forward)

9

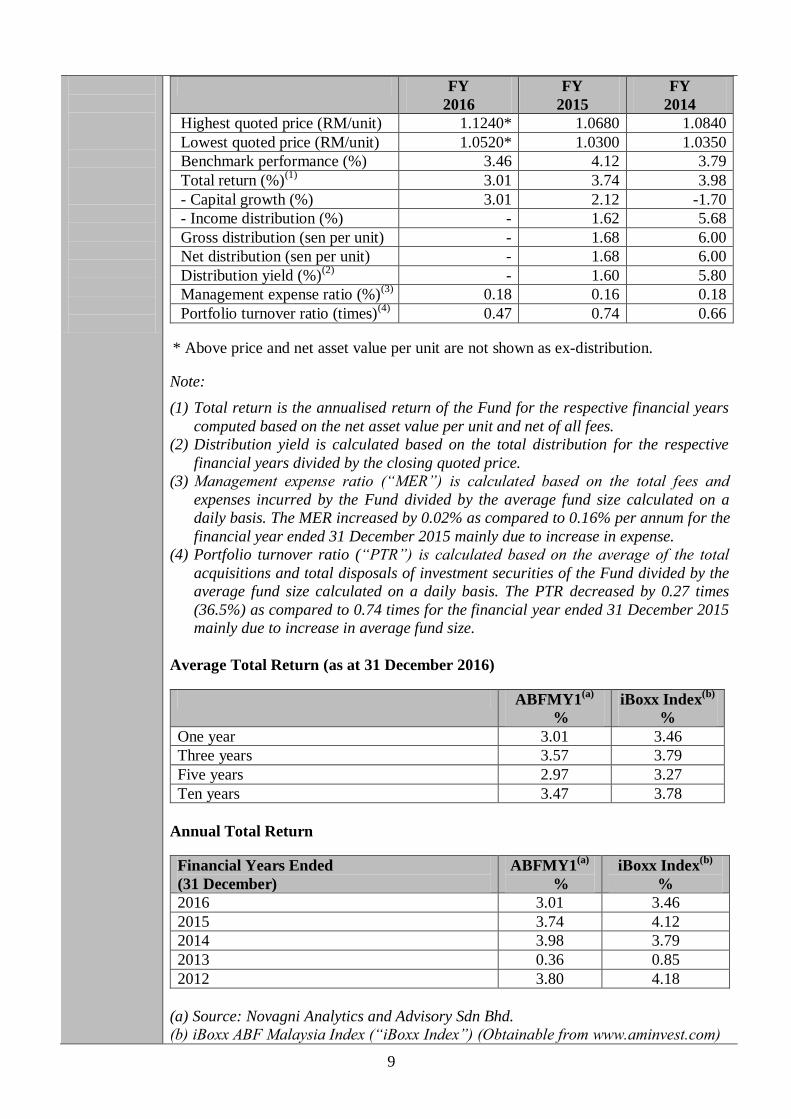

FY

2016

FY

2015

FY

2014

Highest quoted price (RM/unit) 1.1240* 1.0680 1.0840

Lowest quoted price (RM/unit) 1.0520* 1.0300 1.0350

Benchmark performance (%) 3.46 4.12 3.79

Total return (%)(1)

3.01 3.74 3.98

- Capital growth (%) 3.01 2.12 -1.70

- Income distribution (%) - 1.62 5.68

Gross distribution (sen per unit) - 1.68 6.00

Net distribution (sen per unit) - 1.68 6.00

Distribution yield (%)(2)

- 1.60 5.80

Management expense ratio (%)(3)

0.18 0.16 0.18

Portfolio turnover ratio (times)(4)

0.47 0.74 0.66

* Above price and net asset value per unit are not shown as ex-distribution.

Note:

(1) Total return is the annualised return of the Fund for the respective financial years

computed based on the net asset value per unit and net of all fees.

(2) Distribution yield is calculated based on the total distribution for the respective

financial years divided by the closing quoted price.

(3) Management expense ratio (“MER”) is calculated based on the total fees and

expenses incurred by the Fund divided by the average fund size calculated on a

daily basis. The MER increased by 0.02% as compared to 0.16% per annum for the

financial year ended 31 December 2015 mainly due to increase in expense.

(4) Portfolio turnover ratio (“PTR”) is calculated based on the average of the total

acquisitions and total disposals of investment securities of the Fund divided by the

average fund size calculated on a daily basis. The PTR decreased by 0.27 times

(36.5%) as compared to 0.74 times for the financial year ended 31 December 2015

mainly due to increase in average fund size.

Average Total Return (as at 31 December 2016)

ABFMY1(a)

%

iBoxx Index(b)

%

One year 3.01 3.46

Three years 3.57 3.79

Five years 2.97 3.27

Ten years 3.47 3.78

Annual Total Return

Financial Years Ended

(31 December)

ABFMY1(a)

%

iBoxx Index(b)

%

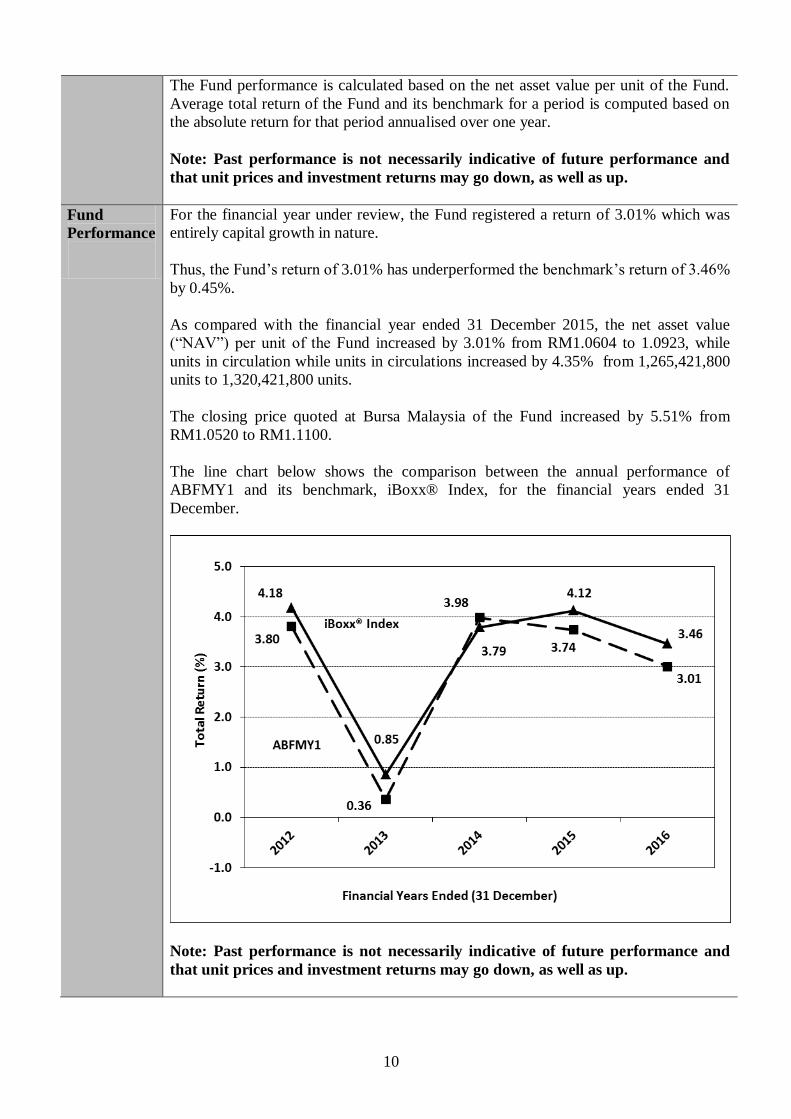

2016 3.01 3.46

2015 3.74 4.12

2014 3.98 3.79

2013 0.36 0.85

2012 3.80 4.18

(a) Source: Novagni Analytics and Advisory Sdn Bhd.

(b) iBoxx ABF Malaysia Index (“iBoxx Index”) (Obtainable from www.aminvest.com)

10

The Fund performance is calculated based on the net asset value per unit of the Fund.

Average total return of the Fund and its benchmark for a period is computed based on

the absolute return for that period annualised over one year.

Note: Past performance is not necessarily indicative of future performance and

that unit prices and investment returns may go down, as well as up.

Fund

Performance

For the financial year under review, the Fund registered a return of 3.01% which was

entirely capital growth in nature.

Thus, the Fund’s return of 3.01% has underperformed the benchmark’s return of 3.46%

by 0.45%.

As compared with the financial year ended 31 December 2015, the net asset value

(“NAV”) per unit of the Fund increased by 3.01% from RM1.0604 to 1.0923, while

units in circulation while units in circulations increased by 4.35% from 1,265,421,800

units to 1,320,421,800 units.

The closing price quoted at Bursa Malaysia of the Fund increased by 5.51% from

RM1.0520 to RM1.1100.

The line chart below shows the comparison between the annual performance of

ABFMY1 and its benchmark, iBoxx® Index, for the financial years ended 31

December.

Note: Past performance is not necessarily indicative of future performance and

that unit prices and investment returns may go down, as well as up.

11

Has the Fund

achieved its

objective?

For the financial year under review, the Fund has met its objective i.e passively

managed against the given benchmark.

Strategies

and Policies

Employed

For the financial year under review, the Fund used a passive strategy whereby the

Manager aims, by way of representative sampling, to achieve a return on the Fund

Assets that closely tracks the returns of the benchmark index.

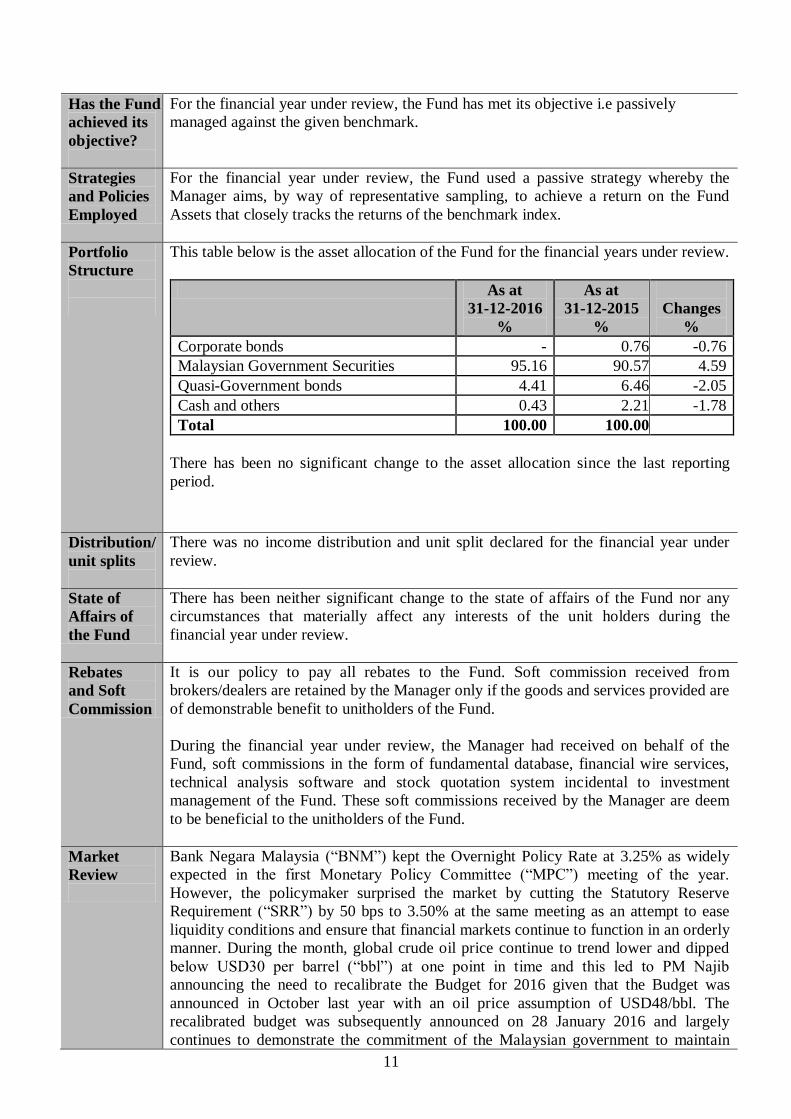

Portfolio

Structure

This table below is the asset allocation of the Fund for the financial years under review.

As at

31-12-2016

%

As at

31-12-2015

%

Changes

%

Corporate bonds - 0.76 -0.76

Malaysian Government Securities 95.16 90.57 4.59

Quasi-Government bonds 4.41 6.46 -2.05

Cash and others 0.43 2.21 -1.78

Total 100.00 100.00

There has been no significant change to the asset allocation since the last reporting

period.

Distribution/

unit splits

There was no income distribution and unit split declared for the financial year under

review.

State of

Affairs of

the Fund

There has been neither significant change to the state of affairs of the Fund nor any

circumstances that materially affect any interests of the unit holders during the

financial year under review.

Rebates

and Soft

Commission

It is our policy to pay all rebates to the Fund. Soft commission received from

brokers/dealers are retained by the Manager only if the goods and services provided are

of demonstrable benefit to unitholders of the Fund.

During the financial year under review, the Manager had received on behalf of the

Fund, soft commissions in the form of fundamental database, financial wire services,

technical analysis software and stock quotation system incidental to investment

management of the Fund. These soft commissions received by the Manager are deem

to be beneficial to the unitholders of the Fund.

Market

Review

Bank Negara Malaysia (“BNM”) kept the Overnight Policy Rate at 3.25% as widely

expected in the first Monetary Policy Committee (“MPC”) meeting of the year.

However, the policymaker surprised the market by cutting the Statutory Reserve

Requirement (“SRR”) by 50 bps to 3.50% at the same meeting as an attempt to ease

liquidity conditions and ensure that financial markets continue to function in an orderly

manner. During the month, global crude oil price continue to trend lower and dipped

below USD30 per barrel (“bbl”) at one point in time and this led to PM Najib

announcing the need to recalibrate the Budget for 2016 given that the Budget was

announced in October last year with an oil price assumption of USD48/bbl. The

recalibrated budget was subsequently announced on 28 January 2016 and largely

continues to demonstrate the commitment of the Malaysian government to maintain

12

fiscal discipline despite the lower oil revenue.

The key takeaways from the recalibrated Budget are as follows:

2016 Gross Domestic Product (“GDP”) growth revise to 4.0 – 4.5% (from 4.0 –

5.0% previously)

Budget based on oil price assumption of USD30-35/bbl

Budget deficit target remains unchanged and maintained at 3.1% of GDP

Operating expenditure to cut by RM4.0b by cutting grants to Government

Linked Companies (“GLCs”) and reducing wastage

Reduction in Employee’s provident Fund (“EPF”) contribution by 3%

Lastly, Moody’s revised Malaysia’s sovereign rating outlook from A3/Positive to

A3/Stable, bringing its view largely in line with the two other major rating agencies

(both at A-/Stable). This is largely to reflect the current external headwinds in the form

of prolonged weakness seen in global crude oil price which will negatively impact the

government’s revenue. Nevertheless, Moody’s highlighted that they continue to view

prior measures taken by the government (such as removal of fuel subsidies and

successful implementation of Goods and Services Tax (“GST”)) to address its fiscal

position as credit positive as it demonstrates the government’s fiscal commitment.

The Malaysian Government Securities (“MGS”) market was fairly active in January as

investors build up positions for the year with total of RM43.3b being traded. Generally,

market sentiment was bullish despite crude oil price dipping below USD30/bbl and

buying interest was seen from both local and offshore investors. As a result, the MGS

yield curve bullish flattened during the month in tandem with the huge rally in

USDMYR which closed at 4.15 at end January 2016 from 4.29 in end December 2015.

In the primary market, three tenders were offered: (1) RM4.0b new issue of Malaysian

Government Investment Issue (“MGII”) 07/23, which drew strong bid-to-cover

(“BTC”) ratio of 2.68x with an average yield of 4.39%; (2) RM3b MGS 03/19

reopening, which drew healthy BTC ratio of 2.058x with an average yield of 3.271%

and; (3) RM2b Government Investment Issue (“GII”) 10/35 reopening, which

registered a decent BTC of 1.915x at an average yield of 4.647%. With these three

tenders, the year-to-date (“YTD”) MGS/GII issuance stood at RM9.0b at as end

January 2016.

During the month of February, Malaysia reported that 4Q2015 GDP grew by 4.5% thus

bringing overall GDP growth for the year to 5.0% and handily beating consensus

forecast of 4.1% for 4Q2015 and 4.8% for 2015. As expected, the outperformance

continued to be led by the resilience in Malaysia’s private consumption growth and a

rebound in exports especially the manufacturing sector. Meanwhile, Malaysia’s

Consumer Price Index (“CPI”) climbed to 3.5% Year-over-year (“YoY”) in Jan 16

(Dec 15: 2.7%). On a Month-over-month (“MoM”) basis, the index contracted by 0.3%

indicating an easing in domestic price pressure on the back of moderating domestic

demand. On the job front, Malaysia's unemployment rate continues to inch higher,

rising to 3.3% in December from 3.2% in the previous month and 3.0% a year ago. The

number of unemployed people climbed to 478,100 in December from 453,300 in

November 432,100 a year ago. The labor force participation rate came in at 67.8%, up

from 67.7% in November. On the commodities front, crude oil price has been

averaging around USD30 to USD35 per barrel as concerns of an oversupplied market

remains. Mirroring the volatility in oil prices, Malaysia’s Ringgit has also been trading

around a tight range of around USD/MYR of RM4.10 to RM4.25. Finally, Fitch

Ratings is keeping Malaysia’s rating at A- with Stable outlook as external liquidity

13

position deteriorated due to large capital outflows and loss of forex reserves.

Nevertheless, Fitch Ratings also mentioned that Malaysia’s liquidity, (as measured by

Fitch’s broader external liquidity metric) still remains above the “A” median.

Despite a shorter trading month, trading in the MGS/GII market was brisk with a total

of RM67.0b value recorded. After the bullish sentiment in January where we saw

active buying by both local and foreign funds, some of the investors probably took

some profit in February especially in the short to mid end of the curve. Overall, the

yields on the 3-year, 5-year, 7-year, 10-year, 15-year, 20-year and 30-year close at

3.30%, 3.58%, 3.72%, 3.95%, 4.25%, 4.45% and 4.75% respectively. In the primary

market, only two tenders were offered: (1) RM4.0b new issue of MGS 08/23, which

drew the lowest BTC ratio of the year at 2.85x with an average yield of 3.80% and; (2)

RM3.5b new issue of GII 08/21, which registered a very strong BTC of 2.85x at an

average yield of 3.743%.

In the month of March BNM kept the OPR (“Overnight Policy Rate”) unchanged at

3.25% as expected and also left the SRR ratio at 3.50% in the second MPC meeting of

the year. The tone of the MPC statement remained broadly similar to the previous MPC

statement as BNM continues to highlight global growth vulnerability to “downside

risks arising from prevailing fragilities that are both cyclical and structural, excessive

leverage, the sharp declines in commodity prices and the rising geopolitical risks.”

BNM released its Annual Report for 2015, highlighting its expectations of slower

domestic growth, which is projected to grow by 4.0 – 4.5% in 2016 primarily driven by

domestic demand and sustained mainly through private consumption. Meanwhile,

inflation is expected to range between 2.5 – 3.5% in 2016. Separately, it was also the

first time BNM released information on the composition of foreign holdings in

MGS/GII and the breakdown is as follows:

Asset Managers: 44%

Central Banks / Governments: 29%

Pension Funds: 13%

Banks:10%

Insurance Companies: 2%

Nominees / Custodians: 1%

Others: 1%

Lastly, S&P affirmed Malaysia’s A-/Stable rating premised on its expectations that the

1 Malaysia Development Berhad (“1MDB”) issues and the upcoming change in BNM

leadership will not diminish the effectiveness of policymaking either in the executive

branch or at the central bank. S&P also believes the government has taken sufficient

offsetting measures to compensate for lost hydrocarbon-related fiscal revenue. In

addition, the country's strong external position and fairly diverse economy can absorb

some weakness in the oil and gas sector.

In March, the MGS yield curve continued its bullish flattening stance as investor

sentiment improved drastically following Fed Chair Janet Yellen’s guidance of a more

cautious and gradual approach to interest rate hike cycle. This coupled with the

stabilization of global commodity prices led the recovery seen in the USD/MYR which

closed at 3.90 at the end of the month. Against the more positive backdrop, trading

volume jumped higher with a total of RM76.6b traded compared to RM67.0b in the

previous month. Overall, the yields on the 3-year, 5-year, 7-year, 10-year, 15-year, 20-

year and 30-year close at 3.22%, 3.45%, 3.67%, 3.82%, 4.15%, 4.37% and 4.69%

14

respectively. In the primary market, there were three tenders: (1) RM2.5b new issue of

MGS 03/46, which drew strong BTC ratio of 2.596x with an average yield of 4.736%;

(2) RM4b new issue of GII 9/26, which a registered a very strong BTC ratio of 3.2x

with an average yield of 4.07%; and (3) RM2.5b re-opening of MGS 06/31, which

garnered BTC ratio of 2.37x with an average yield of 4.20%.

In the month of April, Malaysia released its February exports number, which

rebounded 6.7% YoY. The increase was generally driven by electrical and electronics

(E&E”) sector as well as increase in palm oil and palm-based and timber and timber

based products. On the inflation front, Malaysia’s CPI for March came in much weaker

than expected at 2.6% YoY against consensus expectations of 3.4%. The drop was due

to lower transport cost as RON95 petrol price was reduced by 15 sen to RM1.60 per

litre in March 2016 from RM1.75 in February. Meanwhile, BNM said that the

reduction of the SRR by 50 basis points on 1 February 2016 has had its desired impact

on the banking system’s interbank rates. The base rate of commercial banks, on

average, remained relatively stable at 3.89% in March (February: 3.88%). On the

consumer sentiment front, 1Q16 Consumer Sentiment Index (“CSI”) has rebounded to

72.9 points after plunging for six consecutive quarters. Recall that the index had hit its

all-time lows in the past two quarters, falling to 63.8 in 4Q15. In April, BNM’s

international reserves continue to climb steadily and were last seen at USD97b as at

end-March 2016. More pertinently, foreign holdings in Malaysian bonds of RM226.6b

as at end March has broken the previous record set in November 2014. Strengthening

crude oil prices and foreign fund inflows in both the bond as well as equities market

has help turned the Ringgit into Asia’s best-performing currency, confounding some

analyst’s expectation. The Ringgit has surged around 10% as at end April, the most in

43 years.

In April, the MGS yield curve bearish flattened with most of the selling occurring

towards the last week of the month. Trading volume dipped to RM71.6b compared to

RM76.6b in the previous month. Overall, the yields on the 3-year, 5-year, 7-year, 10-

year, 15-year, 20-year and 30-year close at 3.30% (March: 3.22%), 3.54% (March:

3.45%), 3.75% (March: 3.67%), 3.94% (March: 3.82%), 4.17% (March: 4.15%),

4.32% (March: 4.37%) and 4.67% (March: 4.69%) respectively. In the primary market,

there were three tenders: (1) RM3.5b re-opening of GII 07/23, which drew BTC ratio

of 2.686x with an average yield of 3.932%; (2) RM2.5b re-opening of MGS 05/35,

which a registered a fairly lackluster BTC ratio of 1.986x with an average yield of

4.24%; and (3) RM3.0b re-opening of MGS 08/23, which garnered BTC ratio of

2.044x with an average yield of 3.80%.

In May, BNM kept the OPR and SRR ratio unchanged at 3.25% and 3.50%

respectively as widely expected in Datuk Muhammad Ibrahim’s inaugural MPC

meeting as BNM Governor. The tone of the MPC statement was largely neutral with

the stance broadly similar to the previous MPC statements. BNM also reiterated its

expectations for the domestic economy to expand by 4.0 – 4.5% in 2016 while inflation

is expected to trend lower for the remaining parts of the year from the average CPI of

3.4% in the first quarter of 2016 (“1Q16”). This followed the release of Malaysia’s

1Q16 GDP data which grew at a slower pace of 4.2% YoY, on the back of weakness in

exports and soft private investment growth while on a quarter to quarter basis, the

domestic economy grew 1.0%, compared to 1.5% previously.

The MGS market saw some sell-off following the release of US Fed Federal Open

Market Committee (“FOMC”) April meeting minutes which indicated that members

are looking at potentially raising interest rate in its June FOMC meeting while Fed

15

Chair Janet Yellen signaled in a speech that that a rate increase would be appropriate in

the coming months if the US economy and labour market continue to strengthen. The

hawkish tone by the Fed sent MGS yields higher across all tenures, resulting in the

shift upward in the MGS yield curve. Trading volume for the month fell to RM69.2b

from RM71.6b in the previous month. Overall, the yields on the 3-year, 5-year, 7-year,

10-year, 15-year, 20-year and 30-year close at 3.30%, 3.56%, 3.84%, 3.92%, 4.21%,

4.35% and 4.71% respectively. In the primary market, there were three tenders: (1)

RM2.5b 15-year reopening of MGS 09/30, which drew healthy BTC ratio of 2.621

times with an average yield of 4.417%; (2) RM4.0b 10.5-year new issue of MGS 11/26

garnered BTC ratio of 2.193 times at average yield of 3.90%; and (3) RM4.0b 5.5-year

new issue of MGS 11/21 drew a weak BTC ratio of 1.42 times at average yield of

3.62%.

During the month of June, Malaysia reported a positive growth in exports of 1.6% YoY

for the month of April 2016, while imports contracted by 2.3%, thus leaving a positive

trade balance of RM9.1b. Main contributors to exports came from the E&E sector

which showed an encouraging growth of 2.1% versus 0.5% in the preceding month. On

the inflation front, May’s CPI eases marginally to 2.0% YoY matching market

expectations. Since the implementation of GST in April 2015, the initial price shock

has faded while the current record low pump prices continue to keep inflationary

pressure in check. Meanwhile, Malaysia’s unemployment rate continued to inch up in

April. At 3.6%, the unemployment figure is at the highest since 2010. Finally,

Malaysia’s Ringgit appreciated versus USD by 2.9% from RM4.15 to RM4.03 at as

end June. The Ringgit has been volatile in June primarily due to two key events, the

FOMC meeting as well as the UK Referendum on Brexit.

In contrast to the month of May, the MGS curve bull-flattened as trading volume for

the month of June soared to RM106.2b from RM69.2b in the previous month. The

strong rally was probably contributed by two significant events during the month: (1) a

weak May NFP figure which delayed the much anticipated Fed rate hike in the June

FOMC meeting and (2) Brexit which triggered fears of global economic slowdown. As

both events were bond positive, it’s not a surprised that yields fell across the curve.

Overall, 3-year, 5-year, 7-year, 10-year, 15-year, 20-year and 30-year close at 3.17%,

3.32%, 3.59%, 3.73%, 4.08%, 4.29% and 4.62% respectively. In the primary market,

there were two tenders: (1) RM3.5b 10-year reopening of GII 09/26, which drew

healthy bid-to-cover (“BTC”) ratio of 2.308 times with an average yield of 4.049%;

and (2) RM2.5b 30-year reopening of MGS 03/46 which garnered BTC ratio of 2.369

times at average yield of 4.613%.

In July, BNM cut the OPR by 25bps to 3.00% at its 13 July 2016 meeting. The market

was surprised with consensus expectation that the policy rate would be left unchanged.

BNM sees that it has policy room for easing due to subdued inflation, and has also

revised down the 2016 inflation expectation to 2-3% from 2.5-3.5% previously. The

rate cut is aimed at supporting domestic growth, given that the financial sector is not

expected to be destabilized by the lower policy rate. Malaysia’s inflation came in

significantly below expectations at 1.6% YoY for June 2016 mainly due to transport

prices which contracted -8.5%YoY that is weighted 13.7% of the CPI.

Subsequent to the unexpected OPR cut, the MGS market rallied across the curve even

as trading volume for the month of July dropped from June’s year to date high of

RM106.2b to RM80.8b. The stellar performance over the past two months was not

unexpected as not only has the U.S. Federal Reserve Bank held back the anticipated

rate hike back in June but global central banks including Malaysia seems to on the

16

dovish path ever since the U.S. Federal Reserve Bank meeting as well as the event of

Brexit. Overall, 3-year, 5-year, 7-year, 10-year, 15-year, 20-year and 30-year close at

2.99%, 3.17%, 3.38%, 3.59%, 3.92%, 4.21% (Jun: 4.29%) and 4.53% respectively. In

the primary market, there were two tenders: (1) RM2.5b 15-year reopening of MGS

06/31, which drew healthy BTC ratio of 2.222 times with an average yield of 3.856%;

and (2) RM3.5b 5-year reopening of GII 08/21 which garnered BTC ratio of 2.454

times at average yield of 3.401%.

During the month of August, Malaysia exports bounced back into gain of 3.4% y-o-y

in June after falling by -0.9% in May and compared with +1.6% in April. Meanwhile,

the foreign exchange reserves increased marginally by USD0.1b to USD97.3b as at 29

July 2016. The current account surplus in the balance of payments narrowed to

MYR1.9bn in 2Q 2016, after recording a surplus of MYR5.0bn in 1Q and compared

with a surplus of MYR8.1bn in 2Q 2015. This was attributed to a smaller surplus in the

merchandise trade account and a larger deficit in the income transfers. Meanwhile, the

financial account registered a higher net inflow of MYR9.5bn in 2Q, compared with an

inflow of MYR5.8bn in the previous quarter. The improvement was mainly due to a

rebound in net inflow on other investments and a larger net inflow of direct

investments. On the other hand, the slowdown in the Malaysian economy continued

with real GDP growing at a slower pace of 4.0% YoY in 2Q 2016, from +4.2% in 1Q

and +4.5% in 4Q 2016. The overall growth was dragged lower by a cutback in

inventories and subdued exports. CPI rose just at 1.1% in July 2016, as opposed to

1.6% in the prior month and against consensus of 1.2%. The low CPI rate has

prompted some market players to anticipate BNM to revise the OPR downward at the

next policy meeting.

The rallies in the Malaysian sovereign bonds/sukuk continued in August, following

BNM’s OPR cut by 25 bps to 3.0%. Some of the gains were pared after the BNM

governor stated that there were no plans for a series of rate cuts. Depressed global

yields and divided Fed officials as highlighted in the U.S. July FOMC minutes led to

sell-down of USD and strengthening of MYR. Yields of the local government bonds

shifted down across the board due to global yield hunting. Oil strength during the

month wherein the Brent crude oil closed above USD50.00 per barrel since 4 July 2016

also contributed to the local bond market rallies. On 17 August 2016, there was an

announcement that GII will be eligible for inclusion in the JP Morgan Emerging

Market (“JPM EM”) suite of indices i.e. Government Bond Index – Emerging Market

(“GBI-EM”) Global Diversified and GBI-EM Diversified. This sparked a significant

rally for the GII, particularly GII 7/23 and GII 9/26.The spread between the MGS and

GII has compressed significantly pre and post the announcement. The 7 year GII-MGS

spread has compressed from 14 bps to the current 4-5bps whereas the 10 year GII-

MGS has compressed from 19 bps to the current 5 bps. However, toward the end of the

month, several Fed officials made hawkish statement about raising fed rates possibly as

early as in September. Janet Yellen, The Fed Chair also remarked at the Monetary

Policy Meeting at Jackson Hole, Wyoming that the case for the rate hike has

strengthened, but she did not specify the timing of the rate hike as it will be data

dependent. This had caused the local market government bonds to weaken as traders

were seen trimming down their positions.

Overall, 3-year, 5-year, 7-year, 10-year, 15-year, 20-year and 30-year close at 2.895%,

3.19%, 3.465%, 3.60%, 3.915%, 4.13% and 4.45% respectively. In the primary market,

there were three tenders: (1) RM3.0b 7-year reopening of MGS 8/23 with BTC ratio of

1.577 times with average yield of 3.483 (2) RM3.0b 15-year reopening of MGII 09/30,

which drew strong BTC ratio of 2.493 times with an average yield of 4.160%. Demand

17

predominantly came from local banks, Islamic real money, life and pension funds that

are heavy cash-in-hand; and (3) RM3.0b 10-year reopening of MGS 11/26 which

garnered weak BTC ratio of 1.752 times at average yield of 3.563%.

Malaysia’s Purchasing Manager’s Index (“PMI”) reading rose to 48.6 in September

from 47.4 in August 2016. This marked the highest reading in eight months.

Nevertheless, it was still the eighteenth consecutive month of contraction as indicated

by the sub 50 reading. On the inflation front, headline inflation reading for August

rebounded to 1.5% versus consensus expectation of 1.3%. Main drivers were non-food

items particularly cultural services which saw inflation surging from 1.0% in July to

6.1% YoY in August. Finally, the banking sector’s loan growth moderated for the

twelfth consecutive month to 4.2% YoY in August from 5.1% YoY in July. Notably,

this is the lowest level in at least 13 years, as lending activities continue to face

headwinds from a slowing economy, tepid deposit growth and rising loan impairments.

Global markets revisited the prospect of a rate hike again as the FOMC met over two

days starting 20 Sep 2016. As expected, volatility spiked in the run-up to the meeting

as yields rose across the board globally as well as in Malaysia. The less than hawkish

decision post FOMC was well anticipated by the market and hence saw a reversal in

bond yields. Likewise, Malaysian Government bonds also saw yields declined in

response to the Fed’s decision and ended the month in a slight flattening of the curve.

Overall, 3-year, 5-year, 7-year, 10-year, 15-year, 20-year and 30-year close at 2.94%,

3.22%, 3.44%, 3.54%, 3.92%, 4.15% and 4.47% respectively. In the primary market,

there were two tenders: (1) RM3.0b 5-year Re-opening of MGS 11/21, which drew a

weak BTC ratio of 1.670 times with an average yield of 3.256%; and (2) RM2.0b 20-

year Re-opening of GII 10/35 which garnered BTC ratio of 2.890 times at average

yield of 4.226%.

In October, Malaysia reported its foreign exchange reserves rose by USD0.2bn to

USD97.7bn as at 30 September 2016, from USD97.5bn registered at end-August and

compared to USD95.3bn at end-December 2015. On the inflation front, the headline

inflation rate remained stable in September, as the easing in cost of food and beverages

was mitigated by the smaller magnitude of decline in cost of transport. The core

inflation rate inched lower in September. Growth of the broader money supply, M3,

slowed to 2.2% year-on-year (y-o-y) in September, from +2.4% in August, due to a

decline in external operations and a slowdown in demand for funds by the private and

public sector. Meanwhile, loan growth was stable at 4.2% y-o-y in September,

unchanged from the previous month but lower compared with +5.6 in July, as the

deceleration in growth of household loans were mitigated by the marginal increase in

business loans.

Malaysian bond markets yields rose across the board in October, especially on the

longer end of the curve. There is a sharp steepening of the curve during the month,

following the significant sell-off in the global bond market and also sharp depreciation

of MYR against the USD. As an illustration of the steepening of the curve, the 20-year

MGS yields rose approx. 20 bps compared to the prior month. The sell-off was as a

result of growing expectation of Fed rate hike in December. In addition, the sell-off

was also sparked by major central banks such as Bank of Japan, Bank of England and

European Central Bank questioning the efficacy of unconventional monetary policies

and at times, rumored to taper their asset purchase programs. Overall, 3-year, 5-year, 7-

year, 10-year, 15-year, 20-year and 30-year close at 3.03%, 3.33%, 3.55%, 3.64%,

4.05%, 4.335% and 4.58% respectively. In the primary market, there were three

tenders: (1) RM3.5b New 5-year GII 4/20, which drew a weak bid-to-cover (BTC)

18

ratio of 2.066 times with an average yield of 3.200%; (2) RM3.0b 10-year Re-opening

of GII 9/26, which drew a weak BTC ratio of 2.023 times with an average yield of

3.813%; and (3) RM2.0b 20-year MGS 5/35 which garnered BTC ratio of 2.154 times

at average yield of 4.295%.

Malaysia’s foreign exchange reserves rose by USD0.5bn to USD98.3bn as at 15

November 2016, from USD97.8bn registered at end-October 2016 and compared to

USD95.3bn at end-December 2015. CPI for Oct 2016 came in marginally lower at

1.4% YoY compared to Sep 2016’s reading on 1.5% YoY. 3Q GDP was 4.3% YoY,

higher than consensus expectations of 4.0% YoY (2Q: 4.0%, 1Q: 4.2%). GDP growth

was boosted by higher consumer spending which grew 6.4% YoY, supported by wage

and employment growth. Private investment eased slightly to 4.7% from 5.6% in 2Q,

attributed to a decline in spending on machinery and equipment. Government spending

also slowed to 3.1% from 6.5% in 2Q, on the back of lower spending on supply and

services. BNM left its OPR unchanged at 3.00%, as expected by the market given the

significant degree of financial market volatility following Donald Trump's presidential

victory. Compared to September, BNM slightly upgraded its view on global growth in

2017, but retained its assessment that the domestic economy remains on track to

expand as projected in 2016 and 2017. Malaysian bond markets yields rose across the

board, especially on the shorter end of the curve. The sharp increase in MGS yields

was in line with the significant sell-off in the global bond market as well as the sharp

depreciation of MYR against the USD. As an illustration of the bear flattening of the

curve, the 3-year MGS yield rose approx. 83 bps whilst the 20-year MGS yield rose

approx. 50 bps compared to the prior month. The sell-off was as a result of increasing

global bond yields world-wide following the surprise electoral victory of Donald

Trump, the UST 10-year yield rose from 1.83% to 2.37% during the month. Market

expectation is for the Trump administration to embark on a very fiscally aggressive

policy of tax cuts and increased infrastructure spending which will lead to higher

inflation.

Overall, 3-year, 5-year, 7-year, 10-year, 15-year, 20-year and 30-year close at 3.92%,

4.04%, 4.18%, 4.36%, 4.76%, 4.83% and 4.87% respectively. In the primary market,

there were two tenders: (1) RM3.0 billion 7-year Re-opening of GII 7/23, which drew a

BTC ratio of 2.21 times with an average yield of 4.094%; and (2) RM2.0 billion 10-

year Re-opening of GII 11/26, which drew a BTC ratio of 2.65 times with an average

yield of 4.465%.

Malaysia’s manufacturing PMI continue to remain below the 50-level mark coming in

unchanged at 47.1 in December. This was the twenty first consecutive months of

contraction. On the trade front, exports were below expectations, recording a

contraction of 8.6% YoY in October (September: -3.0%). Consensus expectations were

for a contraction of -5.6%. Imports meanwhile also fell by 6.6% YoY (September: -

0.1%) driven by broad-based declines in capital imports (-2.0%), intermediate imports

(-8.9%), and consumption imports (-8.0%). Nevertheless, trade surplus continues to be

positive at RM9.76b (September: RM7.56b). Indicative of the huge foreign outflows in

the month of November, Malaysia’s foreign reserves fell USD1.4b to USD96.4b. This

was the lowest reserve level since March 2016. The current level of reserves is

sufficient to cover 1.2 times of short-term external debt and 8.3 months of retained

imports. During the month, BNM announced several measures to enhance onshore

foreign exchange liquidity effective 5 December 2016. The measures include the

liberalization and deregulation of the onshore MYR hedging market, streamlining

treatment for investment in foreign currency assets and incentives and treatment of

export proceeds. These pre-emptive measures were implemented to stabilise the ringgit

19

and support financial stability amid further broad strengthening of the USD. Finally,

the banking sector’s loan growth showed signs of bottoming. For the month of

November, growth accelerated to 5.3% YoY (October: 4.5%) and a robust 0.9% MoM,

resulting in YTD annualised loan growth improving to 4.7% (10M2016: 4.0%). The

main driver of loan growth was in working capital loans (+1.6% MoM vs average

MoM run rate of +0.3%). In terms of consumer loans, residential property loan growth

remained stable at 9.5% YoY while automobile loans remain mired in negative

territory at -0.8% YoY.

The November sell-off which emanated from Donald Trump’s winning election bid

took a breather in the month of December as investors digested the implications of

Trump’s policies. With most investors away on holidays, the Malaysian Government

bonds saw some recovery in the yield curve amidst thin volumes. Overall, 3-year, 5-

year, 7-year, 10-year, 15-year, 20-year and 30-year close at 3.55%, 3.67%, 4.13%,

4.21%, 4.66%, 4.65% and 4.58% respectively. In the primary market, there was just

one auction, the RM1.5b 20-year Re-opening of GII 10/35 which garnered BTC ratio

of 3.750 times at average yield of 4.811%. The final auction of the year brought gross

MGS/GII issuance to a total of RM86b. BNM also announced the 2017 government

bonds auction calendar which consist of a total of 32 offerings (2016: 29) made up of

16 MGS (2016: 15) and 16 GII (2016: 14) auctions. The schedule was skewed towards

longer tenures of 15-30y, given the significant redemption schedule in the period 2017

- 2021.

Market

Outlook

Post the US Federal Open Market Committee (“FOMC”) December rate hike, investors

are still digesting the potential implications of a more hawkish FOMC, but more

pertinently, the larger impact of President Trump’s economic policies. Until there is

greater clarity on what President Trump and his team will do, the volatilities in regional

and global markets will likely continue.

Nevertheless, in spite of the challenging global outlook, Malaysia’s economy continues

to display resilience, as shown by a higher than expected 3Q2016 Year-over-year

(“YoY”) Gross Domestic Product (“GDP”) growth of 4.3% which is a reversal from

five quarters of decelerating growth. Moving forward, private consumption is expected

to continue to underpin 2017’s GDP projected growth of 4.3% (Source: World Bank).

In particular, key infrastructure projects such as the ongoing RAPID, Pan Borneo

Highway, KVMRT2, LRT3 and the newly announced East Coast Rail Link will likely

provide positive spin-off effect to the economy.

With Bank Negara Malaysia (“BNM”) having implemented a pre-emptive OPR

(“Overnight Policy Rate”) cut back in July 2016 and given the encouraging 3Q2016

GDP growth, BNM will likely retain its neutral bias espoused in the recent Monetary

Policy Committee (“MPC”) November meeting. While BNM still have room to

implement future OPR cuts given the benign inflation rate, any future easing policy

move will likely take into account the volatile financial markets and the persistent

weakness of the Ringgit. After giving back more than half the gains acquired since

January 2016, the Malaysian Government bonds as represented by the Quantshop

Malaysian Government Securities (“MGS”) All Index closed the year with a return of

3.37%.

The record outflow of close to RM20b in November seems to have tapered in

December with bargain hunting apparent amidst thin liquidity. In fact, the partial

recovery in the MGS yield curve in December was not accompanied by a stronger

Ringgit (versus the USD). Our Ringgit closed 2016 at 4.4862, a level which has not

20

been seen since the Asian Financial Crisis in 1998 and 41.6% down against its

strongest close of 3.168 in 2011.

Given that foreign holdings of Malaysia’s domestic debt securities continue to be near

its recent record high, the prospects of a further rise in the US 10-year treasury and a

bullish USD will continue to weigh on both the Ringgit and by implication the MGS

market.

Finally, from the recently released 2017 government bond auction calendar, we

surmised the following:

The 32 offerings for 2017 is skewed towards the longer maturities (15-30Y).

There will be only 2 3Y benchmark offerings, one each for MGS and

Government Investment Issue (“GII”). Hence, the front end of the yield curve

will likely be well supported with a steepening of the MGS curve expected in

2017.

There will be heavy maturities in the month of February and March in the

1H2017 (RM22.3b) and another RM44.5b maturing in August-November 2017.

These are the months where there will likely be more opportunities to trade.

Except for the current 3Y GII and 30Y MGS, all the existing Benchmark for

MGS and GII will be replace with new Benchmarks.

Finally, a new Benchmark, the 30Y GII will be introduced for the first time

which will complete the Sukuk curve and provide a Benchmark pricing for

corporate Sukuks in future.

Kuala Lumpur, Malaysia

AmFunds Management Berhad

14 February 2017

21

ADDITIONAL INFORMATION

Board of Directors of the Manager

The Board of Directors, of which more than one-third are independent members, exercise

ultimate control over the operations of the Manager. For the financial year ended 31 December

2016 (1 January 2016 to 31 December 2016), there were eight (8) Board of Directors meeting

held by the Manager.

Details of the Directors of the Manager are set out as below:

Name : Pushparani a/p A Moothathamby

Age : 58 years old

Nationality : Malaysian

Qualification : i) Fellow Member of The Chartered Association of Certified

Accountants, United Kingdom

ii) Member of the Malaysian Institute of Accountants,

Malaysia

Executive/Non-Executive

Director

: Non-Executive Director

Independent/Non-Independent

Director

: Non-Independent Director

Working Experience : i) (Dec 1983 – Apr 1986)

Sri Alam Group

[Group Accountant ]

ii) (May 1986 – Apr 1989)

Coopers & Lybrand

(now known as PricewaterhouseCoopers Malaysia)

[Consultant]

iii) (May 1989 – Dec 2004)

AmMerchant Bank Berhad

(now known as AmInvestment Bank Berhad)

[Last position held - Head of Corporate Finance]

iv) (Jan 2005 – July 2008)

AmMerchant Bank Berhad

(now known as AmInvestment Bank Berhad)

[Executive Director]

v) (July 2008 – Oct 2009)

AmInvestment Bank Berhad

[Managing Director, Relationship Banking & Regional

Business]

22

vi) (Oct 2009 – Oct 2013)

AmInvestment Bank Berhad

[Managing Director, Corporate & Institutional Banking]

vii) (Oct 2013 – May 2014)

AmInvestment Bank Berhad

[Managing Director, Wholesale Banking Coverage]

viii) (May 2014 – Present)

AmBank (M) Berhad

[Managing Director, Wholesale Banking Coverage]

Occupation : Managing Director, Wholesale Banking and Acting Chief

Executive Officer of AmInvestment Bank Berhad

Date of appointment : 2 November 2015

Directorship of other public

companies

: FIDE Forum

Number of Board meeting

attended for the financial year

ended 31 December 2016

: Eight (8)

Member of any other Board

Committee

: Audit Committee of Directors

Date of appointment to the

Investment Committee

: Not applicable

Number of Investment

Committee meeting attended for

the financial year ended 31

December 2016

: Not applicable

Family relationship with any

director

: None

Conflict of interest with the

Fund

: None

List of convictions for offences

within the past 10 years (if any)

: None

Name : Dato’ Mustafa bin Mohd Nor

Age : 65 years old

Nationality : Malaysian

Qualification : i) Master of Arts (Economic Policy), Boston University,

USA

ii) Bachelor of Economics (Analytical), University of

Malaya, Malaysia

Executive/Non-Executive

Director

: Non-Executive Director

Independent/Non-Independent

Director

: Independent Director

23

Working Experience : i) (1975-1988)

Ministry of Finance

[Last position held – Head of Macroeconomic Section,

Economic and International Division]

ii) (1988-1990)

Development & Commercial Bank Berhad.

[Manager, Treasury Department]

iii) March 1990-August 1992)

Arab Malaysian Securities Sdn Bhd

[Chief Economist]

iv) (September 1992-December 2001)

AmSecurities Sdn Bhd

[Executive Director/Chief Economist]

v) (January 2002-December 2005)

AmSecurities Sdn Bhd

[Managing Director]

vi) (January 2006-May 2009) (Retirement)

AmInvestment Bank Berhad Group

[Economic Advisor]

vii) (September 2009-August 2012) (Contract)

Permodalan Nasional Berhad

[Senior Vice President/Head, Research Division]

Occupation : Director

Date of appointment : 3 March 2014

Directorship of other public

companies

: KUISAS Berhad

Number of Board meeting

attended for the financial year

ended 31 December 2016

: Eight (8)

Member of any other Board

Committee

: i) Audit Committee of Directors

ii) Investment Committee

Date of appointment to the

Investment Committee

: 3 March 2014

Number of Investment

Committee meeting attended for

the financial year ended 31

December 2016

: Four (4)

Family relationship with any

director

: None

24

Conflict of interest with the

Fund

: None

List of convictions for offences

within the past 10 years (if any)

: None

Name : Tai Terk Lin

Age : 56 years old

Nationality : Malaysian

Qualification : i) Master of Business Administration (School of

Management), Cranfield Institute of Technology,

United Kingdom.

ii) Bachelor of Science with Education, Mathematics &

Physics, University of Malaya, Malaysia.

iii) Certified Financial Planner Board of Standard, Inc,

USA Certified Financial Planner

iv) Financial Industry Certified Professional, FICP,

Institute of Banking & Finance (IBF), Singapore

Executive/Non-Executive

Director

: Non-Executive Director

Independent/Non-Independent

Director

: Independent Director

Working Experience : i) (October 2009 – September 2012)

(Oct 2012 with ICB Indonesia)

AGICB Banking Group

[Group Chief Executive Officer of ICB Financial Group

Holdings]

ii) (January 2009 – August 2009)

Platinum Capital Management (Asia) Pte Ltd,

Singapore

[Executive Director/Head of Business Development

Asia]

iii) (January 2007 – November 2008)

DBS Bank, Singapore

[Senior Vice President/Head – Malaysia Coverage

Private Banking]

iv) (March 2002 – December 2006)

AmInvestment Bank Berhad

[Director/Head, Private Banking]

v) (April 1995 – December 2001)

HLB Unit Trust Management Bhd

[Chief Executive Officer]

25

vi) (April 1994 – March 1995)

Hong Leong Bank Berhad (Ex-Hong Leong Finance)

[Chief Project Manager/Credit Manager]

vii) (January 1994 – April 1994)

United Merchant Finance Berhad

[Special Assistant to Executive Chairman]

viii) (June 1992 – December 1993)

Hong Leong Management Company Sdn Bhd

[Senior Analyst (Executive Chairman’s Office)]

ix) (January 1991 – June 1992)

Corporate Care Division, PricewaterhouseCoopers

[Consulting Manager]

Occupation : Director

Date of appointment : 15 December 2014

Directorship of other public

companies

: Nil

Number of Board meeting

attended for the financial year

ended 31 December 2016

: Eight (8)

Member of any other Board

Committee

: Investment Committee and Audit Committee of Directors

(Independent)

Date of appointment to the

Investment Committee

: 15 December 2014

Number of Investment

Committee meeting attended for

the financial year ended 31

December 2016

: Four (4)

Family relationship with any

director

: None

Conflict of interest with the

Fund

: None

List of convictions for offences

within the past 10 years (if any)

: None

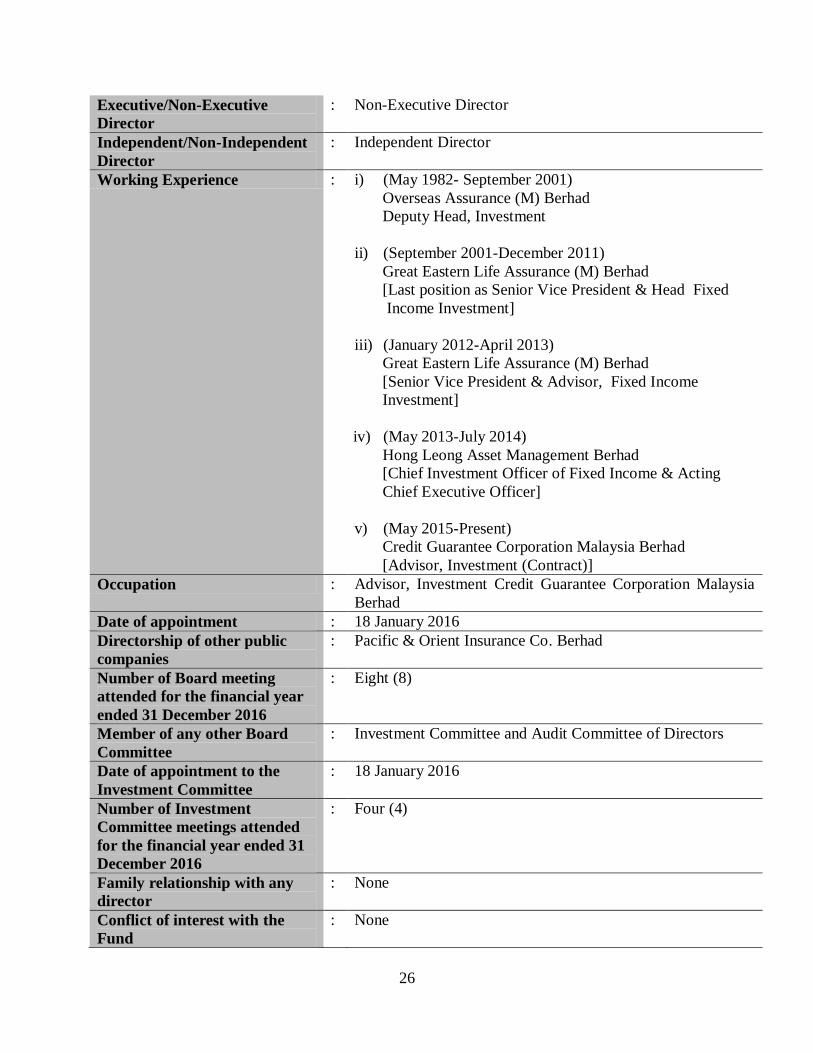

Name : Sum Leng Kuang

Age : 62 years old

Nationality : Malaysian

Qualification : i) Bachelor of Commerce (Finance), University of

Canterbury, New Zealand

ii) Certified Financial Planner, Financial Planning

Association of Malaysia

26

Executive/Non-Executive

Director

: Non-Executive Director

Independent/Non-Independent

Director

: Independent Director

Working Experience : i) (May 1982- September 2001)

Overseas Assurance (M) Berhad

Deputy Head, Investment

ii) (September 2001-December 2011)

Great Eastern Life Assurance (M) Berhad

[Last position as Senior Vice President & Head Fixed

Income Investment]

iii) (January 2012-April 2013)

Great Eastern Life Assurance (M) Berhad

[Senior Vice President & Advisor, Fixed Income

Investment]

iv) (May 2013-July 2014)

Hong Leong Asset Management Berhad

[Chief Investment Officer of Fixed Income & Acting

Chief Executive Officer]

v) (May 2015-Present)

Credit Guarantee Corporation Malaysia Berhad

[Advisor, Investment (Contract)]

Occupation : Advisor, Investment Credit Guarantee Corporation Malaysia

Berhad

Date of appointment : 18 January 2016

Directorship of other public

companies

: Pacific & Orient Insurance Co. Berhad

Number of Board meeting

attended for the financial year

ended 31 December 2016

: Eight (8)

Member of any other Board

Committee

: Investment Committee and Audit Committee of Directors

Date of appointment to the

Investment Committee

: 18 January 2016

Number of Investment

Committee meetings attended

for the financial year ended 31

December 2016

: Four (4)

Family relationship with any

director

: None

Conflict of interest with the

Fund

: None

27

List of convictions for offences

within the past 10 years (if any)

: None

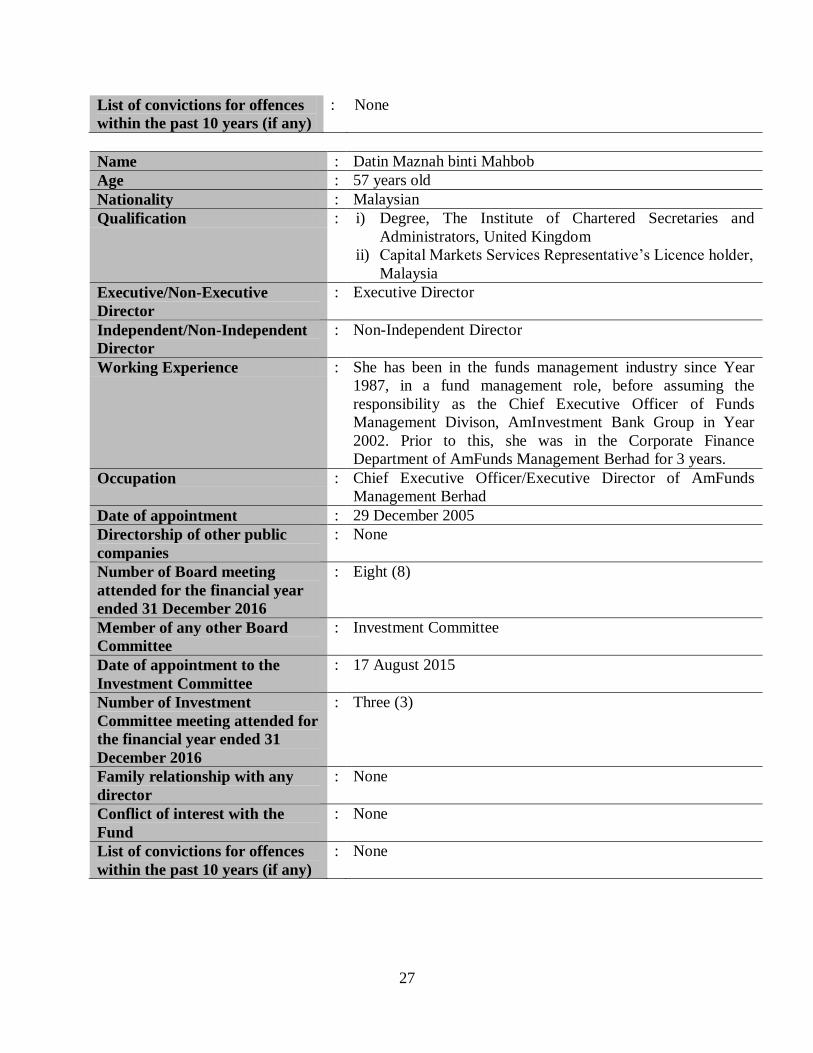

Name : Datin Maznah binti Mahbob

Age : 57 years old

Nationality : Malaysian

Qualification : i) Degree, The Institute of Chartered Secretaries and

Administrators, United Kingdom

ii) Capital Markets Services Representative’s Licence holder,

Malaysia

Executive/Non-Executive

Director

: Executive Director

Independent/Non-Independent

Director

: Non-Independent Director

Working Experience : She has been in the funds management industry since Year

1987, in a fund management role, before assuming the

responsibility as the Chief Executive Officer of Funds

Management Divison, AmInvestment Bank Group in Year

2002. Prior to this, she was in the Corporate Finance

Department of AmFunds Management Berhad for 3 years.

Occupation : Chief Executive Officer/Executive Director of AmFunds

Management Berhad

Date of appointment : 29 December 2005

Directorship of other public

companies

: None

Number of Board meeting

attended for the financial year

ended 31 December 2016

: Eight (8)

Member of any other Board

Committee

: Investment Committee

Date of appointment to the

Investment Committee

: 17 August 2015

Number of Investment

Committee meeting attended for

the financial year ended 31

December 2016

: Three (3)

Family relationship with any

director

: None

Conflict of interest with the

Fund

: None

List of convictions for offences

within the past 10 years (if any)

: None

28

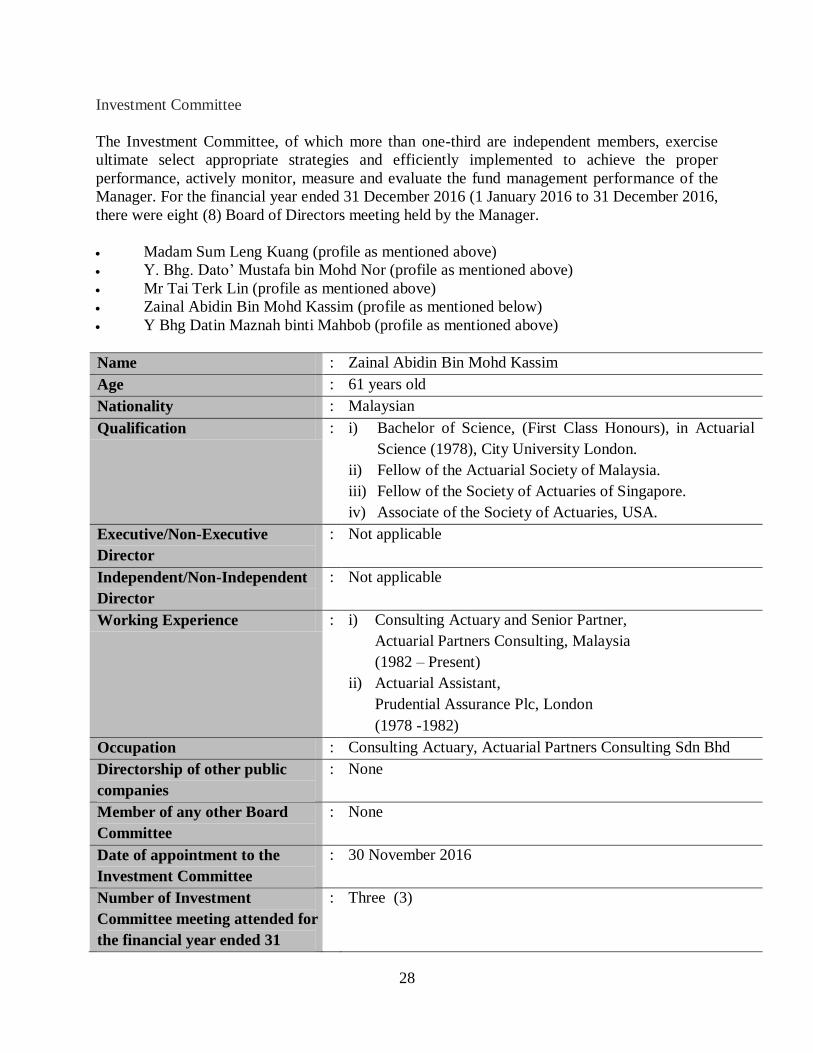

Investment Committee

The Investment Committee, of which more than one-third are independent members, exercise

ultimate select appropriate strategies and efficiently implemented to achieve the proper

performance, actively monitor, measure and evaluate the fund management performance of the

Manager. For the financial year ended 31 December 2016 (1 January 2016 to 31 December 2016,

there were eight (8) Board of Directors meeting held by the Manager.

Madam Sum Leng Kuang (profile as mentioned above)

Y. Bhg. Dato’ Mustafa bin Mohd Nor (profile as mentioned above)

Mr Tai Terk Lin (profile as mentioned above)

Zainal Abidin Bin Mohd Kassim (profile as mentioned below)

Y Bhg Datin Maznah binti Mahbob (profile as mentioned above)

Name : Zainal Abidin Bin Mohd Kassim

Age : 61 years old

Nationality : Malaysian

Qualification : i) Bachelor of Science, (First Class Honours), in Actuarial

Science (1978), City University London.

ii) Fellow of the Actuarial Society of Malaysia.

iii) Fellow of the Society of Actuaries of Singapore.

iv) Associate of the Society of Actuaries, USA.

Executive/Non-Executive

Director

: Not applicable

Independent/Non-Independent

Director

: Not applicable

Working Experience : i) Consulting Actuary and Senior Partner,

Actuarial Partners Consulting, Malaysia

(1982 – Present)

ii) Actuarial Assistant,

Prudential Assurance Plc, London

(1978 -1982)

Occupation : Consulting Actuary, Actuarial Partners Consulting Sdn Bhd

Directorship of other public

companies

: None

Member of any other Board

Committee

: None

Date of appointment to the

Investment Committee

: 30 November 2016

Number of Investment

Committee meeting attended for

the financial year ended 31

: Three (3)

29

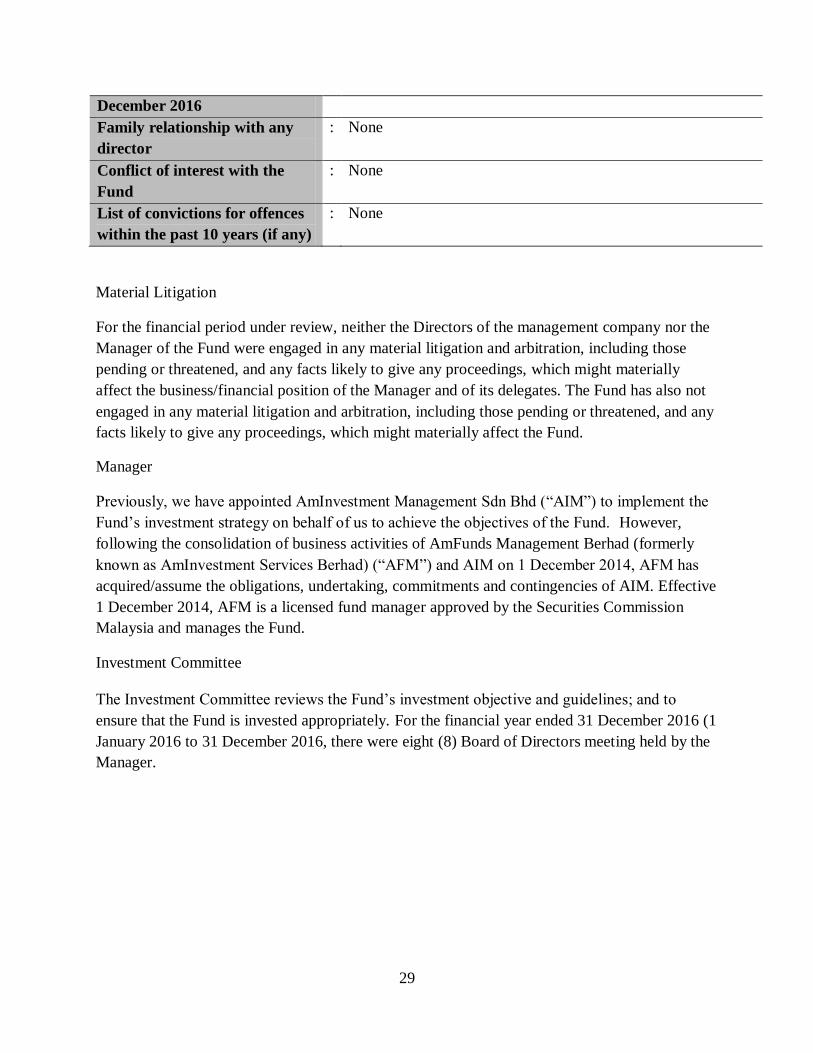

December 2016

Family relationship with any

director

: None

Conflict of interest with the

Fund

: None

List of convictions for offences

within the past 10 years (if any)

: None

Material Litigation

For the financial period under review, neither the Directors of the management company nor the

Manager of the Fund were engaged in any material litigation and arbitration, including those

pending or threatened, and any facts likely to give any proceedings, which might materially

affect the business/financial position of the Manager and of its delegates. The Fund has also not

engaged in any material litigation and arbitration, including those pending or threatened, and any

facts likely to give any proceedings, which might materially affect the Fund.

Manager

Previously, we have appointed AmInvestment Management Sdn Bhd (“AIM”) to implement the

Fund’s investment strategy on behalf of us to achieve the objectives of the Fund. However,

following the consolidation of business activities of AmFunds Management Berhad (formerly

known as AmInvestment Services Berhad) (“AFM”) and AIM on 1 December 2014, AFM has

acquired/assume the obligations, undertaking, commitments and contingencies of AIM. Effective

1 December 2014, AFM is a licensed fund manager approved by the Securities Commission

Malaysia and manages the Fund.

Investment Committee

The Investment Committee reviews the Fund’s investment objective and guidelines; and to

ensure that the Fund is invested appropriately. For the financial year ended 31 December 2016 (1

January 2016 to 31 December 2016, there were eight (8) Board of Directors meeting held by the

Manager.

30

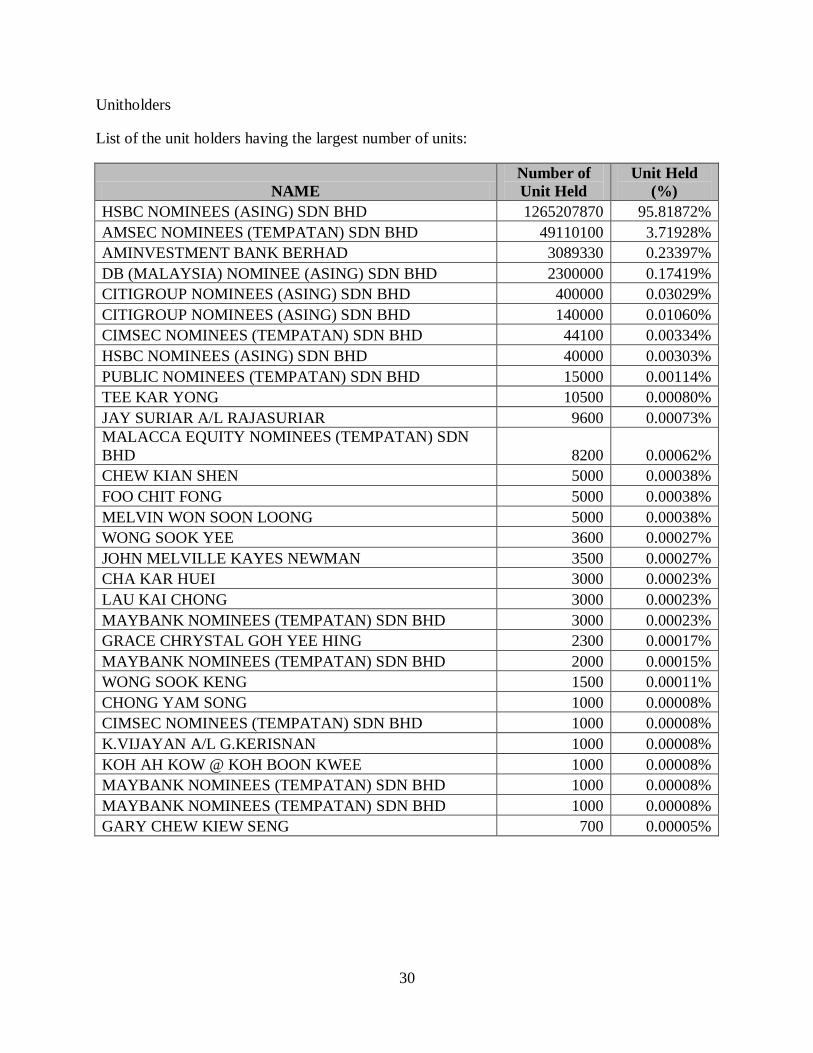

Unitholders

List of the unit holders having the largest number of units:

NAME

Number of

Unit Held

Unit Held

(%)

HSBC NOMINEES (ASING) SDN BHD 1265207870 95.81872%

AMSEC NOMINEES (TEMPATAN) SDN BHD 49110100 3.71928%

AMINVESTMENT BANK BERHAD 3089330 0.23397%

DB (MALAYSIA) NOMINEE (ASING) SDN BHD 2300000 0.17419%

CITIGROUP NOMINEES (ASING) SDN BHD 400000 0.03029%

CITIGROUP NOMINEES (ASING) SDN BHD 140000 0.01060%

CIMSEC NOMINEES (TEMPATAN) SDN BHD 44100 0.00334%

HSBC NOMINEES (ASING) SDN BHD 40000 0.00303%

PUBLIC NOMINEES (TEMPATAN) SDN BHD 15000 0.00114%

TEE KAR YONG 10500 0.00080%

JAY SURIAR A/L RAJASURIAR 9600 0.00073%

MALACCA EQUITY NOMINEES (TEMPATAN) SDN

BHD 8200 0.00062%

CHEW KIAN SHEN 5000 0.00038%

FOO CHIT FONG 5000 0.00038%

MELVIN WON SOON LOONG 5000 0.00038%

WONG SOOK YEE 3600 0.00027%

JOHN MELVILLE KAYES NEWMAN 3500 0.00027%

CHA KAR HUEI 3000 0.00023%

LAU KAI CHONG 3000 0.00023%

MAYBANK NOMINEES (TEMPATAN) SDN BHD 3000 0.00023%

GRACE CHRYSTAL GOH YEE HING 2300 0.00017%

MAYBANK NOMINEES (TEMPATAN) SDN BHD 2000 0.00015%

WONG SOOK KENG 1500 0.00011%

CHONG YAM SONG 1000 0.00008%

CIMSEC NOMINEES (TEMPATAN) SDN BHD 1000 0.00008%

K.VIJAYAN A/L G.KERISNAN 1000 0.00008%

KOH AH KOW @ KOH BOON KWEE 1000 0.00008%

MAYBANK NOMINEES (TEMPATAN) SDN BHD 1000 0.00008%

MAYBANK NOMINEES (TEMPATAN) SDN BHD 1000 0.00008%

GARY CHEW KIEW SENG 700 0.00005%

Independent auditors’ report to the unitholders of

ABF Malaysia Bond Index Fund

Report on the audit of the financial statements

Opinion

Key audit matters

Basis for opinion

We conducted our audit in accordance with approved standards on auditing in Malaysia and

International Standards on Auditing. Our responsibilities under those standards are further described

in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We

believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for

our opinion.

Independence and other ethical responsibilities

We are independent of the Fund in accordance with the By-Laws (on Professional Ethics, Conduct

and Practice) of the Malaysian Institute of Accountants (“By-Laws”) and the International Ethics

Standards Board for Accountants’ Code of Ethics for Professional Accountants (“IESBA Code”),

and we have fulfilled our other ethical responsibilities in accordance with the By-Laws and the

IESBA Code.

Key audit matters are those matters that, in our professional judgement, were of most significance in

our audit of the financial statements of the Fund for the current year. These matters were addressed

in the context of our audit of the financial statements as a whole, and in forming our opinion thereon,

and we do not provide a separate opinion on these matters. For the matter below, our description of

how our audit addressed the matter is provided in that context.

We have audited the financial statements of ABF Malaysia Bond Index Fund (“the Fund”), which

comprise the statement of financial position as at 31 December 2016, the statement of

comprehensive income, statement of changes in equity and statement of cash flows for the financial

year then ended, and a summary of significant accounting policies and other explanatory notes, as set

out on pages 35 to 58.

In our opinion, the accompanying financial statements give a true and fair view of the financial

position of the Fund as at 31 December 2016, and of its financial performance and its cash flows for

the year then ended in accordance with Malaysian Financial Reporting Standards and International

Financial Reporting Standards.

31

Valuation and existence of investments

If based on the work we have performed, we conclude that there is a material misstatement of this

other information, we are required to report that fact. We have nothing to report in this regard.

Our response: Our audit work included, but was not restricted to, understanding the Manager’s

process and controls for the valuation of investments in order to assess compliance with relevant

accounting standards, performing walkthrough procedures and testing the operating effectiveness of

relevant controls on a sample basis. We agreed the valuation of all investments as at the year end to

an independent source of market prices. We obtained confirmation of the existence and ownership of

the investments as at the year- end directly from the Fund’s independent Trustee. The Fund’s

accounting policy on the valuation of investments is included in Note 3, and its disclosures about

investments held at the year-end are included in Note 4.

The risk: The Fund’s business is investing in a portfolio consisting of mainly Ringgit Malaysia

denominated Government and quasi-Government debt securities for investors who seek an ‘index-

based approach to investing. Accordingly, the investment portfolio of mainly Government debt

securities is a significant material item in the financial statements. The valuation of the assets held in

the investment portfolio is the key driver of the Fund’s net asset value and investment return.

Incorrect asset pricing or a failure to maintain proper legal title of assets by the Fund could have a

significant impact on portfolio valuation and, therefore, the return generated for shareholders. We

therefore identified the valuation and existence of the investment portfolio as risks that require

particular audit attention.

Independent auditors’ report to the unitholders of