minit mesyuarat majlis dialog operasi bil. 1/2006 · sample of the borang be from the e-filling...

TRANSCRIPT

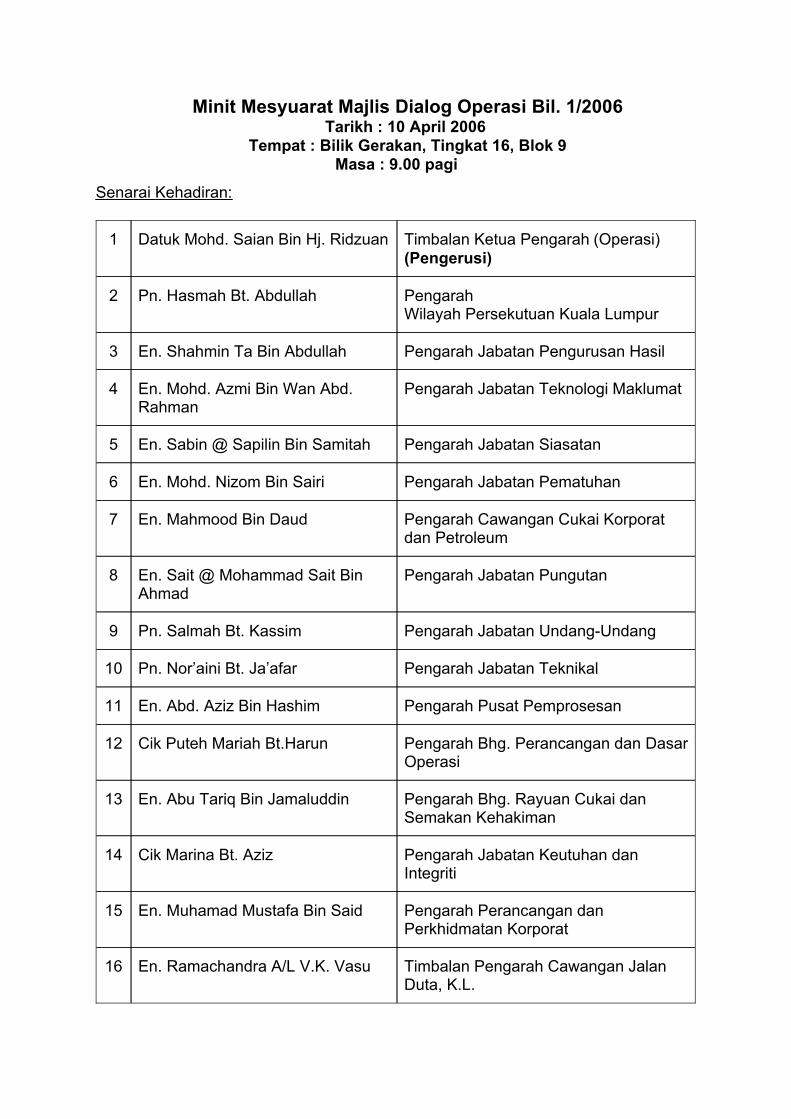

Minit Mesyuarat Majlis Dialog Operasi Bil. 1/2006Tarikh : 10 April 2006

Tempat : Bilik Gerakan, Tingkat 16, Blok 9Masa : 9.00 pagi

Senarai Kehadiran:

Timbalan Pengarah Cawangan JalanDuta, K.L.

En. Ramachandra A/L V.K. Vasu16

Pengarah Perancangan danPerkhidmatan Korporat

En. Muhamad Mustafa Bin Said15

Pengarah Jabatan Keutuhan danIntegriti

Cik Marina Bt. Aziz14

Pengarah Bhg. Rayuan Cukai danSemakan Kehakiman

En. Abu Tariq Bin Jamaluddin13

Pengarah Bhg. Perancangan dan DasarOperasi

Cik Puteh Mariah Bt.Harun12

Pengarah Pusat PemprosesanEn. Abd. Aziz Bin Hashim11

Pengarah Jabatan TeknikalPn. Nor’aini Bt. Ja’afar10

Pengarah Jabatan Undang-UndangPn. Salmah Bt. Kassim9

Pengarah Jabatan PungutanEn. Sait @ Mohammad Sait BinAhmad

8

Pengarah Cawangan Cukai Korporatdan Petroleum

En. Mahmood Bin Daud7

Pengarah Jabatan PematuhanEn. Mohd. Nizom Bin Sairi6

Pengarah Jabatan SiasatanEn. Sabin @ Sapilin Bin Samitah5

Pengarah Jabatan Teknologi MaklumatEn. Mohd. Azmi Bin Wan Abd.Rahman

4

Pengarah Jabatan Pengurusan HasilEn. Shahmin Ta Bin Abdullah3

Pengarah Wilayah Persekutuan Kuala Lumpur

Pn. Hasmah Bt. Abdullah2

Timbalan Ketua Pengarah (Operasi)(Pengerusi)

Datuk Mohd. Saian Bin Hj. Ridzuan1

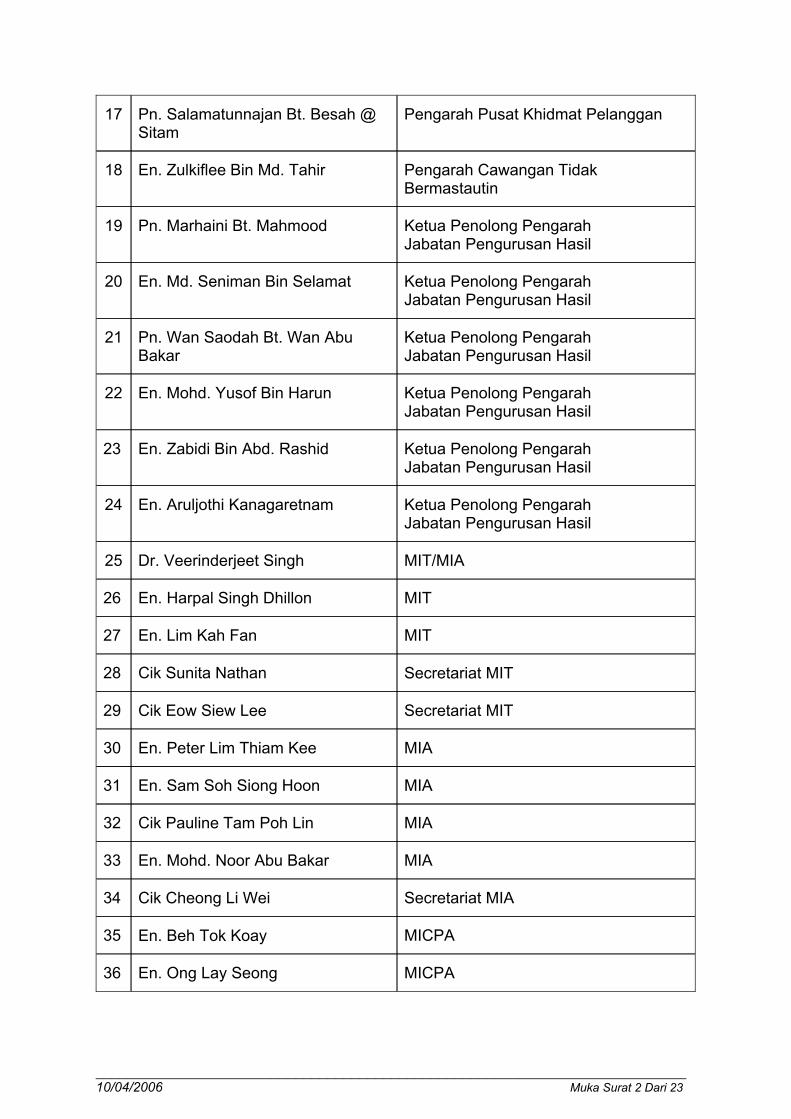

MICPAEn. Ong Lay Seong36

MICPAEn. Beh Tok Koay35

Secretariat MIACik Cheong Li Wei34

MIAEn. Mohd. Noor Abu Bakar33

MIACik Pauline Tam Poh Lin32

MIAEn. Sam Soh Siong Hoon31

MIAEn. Peter Lim Thiam Kee30

Secretariat MITCik Eow Siew Lee 29

Secretariat MITCik Sunita Nathan28

MITEn. Lim Kah Fan27

MITEn. Harpal Singh Dhillon26

MIT/MIADr. Veerinderjeet Singh25

Ketua Penolong Pengarah Jabatan Pengurusan Hasil

En. Aruljothi Kanagaretnam24

Ketua Penolong Pengarah Jabatan Pengurusan Hasil

En. Zabidi Bin Abd. Rashid23

Ketua Penolong Pengarah Jabatan Pengurusan Hasil

En. Mohd. Yusof Bin Harun22

Ketua Penolong Pengarah Jabatan Pengurusan Hasil

Pn. Wan Saodah Bt. Wan AbuBakar

21

Ketua Penolong Pengarah Jabatan Pengurusan Hasil

En. Md. Seniman Bin Selamat20

Ketua Penolong Pengarah Jabatan Pengurusan Hasil

Pn. Marhaini Bt. Mahmood19

Pengarah Cawangan TidakBermastautin

En. Zulkiflee Bin Md. Tahir18

Pengarah Pusat Khidmat Pelanggan Pn. Salamatunnajan Bt. Besah @Sitam

17

__________________________________________________________________________10/04/2006 Muka Surat 2 Dari 23

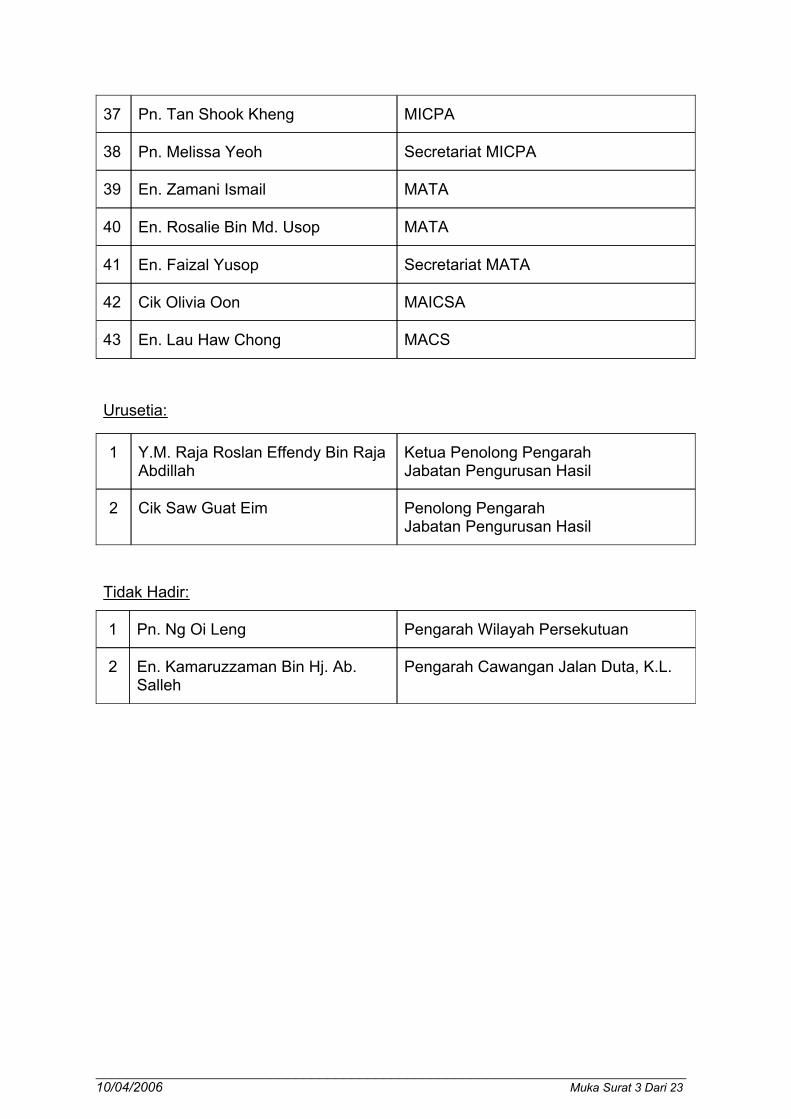

Penolong Pengarah Jabatan Pengurusan Hasil

Cik Saw Guat Eim2

Ketua Penolong PengarahJabatan Pengurusan Hasil

Y.M. Raja Roslan Effendy Bin RajaAbdillah

1

Urusetia:

MACSEn. Lau Haw Chong43

MAICSACik Olivia Oon42

Secretariat MATAEn. Faizal Yusop41

MATAEn. Rosalie Bin Md. Usop40

MATAEn. Zamani Ismail39

Secretariat MICPAPn. Melissa Yeoh38

MICPAPn. Tan Shook Kheng37

Pengarah Cawangan Jalan Duta, K.L.En. Kamaruzzaman Bin Hj. Ab.Salleh

2

Pengarah Wilayah PersekutuanPn. Ng Oi Leng1

Tidak Hadir:

__________________________________________________________________________10/04/2006 Muka Surat 3 Dari 23

1. Pendahuluan

1.1 Tuan Pengerusi mengalu-alukan kehadiran wakil-wakil dari MIT, MIA,MICPA, MATA, MAICSA dan MACS ke majlis dialog ini. Beliaumemperkenalkan pegawai-pegawai dari LHDNM yang hadir dalammesyuarat. Seterusnya wakil-wakil persatuan memperkenalkan dirimasing-masing.

1.2 Tuan Pengerusi seterusnya menjemput wakil rakan dialog untukmembentangkan isu-isu yang ingin dibincangkan.

2. Isu-isu Asal daripada MIT / MIA / MICPA

2.1 Submission of Income Tax Returns

Currently, all non-business income individual tax returns (Form BE) arerequired to be filed by 30 April. As most of the individual taxpayers areunder this category and there is only one deadline for them to file thetax returns and settle the balance of the tax liability by 30 April, a lot ofproblems/difficulties were encountered last year by members of theInstitutes. These difficulties are highlighted below with the view ofensuring that these issues can be handled effectively this year.

2.1.1 Submission by courier services

With regard to the submission of tax returns (Forms BE) to theProcessing Centre at Pandan Indah by courier services, theInstitutes were informed that the courier services staff canproceed to the 12th Floor of the Processing Centre and drop thereturn forms at the counter without the need to queue up.However, the courier staff would only be able to obtain theacknowledgement copy one week later. The LHDNM’s officerswill sort out the acknowledgement copy according to the nameof the courier service company.

In view of the above, the Institutes sincerely hope that,where necessary, more LHDNM staff are deployed so as tospeed up the matter and the acknowledgement copiescould be given out immediately upon verifying that therelevant return forms are received.

JAWAPAN:

Pembayar cukai dan ejen cukai sentiasa dinasihatkansupaya mengemukakan borang nyata dengan lebih awal.Oleh kerana bilangan borang yang diterima pada hari-hariterakhir menjelang 30 April adalah terlalu banyak, makamasa diperlukan untuk menyemak dan mengesahkan

__________________________________________________________________________10/04/2006 Muka Surat 4 Dari 23

penerimaan borang-borang yang dihantar melaluiperkhidmatan “courier” bagi mengelakkan sebarangmasalah/pertikaian kelak. Pihak Persatuan dimintabekerjasama supaya jangan menghantar borang-borangnyata pada saat-saat terakhir.

Untuk mengatasi masalah tersebut, penggunaan e-filingdigalakkan kerana akuan terima dapat diperolehi secara“on-line”. Pelbagai usaha telah dilakukan oleh LHDNMtermasuk pemberian sijil digital percuma dan taklimatpembelajaran e-filing kepada pembayar-pembayar cukai disektor awam dan swasta. Pihak Persatuan dimintamenyokong usaha LHDNM dengan menggunakan e-filingmulai tahun ini dan mengubah cara pemikiran (“mindset”)/keyakinan pembayar cukai terhadap penggunaan e-filing.Pihak Persatuan boleh menghubungi LHDNM jikapembelajaran e-filing diperlukan dan sekiranya menghadapimasalah talian.

2.1.2 Submission via postal servicesThe Institutes were also informed that the postal date isacceptable as the date of submission of the tax return to theLHDNM if one uses postal services.

Please be informed that the only way a taxpayer can getevidence of posting is via registered mail or delivery by Poslaju.This means additional cost to taxpayers. Normal mailing of taxreturns, however, does not seem to suffice as no proof ofposting is available. Notwithstanding this, we believe that theLHDNM should be assisting taxpayers rather than havingtaxpayers incur additional costs. It should be noted that whenthe LHDNM sends out correspondence to taxpayers, the lettersare not registered or sent via Poslaju and the LHDNM does notneed to have any proof of posting a letter. The taxpayer shouldnot be placed in a different situation.

In this connection, the Institutes hope that the LHDNM canlook into other ways of assisting taxpayers on this matter.

JAWAPAN:

Sebagai konsesi, penalti tidak akan dikenakan sekiranyaborang nyata diterima dalam tempoh 14 hari dari tarikhterakhir untuk pengembalian borang nyata. Untuk borangnyata yang diterima selepas tempoh 14 hari tersebut dimana penalti telah dikenakan, rayuan bolehdipertimbangkan jika dapat dibuktikan bahawa ia dihantarpada atau sebelum tarikh terakhir untuk pengembalianborang nyata.

__________________________________________________________________________10/04/2006 Muka Surat 5 Dari 23

2.1.3 Submission to assessment branchesWe would like to seek confirmation as to the current position forthe submission of Form BE and Form B on 30 April and 30 Junerespectively.

The Institutes are of the view that insisting that all taxpayers togo to Pandan Indah to file tax returns is not an appropriate step.This causes various problems including long queues whichresulted in the courier companies refusing to deliver theoutstation return forms to Pandan Indah as mentioned in 1.1above as well as unnecessary stress and frayed tempers. Wedo note that in the last few days of April 2005, other branchesdid accept tax returns.

In this regard, the Institutes would like to suggest thattaxpayers/tax agents be allowed to submit tax returns at thevarious Assessment Branches so as to avoid the bottleneckthat would normally occur on the last day of filing taxreturns. These branches can then collate and send the taxreturns to the Processing Centre. We believe this shouldbe part of the service provided by the LHDNM.

JAWAPAN:

Semua borang nyata mesti dikemukakan ke PusatPemprosesan di Pandan Indah, Kuala Lumpur. Untukmengatasi masalah ini, pihak Persatuan digalakkan supayamenggunakan e-filing mulai tahun ini.

2.1.4 Acknowledgement cardsThe Institutes were surprised to be informed that last yearacknowledgement cards were not issued to taxpayers whocame to file their tax returns.

We would like to suggest that such cards/slips should beissued to taxpayers as proof of submission. For the future,we would like to suggest that on the cover page of the taxreturn, the LHDNM could have a perforated slip which canbe filled up by a taxpayer and torn off and then stamped bythe LHDNM counter staff to acknowledge receipt. Thiswould cut down the time spent in filling upacknowledgement cards.

JAWAPAN:

Amalan mengeluarkan kad akuan terima tidak akandipraktikkan lagi oleh LHDNM. Sekiranya borang nyatadikemukakan melalui e-filing, akuan terima dapat diperolehisecara “on-line”.

__________________________________________________________________________10/04/2006 Muka Surat 6 Dari 23

2.2 Completion of Borang B/BE

The Institutes wish to seek clarification on the following matters:-

2.2.1 Where column is not applicable

It is noted that certain items in a particular column in the BorangB/BE may not be relevant to all taxpayers.

The Institutes wish to clarify in such instances should thecolumn be (i) left blank, (ii) a dash be drawn across the last3 boxes or (iii) a “0” is inserted.

(We have been informed that the Kuantan branch office isadvising taxpayers to leave the column blank whilst asample of the Borang BE from the e-filling software shownduring the Program Pembelajaran shows a “0”. It is alsonoted that for the completion of Borang C & R, taxpayersare allowed to either leave the column blank or indicate adash in the column.)

JAWAPAN:

Ruang yang tidak berkenaan tidak perlu diisi.

2.2.2 Assistance

As 2005 was the first year the Borang B/BE was submitted, it ishighly likely that mistakes were made by taxpayers and taxagents in completing the forms.

In order to minimise future errors, the Institutes proposethat the LHDNM provide assistance in highlighting whatevererrors made and the correct approach that should beadopted to avoid a repeat of such errors.

JAWAPAN:

LHDNM berterima kasih atas inisiatif pihak Persatuan untukmengurangkan kadar kesilapan dalam pengisian Borang B /BE.

Sila rujuk Lampiran yang disertakan untuk senaraikesilapan-kesilapan biasa dalam pengisian borang nyataberdasarkan Borang B / BE 2004.

__________________________________________________________________________10/04/2006 Muka Surat 7 Dari 23

2.2.3 Issuance of Borang B / BE

It was reported in the Chinese dailies that the LHDNM may notbe issuing the Borang B/BE for Year of Assessment 2007 totaxpayers in view of the available e-filing services.

The Institutes would like to seek clarification on theaccuracy of such reports and highlight that the practice ofthe LHDNM in issuing the return forms should continue. Tofacilitate the successful implementation of the selfassessment system, this would require the co-operation ofboth the LHDNM and taxpayers.

JAWAPAN:

Tiada isu.

2.3 Payment of Final Tax Liability to be given 30 days Extension ofTime from the Date of Submission of Tax Return

Under the Official Assessment System, the legislation allowed thetaxpayers to pay tax to the LHDNM within 30 days from the date ofissuance of a Notice of Assessment and a grace period of additional 14days was granted by concession.

It is proposed that a provision be introduced in the current taxlegislation to allow taxpayers to settle their final tax balancewithin 30 days from the date of submission of the tax returns(deemed assessment) so as to ease the financial burden of thetaxpayers.

JAWAPAN:

Layanan yang sama seperti untuk borang nyata iaitu tempoh 14hari dibenarkan sebagai konsesi. Sila rujuk Perkara 2.1.2.

2.4 Utilisation of Tax Credits

2.4.1 The Institutes are of the view that the utilisation of availabletax credits should not be by request. The offset of taxcredits should be done automatically so long as there areavailable tax credits unless a request for refund has beenmade by the taxpayer. Taxpayers should not be required tomake a request for an offset. This would assist to ease theadministrative burden of both the LHDNM and taxpayers.

__________________________________________________________________________10/04/2006 Muka Surat 8 Dari 23

JAWAPAN:

Tuan Pengerusi menjelaskan bahawa terdapat dua keadaan“set-off” untuk kes “clear credit” iaitu:-

(a) “set-off” adalah automatik bagi cukai yang masihterhutang; dan

(b) baki kredit (jika ada) selepas itu boleh digunakansepenuhnya untuk “set-off” ansuran akan datangyang perlu dibayar (tiada had bilangan ansuran)tetapi permohonan daripada pembayar cukaidiperlukan.

Kredit cukai akan dibayar balik sekiranya tiada permohonandaripada pembayar cukai.

Pihak Persatuan boleh menghubungi LHDNM sekiranyaterdapat masalah di cawangan berhubung perkara di atas.

2.4.2 Under the self assessment system, when the tax returns arefiled, any excess tax paid can be refunded or utilised to offsetagainst future tax liabilities. We have been informed that inpractice, such tax credits will only be allowed for utilisation afterthe return has been keyed into the system.

The Institutes are of the view that where the taxpayer isable to provide supporting documents to substantiate theavailable tax credits, the utilisation should be allowed bythe LHDNM. The Institutes also wish to clarify the timeframe taken from the submission date to the time therelevant data is captured into the system.

JAWAPAN:

“Clear credit” hanya dapat ditentukan selepas borangdiproses, di antaranya cukai kena bayar mesti direkodkandalam lejer pembayar cukai.

Pemprosesan borang fizikal memakan masa kerana perlumelalui pelbagai proses seperti pengisihan borang,kemasukan data dan sebagainya. Walau bagaimanapunLHDNM akan menangani masalah tempoh pemprosesanborang tetapi pihak Persatuan juga boleh membantudengan memastikan bahawa borang nyata yangdikemukakan adalah teratur; dan kes-kes bayaran balikdiasingkan dan dicatatkan sedemikian pada sampul surat.Ini adalah kerana kes-kes bayaran balik seksyen 110(dividen) dan lebihan bayaran akan diproses terlebihdahulu.

Sebagai langkah mempercepatkan pemprosesan borang,LHDNM menggalakkan penggunaan e-filing.

__________________________________________________________________________10/04/2006 Muka Surat 9 Dari 23

2.5 Processing of Dividend Vouchers in a Section 110 Refund Case

Where there is a repayment arising from Section 110 credits, taxpayersare required to submit the original dividend vouchers together with thetax return to the Processing Centre. After the necessary verification bythe Processing Centre, the original vouchers are returned to thetaxpayers. However, when a desk audit is carried out, the CawanganSyarikat has requested for the dividend vouchers again.

The Institutes wish to clarify the procedure undertaken by LHDNMto process repayments arising from Section 110 credits and theneed for the dividend vouchers to be submitted twice to theLHDNM. The Institutes also wish to highlight that in the spirit ofself assessment, the refund of Section 110 credits should beprocessed irrespective of whether tax audits have beenconducted.

JAWAPAN:

Senario ini berlaku apabila pembayar cukai memohon supayadipercepatkan kes bayaran balik ataupun bila kes diaudit.Mengikut prosedur, kes bayaran balik seksyen 110 (dividen)biasanya akan diaudit untuk mengesahkan kesahihan baucardividen.

Di bawah keadaan biasa, sekiranya borang nyata adalah lengkapdan betul; dan baucar dividen telah disenaraikan dengan betuldan teratur dalam helaian kerja HK-3, maka tempoh purata lebihkurang satu bulan diperlukan untuk memproses. Akan tetapitempoh proses tidak lagi sedemikian jika borang diterima padahari-hari terakhir menjelang tarikh terakhir untuk pengembalianborang nyata.

2.6 Outstanding Taxes

The Institutes have been informed that the LHDNM has issued lettersregarding the outstanding taxes payable by some companies. Thecompanies are required to respond or settle the outstanding amountwithin 14 days from the date of the letter, failing which actions may betaken against the company or the directors under Section 75A of theIncome Tax Act 1967 (the Act). However, no detailed calculation wasprovided as to the derivation of the outstanding figure.

The Institutes would like to highlight the following:-

(a) the calculation of the outstanding tax payable figure shouldbe provided to enable taxpayers to understand thederivation of the said figure in order for them to respond;

__________________________________________________________________________10/04/2006 Muka Surat 10 Dari 23

(b) a reasonable time frame should be given for taxpayers toverify and revert to the LHDNM.

JAWAPAN:

(a) Pada kebiasaannya, LHDNM akan memberikan pengiraancukai masih terhutang yang kena dibayar. Akan tetapisekiranya tiada sebarang maklum balas daripada pembayarcukai dalam tempoh masa yang dinyatakan, LHDNM akanmengeluarkan surat pemberitahu cukai masih terhutangyang dijanakan oleh sistem berdasarkan baki bersih dantidak menunjukkan pengiraan terperinci. Pembayar cukaiboleh menghubungi Cawangan/Unit Pungutan yangmengendalikan kes tersebut untuk mendapatkanpengiraannya.

(b) Sekiranya tempoh masa yang diberikan tidak memadai,pembayar cukai boleh memohon untuk lanjutan masaberdasarkan fakta kes.

2.7 Issuance of Computation of Repayment

Members of the Institutes have informed that Computations ofRepayment (COR) have been issued for companies before desk auditsare carried out. It is expected that upon the receipt of a COR, therefund cheque would be sent to the taxpayers in due course. However,upon further enquiry, taxpayers have been informed that the case hasnot been selected for audit and therefore, the refund cheques cannotbe processed.

The Institutes would like to seek clarification as to when a CORwould be issued as the above practice creates confusion.

JAWAPAN:

Pengiraan bayaran balik (COR) hanya dikeluarkan selepastindakan Audit Meja diambil.

2.8 Benefit of Doubt to be given to Expatriate Employees whoseResidence Status could not be determined at the point ofSubmission of the Tax Return

In view of the manner in which the tax residence status is determined(especially for individuals who may qualify as a tax resident underSection 7(1)(b) of the Act), an expatriate who may technically not bequalified as a tax resident at the time of filing of the tax return, may bequalified as a tax resident if time up to July of the same calendar yearwas given.

__________________________________________________________________________10/04/2006 Muka Surat 11 Dari 23

In view of the above circumstance, the Institutes would like torequest the LHDNM to accept the tax return which is filed basedon tax resident basis and only raise the Additional Assessmentwithout imposing any penalties if the individual expatriate fails toqualify as a tax resident subsequently. The individual expatriatewould then settle the additional tax when the AdditionalAssessment is issued.

JAWAPAN:

Mengikut prosedur biasa, majikan dinasihatkan supaya membuatpotongan PCB pada kadar 28% bagi tempoh enam bulan pertamapekerja asing itu berada di Malaysia. Bagi pekerja asing yangdatang selepas bulan Jun, majikan perlu membuat potongan PCBpada kadar 28% bagi tempoh enam bulan dalam tahun berikutnya.

Tindakan tersebut diambil kerana:-

(a) pekerja asing menamatkan tempoh perkhidmatan merekalebih awal dari tempoh yang tercatat dalam kontrak misalnyadalam tempoh 24 jam; dan ini mengakibatkan cukai terhutangyang tidak dapat dijelaskan.

(b) pekerja asing tidak mematuhi syarat perenggan 7(1)(b) AktaCukai Pendapatan 1967 kerana tempoh ketiadaan sementara(“temporary absence”) bagi lawatan sosial sering melebihi 14hari.

PCB hanya boleh dibuat pada kadar cukai untuk pemastautin jikadapat dibuktikan bahawa pekerja asing itu berada di Malaysiasekurang-kurangnya 182 hari dalam tahun pertama.

Penentuan taraf mastautin berdasarkan permit kerja bolehdipertimbangkan mengikut fakta kes.

2.9 Resolving Appeals on a Timely Basis

Paragraph 3.7.1 of the Public Ruling 3/2001 provides that an appealmust be forwarded to the Special Commissioners of Income Tax(SCIT) within 12 months from the date of receipt and if the reviewcannot be completed within that period, the Director General of InlandRevenue (DGIR) may apply for an extension of that period, which willnot be more than 6 months.

However, feedback from the members of the Institutes indicates thatsome of the appeal cases have been outstanding for more than 2 yearsdespite numerous calls and reminders to the Assessment Branch andTechnical Division of the LHDNM. The Institutes are of the view that it

__________________________________________________________________________10/04/2006 Muka Surat 12 Dari 23

is unfair to taxpayers as they are forced to pay the tax which in somecases can be very substantial. It is regrettable to hear that a publicruling which is issued to provide guidance to the public and officers ofthe LHDNM, is not complied with by the LHDNM’s officers but it isrequired to be complied with by taxpayers. In addition, the Institutes arealso of the opinion that the review of an appeal case by the LHDNM fora maximum period of 18 months before it is forwarded to the SCIT isfar too long.

In view of the above, the Institutes request the LHDNM to resolveall appeals on a timely basis and expedite the process of thereview in accordance with paragraph 3.7.1 of the Public Ruling3/2001.

JAWAPAN:

Keadaan ini tidak sepatutnya berlaku. Pihak Persatuan dimintamenghubungi LHDNM sekiranya terdapat kes sedemikian. Arahantelah dikeluarkan kepada semua Pengarah Negeri supayamemantau dan memastikan kes-kes rayuan kepada PesuruhjayaKhas Cukai Pendapatan diselesaikan dalam tempoh tidakmelebihi 12 bulan walaupun lanjutan masa selama 6 bulan bolehdipohon.

2.10. Timely Responses from the LHDNM

2.10.1 Submission of lower tax estimate

Based on the general guideline issued by the LHDNM, FormCP204 which is submitted with a lower tax estimate than theamount allowed by the Act must be accompanied with anappeal letter with valid reasons for the LHDNM’sconsideration. Consideration of the appeal will be based on themerit of each case as stated in Paragraph 2.1 of the minutesof Operations Dialogue held on 16 February 2005.

Members of the Institutes have highlighted that the reply to theabove application is given verbally by the LHDNM’s officerswithout any written evidence for approval or disapproval. Theinstruction to disregard the Form CP205 which was sent earlieris also given verbally.

__________________________________________________________________________10/04/2006 Muka Surat 13 Dari 23

JAWAPAN:

Jika surat rayuan diterima bersama dengan borangAnggaran Cukai Yang Kena Dibayar (CP 204), kes tersebutakan diproses dan diluluskan/tidak diluluskanberdasarkan kepada fakta kes. Status kelulusan akandimasukkan ke dalam sistem komputer dan suratkelulusan (CP 216) akan dikeluarkan oleh sistem kepadapembayar cukai dalam tempoh purata lebih kurang satubulan. Pihak Persatuan boleh menghubungi PusatPemprosesan di Pandan Indah sekiranya CP 216 tidakditerima.

2.10.2 Letter for refund/set-off of credit balances

The Institutes were informed that letters for refund of creditbalances are not replied to even though follow-up has beenmade. For those cases where the taxes have not beenassessed yet, the application letters will be put in a wait caseand the file will not be distributed to the officers for furtheraction until the taxpayers have done some follow up andrequested the officer in charge to look into the refundapplication.

Members have come across situations whereby the approvalto set-off the instalment payments with the credit balance wasgiven verbally by the LHDNM’s officer and the instalmentpayment was discontinued the accordingly. After some time,the taxpayers received a statement showing penalties forthose instalments which were allowed to be set-off. Uponfurther enquiry, members were informed that the officer hadresigned and the new person-in-charge alleged that there wasno proof of such approval.

In view of the above situations, the Institutes would like torequest the LHDNM to update the computerised systemon a timely basis and provide a written response (withdetailed breakdown for those cases related to taxbalances) to all written applications submitted bytaxpayers on a timely basis to avoid unnecessaryconfusion and disputes which is unproductive for allconcerned.

__________________________________________________________________________10/04/2006 Muka Surat 14 Dari 23

JAWAPAN:

Untuk mempercepatkan proses bayaran balik,penggunaan e-filing digalakkan. Jika tiada maklum balaskepada permohonan untuk bayaran balik/“set-off”,pembayar cukai dinasihatkan supaya merujuk semulakepada Cawangan/Unit Pungutan yang mengendalikankesnya. Bagi kes “set-off”, adalah dinasihatkan supayamendapatkan jawapan/kelulusan secara bertulis daripadaCawangan/Unit Pungutan yang berkenaan untukmengelakkan sebarang masalah/pertikaian kelak.

2.11 Assignment of Tax Officers

The Institutes have been informed that there are instances where noofficers have been assigned to handle specific cases at the CawanganSyarikat. In the event an officer has been assigned, the officer isunable to provide an indication as to when the particular case can befinalised.

The Institutes wish to propose that the assignment of officers bedone quickly to expedite the finalisation of cases, especiallywhere revised computations submitted involve tax refunds.Taxpayers are imposed with various deadlines to comply forexample, within 7 months after the financial year end to submitthe tax returns, within 30 days before the beginning of thefinancial year to submit the CP 204, etc. Likewise, it is also hopedthat officers are able to provide an indication of when the casescan be finalised.

JAWAPAN:

Mengikut Pekeliling yang telah dikeluarkan, kes-kes audit mestidiselesaikan dalam tempoh 3 bulan. Pihak Persatuan dimintamengemukakan senarai kes-kes yang melebihi tempoh 3 bulanwalaupun dokumen-dokumen yang dikehendaki oleh LHDNMtelah dikemukakan oleh pembayar cukai. Akan tetapi, untukkes-kes di mana taksiran tambahan dibangkitkan keranadokumen-dokumen tidak dapat dikemukakan kepada LHDNMsebagai bukti, pembayar cukai boleh membuat rayuan kepadaPesuruhjaya Khas Cukai Pendapatan.

Oleh kerana kebanyakan kes yang dimaksudkan adalah kesrayuan untuk kurangan cukai dan pembayaran balik, LHDNMmenasihatkan pihak Persatuan supaya anggaran cukai tidakdibuat dengan sewenang-wenangnya walaupun kesuntukan masauntuk mengemukakan borang nyata mengikut tempoh yangditetapkan.

__________________________________________________________________________10/04/2006 Muka Surat 15 Dari 23

2.12 Bilingual Income Tax Returns

With Malaysia opening its doors to foreign manpower, we have seenan increasing influx of expatriates seeking career opportunities inMalaysia. Some of these expatriates may eventually qualify asMalaysian tax residents due to their presence in Malaysia andtherefore, will be required under the legislation to discharge their taxresponsibilities. With the recent implementation of self-assessmentsystem for individuals, these resident expatriates need to understandtheir obligations in order for them to fully discharge theirresponsibilities.

The Institutes would like to propose that the prescribed incometax return be available in both Bahasa Malaysia and English forsubmission purposes. This will be seen as a genuine gesture ofthe Government to attract foreign expatriates.

JAWAPAN:

Hanya Borang M ditetapkan (“prescribed”) dalam BahasaInggeris. Versi Bahasa Inggeris untuk borang nyata lain yangditetapkan dalam Bahasa Malaysia boleh diperolehi dari lamanweb LHDNM (http://www.hasil.org.my) untuk rujukan dan tidakboleh digunakan sebagai borang nyata ditetapkan untuk tujuanpengemukaan.

2.13 Management Changes in LHDNM

The Institutes noted that there have been recent managementchanges in the LHDNM.

The Institutes would like to request that in the spirit ofco-operation and dissemination of information, the LHDNM informits dialogue partners i.e. the Institutes of any such changes sothat these changes can be disseminated. Perhaps the PublicRelations Department could be assigned to communicate suchinformation to the Institutes.

JAWAPAN:

Pihak Persatuan boleh melayari laman web LHDNM untukmendapatkan maklumat berkenaan.

Atas permintaan pihak Persatuan, maklumat seperti nama,jabatan/cawangan dan nombor telefon Ketua-Ketua di Ibu Pejabatdan Cawangan akan dipaparkan/dikemaskinikan dalam lamanweb.

__________________________________________________________________________10/04/2006 Muka Surat 16 Dari 23

2.14 Extension of filing deadline for December year-end companies (refer to Minutes of Operations dialogue held on 16 February2005)

Members of the Institutes have reported difficulties in coping with thevolume of tax returns that need to be filed for December-year-endcompanies in July every year despite taking various measures such asincreasing manpower, etc.

Since taxes are being paid by companies under the instalmentscheme, the Institutes would like to request the LHDNM to grant anadministrative concession of an automatic two-week extension of timeto file the tax returns for December year-end companies. The two-weekextension of time is needed by the tax agents to handle the largevolume of tax returns for such companies.

The LHDNM has stated that for companies which close their accountson 31 December, the Forms C and R have to be submitted inaccordance with the deadline set by the Act (on or before 31 July2005). Nevertheless, no penalty was imposed on taxpayers if theForms are received by the LHDNM on or before 14 August 2005.

The Institutes would like to confirm that the above administrativeconcession is still applicable for this year. Hence, no penalty willbe imposed on taxpayers if the Forms C and R of the Decemberyear-end companies are received by the LHDNM on or before 14August 2006.

JAWAPAN:

Syarikat dikehendaki mengembalikan Borang C dan Borang Rmengikut tarikh yang ditetapkan oleh undang-undang.

Sebagai konsesi, penalti tidak akan dikenakan sekiranya borangnyata diterima dalam tempoh 14 hari dari tarikh terakhir untukpengembalian borang nyata. Untuk borang nyata yang diterimaselepas tempoh 14 hari tersebut di mana penalti telah dikenakan,rayuan boleh dipertimbangkan jika dapat dibuktikan bahawa iadihantar pada atau sebelum tarikh terakhir untuk pengembalianborang nyata.

Layanan yang sama terpakai untuk bayaran baki cukaipendapatan di bawah seksyen 103(1) Akta Cukai Pendapatan1967.

__________________________________________________________________________10/04/2006 Muka Surat 17 Dari 23

2.15 Companies under Liquidation

2.15.1 Issuance of clearance letter (refer to Minutes of Operations Dialogue held on 15 April2002)

During the dialogue with the Operations Division of theLHDNM held on 15 April 2002, the LHDNM stated thatinstructions would be given to the assessment branches toexpedite the issuance of clearance letters for companies underliquidation.

However, members of the Institutes have reported that thesituation has not improved over these years and they are stillexperiencing delays from the Assessment Branch to obtainclearance letter for companies under liquidation as a result ofMembers’ Voluntary Liquidations or strike-off cases underSection 308 of the Companies Act, 1965. Undue delay of theissuance of the clearance letter only increases the compliancecosts of the taxpayer.

In this regard, the Institutes would like to propose that theclearance letter be issued within one month from the dateof the application to the Assessment Branch, failing whicha NIL deemed assessment will be treated as the finalclearance letter from the LHDNM.

JAWAPAN:

Pihak Persatuan diminta memberikan butiran sekiranyamasih terdapat kes-kes kelewatan dalam pengeluaransurat penyelesaian.

2.15.2 Requirement to maintain records

Normally, books and records will be destroyed within a shortperiod of time after liquidation or strike-off of a company asthere are no funds to store such records once the entity isliquidated.

In view of the above, the Institutes would like to requestfor an exemption from the requirement of maintainingbooks and records of a liquidated company.

__________________________________________________________________________10/04/2006 Muka Surat 18 Dari 23

JAWAPAN:

Rekod-rekod syarikat yang telah dibubarkan hanya bolehdimusnahkan lebih awal sekiranya semua urusanberkaitan cukai pendapatan syarikat telah diselesaikan.Jika tidak, keperluan menyimpan rekod perlu dipatuhiseperti biasa.

3. Isu-isu Tambahan daripada MIT / MIA / MICPA

3.1 Delay in issuance of receipt for withholding tax payment

Taxpayers have faced penalty as a result of delay in the issuance ofreceipt for withholding tax payment, which have been remitted to theLHDNM within one month from date of payment (via courier companyand has an acknowledgement of receipt by the LHDNM).

For example, a courier company handed a cheque to LHDNM on 5February 2005 i.e. within one month of the payment (as peracknowledgement stamp of LHDNM). However the official receipt wasonly issued on 4 March 2005 (one month later). Due to the delay in theissuance of the receipt by LHDNM, a notification was issued byLHDNM on 16 January 2006 and penalty for late payment wasimposed on the taxpayer.

Such incident has caused considerable inconvenience to taxpayers asthe taxpayers had to retrieve their records/documents in order to provethat the withholding tax was paid on time. Taxpayers have alsoexperienced penalties imposed for alleged late payment which tookplace many years ago (in some instances more than 8 years ago).Obviously, the taxpayers would not be able to remember the facts orcould not locate the documents and thus, are forced to pay the penalty.

The Institutes would like to propose that the LHDNM:

(a) Issue receipts for withholding tax immediately on paymentof the withholding tax

(b) Do not open old cases for the imposition of penalty forgenuine cases.

JAWAPAN:

(a) Sekiranya bayaran dibuat di kaunter bayaran LHDNM, resitrasmi akan dikeluarkan pada hari bayaran itu dibuat.Apabila bayaran diterima melalui pos, “time-lag”kadangkala berlaku di antara tarikh penerimaan dokumendan tarikh resitan kerana masa diperlukan untuk

__________________________________________________________________________10/04/2006 Muka Surat 19 Dari 23

memproses dokumen yang diterima dengan banyak melaluipos. Akan tetapi, sebarang kenaikan cukai kerana lewatbayaran adalah berdasarkan tarikh penerimaan dokumendan bukannya tarikh resitan.

(b) Kes lama yang disemak semula dan dikenakan penaltikerana lewat bayaran boleh dirujuk kepada LHDNM untukpertimbangan berdasarkan fakta kes.

Semakan semula kes lama dihadkan kepada tempoh 7tahun dan pihak Persatuan boleh merujuk kepada LHDNMjika terdapat kes yang disemak semula berhubung cukaipegangan yang telah dibayar lebih daripada 7 tahun dahulu.

3.2 Repayment cases (due to section 110 set-off)

When carrying out desk audits for repayment cases, the LHDNM hadrequested taxpayers to submit photocopies of the Form BE, amongother items.

The Institutes wish to clarify the procedure undertaken by LHDNMin processing repayments arising from S110 set-off and the needfor the Form BE to be submitted again. The Institutes are of theview that taxpayers should not be made to re-submit a photocopyof the Form BE as the original form has already been submitted tothe LHDNM before.

JAWAPAN:

Sila rujuk jawapan untuk Perkara 2.5.

4. Isu daripada MAICSA

Employee Share Option Scheme Benefit Public Ruling No.4/2004 dated 9/12/2004Effective from Year of Assessment 2004

IRB Ruling

Employer is required to deduct PCB on the benefit that arises from ESOS inthe month the option is exercised based on PCB schedule. However,employee has the option to pay the tax by instalments through PCB up to amaximum of 12 months from the month in which the option is exercised.

If employee chooses to pay by himself the tax at the end of the year,employer must ensure that the election made by employee is done in writing.

__________________________________________________________________________10/04/2006 Muka Surat 20 Dari 23

Issues / problems faced by employer

The provision of a variable number of instalment payment options toemployee would cause much difficulty to employer in monitoring PCBdeductions, especially when there are multiple options exercised during themonth or in the same year with the number of instalment varies for eachexercise of options.

In addition, where the PCB deductions spill over to the next calendar year, theemployee would have difficulty in determining the balance of tax payablewhen the Form BE is filed with the IRB in April the following year besidescreating administrative work to the employer.

Proposal IRB to waive the requirement to deduct PCB in respect of tax liabilityarisingfrom the exercise of ESOS. Employee should be required to pay taxarising from the exercise of ESOS at the time Form BE is filed. This is toprovide time to the employee to cash out part of their investment to pay tax.With this procedure, no time and resources are wasted on modifying thepayroll system and monitoring of PCB deductions.

Catatan Tambahan:

Pihak Persatuan menyuarakan kesukaran majikan untuk melaksanakantanggungjawabnya mengikut Ketetapan Umum tersebut terutamanya berhubungESOS yang ditawarkan oleh syarikat asing ( misalnya syarikat induk ) di luarMalaysia. Ini adalah kerana tiada mekanisme yang mewajibkan pekerja untukmemberitahu majikannya bila haknya dilaksanakan di bawah opsyen tersebut. Olehkerana ESOS berkenaan bukan ditawarkan oleh majikan di Malaysia, maka ia tidakdilaporkan dalam penyata pendapatan (Borang EA) pekerja.

JAWAPAN:

LHDNM berpendapat bahawa majikan di Malaysia sepatutnyamengetahui berkenaan ESOS yang ditawarkan itu kerana ia beradadalam kumpulan syarikat yang sama dan berkaitan dengan penggajianyang dijalankan di Malaysia. Oleh itu LHDNM menasihatkan supayaESOS tersebut dimasukkan dalam Borang EA. Pihak Persatuan dimintamengemukakan kertas kerja berkenaan isu tersebut untuk pertimbanganLHDNM.

Buat masa sekarang, Ketetapan Umum Bil. 4/2004 masih terpakai. Jikamajikan mendapati sukar untuk membuat dan memantau PCB, majikandigalakkan untuk membuat potongan PCB sekaligus sebaik sahajaopsyen dilaksanakan ataupun memastikan pekerja itu menyatakanpilihannya secara bertulis sekiranya membayar sendiri.

__________________________________________________________________________10/04/2006 Muka Surat 21 Dari 23

5. Perkara Lain Yang Berbangkit

5.1 Ketetapan Umum yang baru untuk laman web

Menurut pihak Persatuan, Ketetapan Umum yang baru biasanyadimasukkan dalam laman web LHDNM selepas tarikh mulakuatkuasanya.

JAWAPAN:

LHDNM akan memastikan bahawa Ketetapan Umum yang barudimasukkan dalam laman web pada atau sebelum tarikhberkuatkuasanya.

5.2 Penggunaan Sijil Digital Pelanggan oleh Ejen Cukai

Ejen cukai dimaklumkan bahawa sijil digital sendiri ataupun sijildigital pelanggan boleh digunakan untuk mengemukakan borangnyata pelanggan berkenaan. Walaupun sudah ada surat kuasaperlantikan sebagai ejen cukai daripada pelanggan, ejen cukaidinasihatkan supaya mendapatkan surat kebenaran pelangganuntuk mengendalikan sijil digital mereka seperti mendapatkan sijildigital bagi pihak pelanggan dan menggunakan nombor peribadisijil digital pelanggan untuk mengemukakan borang.

Pihak Persatuan mencadangkan supaya sijil digital khasdikeluarkan untuk membolehkan ejen-ejen cukai mengemukakanborang nyata bagi pihak pelanggan mereka. Cadangan tersebutakan dipertimbangkan.

5.3 Kadar pematuhan Borang C dan Borang R

Pihak Persatuan ditanya mengapa kadar pematuhan Borang Rtidak setara dengan kadar pematuhan Borang C. Pihak Persatuanmenerangkan bahawa mengikut kebiasaan, kedua-dua borangdisediakan bersama.

Walau bagaimanapun, LHDNM meminta pihak Persatuan supayamemastikan Borang R dikemukakan oleh pelanggan syarikat.

__________________________________________________________________________10/04/2006 Muka Surat 22 Dari 23

5.4 Borang-borang baru untuk Relif Kumpulan

Dua borang baru diperkenalkan iaitu:

5.4.1 Borang C (RK-T) untuk syarikat menuntut; dan

5.4.2 Borang C (RK-S) untuk syarikat menyerah.

Borang-borang tersebut boleh dimuat turun dari laman webLHDNM.

5.5 Lesen ejen cukai

Pihak Persatuan meminta supaya dipercepatkan prosespengeluaran/pembaharuan lesen ejen cukai.

Tuan Pengerusi menjelaskan bahawa syarat-syarat danpengeluaran/pembaharuan lesen ejen cukai adalah di bawahkuasa pejabat Perbendaharaan tetapi LHDNM akan cubamempercepatkannya.

6. Penutup

Mesyuarat ditangguhkan pada pukul 12.00 tengahari dengan ucapan terimakasih oleh Tuan Pengerusi kepada para hadirin Majlis Dialog tersebut.

__________________________________________________________________________10/04/2006 Muka Surat 23 Dari 23

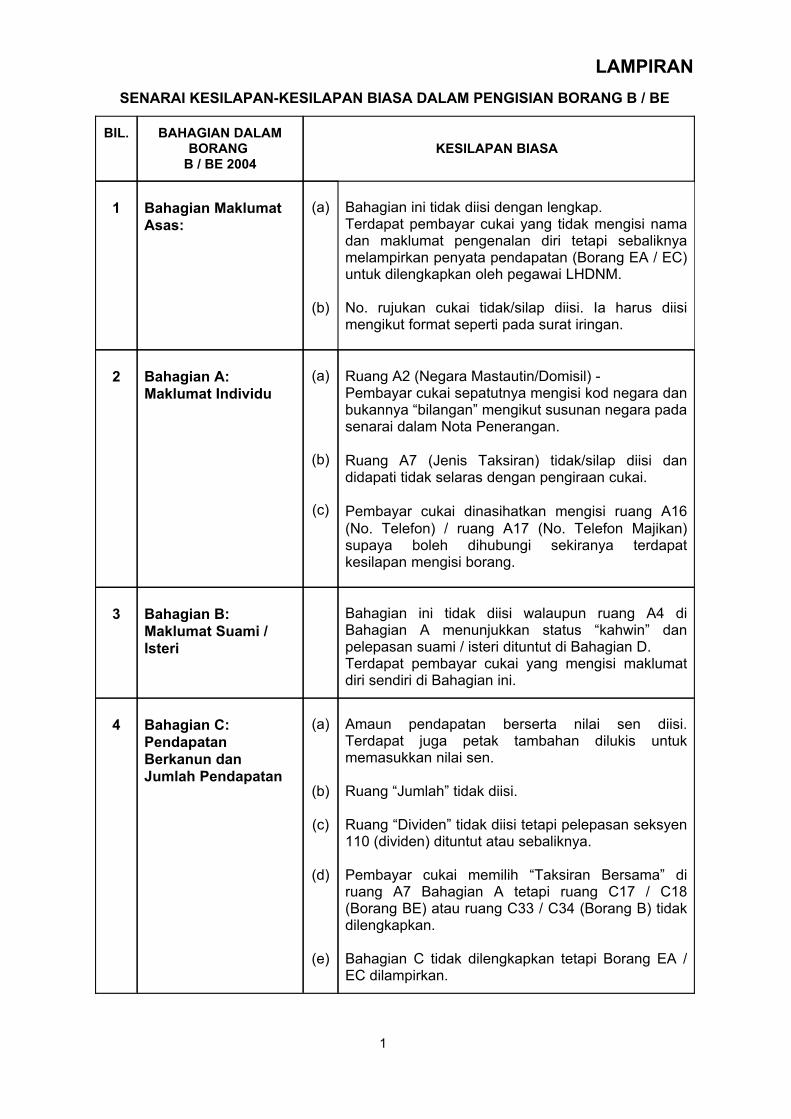

LAMPIRANSENARAI KESILAPAN-KESILAPAN BIASA DALAM PENGISIAN BORANG B / BE

Amaun pendapatan berserta nilai sen diisi.Terdapat juga petak tambahan dilukis untukmemasukkan nilai sen.

Ruang “Jumlah” tidak diisi.

Ruang “Dividen” tidak diisi tetapi pelepasan seksyen110 (dividen) dituntut atau sebaliknya.

Pembayar cukai memilih “Taksiran Bersama” diruang A7 Bahagian A tetapi ruang C17 / C18(Borang BE) atau ruang C33 / C34 (Borang B) tidakdilengkapkan.

Bahagian C tidak dilengkapkan tetapi Borang EA /EC dilampirkan.

(a)

(b)

(c)

(d)

(e)

Bahagian C: PendapatanBerkanun danJumlah Pendapatan

4

Bahagian ini tidak diisi walaupun ruang A4 diBahagian A menunjukkan status “kahwin” danpelepasan suami / isteri dituntut di Bahagian D.Terdapat pembayar cukai yang mengisi maklumatdiri sendiri di Bahagian ini.

Bahagian B: Maklumat Suami /Isteri

3

Ruang A2 (Negara Mastautin/Domisil) - Pembayar cukai sepatutnya mengisi kod negara danbukannya “bilangan” mengikut susunan negara padasenarai dalam Nota Penerangan.

Ruang A7 (Jenis Taksiran) tidak/silap diisi dandidapati tidak selaras dengan pengiraan cukai.

Pembayar cukai dinasihatkan mengisi ruang A16(No. Telefon) / ruang A17 (No. Telefon Majikan)supaya boleh dihubungi sekiranya terdapatkesilapan mengisi borang.

(a)

(b)

(c)

Bahagian A: Maklumat Individu

2

Bahagian ini tidak diisi dengan lengkap. Terdapat pembayar cukai yang tidak mengisi namadan maklumat pengenalan diri tetapi sebaliknyamelampirkan penyata pendapatan (Borang EA / EC)untuk dilengkapkan oleh pegawai LHDNM.

No. rujukan cukai tidak/silap diisi. Ia harus diisimengikut format seperti pada surat iringan.

(a)

(b)

Bahagian MaklumatAsas:

1

KESILAPAN BIASA BAHAGIAN DALAM

BORANG B / BE 2004

BIL.

1

Sebahagian borang terdiri daripada borang asal dansebahagian lagi borang fotostat.

Muka surat borang yang dikemukakan tidakmencukupi.

Borang fofostat diisi dan dihantar kepada LHDNM.

Menggunakan borang nyata tahun kebelakanganuntuk melaporkan pendapatan tahun semasa.

(a)

(b)

(c)

(d)

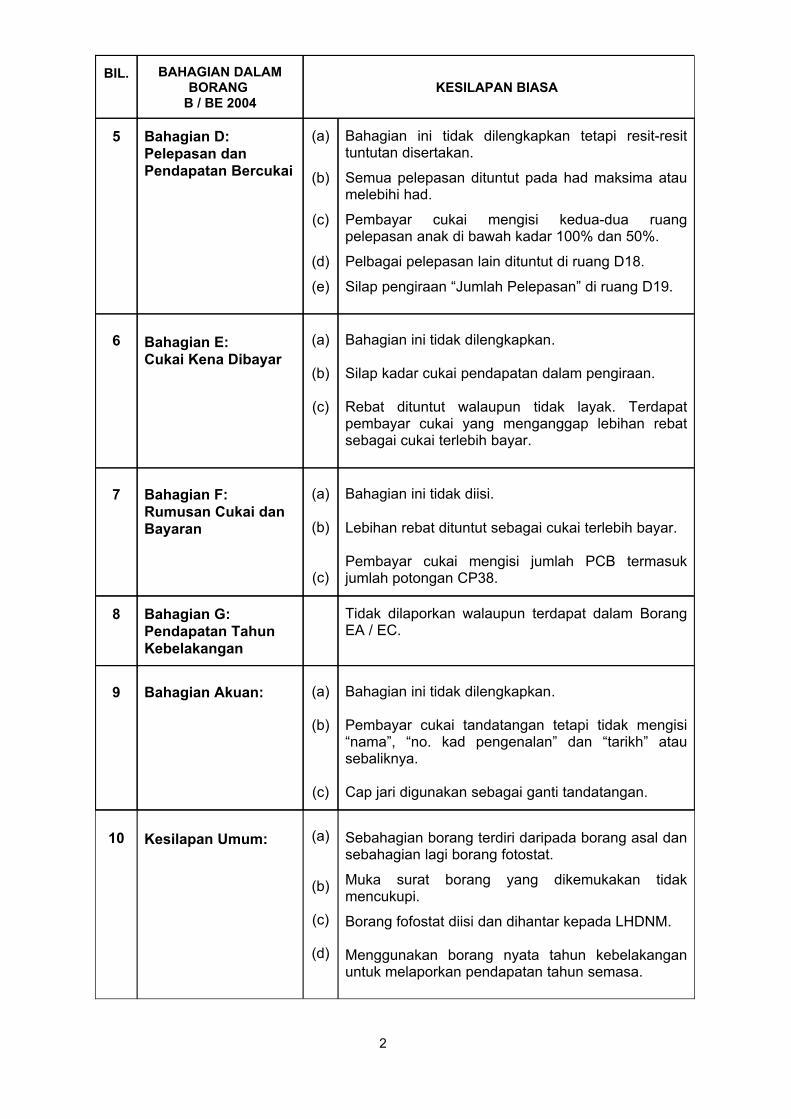

Kesilapan Umum:10

Bahagian ini tidak dilengkapkan.

Pembayar cukai tandatangan tetapi tidak mengisi“nama”, “no. kad pengenalan” dan “tarikh” atausebaliknya.

Cap jari digunakan sebagai ganti tandatangan.

(a)

(b)

(c)

Bahagian Akuan:9

Tidak dilaporkan walaupun terdapat dalam BorangEA / EC.

Bahagian G:Pendapatan TahunKebelakangan

8

Bahagian ini tidak diisi.

Lebihan rebat dituntut sebagai cukai terlebih bayar.

Pembayar cukai mengisi jumlah PCB termasukjumlah potongan CP38.

(a)

(b)

(c)

Bahagian F: Rumusan Cukai danBayaran

7

Bahagian ini tidak dilengkapkan.

Silap kadar cukai pendapatan dalam pengiraan.

Rebat dituntut walaupun tidak layak. Terdapatpembayar cukai yang menganggap lebihan rebatsebagai cukai terlebih bayar.

(a)

(b)

(c)

Bahagian E: Cukai Kena Dibayar

6

Bahagian ini tidak dilengkapkan tetapi resit-resittuntutan disertakan.

Semua pelepasan dituntut pada had maksima ataumelebihi had.

Pembayar cukai mengisi kedua-dua ruangpelepasan anak di bawah kadar 100% dan 50%.

Pelbagai pelepasan lain dituntut di ruang D18.

Silap pengiraan “Jumlah Pelepasan” di ruang D19.

(a)

(b)

(c)

(d)

(e)

Bahagian D: Pelepasan danPendapatan Bercukai

5

KESILAPAN BIASA BAHAGIAN DALAM

BORANG B / BE 2004

BIL.

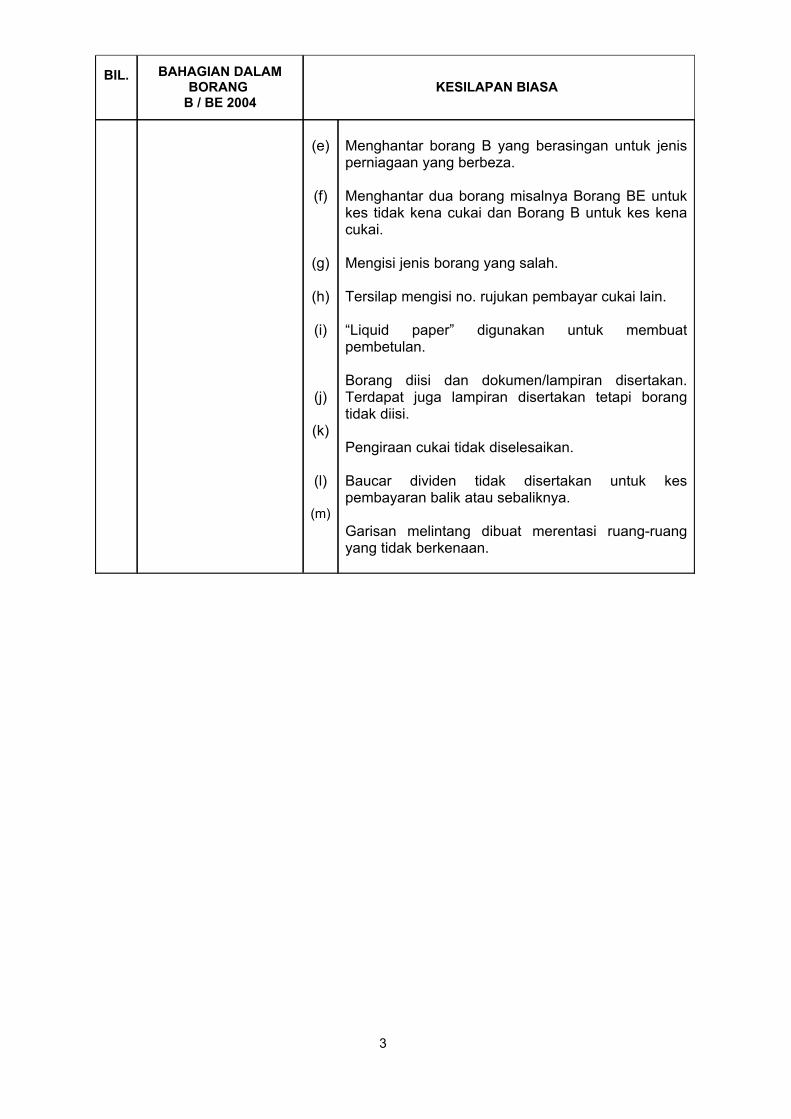

2

Menghantar borang B yang berasingan untuk jenisperniagaan yang berbeza.

Menghantar dua borang misalnya Borang BE untukkes tidak kena cukai dan Borang B untuk kes kenacukai.

Mengisi jenis borang yang salah.

Tersilap mengisi no. rujukan pembayar cukai lain.

“Liquid paper” digunakan untuk membuatpembetulan.

Borang diisi dan dokumen/lampiran disertakan.Terdapat juga lampiran disertakan tetapi borangtidak diisi.

Pengiraan cukai tidak diselesaikan.

Baucar dividen tidak disertakan untuk kespembayaran balik atau sebaliknya.

Garisan melintang dibuat merentasi ruang-ruangyang tidak berkenaan.

(e)

(f)

(g)

(h)

(i)

(j)

(k)

(l)

(m)

KESILAPAN BIASA BAHAGIAN DALAM

BORANG B / BE 2004

BIL.

3