menara ta one, 22 jalan p. ramlee, 50250 kuala...

TRANSCRIPT

ta securities holdings berhad(14948-M)

A member of the ta group

IN IT IAT ING COVERAGE

Thursday, December 02, 2010 FBM KLCI: 1,485.42 Sector: Healthcare

MENARA TA ONE, 22 JALAN P. RAMLEE, 50250 KUALA LUMPUR, MALAYSIA TEL: +603-20721277 / FAX: +603-20325048

Page 1 of 13

‐

KPJ Healthcare Berhad TP:RM4.32(+15.07%)

Care For Life Last traded: RM3.75 THIS REPORT IS STRICTLY FOR INTERNAL CIRCULATION ONLY*

BUY

TA Research Team Coverage

+603-2072-1277 ext:1634

www.taonline.com.my

EXECUTIVE SUMMARY We are initiating coverage on KPJ Healthcare Berhad (KPJ) with a BUY recommendation and a target price of RM4.32. This implies an upside potential of 15.07% to its last closing of RM3.75. KPJ is the healthcare division of Johor Corporation and it’s principal activity is ownership and the management of private specialist hospitals. KPJ is majority owned by Johor Corporation with direct / indirect interest of approximately 42.86%. Kumpulan Waqaf An‐Nur Berhad, Skim Amanah Saham Bumiputera and Employees Provident Fund Board hold approximately 8.38%, 8.68% and 8.97% respectively. We advocate our investment thesis for KPJ to its:

1) Solid financial profile and positive outlook in the healthcare industry;

2) Experienced team (29 years experiences in healthcare business) with a viable business model; and

3) Attractive valuation as compared to regional peers. We project KPJ’s FY10‐13 earnings to grow at a CAGR of approximately 17% on the back of 1) 5‐10% growth in patients; 2) 5‐10% growth in patients’ expenditure; and 3) 5% growth in contribution from associates. Besides, our FY10‐FY13 earnings projections are premised on the following assumptions:‐

1) KPJ continue to expand its fleet of hospitals (which includes the opening of new hospitals and expansion of its existing hospitals); and

2) Capex of RM150‐180mn for construction / upgrading of hospitals and replenishment of medical equipment.

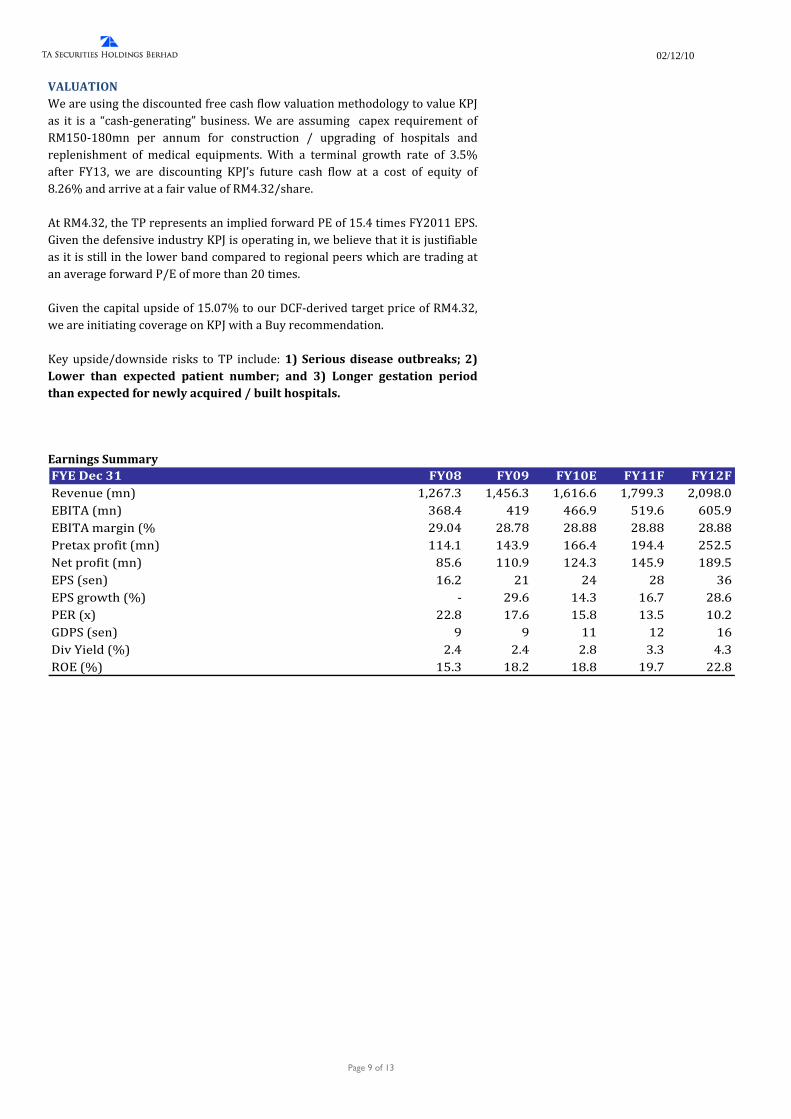

Key upside/downside risks to TP include: 1) Serious disease outbreaks; 2) Lower than expected patient number; and 3) Longer gestation period than expected for newly acquired / built hospitals. Earnings Summary FYE Dec 31 FY08 FY09 FY10E FY11F FY12F Revenue (mn) 1,267.3 1,456.3 1,616.6 1,799.3 2,098.0 EBITA (mn) 368.4 419.0 466.9 519.6 605.9 EBITA margin (%) 29.04 28.78 28.88 28.88 28.88 Pretax profit (mn) 114.1 143.9 166.4 194.4 252.5 Net profit (mn) 85.6 110.9 124.3 145.9 189.5 EPS (sen) 16.2 21 24 28 36 EPS growth (%) ‐ 29.6 14.3 16.7 28.6 PER (x) 22.8 17.6 15.8 13.5 10.2 GDPS (sen) 9 9 11 12 16 Div Yield (%) 2.4 2.4 2.8 3.3 4.3 ROE (%) 15.3 18.2 18.8 19.7 22.8

Share InformationBloomberg Code KPJ MKStock Code 5878Listing Main MarketShare Cap (mn) 528.9Market Cap (RMmn) 1,999.2 Par Value 0.552‐wk Hi/Lo (RM) 3.85 / 2.0512‐mth Avg Daily Vol ('000 shrs) 1176.8Estimated Free Float (%) 32Beta 0.635Major Shareholders (%)

Johor Corporation (42.86)Kumpulan Waqaf An‐Nur Berhad (8.38)

Emplyees Provident Fund (8.97)Skim Amanah Saham Bumiputera (8.68)

Forecast Revision

FY10 FY11Forecast Revision ‐ ‐Net Profit (RMmn) 124.3 145.9Consensus 116.3 132.6TA's / Consensus (%) 107 110Previous Rating ‐ Financial Indicators

FY10 FY11Gearing (x) 0.6 0.6CFPS (sen) 1 nmPrice/CFPS (x) 375 nmROE (%) 18.88 19.67NTA/Share (RM) 1.11 1.26Price/NTA (x) 3.38 2.98 Share Performance (%)Price Change KPJ FBM KLCI1 mth 1.08 (1.41) 3 mth 8.70 3.07 6 mth 25.84 16.41 12 mth 76.06 16.85

02/12/10

Page 2 of 13

COMPANY BACKGROUND KPJ healthcare Berhad (KPJ) has been in the healthcare business for 29 years and is one of Malaysia’s largest healthcare enterprises with a network of 19 hospitals in the country and another 2 hospitals in Indonesia. Its principal activity is ownership and the management of private specialist hospitals. Other business portfolios include hospital development and commissioning, nursing education, healthcare technical services, health sciences, pathology services and central procurement. Since the establishment of its first hospital in 1981, KPJ has grown from strength to strength. Starting with two hospitals when it was listed in 1994. KPJ Healthcare Berhad has transformed into the nation’s leading private healthcare service provider and is increasingly being seen as the sector’s benchmark as competition rises. KPJ leads the Malaysian private healthcare industry with a network of 19 hospitals that span the lenghth and breath of the country. These hospitals are located in Kuala Lumpur, Selangor, Johor, Negeri Sembilan, Perak, Penang, Kedah, Pahang, Kelantan, Sabah and Sarawak. These hospitals are mainly community‐based and receive consistent, strong support and loyalty from the community where the respective hospitals are located. Regionally, the Group continues to manage 2 hospitals in Jakarta, Indonesia. The Group is also actively involved in the medical education sector through the KPJ International College of Nursing and Health Sciences. KPJ had ventured into the retirement village business in Australia by purchasing 51% equity interest in Jeta Gardens Waterford Trust (JGWT). JGWT is the owner of the aged care facility with 108 beds, 23 units of retirement villas and 32 units of apartments known as ‘Jeta Garden,’ which is located on a 54‐acres land in Queensland, Australia. KPJ made it to the list of Malaysia’s Top 100 Companies in Bursa Malaysia given the increase in market capitalization. As at 31 December 2009, KPJ was ranked 91st out of the 100 top companies. KPJ has set up a first Asia Islamic Hospitality REIT, AL‐‘AQAR KPJ REIT in 2007. As at 22 November 2010, KPJ holds approximately 49% stake in AL‐‘AQAR KPJ REIT. AL‐‘AQAR KPJ REIT is an investment vehicle investing in Syariah‐compliant real estates. The key objective of AL‐‘AQAR KPJ REIT is to provide unitholders stable distributions and the increase net asset value over the long run. MAJOR SHAREHOLDER / MANAGEMENT KPJ is majority owned by Johor Corporation with direct / indirect interest of approximately 42.86%. Kumpulan Waqaf An‐Nur Berhad, Skim Amanah Saham Bumiputera and Employees Provident Fund Board hold approximately 8.97%, 8.68% and 8.38% respectively. The Managing Director of KPJ, Datin Paduka Siti Sa’diah Sheik Bakir is committed in promoting excellence in healthcare. She is the President of the Malaysian Society for Quality in Health, elected since its inception in 1997 to date. Datin Paduka is highly rated as a professional manager. As a regonition of her excellence performance, she was awarded Malaysia’s CEO of the year 2009.

Share Price relative to the FBM KLCI

Source: Bloomberg

02/12/10

Page 3 of 13

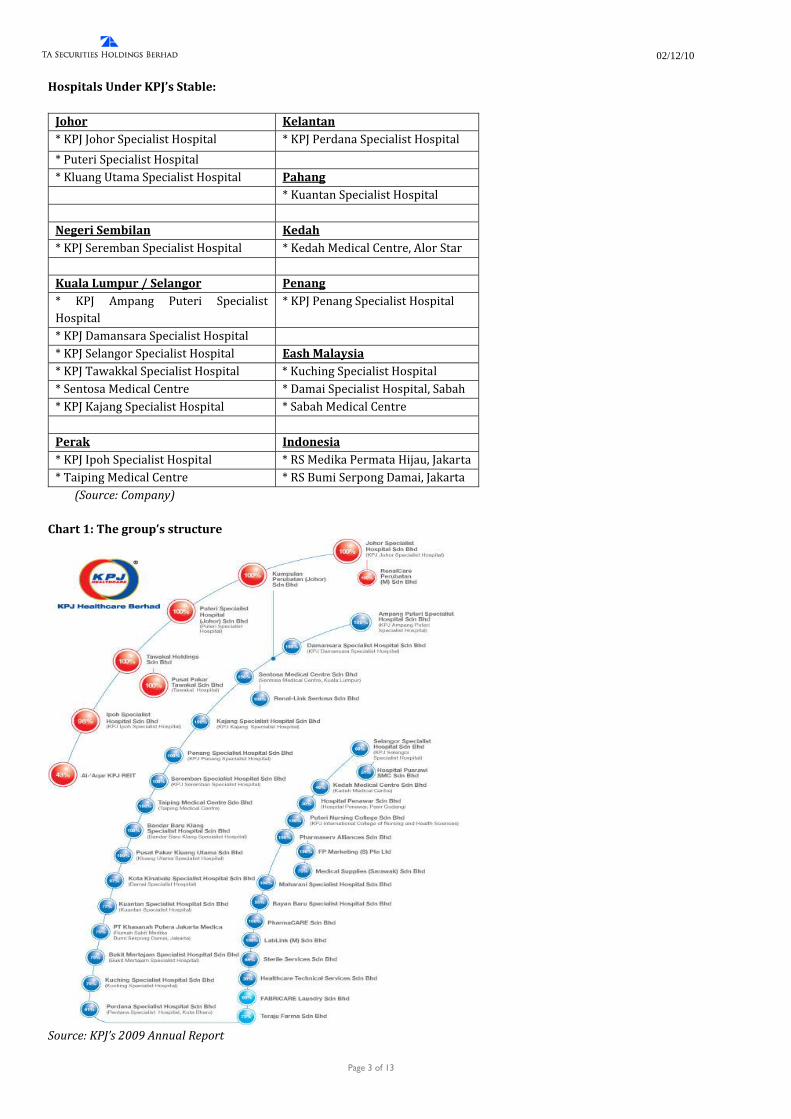

Hospitals Under KPJ’s Stable: Johor Kelantan * KPJ Johor Specialist Hospital * KPJ Perdana Specialist Hospital * Puteri Specialist Hospital * Kluang Utama Specialist Hospital Pahang * Kuantan Specialist Hospital Negeri Sembilan Kedah * KPJ Seremban Specialist Hospital * Kedah Medical Centre, Alor Star Kuala Lumpur / Selangor Penang * KPJ Ampang Puteri Specialist Hospital

* KPJ Penang Specialist Hospital

* KPJ Damansara Specialist Hospital * KPJ Selangor Specialist Hospital Eash Malaysia * KPJ Tawakkal Specialist Hospital * Kuching Specialist Hospital * Sentosa Medical Centre * Damai Specialist Hospital, Sabah * KPJ Kajang Specialist Hospital * Sabah Medical Centre Perak Indonesia * KPJ Ipoh Specialist Hospital * RS Medika Permata Hijau, Jakarta * Taiping Medical Centre * RS Bumi Serpong Damai, Jakarta

(Source: Company) Chart 1: The group’s structure

Source: KPJ’s 2009 Annual Report

02/12/10

Page 4 of 13

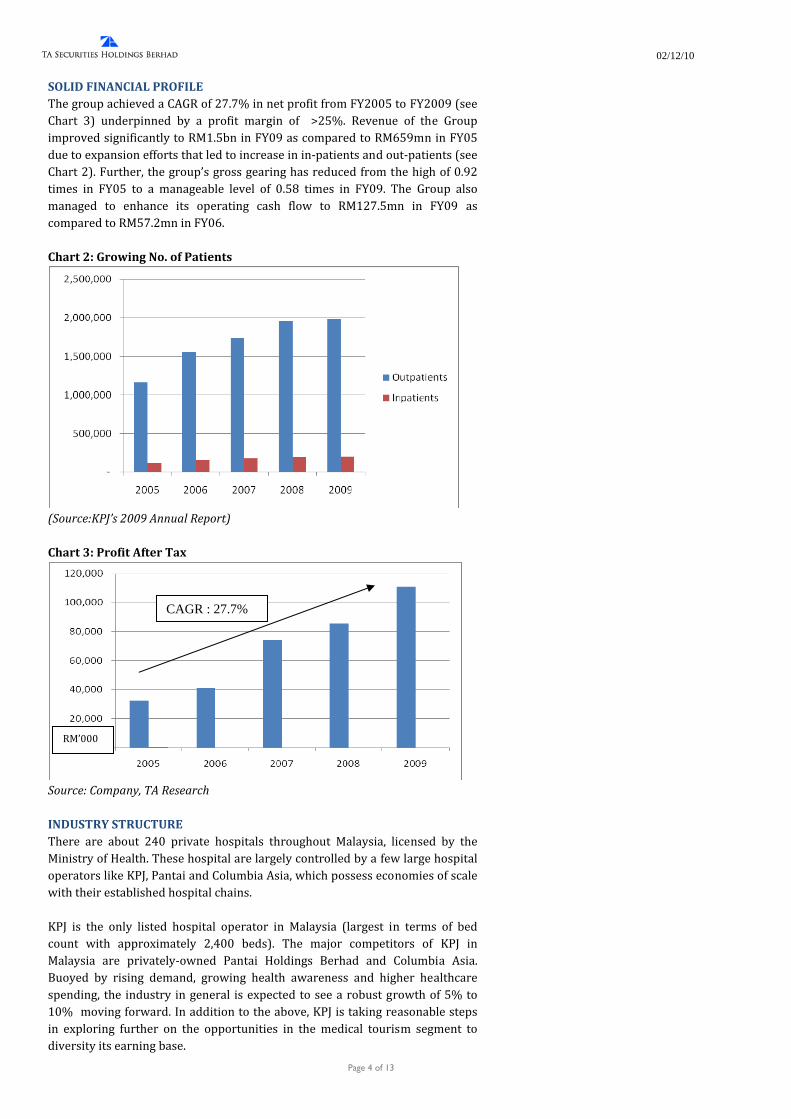

SOLID FINANCIAL PROFILE The group achieved a CAGR of 27.7% in net profit from FY2005 to FY2009 (see Chart 3) underpinned by a profit margin of >25%. Revenue of the Group improved significantly to RM1.5bn in FY09 as compared to RM659mn in FY05 due to expansion efforts that led to increase in in‐patients and out‐patients (see Chart 2). Further, the group’s gross gearing has reduced from the high of 0.92 times in FY05 to a manageable level of 0.58 times in FY09. The Group also managed to enhance its operating cash flow to RM127.5mn in FY09 as compared to RM57.2mn in FY06. Chart 2: Growing No. of Patients

(Source:KPJ’s 2009 Annual Report) Chart 3: Profit After Tax

Source: Company, TA Research INDUSTRY STRUCTURE There are about 240 private hospitals throughout Malaysia, licensed by the Ministry of Health. These hospital are largely controlled by a few large hospital operators like KPJ, Pantai and Columbia Asia, which possess economies of scale with their established hospital chains. KPJ is the only listed hospital operator in Malaysia (largest in terms of bed count with approximately 2,400 beds). The major competitors of KPJ in Malaysia are privately‐owned Pantai Holdings Berhad and Columbia Asia. Buoyed by rising demand, growing health awareness and higher healthcare spending, the industry in general is expected to see a robust growth of 5% to 10% moving forward. In addition to the above, KPJ is taking reasonable steps in exploring further on the opportunities in the medical tourism segment to diversity its earning base.

CAGR : 27.7%

RM’000

02/12/10

Page 5 of 13

Today, with the support from the Malaysian government, a large number of Malaysian private hospitals are actively participating in health tourism. We also note that Malaysia’s spending on healthcare, stands at 5% of GNP currently. The Healthcare National Key Economic Areas is targeting to welcome 1mn health travellers moving forward. The industry projections also indicates that the total revenue from healthcare travel for the key players in the Asian region, namely India, Singapore, Thailand and Malaysia, will grow to USD4.4bn in 2012 from USD2.5bn in 2006. The Government also beefs up its efforts in promoting & facilitating growth in this segment by setting up the Malaysia Health Travel Council. We gathered that KPJ is participating in campaigns organized by Malaysia Healthcare Travel Council in order to further penetrate in the healthcare tourism segment. In addition to the above, the healthcare sector is set to be transformed from a social service and consumer of wealth to a private sector‐driven engine for economic growth under the Economic Transformation Programme. Medical Tourism Medical tourism has emerged as a growing segment of the tourism industry. High cost of treatments in developed countries, have been continually attracting patients from such regions towards alternative cost‐effective destinations like Malaysia, India and other Asian countries. Malaysia has one of the most developed healthcare infrastructures in the region and is considered as the paradise for healthcare facilities and hospitals. Medical tourism has become a major segment of the tourism industry of Malaysia because of its medical excellence with high quality services and well‐trained medical specialists. Its network of private hospitals offers comprehensive services in all‐medical disciplines. Having said that, Malaysia ranked third in nuwireinvestor.com’s Top Five Medical Destinations, which rank the five most attractive opportunities for medical tourists and foreign investors alike. Malaysia’s growing reputation as a preferred health and medical destination sees it welcoming visitors from around the world seeking remedies for a range of medical needs. These include both critical health services as well as cosmetic and remedial care. Medical charges and hospitalization costs here are very competitive compared to those in many developed countries, and the expertise here ranks among the best in the world. There is a plethora of state‐of‐the‐art, well‐equipped and well‐staffed private medical centres. All of which have extensive diagnostic and therapeutic resources such as endoscopic suites, haemodialysis centres, cardiac catheterisation and magnetic resonance imaging facilities among others. Medical specialists are also highly qualified professionals with extensive international qualifications and are supported by well‐trained para‐medical staff. Premised on the above and given the increasing healthcare expenditure and healthcare awareness, we are optimistic on the prospects of the healthcare industry in general as the healthcare industry is relatively resilient to fluctuations of the economy, and demand for medical care in the country is generally stable.

02/12/10

Page 6 of 13

INVESTMENT THESIS We advocate our investment thesis for KPJ for its:

1) Solid financial profile and positive outlook in the healthcare industry;

2) Experienced team (29 years experiences in healthcare business) with a viable business model; and

3) Attractive valuation as compared to regional peers.

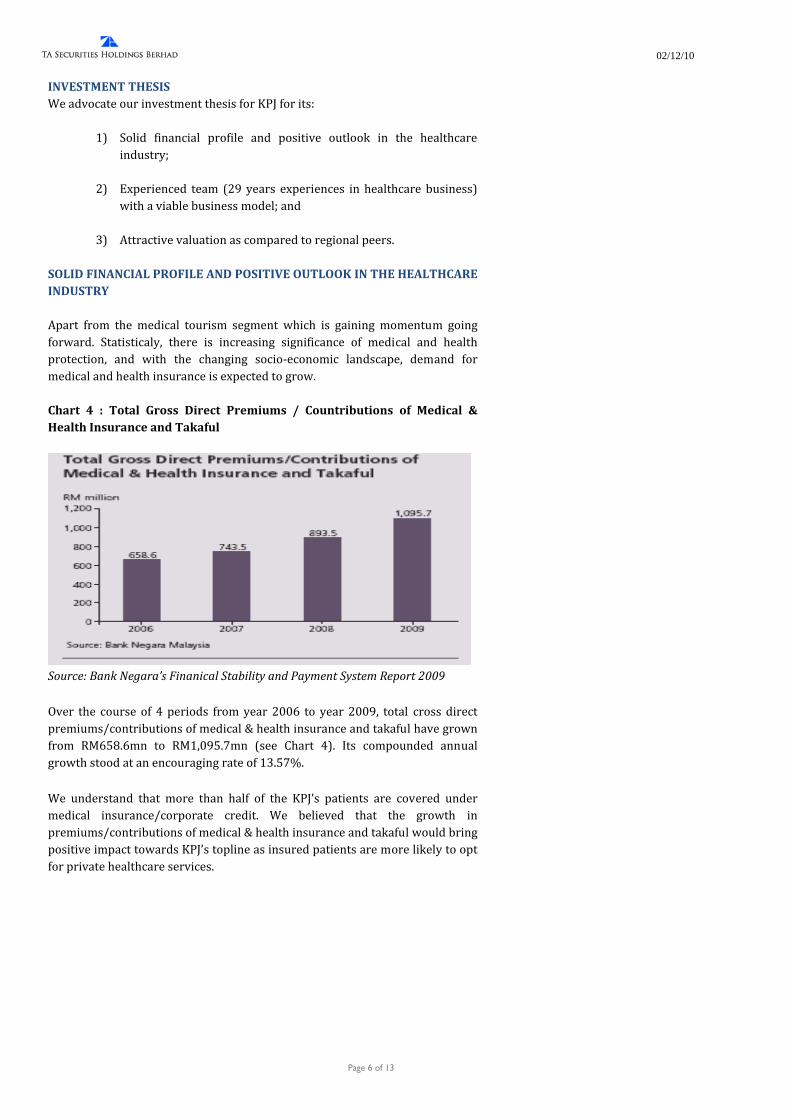

SOLID FINANCIAL PROFILE AND POSITIVE OUTLOOK IN THE HEALTHCARE INDUSTRY Apart from the medical tourism segment which is gaining momentum going forward. Statisticaly, there is increasing significance of medical and health protection, and with the changing socio‐economic landscape, demand for medical and health insurance is expected to grow. Chart 4 : Total Gross Direct Premiums / Countributions of Medical & Health Insurance and Takaful

Source: Bank Negara’s Finanical Stability and Payment System Report 2009

Over the course of 4 periods from year 2006 to year 2009, total cross direct premiums/contributions of medical & health insurance and takaful have grown from RM658.6mn to RM1,095.7mn (see Chart 4). Its compounded annual growth stood at an encouraging rate of 13.57%.

We understand that more than half of the KPJ’s patients are covered under medical insurance/corporate credit. We believed that the growth in premiums/contributions of medical & health insurance and takaful would bring positive impact towards KPJ’s topline as insured patients are more likely to opt for private healthcare services.

02/12/10

Page 7 of 13

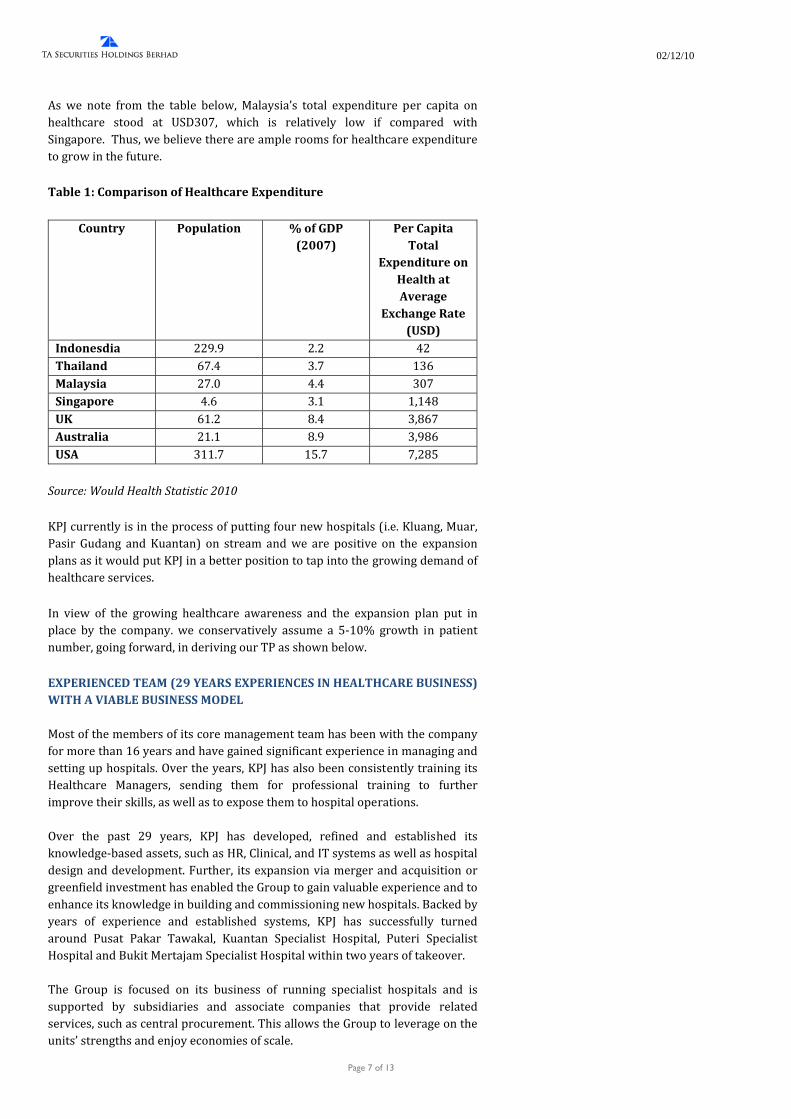

As we note from the table below, Malaysia’s total expenditure per capita on healthcare stood at USD307, which is relatively low if compared with Singapore. Thus, we believe there are ample rooms for healthcare expenditure to grow in the future.

Table 1: Comparison of Healthcare Expenditure

Country Population % of GDP (2007)

Per Capita Total

Expenditure on Health at Average

Exchange Rate (USD)

Indonesdia 229.9 2.2 42 Thailand 67.4 3.7 136 Malaysia 27.0 4.4 307 Singapore 4.6 3.1 1,148 UK 61.2 8.4 3,867 Australia 21.1 8.9 3,986 USA 311.7 15.7 7,285

Source: Would Health Statistic 2010

KPJ currently is in the process of putting four new hospitals (i.e. Kluang, Muar, Pasir Gudang and Kuantan) on stream and we are positive on the expansion plans as it would put KPJ in a better position to tap into the growing demand of healthcare services.

In view of the growing healthcare awareness and the expansion plan put in place by the company. we conservatively assume a 5‐10% growth in patient number, going forward, in deriving our TP as shown below.

EXPERIENCED TEAM (29 YEARS EXPERIENCES IN HEALTHCARE BUSINESS) WITH A VIABLE BUSINESS MODEL Most of the members of its core management team has been with the company for more than 16 years and have gained significant experience in managing and setting up hospitals. Over the years, KPJ has also been consistently training its Healthcare Managers, sending them for professional training to further improve their skills, as well as to expose them to hospital operations. Over the past 29 years, KPJ has developed, refined and established its knowledge‐based assets, such as HR, Clinical, and IT systems as well as hospital design and development. Further, its expansion via merger and acquisition or greenfield investment has enabled the Group to gain valuable experience and to enhance its knowledge in building and commissioning new hospitals. Backed by years of experience and established systems, KPJ has successfully turned around Pusat Pakar Tawakal, Kuantan Specialist Hospital, Puteri Specialist Hospital and Bukit Mertajam Specialist Hospital within two years of takeover. The Group is focused on its business of running specialist hospitals and is supported by subsidiaries and associate companies that provide related services, such as central procurement. This allows the Group to leverage on the units’ strengths and enjoy economies of scale.

02/12/10

Page 8 of 13

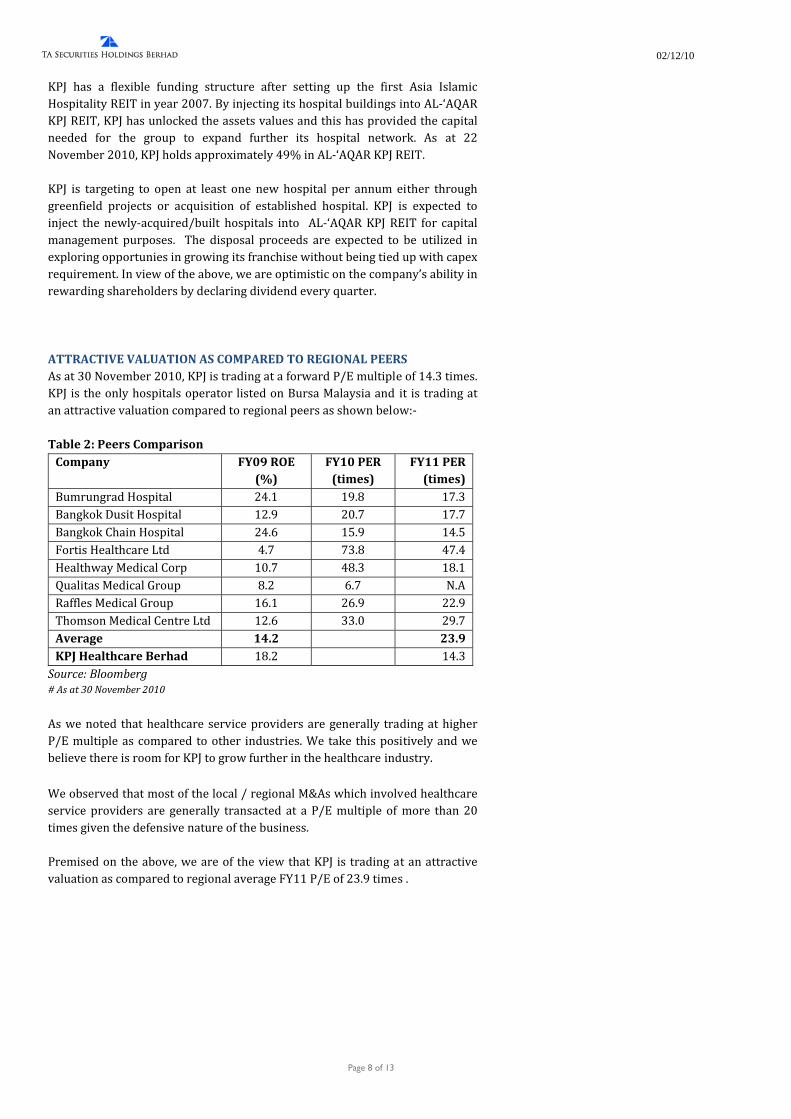

KPJ has a flexible funding structure after setting up the first Asia Islamic Hospitality REIT in year 2007. By injecting its hospital buildings into AL‐‘AQAR KPJ REIT, KPJ has unlocked the assets values and this has provided the capital needed for the group to expand further its hospital network. As at 22 November 2010, KPJ holds approximately 49% in AL‐‘AQAR KPJ REIT. KPJ is targeting to open at least one new hospital per annum either through greenfield projects or acquisition of established hospital. KPJ is expected to inject the newly‐acquired/built hospitals into AL‐‘AQAR KPJ REIT for capital management purposes. The disposal proceeds are expected to be utilized in exploring opportunies in growing its franchise without being tied up with capex requirement. In view of the above, we are optimistic on the company’s ability in rewarding shareholders by declaring dividend every quarter. ATTRACTIVE VALUATION AS COMPARED TO REGIONAL PEERS As at 30 November 2010, KPJ is trading at a forward P/E multiple of 14.3 times. KPJ is the only hospitals operator listed on Bursa Malaysia and it is trading at an attractive valuation compared to regional peers as shown below:‐ Table 2: Peers Comparison Company FY09 ROE

(%) FY10 PER (times)

FY11 PER (times)

Bumrungrad Hospital 24.1 19.8 17.3 Bangkok Dusit Hospital 12.9 20.7 17.7 Bangkok Chain Hospital 24.6 15.9 14.5 Fortis Healthcare Ltd 4.7 73.8 47.4 Healthway Medical Corp 10.7 48.3 18.1 Qualitas Medical Group 8.2 6.7 N.A Raffles Medical Group 16.1 26.9 22.9 Thomson Medical Centre Ltd 12.6 33.0 29.7 Average 14.2 23.9 KPJ Healthcare Berhad 18.2 14.3 Source: Bloomberg # As at 30 November 2010

As we noted that healthcare service providers are generally trading at higher P/E multiple as compared to other industries. We take this positively and we believe there is room for KPJ to grow further in the healthcare industry.

We observed that most of the local / regional M&As which involved healthcare service providers are generally transacted at a P/E multiple of more than 20 times given the defensive nature of the business. Premised on the above, we are of the view that KPJ is trading at an attractive valuation as compared to regional average FY11 P/E of 23.9 times .

02/12/10

Page 9 of 13

Earnings Summary FYE Dec 31 FY08 FY09 FY10E FY11F FY12FRevenue (mn) 1,267.3 1,456.3 1,616.6 1,799.3 2,098.0EBITA (mn) 368.4 419 466.9 519.6 605.9EBITA margin (% 29.04 28.78 28.88 28.88 28.88Pretax profit (mn) 114.1 143.9 166.4 194.4 252.5Net profit (mn) 85.6 110.9 124.3 145.9 189.5EPS (sen) 16.2 21 24 28 36EPS growth (%) ‐ 29.6 14.3 16.7 28.6PER (x) 22.8 17.6 15.8 13.5 10.2GDPS (sen) 9 9 11 12 16Div Yield (%) 2.4 2.4 2.8 3.3 4.3ROE (%) 15.3 18.2 18.8 19.7 22.8

VALUATION We are using the discounted free cash flow valuation methodology to value KPJ as it is a “cash‐generating” business. We are assuming capex requirement of RM150‐180mn per annum for construction / upgrading of hospitals and replenishment of medical equipments. With a terminal growth rate of 3.5% after FY13, we are discounting KPJ’s future cash flow at a cost of equity of 8.26% and arrive at a fair value of RM4.32/share. At RM4.32, the TP represents an implied forward PE of 15.4 times FY2011 EPS. Given the defensive industry KPJ is operating in, we believe that it is justifiable as it is still in the lower band compared to regional peers which are trading at an average forward P/E of more than 20 times. Given the capital upside of 15.07% to our DCF‐derived target price of RM4.32, we are initiating coverage on KPJ with a Buy recommendation. Key upside/downside risks to TP include: 1) Serious disease outbreaks; 2) Lower than expected patient number; and 3) Longer gestation period than expected for newly acquired / built hospitals.

02/12/10

Page 10 of 13

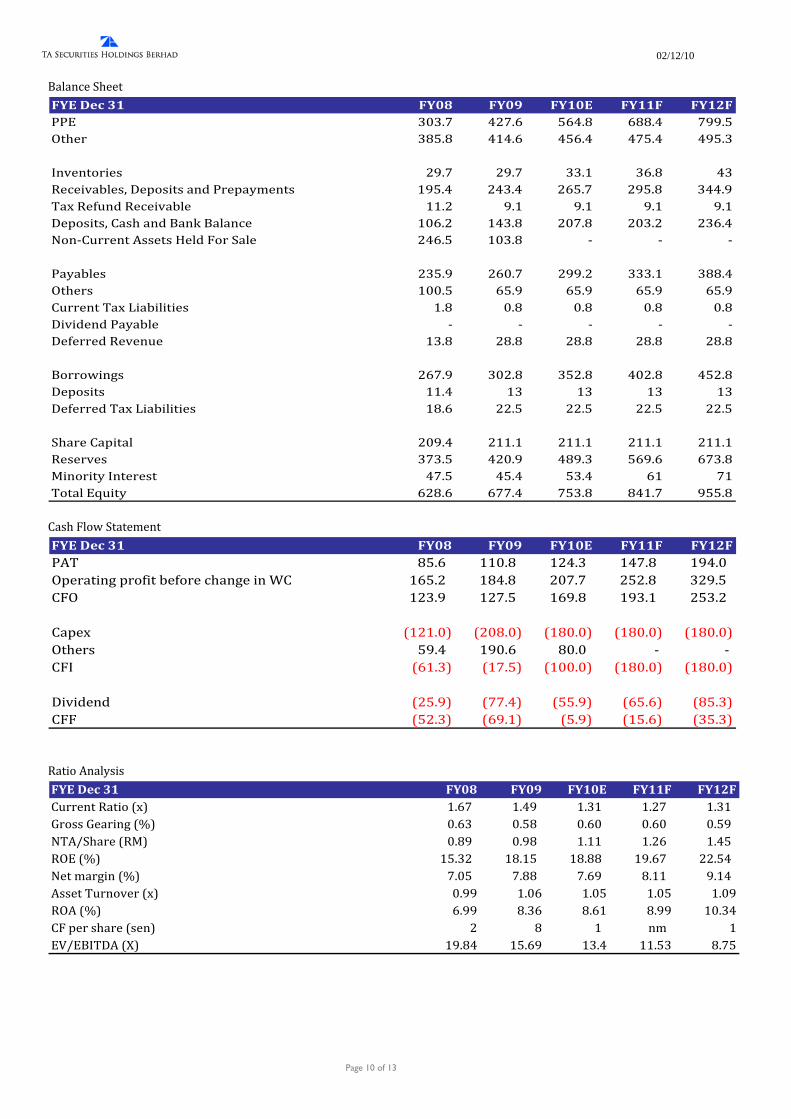

Balance Sheet FYE Dec 31 FY08 FY09 FY10E FY11F FY12FPPE 303.7 427.6 564.8 688.4 799.5Other 385.8 414.6 456.4 475.4 495.3

Inventories 29.7 29.7 33.1 36.8 43Receivables, Deposits and Prepayments 195.4 243.4 265.7 295.8 344.9Tax Refund Receivable 11.2 9.1 9.1 9.1 9.1Deposits, Cash and Bank Balance 106.2 143.8 207.8 203.2 236.4Non‐Current Assets Held For Sale 246.5 103.8 ‐ ‐ ‐

Payables 235.9 260.7 299.2 333.1 388.4Others 100.5 65.9 65.9 65.9 65.9Current Tax Liabilities 1.8 0.8 0.8 0.8 0.8Dividend Payable ‐ ‐ ‐ ‐ ‐Deferred Revenue 13.8 28.8 28.8 28.8 28.8

Borrowings 267.9 302.8 352.8 402.8 452.8Deposits 11.4 13 13 13 13Deferred Tax Liabilities 18.6 22.5 22.5 22.5 22.5

Share Capital 209.4 211.1 211.1 211.1 211.1Reserves 373.5 420.9 489.3 569.6 673.8Minority Interest 47.5 45.4 53.4 61 71Total Equity 628.6 677.4 753.8 841.7 955.8 Cash Flow Statement FYE Dec 31 FY08 FY09 FY10E FY11F FY12FPAT 85.6 110.8 124.3 147.8 194.0Operating profit before change in WC 165.2 184.8 207.7 252.8 329.5CFO 123.9 127.5 169.8 193.1 253.2

Capex (121.0) (208.0) (180.0) (180.0) (180.0)Others 59.4 190.6 80.0 ‐ ‐ CFI (61.3) (17.5) (100.0) (180.0) (180.0)

Dividend (25.9) (77.4) (55.9) (65.6) (85.3)CFF (52.3) (69.1) (5.9) (15.6) (35.3) Ratio Analysis FYE Dec 31 FY08 FY09 FY10E FY11F FY12FCurrent Ratio (x) 1.67 1.49 1.31 1.27 1.31 Gross Gearing (%) 0.63 0.58 0.60 0.60 0.59 NTA/Share (RM) 0.89 0.98 1.11 1.26 1.45 ROE (%) 15.32 18.15 18.88 19.67 22.54 Net margin (%) 7.05 7.88 7.69 8.11 9.14 Asset Turnover (x) 0.99 1.06 1.05 1.05 1.09ROA (%) 6.99 8.36 8.61 8.99 10.34CF per share (sen) 2 8 1 nm 1EV/EBITDA (X) 19.84 15.69 13.4 11.53 8.75

02/12/10

Page 11 of 13

Appendix A – KPJ Hospitals (Lists Are Not Exhaustive)

Source: Company

02/12/10

Page 12 of 13

Source: Company

02/12/10

Page 13 of 13

RS Bumi Serpong Damai, Jakarta

RS Medika Permata Hijau, Jakarta

Source: Company Disclaimer

The information in this report has been obtained from sources believed to be reliable. Its accuracy or completeness is not guaranteed and opinions are subject to change without notice. This report is for information only and not to be construed as a solicitation for contracts. We accept no liability for any direct or indirect loss arising from the use of this document. We, our

associates, directors, employees may have an interest in the securities and/or companies mentioned herein. for TA SECURITIES HOLDINGS BERHAD(14948‐M)

(A Participating Organisation of Bursa Malaysia Securities Berhad) Kaladher Govindan – Head of Research