global economic limbo by ms hew sue ling

TRANSCRIPT

Global Economic Limbo:

The Emerging Markets

Slowdown and The Malaysian

Bond Market

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD - All rights reserved.

Presented by Hew Sue Ling

Head of Pricing, BPAM

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 2

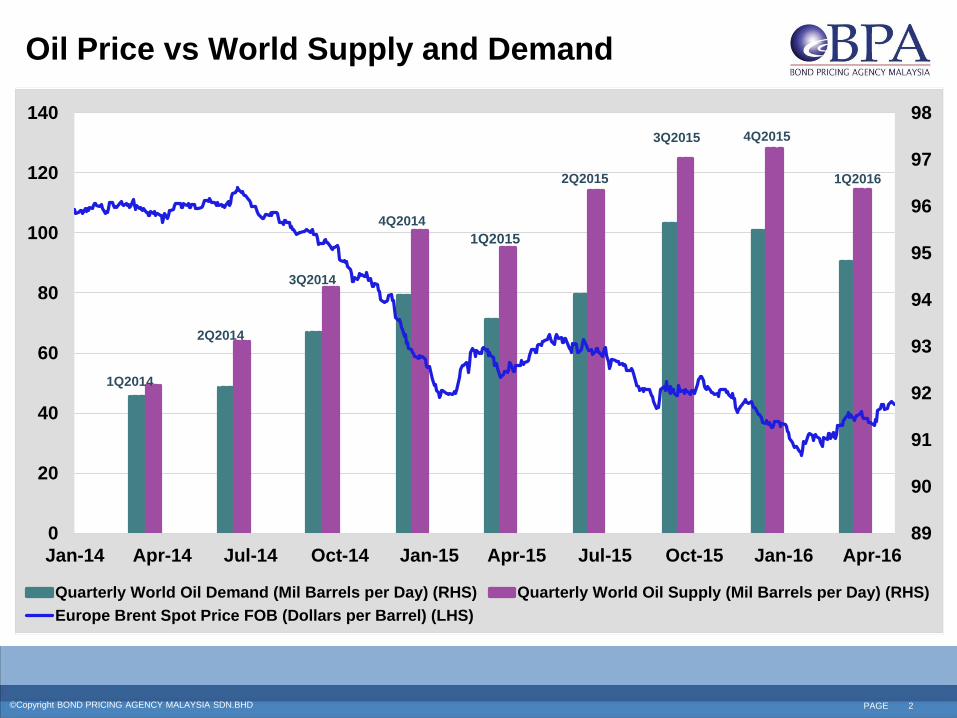

Oil Price vs World Supply and Demand

89

90

91

92

93

94

95

96

97

98

0

20

40

60

80

100

120

140

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16

Quarterly World Oil Demand (Mil Barrels per Day) (RHS) Quarterly World Oil Supply (Mil Barrels per Day) (RHS)

Europe Brent Spot Price FOB (Dollars per Barrel) (LHS)

1Q2014

2Q2014

3Q2014

4Q2014

1Q2015

2Q2015

3Q2015 4Q2015

1Q2016

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 3

The goal is to achieve sustainable economic growth

Inevitable slowdown and expected to drag on

Ripple effect across the world

China initiated economic rebalancing to increase the

consumption portion of economic growth

Faced with challenges: high saving rates and low

wages economic slowdown

China’s growth had been driven by investment, mostly

funded by shadow banking and debt

Resulted in excess capacity and economic bubble

China Sneezes…

Lower Investment

Increase Consumption

Sustainable Growth

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 4

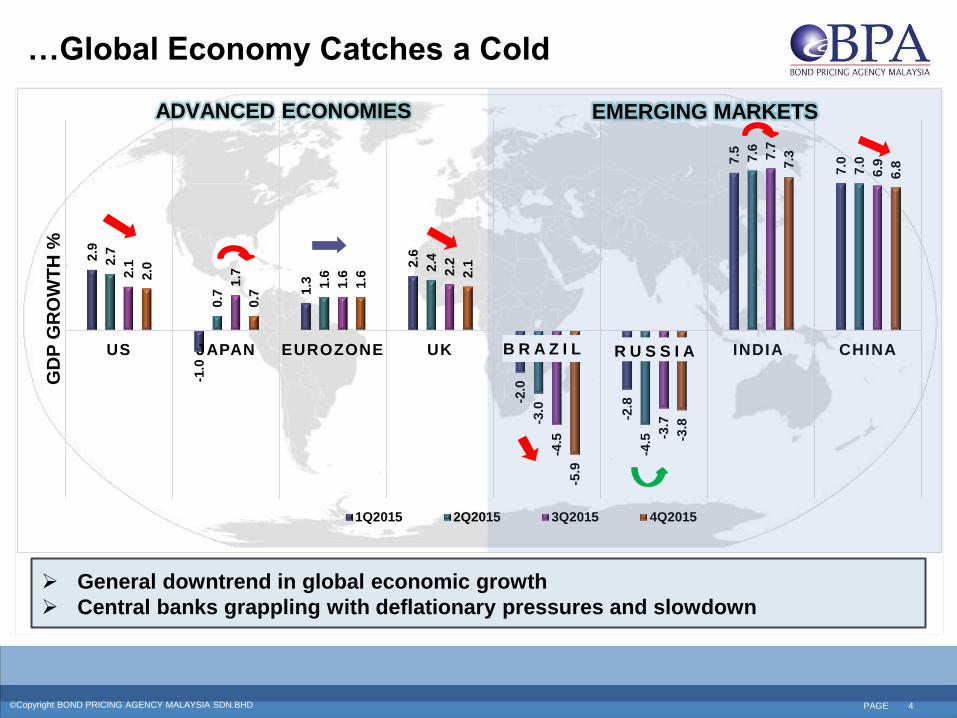

…Global Economy Catches a Cold

General downtrend in global economic growth

Central banks grappling with deflationary pressures and slowdown

2.9

-1.0

1.3

2.6

-2.0

-2.8

7.5

7.0

2.7

0.7

1.6

2.4

-3.0

-4.5

7.6

7.0

2.1

1.7

1.6

2.2

-4.5

-3.7

7.7

6.9

2.0

0.7

1.6

2.1

-5.9

-3.8

7.3

6.8

US JAPAN EUROZONE UK BRAZIL RUSSIA INDIA CHINA

GD

P G

RO

WT

H %

1Q2015 2Q2015 3Q2015 4Q2015

ADVANCED ECONOMIES EMERGING MARKETS

B R A Z I L R U S S I A

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 5

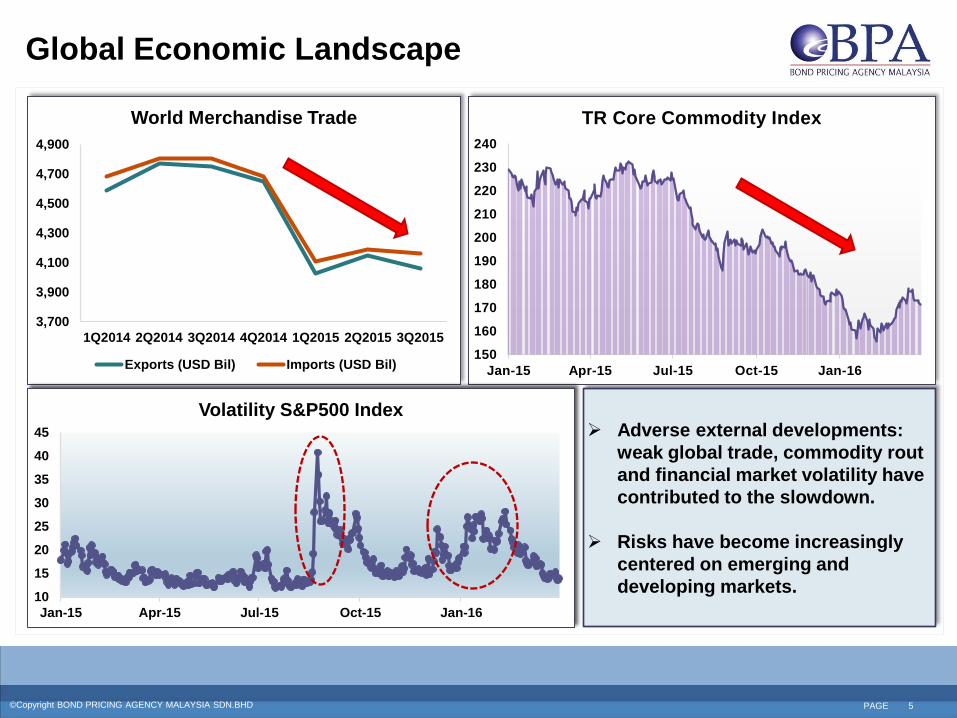

Global Economic Landscape

3,700

3,900

4,100

4,300

4,500

4,700

4,900

1Q2014 2Q2014 3Q2014 4Q2014 1Q2015 2Q2015 3Q2015

World Merchandise Trade

Exports (USD Bil) Imports (USD Bil)

Adverse external developments:

weak global trade, commodity rout

and financial market volatility have

contributed to the slowdown.

Risks have become increasingly

centered on emerging and

developing markets.

150

160

170

180

190

200

210

220

230

240

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16

TR Core Commodity Index

10

15

20

25

30

35

40

45

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16

Volatility S&P500 Index

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 6

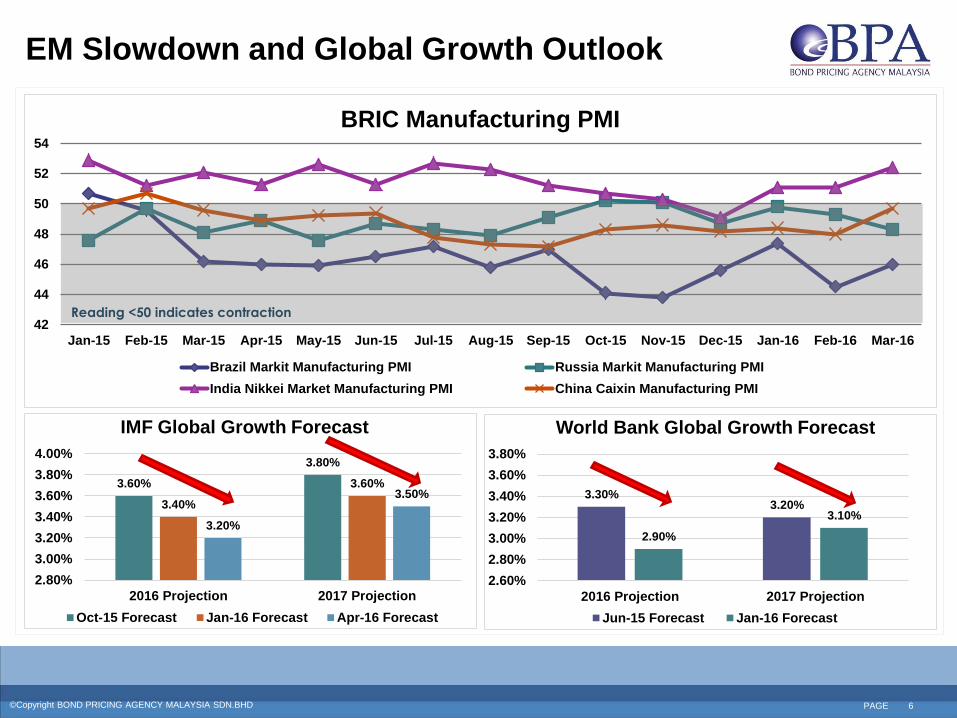

EM Slowdown and Global Growth Outlook

42

44

46

48

50

52

54

Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16

BRIC Manufacturing PMI

Brazil Markit Manufacturing PMI Russia Markit Manufacturing PMI

India Nikkei Market Manufacturing PMI China Caixin Manufacturing PMI

Reading <50 indicates contraction

3.30% 3.20%

2.90%

3.10%

2.60%

2.80%

3.00%

3.20%

3.40%

3.60%

3.80%

2016 Projection 2017 Projection

World Bank Global Growth Forecast

Jun-15 Forecast Jan-16 Forecast

3.60%

3.80%

3.40%

3.60%

3.20%

3.50%

2.80%

3.00%

3.20%

3.40%

3.60%

3.80%

4.00%

2016 Projection 2017 Projection

IMF Global Growth Forecast

Oct-15 Forecast Jan-16 Forecast Apr-16 Forecast

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 7

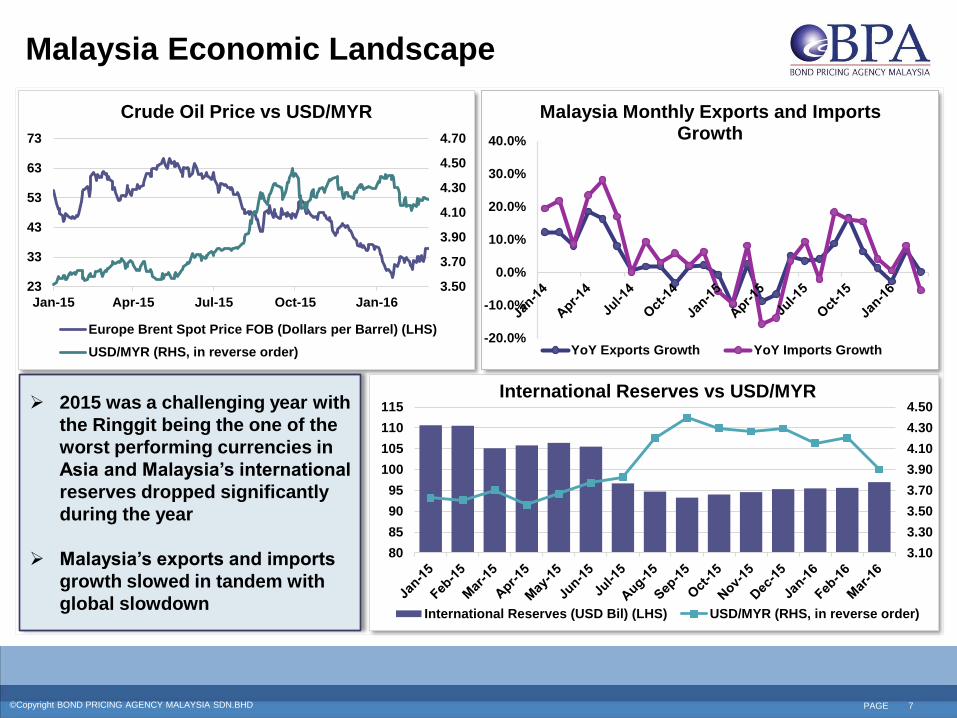

Malaysia Economic Landscape

2015 was a challenging year with

the Ringgit being the one of the

worst performing currencies in

Asia and Malaysia’s international

reserves dropped significantly

during the year

Malaysia’s exports and imports

growth slowed in tandem with

global slowdown

3.50

3.70

3.90

4.10

4.30

4.50

4.70

23

33

43

53

63

73

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16

Crude Oil Price vs USD/MYR

Europe Brent Spot Price FOB (Dollars per Barrel) (LHS)

USD/MYR (RHS, in reverse order)

3.10

3.30

3.50

3.70

3.90

4.10

4.30

4.50

80

85

90

95

100

105

110

115International Reserves vs USD/MYR

International Reserves (USD Bil) (LHS) USD/MYR (RHS, in reverse order)

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

Malaysia Monthly Exports and Imports Growth

YoY Exports Growth YoY Imports Growth

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 8

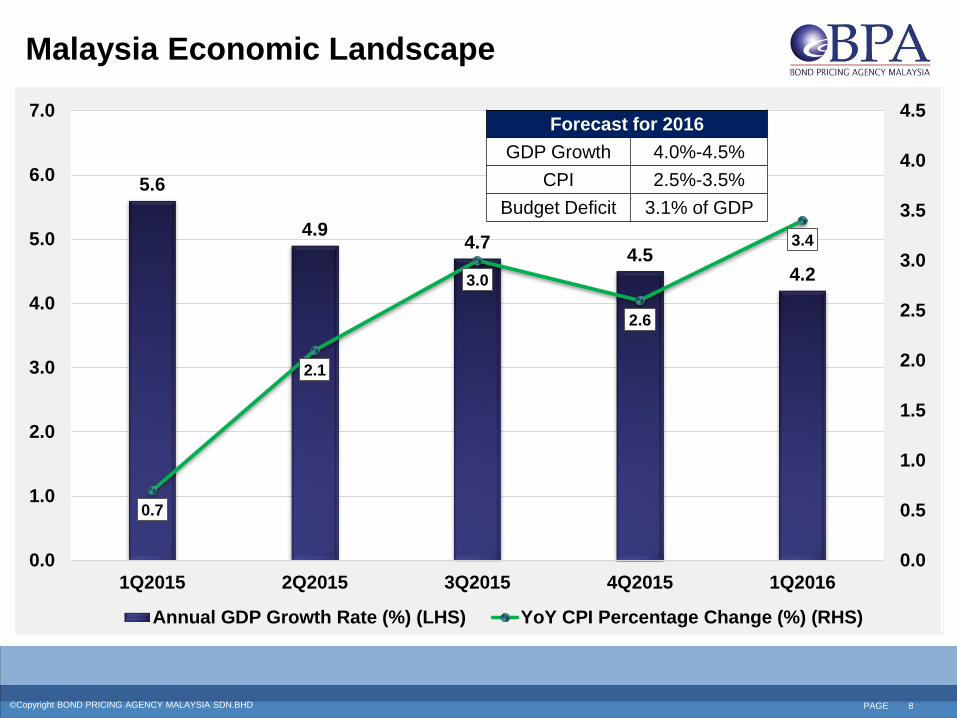

Malaysia Economic Landscape

5.6

4.9 4.7

4.5 4.2

0.7

2.1

3.0

2.6

3.4

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1Q2015 2Q2015 3Q2015 4Q2015 1Q2016

Annual GDP Growth Rate (%) (LHS) YoY CPI Percentage Change (%) (RHS)

Forecast for 2016

GDP Growth 4.0%-4.5%

CPI 2.5%-3.5%

Budget Deficit 3.1% of GDP

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 9

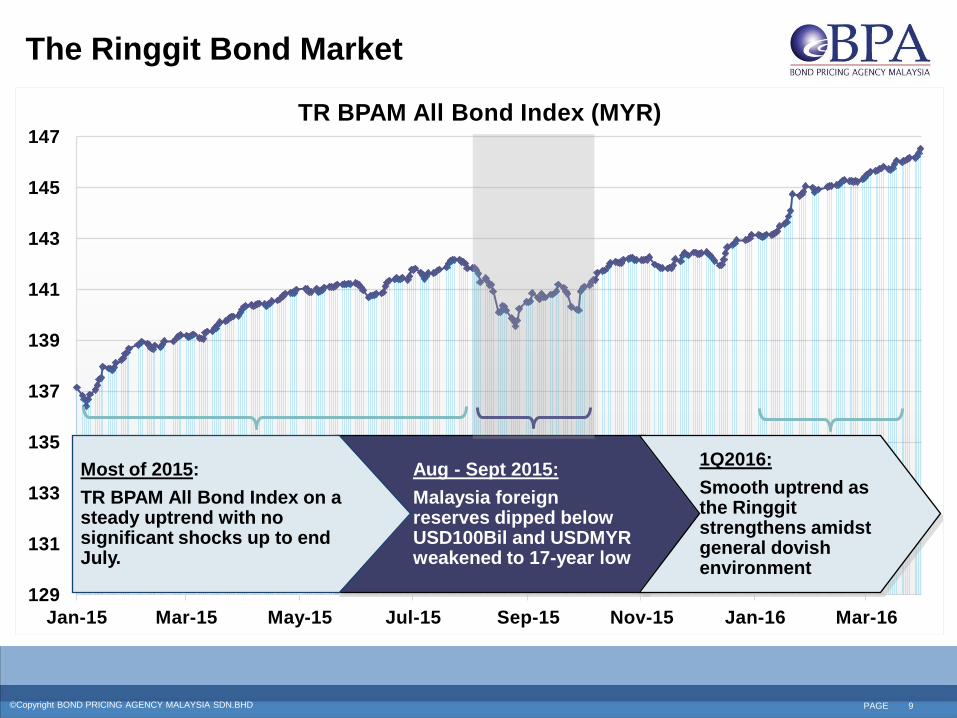

129

131

133

135

137

139

141

143

145

147

Jan-15 Mar-15 May-15 Jul-15 Sep-15 Nov-15 Jan-16 Mar-16

TR BPAM All Bond Index (MYR)

Aug - Sept 2015:

Malaysia foreign reserves dipped below USD100Bil and USDMYR weakened to 17-year low

1Q2016:

Smooth uptrend as the Ringgit strengthens amidst general dovish environment

Most of 2015:

TR BPAM All Bond Index on a steady uptrend with no significant shocks up to end July.

The Ringgit Bond Market

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 10

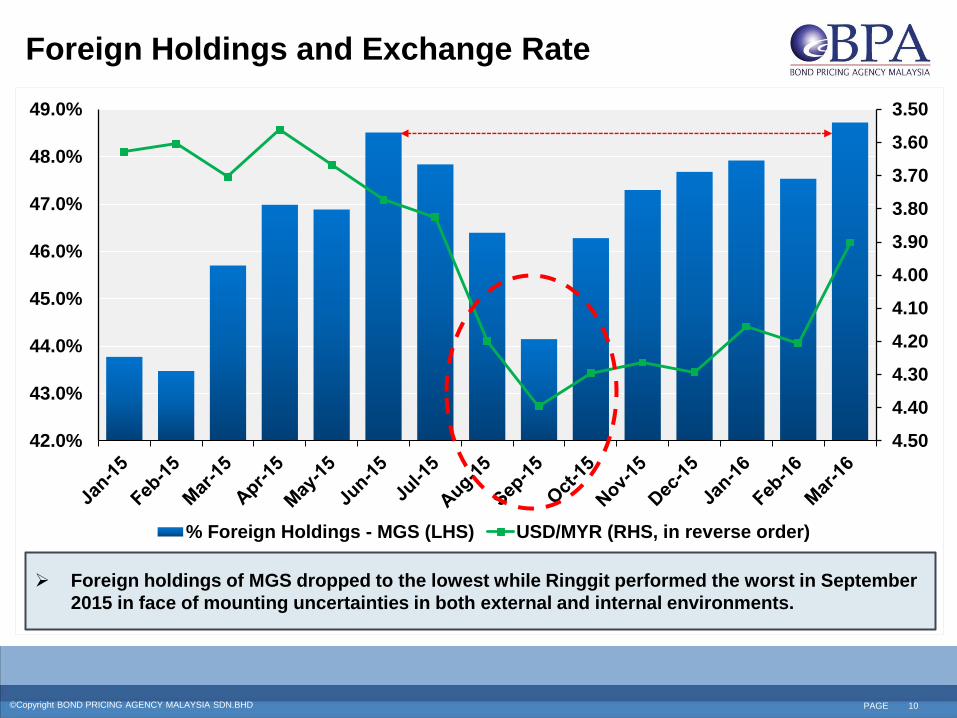

Foreign Holdings and Exchange Rate

Foreign holdings of MGS dropped to the lowest while Ringgit performed the worst in September

2015 in face of mounting uncertainties in both external and internal environments.

3.50

3.60

3.70

3.80

3.90

4.00

4.10

4.20

4.30

4.40

4.5042.0%

43.0%

44.0%

45.0%

46.0%

47.0%

48.0%

49.0%

% Foreign Holdings - MGS (LHS) USD/MYR (RHS, in reverse order)

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 11

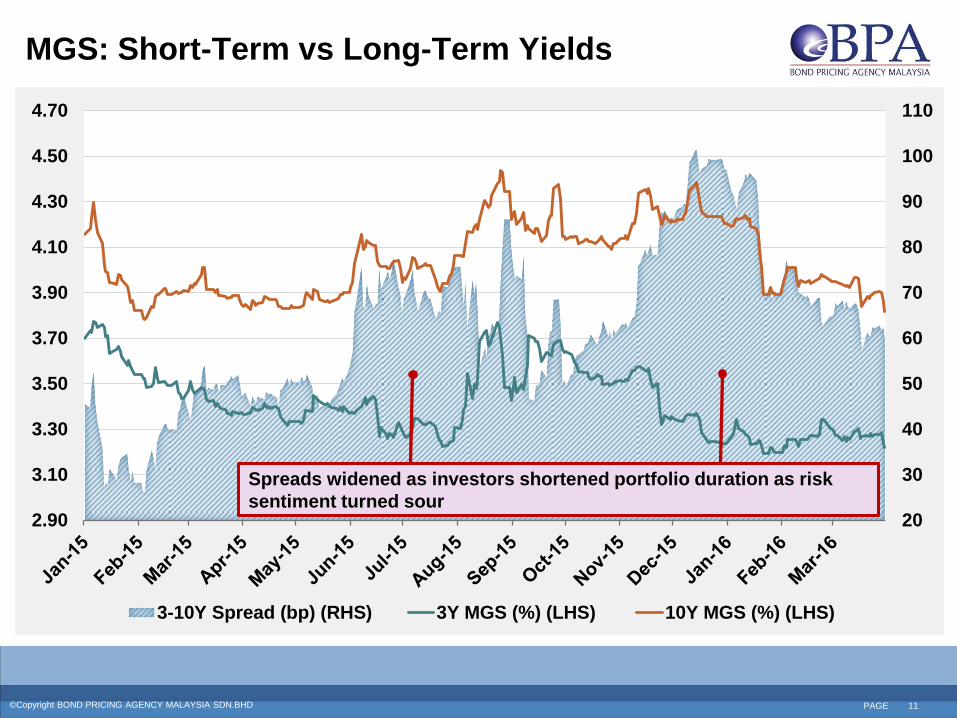

MGS: Short-Term vs Long-Term Yields

20

30

40

50

60

70

80

90

100

110

2.90

3.10

3.30

3.50

3.70

3.90

4.10

4.30

4.50

4.70

3-10Y Spread (bp) (RHS) 3Y MGS (%) (LHS) 10Y MGS (%) (LHS)

Spreads widened as investors shortened portfolio duration as risk

sentiment turned sour

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 12

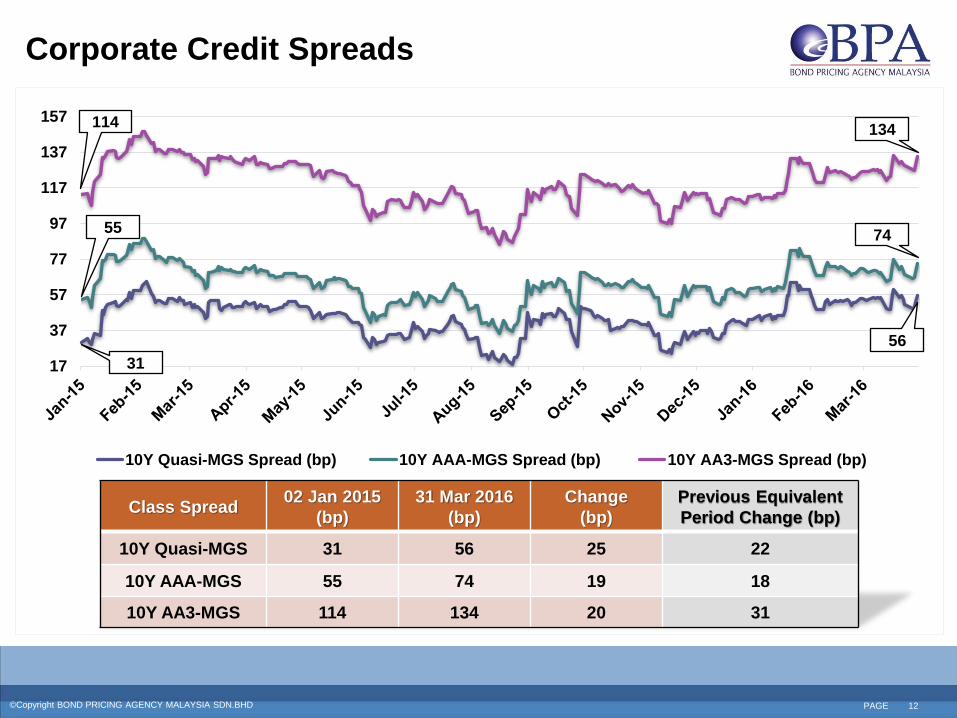

Corporate Credit Spreads

17

37

57

77

97

117

137

157

10Y Quasi-MGS Spread (bp) 10Y AAA-MGS Spread (bp) 10Y AA3-MGS Spread (bp)

114

55

31

134

74

56

Class Spread 02 Jan 2015

(bp)

31 Mar 2016

(bp)

Change

(bp)

Previous Equivalent

Period Change (bp)

10Y Quasi-MGS 31 56 25 22

10Y AAA-MGS 55 74 19 18

10Y AA3-MGS 114 134 20 31

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 13

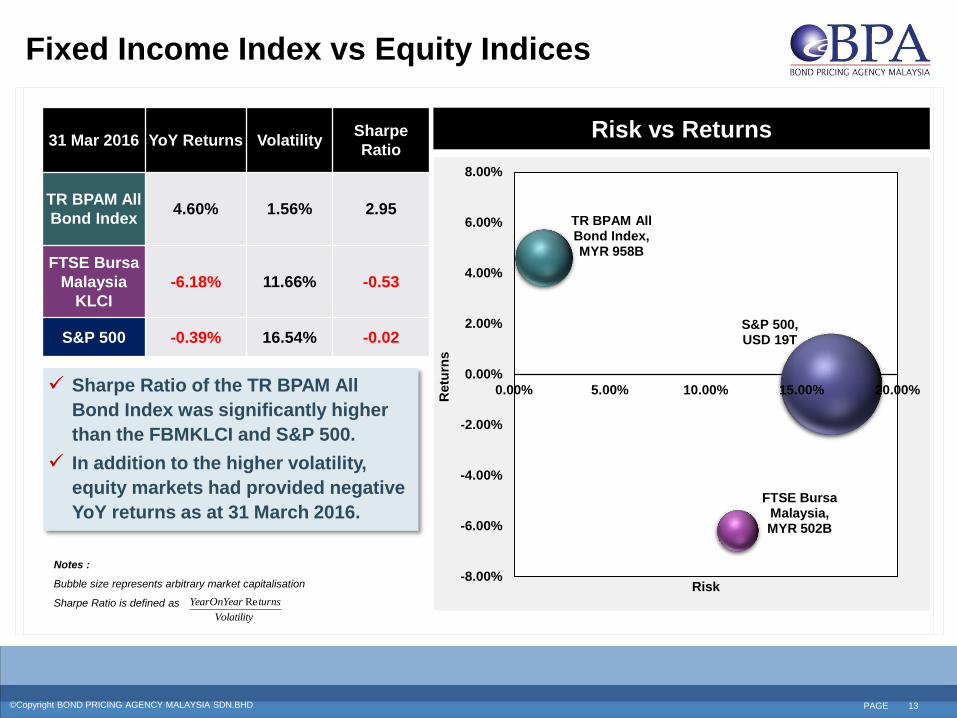

Fixed Income Index vs Equity Indices

Risk vs Returns 31 Mar 2016 YoY Returns Volatility

Sharpe

Ratio

TR BPAM All

Bond Index 4.60% 1.56% 2.95

FTSE Bursa

Malaysia

KLCI

-6.18% 11.66% -0.53

S&P 500 -0.39% 16.54% -0.02

Sharpe Ratio of the TR BPAM All

Bond Index was significantly higher

than the FBMKLCI and S&P 500.

In addition to the higher volatility,

equity markets had provided negative

YoY returns as at 31 March 2016.

Notes :

Bubble size represents arbitrary market capitalisation

Sharpe Ratio is defined as

FTSE Bursa Malaysia, MYR 502B

S&P 500, USD 19T

TR BPAM All Bond Index, MYR 958B

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

0.00% 5.00% 10.00% 15.00% 20.00%

Retu

rns

Risk

Volatility

turnsYearOnYear Re

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 14

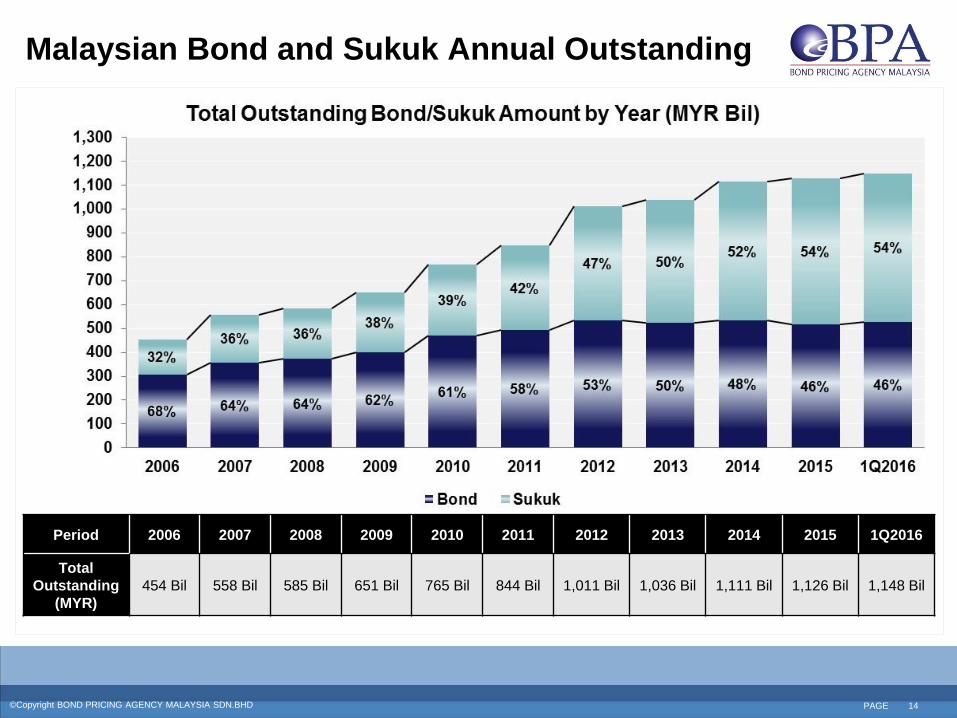

Malaysian Bond and Sukuk Annual Outstanding

Period 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 1Q2016

Total

Outstanding

(MYR)

454 Bil 558 Bil 585 Bil 651 Bil 765 Bil 844 Bil 1,011 Bil 1,036 Bil 1,111 Bil 1,126 Bil 1,148 Bil

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 15

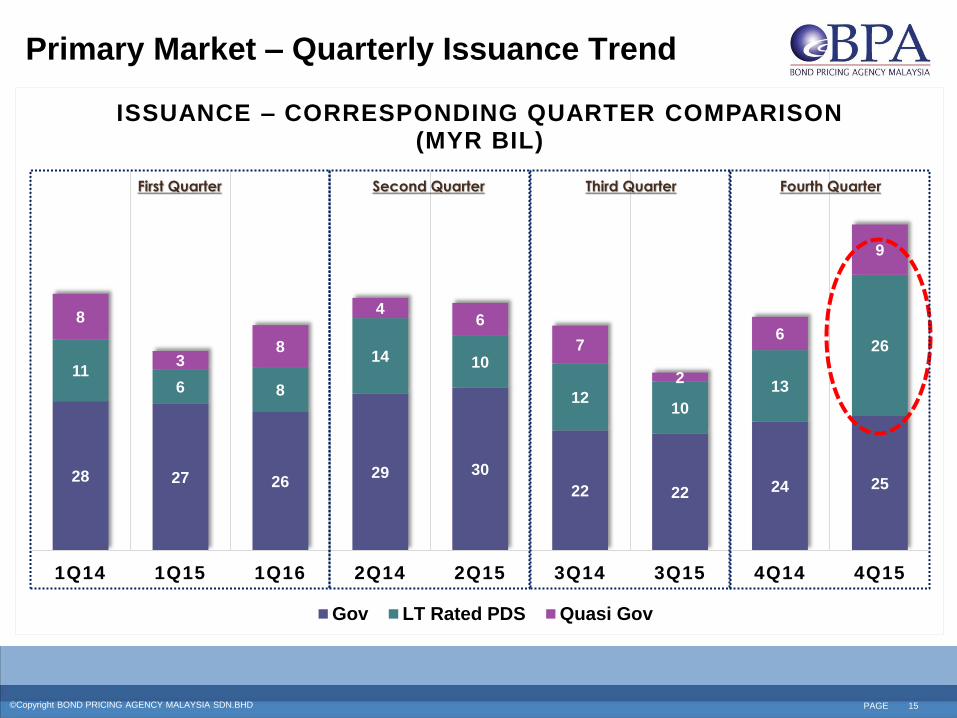

Primary Market – Quarterly Issuance Trend

28 27 26 29 30

22 22 24 25

11 6 8

14 10

12 10

13

26

8

3 8

4 6

7

2

6

9

1Q14 1Q15 1Q16 2Q14 2Q15 3Q14 3Q15 4Q14 4Q15

ISSUANCE – CORRESPONDING QUARTER COMPARISON (MYR BIL)

Gov LT Rated PDS Quasi Gov

First Quarter Second Quarter Third Quarter Fourth Quarter

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 16

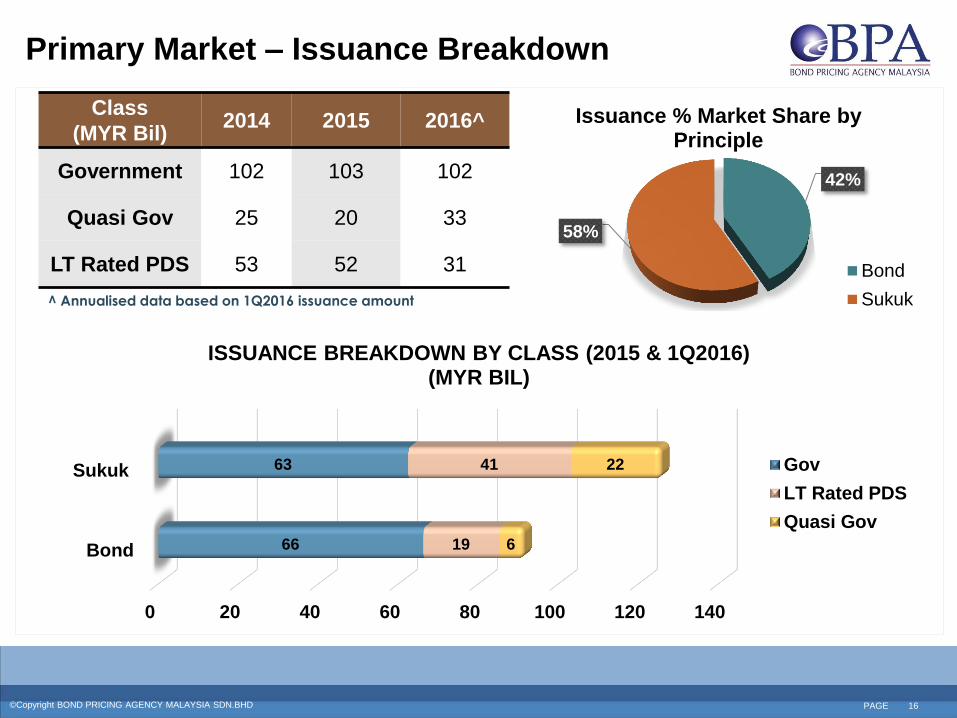

Primary Market – Issuance Breakdown

^ Annualised data based on 1Q2016 issuance amount

42%

58%

Issuance % Market Share by Principle

Bond

Sukuk

Class

(MYR Bil) 2014 2015 2016^

Government 102 103 102

Quasi Gov 25 20 33

LT Rated PDS 53 52 31

0 20 40 60 80 100 120 140

Bond

Sukuk

66

63

19

41

6

22

ISSUANCE BREAKDOWN BY CLASS (2015 & 1Q2016) (MYR BIL)

Gov

LT Rated PDS

Quasi Gov

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 17

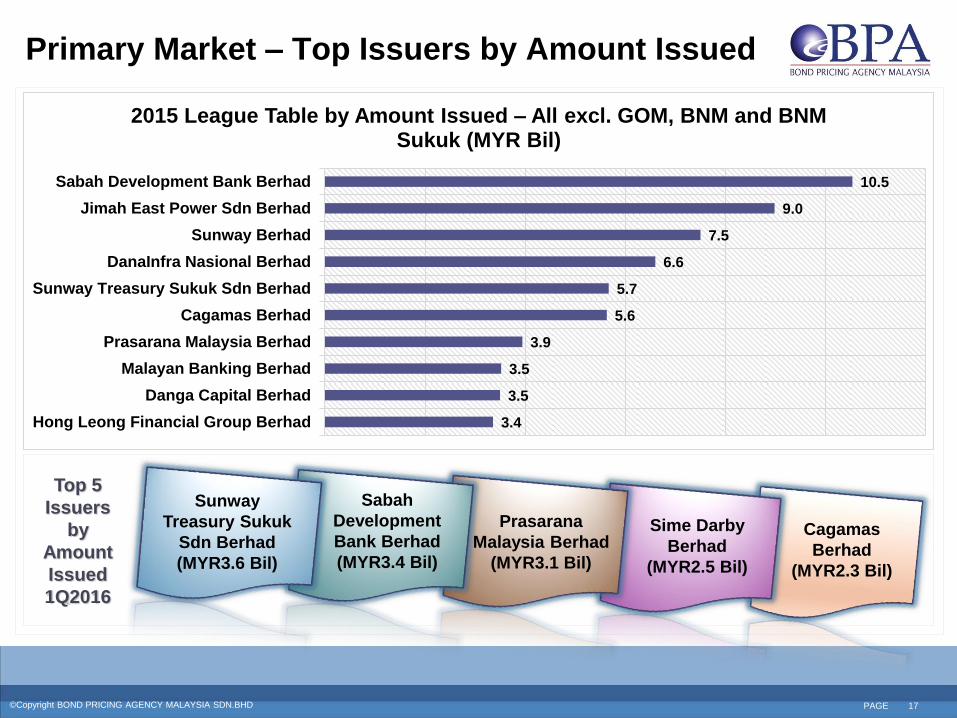

Primary Market – Top Issuers by Amount Issued

Top 5

Issuers

by

Amount

Issued

1Q2016

Sunway

Treasury Sukuk

Sdn Berhad

(MYR3.6 Bil)

Sabah

Development

Bank Berhad

(MYR3.4 Bil)

Prasarana

Malaysia Berhad

(MYR3.1 Bil)

Sime Darby

Berhad

(MYR2.5 Bil)

Cagamas

Berhad

(MYR2.3 Bil)

3.4

3.5

3.5

3.9

5.6

5.7

6.6

7.5

9.0

10.5

Hong Leong Financial Group Berhad

Danga Capital Berhad

Malayan Banking Berhad

Prasarana Malaysia Berhad

Cagamas Berhad

Sunway Treasury Sukuk Sdn Berhad

DanaInfra Nasional Berhad

Sunway Berhad

Jimah East Power Sdn Berhad

Sabah Development Bank Berhad

2015 League Table by Amount Issued – All excl. GOM, BNM and BNM Sukuk (MYR Bil)

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 18

Secondary Market – Quarterly Trading Trend

Since 2013, trading activities dwindled as investors

shied away from local bond market amid global

liquidity tightening initiated by the US Fed.

In 2015, total trade dipped below MYR1 billion.

In 1Q2016, trade volume picked up as the Ringgit

strengthened and general dovish tone among major

central banks gave domestic bond market a boost.

269 280

316 326 305

229 252

188

291

1Q2014 2Q2014 3Q2014 4Q2014 1Q2015 2Q2015 3Q2015 4Q2015 1Q2016

Quarterly Trade Volume (MYR Bil)

-17%

-18%

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 19

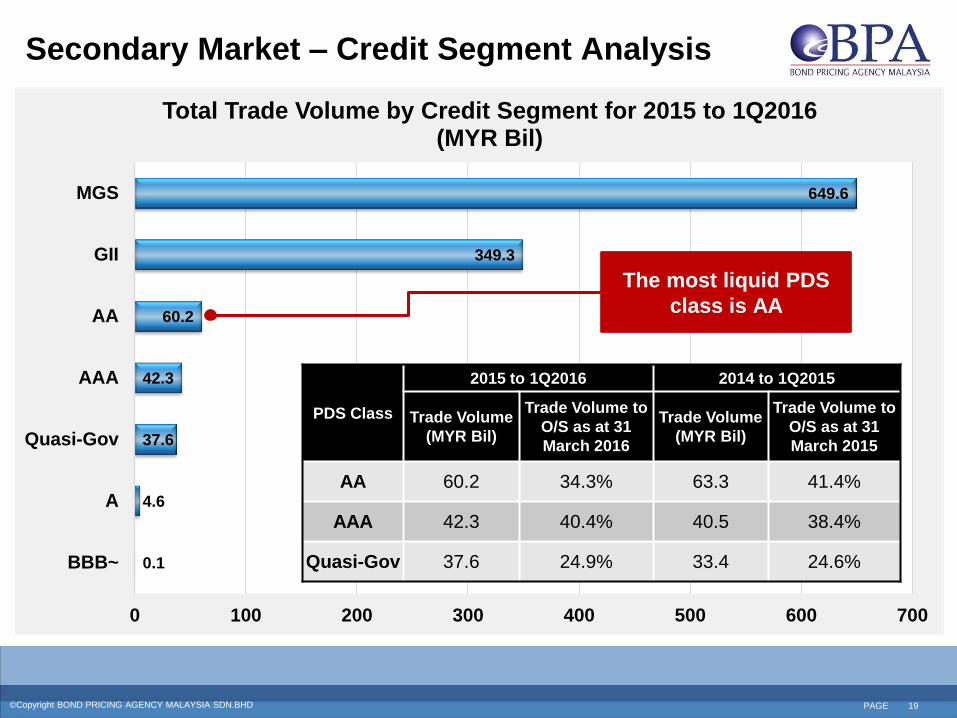

Secondary Market – Credit Segment Analysis

0.1

4.6

37.6

42.3

60.2

349.3

649.6

0 100 200 300 400 500 600 700

BBB~

A

Quasi-Gov

AAA

AA

GII

MGS

Total Trade Volume by Credit Segment for 2015 to 1Q2016 (MYR Bil)

The most liquid PDS

class is AA

PDS Class

2015 to 1Q2016 2014 to 1Q2015

Trade Volume

(MYR Bil)

Trade Volume to

O/S as at 31

March 2016

Trade Volume

(MYR Bil)

Trade Volume to

O/S as at 31

March 2015

AA 60.2 34.3% 63.3 41.4%

AAA 42.3 40.4% 40.5 38.4%

Quasi-Gov 37.6 24.9% 33.4 24.6%

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 20

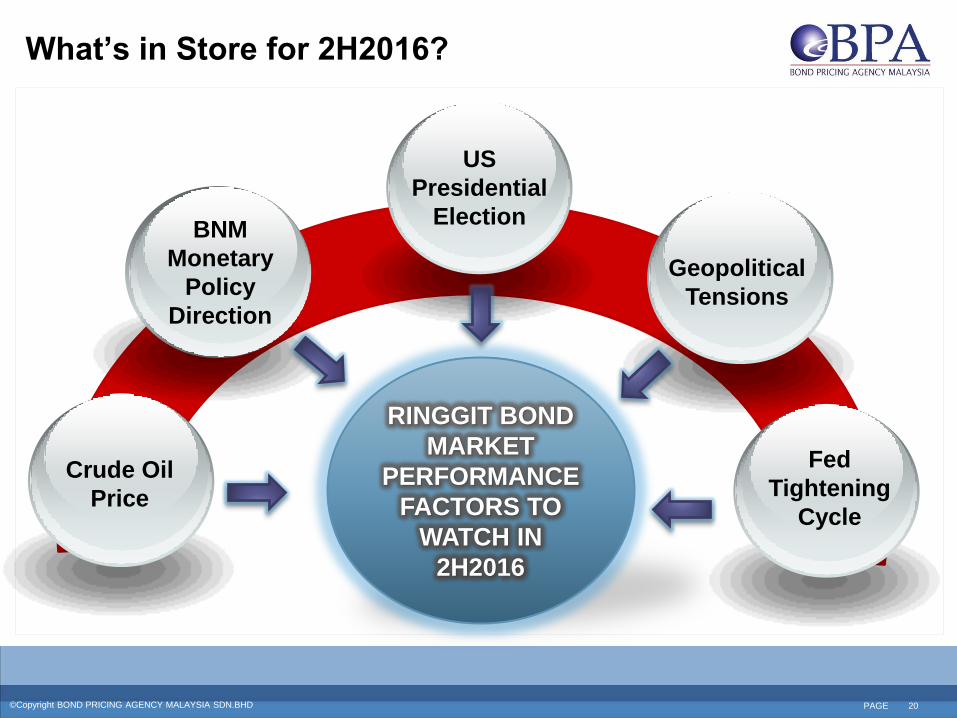

RINGGIT BOND

MARKET

PERFORMANCE

FACTORS TO

WATCH IN

2H2016

What’s in Store for 2H2016?

Fed

Tightening

Cycle

Crude Oil

Price

BNM

Monetary

Policy

Direction

US

Presidential

Election

Geopolitical

Tensions

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 21

Track and Time the Market

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 22

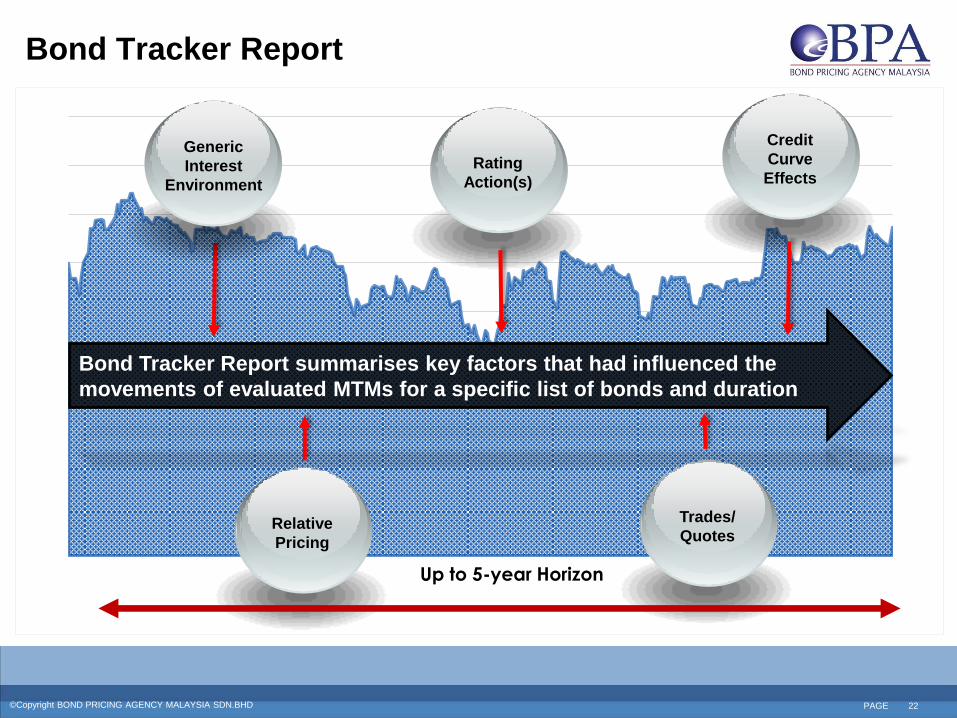

Bond Tracker Report

Bond Tracker Report summarises key factors that had influenced the

movements of evaluated MTMs for a specific list of bonds and duration

Generic

Interest

Environment

Rating

Action(s)

Credit

Curve

Effects

Relative

Pricing

Trades/

Quotes

Up to 5-year Horizon

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD (FORMERLY BONDWEB MALAYSIA SDN BHD). - All rights reserved. ©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD PAGE 23

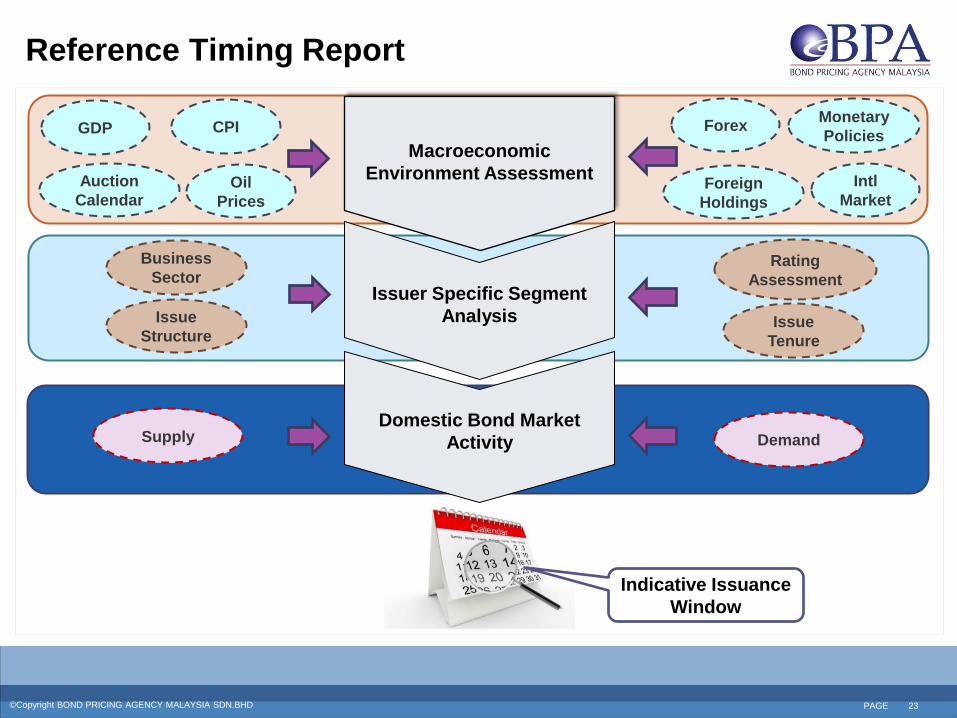

Reference Timing Report

Macroeconomic

Environment Assessment

Domestic Bond Market

Activity

GDP

Oil

Prices

CPI

Foreign

Holdings

Forex Monetary

Policies

Auction

Calendar

Business

Sector Rating

Assessment

Issue

Structure

Supply Demand

Issuer Specific Segment

Analysis

Domestic Bond Market

Activity

Intl

Market

Issue

Tenure

Indicative Issuance

Window

THANK YOU

No 17-8 & 19-8 , The Boulevard, Mid Valley City, Lingkaran Syed Putra, 59200 Kuala Lumpur, Malaysia

Tel: +603 2772 0889 Fax: +603 2772 0808 Email : [email protected]

©Copyright BOND PRICING AGENCY MALAYSIA SDN.BHD - All rights reserved.