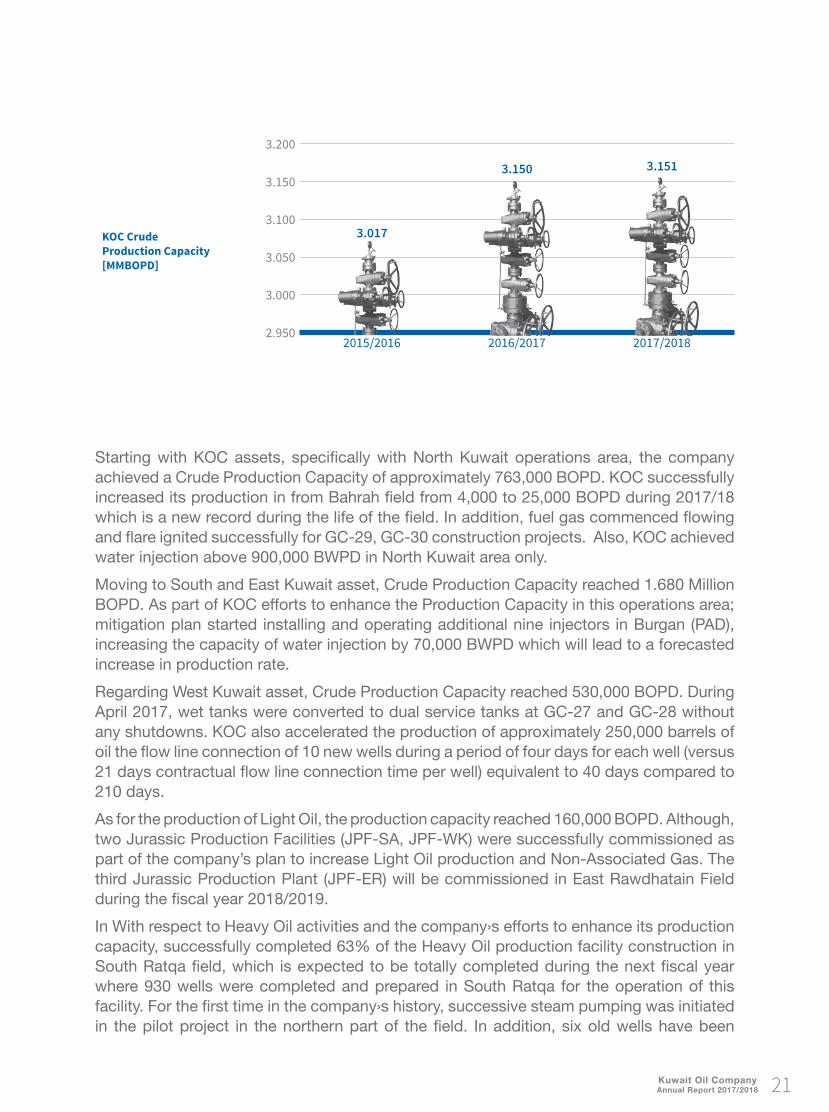

annual report reports/2017-2018 english.pdf · the year-long comprehensive process resulted in,...

TRANSCRIPT

Annual Report2017 - 2018

WWW.KOCKW.COM

His HighnessSheikh Sabah Al-Ahmad Al-Jaber Al-Sabah

Amir of Kuwait

His HighnessSheikh Nawaf Al-Ahmad Al-Jaber Al-Sabah

The Crown Prince of Kuwait

Membersof the Board

Saud Al-ShammariSecretary to the Board

of Directors

Abdullah BarounDeputy Chairman of the Board

Khaled Al-QaoudBoard Member

Hatem Al-AwadhiBoard Member

Wafa Al-ZaabiBoard Member

Mutlaq Al-AzemiBoard Member

Mohammad Al-JazzafChairman of the Board

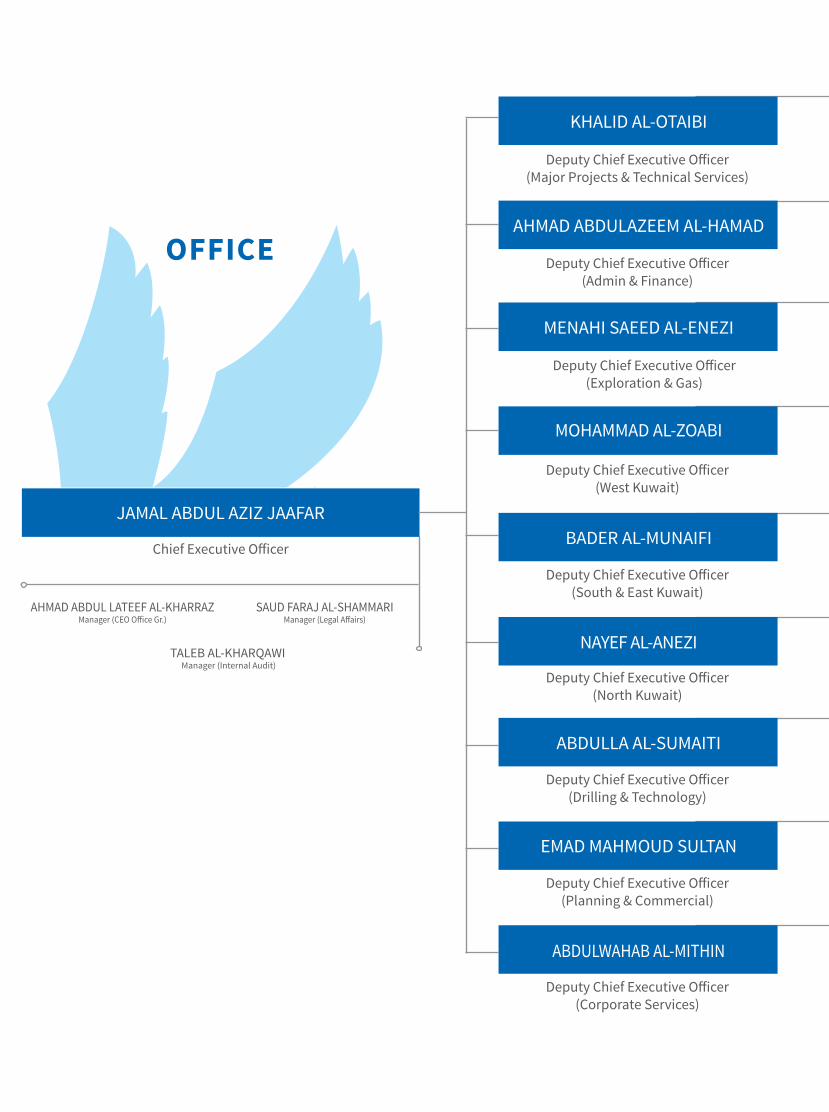

Jamal JaafarChief Executive Officer

Chief Executive Officer

Saud Faraj al-Shammarimanager (legal affairs)

ahmad aBdul latEEF al-Kharrazmanager (CEO Office Gr.)

talEB al-Kharqawi manager (internal audit)

OFFICE

jamal aBdul aziz jaaFar

mOhammad al-zOaBi

mENahi SaEEd al-ENEzi

ahmad aBdulazEEm al-hamad

BadEr al-muNaiFi

aBdulla al-Sumaiti

Emad mahmOud SultaN

aBdulwahaB al-mithiN

NaYEF al-aNEzi

deputy Chief Executive Officer(admin & Finance)

deputy Chief Executive Officer(west Kuwait)

deputy Chief Executive Officer(South & East Kuwait)

deputy Chief Executive Officer(drilling & technology)

deputy Chief Executive Officer(Planning & Commercial)

deputy Chief Executive Officer(Corporate Services)

deputy Chief Executive Officer(North Kuwait)

Khalid al-OtaiBi

deputy Chief Executive Officer(major Projects & technical Services)

deputy Chief Executive Officer(Exploration & Gas)

AREF AL-ABBASSI maNaGEr

(lONdON OFFiCE)

EMAd AL-AwAdH maNaGEr (mEdiCal)

MOHAMMEd ABdUL AZIZ JAAFAR

maNaGEr (CONtraCt maNPOwEr

KuwaitizatiON)

HASSAN ABdULLA AL-KANdARI

maNaGEr (humaN rESOurCES)

NOURI Y. AL-KHATRASH

maNaGEr (ahmadi SErviCES)

MOHAMMEd ABdUL JAwAd AL-BASRYmaNaGEr (Pr & i)

SAMI ALYAQOUT maNaGEr (hSE)

YOUSEF ABdULLAH ABdUL KARIM

maNaGEr (FiNaNCial SYStEmS aNd

CONtrOl)

MUSLEH AL-OTAIBI maNaGEr

(maNaGEmENt SuPPOrt)

AHMAd AL-ZAABI maNaGEr (ahmadi

PrOjECtS)

AdEL R. AL-AZMI maNaGEr (SECuritY)

ALIAL-FAILAKAwI

maNaGEr (FirE)

MANSOURAL-KHAREJI

maNaGEr (SOil rEmEdiatiON)

KHALEd SAAd AL-AJMI

maNaGEr (FiNaNCial aCCOuNtS aNd

SErviCES)

QUSAI NASER AL-AMER maNaGEr (traiNiNG & CarEEr

dEvElOPmENt)

FAROUQ AL-HINdAL maNaGEr SuPPOrt

SErviCES (wK)

FALAH MUTLAQ AL-AZMI maNaGEr OPEratiONS

(wESt Kuwait)

EISA AL-MARAGHI maNaGEr (FiEldS dEvElOPmENt)

ALI SAYEd HASHEM maNaGEr (ExPOrt

OPEratiONS)

BAdER MAHMOUd maNaGEr OPEratiONS SuPPOrt (S&E Kuwait)

MOHAMMEd AL-ABdUL JALIL

maNaGEr (CaPital PrOGram PlaNNiNG)

HAMAd AL-ZA’ABI maNaGEr

FiEldS dEvElOPmENt(NK)

BAdER AL-TELAIHI maNaGEr

OPEratiONS (SOuth Kuwait)

MEQdAd ABdULAZIZ AL-NAQI

maNaGErFiEldS

dEvElOPmENt (S&EK)

FARIdA ALI maNaGEr (rESErvOir

maNaGEmENt)

AdNAN AL-AdwANI maNaGEr

OPEratiONS SuPPOrt (NK)

OMAR ALI SAdEQ maNaGEr

OPEratiONS (EaSt Kuwait)

BAdER AL-ATTAR maNaGEr (PlaNNiNG)

IBRAHIM AL-SAMMAK maNaGEr FiEldS dEv (hEavY Oil)

AMEENA RAJAB maNaGEr SuPPOrt

SErviCES (S&EK)

IBRAHIM ALKHARJI maNaGEr (CONtraCtS)

maNaGEr (PurChaSiNG & matErial maNaGEmENt)

KHALEd AL-AdSANI maNaGEr (COmmErCial

SuPPOrt)

EALIAN AL-ANZI maNaGEr OPEratiONS

(hEavY Oil)

FUAd M. AL-SHAIKH maNaGEr OPEratiONS

(NK)

MOHAMMEd J. AL-OTAIBI

maNaGEr SuPPOrt SErviCES (NK)

YACOUB AHMAd AL-dASHTI

maNaGEr (majOr PrOjECtS iii)

SAUd JUMAHAL-FOUdARI

maNaGEr (dEEP drilliNG)

ABdULLA KHALId HAMAd AL-ZAMAMI maNaGEr (majOr

PrOjECtS i)

BAdER MUTLAQ AL-AZMI

maNaGEr (dEvElOPmENt

drilliNG i)

FAHAd AL-KHARQAwI maNaGEr (majOr

PrOjECtS - ii)

MOHSEN JASSER AL-SHAMMARI

maNaGEr (PrOjECt SuPPOrt SErviCES)

YOUSEF MUSAAdAL-HAMOUd

maNaGEr (PrOCESS SaFEtY maNaGEmENt)

ALI M. AL-SALEH maNaGEr

(dEvElOPmENt drilliNG ii)

ALI AL-NAKEEB maNaGEr (COrPOratE

iNFOrmatiON tEChNOlOGY)

BAdER AL-KHAYYAT maNaGEr (drilliNG

ENGiNEEriNG)

KHALEd SULAIMAN AL-FOZAN maNaGEr

iNduStrial SErviCES

JAMAL AL-HUMOUd

maNaGEr (rESEarCh &

tEChNOlOGY)

AHMAd KH. AL-JASMI maNaGEr

(rESEarCh & dEvElOPmENt)

MUBARAKAL-MUTAIRI

maNaGEr (wEll SurvEillaNCE)

BANdAR AL-MUTAIRI maNaGEr

(tEChNiCal SuPPOrt)

MOHAMMAd dAwwAS AL-AJMI

maNaGEr (ExPlOratiON)

ALI AL-KANdARI maNaGEr PrOduCtiON &

PrOjECtS (GaS)

HAMAd RASHIdAL-ZUwAYER

maNaGEr (GaS OPEratiONS)

BAdER AL-QAOUd maNaGEr OPEratiONS

SuPPOrt (GaS)

MOHAMMAd AL-QENAEI maNaGEr (GaS FiEldS

dEvElOPmENt)

SHAMLAN AL-ROOMI maNaGEr

(ExPOrt SuPPOrt SErviCES & mariNE)

SAMI AL-SAwAGH maNaGEr (mariNE

OPEratiONS)

• Chief Executive Officer’s Message1. Maximize the Strategic Value from Oil2. Realize the Potential of Gas3. Grow Reserves for a Sustainable Future4. Be an Employer of Choice5. Realize Value from Technology6. Strengthen Our Commitment to HSSE7. Strive For Excellence In Performance8. Contribute to Enterprise and State9. KOC’s Aspirations towards meeting its

Strategic Objectives for 2018/19

Table of Contents

12 Kuwait Oil CompanyAnnual Report 2017/2018

During 2017/2018, KOC achieved many accom-plishments and overcame the challenges through concerted efforts among all groups within the company. One of the company’s highlights during the year is the development of 2040 strategy in collaboration with other stakeholders. KOC had a principal role in the development of the Kuwait Oil Sector’s 2040 Strategic Plan, with particular reference to the Domestic Upstream segment. The year-long comprehensive process resulted in, among other things, ambitious crude and non-associated gas production capability targets of 4.250 Million BOPD and 2.0 Billion SCFD respec-tively. Critical elements of the exercise included updating the Strategic Plans, developing the Ini-tiatives to achieve Strategic Directions and the plans to execute eight Core Strategic Initiatives and 11 Enabling Initiatives. The 2040 Strategy affirmed the Company’s Mis-sion - “We optimize the value of Kuwait’s hydro-carbon resources through exploration, develop-ment and production to ensure sustainability” and Vision “To be an upstream leader recognized globally for excellence.” Additionally, a set of Strategic Objectives were articulated based on

KPC’s Strategic Directions, namely:• Strive for World-class Operational Excel-

lence• Optimize Portfolio Management• Achieve sustainable crude oil production ca-

pacity• Achieve sustainable non-associated gas

production capacity• Replace Reserves to sustain production• Facilitate Technology and Capability Trans-

fer • Actively manage stakeholders to satisfy Ku-

wait energy demand efficiently

In order to achieve the ambitious 2040 Strategy goals and objectives, KOC recognizes the es-sential need to progress towards a performance-oriented culture. To this end, the Company has embarked on initiatives and programs aimed at enhancing cost optimization, efficiency, produc-tivity, competitiveness and organizational effec-tiveness. Significantly, it is imperative to note that success of the 2040 Strategy must be built on a foundation of common understanding and shared ownership

Introduction

13Kuwait Oil CompanyAnnual Report 2017/2018

by all the groups within KOC. Consequently, a 2040 Strategy Communications campaign has been initiated to ensure that employees under-stand the challenges faced, plans and initiatives to address them, and our much needed individ-ual contributions. Working together, KOC’s 2040 Strategy goals serve a catalyst for collaborative achievement.

By year-end; the company achieved Crude Pro-duction Capacity of 3.151 Million BOPD, main-taining the level of production capacity. The number of drilling and workover rigs reached 129 rigs; accordingly, 672 new wells of Crude Oil and Non-Associated Gas Production were drilled across Kuwait fields. During March 2018, Non-Associated Gas Production reached its highest level ever about 264 MMSCFD. In addition, the company accomplished a number of discoveries and Heavy Oil production is one of company’s fo-cus where certain number of wells were released within heavy Oil project.

The company has been keen to employ technolo-gy in all aspects of its business in order to reduce

costs and improve the performance of its opera-tions. Also, it was fully focused on recruitment and training, especially Kuwaitis recruitment for both KOC and contractors; 840 employees were recruited of which 633 new Kuwaiti new gradu-ates, and around 3,156 Kuwaitis were accepted to work within KOC signed contracts. Talking about Health, Security, Safety and Environmental; KOC’s efforts and endeavors are focused to re-duce the Lost Time Injury Frequency Rate, which reached 0.016 accidents per 200,000 working hours at year end, and also to reduce volume of oil spilled that reached only 540 barrels.

Moreover, the company participated in numer-ous conferences and exhibitions in order to attain excellence in performance. Likewise, it organized different initiatives and campaigns as part of its “Corporate Social Responsibility”. Also, the com-pany opened the Ahmadi New Hospital to serve its employees and their families. In this report, we describe the company’s performance and achievements within the framework of the 2040 strategic objectives.

Chief Executive Officer’sMessage

14 Kuwait Oil CompanyAnnual Report 2017/2018

As CEO of Kuwait Oil Company, it gives me enormous pride to present you with the KOC Annual Report for 2017/18. In the pages that follow, you will find an extensive review of the activities and achievements KOC has regis-tered over the past year. Before I begin, I would like to take this oppor-tunity to thank every KOC employee who has made the effort over the past year to push our company forward as we strive for operational excellence and safety in all our areas of op-eration. Our company is entirely reliant on our employees and partners, and this human capi-tal is by far our most important resource – and it is one which we continuously endeavor to strengthen.Our activities over the last fiscal year have been defined by close cooperation amongst all KOC Directorates, Groups, and Teams. This is especially true when viewed through the prism of Kuwait’s 2040 Strategic Plan for the Oil Sec-tor, which KOC played a major role in defining. In part, this new strategic vision calls for an in-crease in KOC’s production capabilities in the years ahead while maintaining our adherence to world-class standards as they relate to op-erational excellence, efficiency, and safety. From a technical perspective, KOC’s produc-tion capacity for the past fiscal year currently stands at 3.151 Million BOPD, which trans-lates to maintaining the production level from the previous fiscal year, which stood at 3.150 Million BOPD. However, our crude and non-associated gas production capability figures stand at 4.25 Million BOPD and 2 Billion SCFD respectively. Meanwhile, KOC continues to drill new wells, and over the course of the past year, 672 new wells were drilled across KOC’s areas of operation. Going forward, KOC’s focus in terms of new operations and investment is in the field of heavy oil, the operations of which are predomi-nantly centered in North Kuwait. This Annual Report covers in detail how KOC will continue its efforts to ensure those heavy oil resources will become a significant portion of our total output. In addition to heavy oil production in North Kuwait, KOC is actively planning how our offshore resources can be utilized in the future. In this regard, KOC recently completed an offshore 3D seismic survey of the entirety

of Kuwait Bay, which was one of the largest geophysical projects associated with shallow water in the world. While the exploration and production of Ku-wait’s hydrocarbon resources remains our pri-mary objective, KOC’s activities in fact extend far beyond the oilfield. For example, in the past year, KOC successfully inaugurated the New Ahmadi Hospital for employees working in Ku-wait’s oil sector. The new, state-of-the-art facil-ity will serve our community in the decades to come, and is another addition to KOC’s reper-toire of projects which are aimed at Corporate Social Responsibility efforts and giving back to the community in which we operate. Along-side the new hospital, the brand new Ahmad Al-Jaber Oil & Gas Exhibition was also inaugu-rated. This new facility, in addition to be being an architectural marvel, provides a history of Kuwait’s relationship with oil and will go a long way in inspiring Kuwait’s next generation of oil and gas leaders. Meanwhile, KOC continues to actively acquire and utilize the latest technologies in the world available to us for the benefit and development of our operations. We have also continued to spare no effort in strengthening our commit-ment to HSE-related matters, which play a crit-ical role in our future policies and plans. Issues related to HSE also play a very important role in improving the performance of our employees, who continue to receive prestigious awards and certifications from institutions around the world. This introduction merely provides a brief over-view of the many achievements made by KOC over the last fiscal year, and it is without ques-tion that these achievements would not have been possible without the efforts put forth by our diverse group of dedicated employees and partners. As we move forward and carry KOC into the future, we aim to remain steadfast in our dedication to operational excellence and safety while being a reliable supplier of energy to the world.

Sincerely,Jamal Abdul Aziz JaafarCEOKuwait Oil Company

15Kuwait Oil CompanyAnnual Report 2017/2018

16 Kuwait Oil CompanyAnnual Report 2017/2018

Kuwait Oil CompanyAnnual Report

2017/2018

17Kuwait Oil CompanyAnnual Report 2017/2018

18 Kuwait Oil CompanyAnnual Report 2017/2018

1st Strategic Objective:Maximize the Strategic Value from Oil

19Kuwait Oil CompanyAnnual Report 2017/2018

A- Crude Production Capacity Kuwait Oil Company strives to create the necessary plans and elements leading to increase and enhance Crude Oil Production Capacity. As a result, Crude Production Capacity reached 3.151 MMBOPD at year-end. Efforts are still ongoing to make progress on plans in order to reach targeted Crude Production Capacity for the next year.Two integrated drilling services tenders were successfully launched, the first for exploration of new oil reserves in Kuwait’s Regional waters, and the second for the development of new fields in west Kuwait. The company also signed two huge contracts in the second quarter of the financial year for the “KOC FEED Pipelines for New Refinery Project (NRP) for Al-Zour Refinery” and installation of “New 48 inch” Crude Transit Line from North Kuwait to Central Mixing Manifold (CMM)”.

20 Kuwait Oil CompanyAnnual Report 2017/2018

Starting with KOC assets, specifically with North Kuwait operations area, the company achieved a Crude Production Capacity of approximately 763,000 BOPD. KOC successfully increased its production in from Bahrah field from 4,000 to 25,000 BOPD during 2017/18 which is a new record during the life of the field. In addition, fuel gas commenced flowing and flare ignited successfully for GC-29, GC-30 construction projects. Also, KOC achieved water injection above 900,000 BWPD in North Kuwait area only.Moving to South and East Kuwait asset, Crude Production Capacity reached 1.680 Million BOPD. As part of KOC efforts to enhance the Production Capacity in this operations area; mitigation plan started installing and operating additional nine injectors in Burgan (PAD), increasing the capacity of water injection by 70,000 BWPD which will lead to a forecasted increase in production rate. Regarding West Kuwait asset, Crude Production Capacity reached 530,000 BOPD. During April 2017, wet tanks were converted to dual service tanks at GC-27 and GC-28 without any shutdowns. KOC also accelerated the production of approximately 250,000 barrels of oil the flow line connection of 10 new wells during a period of four days for each well (versus 21 days contractual flow line connection time per well) equivalent to 40 days compared to 210 days.As for the production of Light Oil, the production capacity reached 160,000 BOPD. Although, two Jurassic Production Facilities (JPF-SA, JPF-WK) were successfully commissioned as part of the company’s plan to increase Light Oil production and Non-Associated Gas. The third Jurassic Production Plant (JPF-ER) will be commissioned in East Rawdhatain Field during the fiscal year 2018/2019.In With respect to Heavy Oil activities and the company›s efforts to enhance its production capacity, successfully completed 63% of the Heavy Oil production facility construction in South Ratqa field, which is expected to be totally completed during the next fiscal year where 930 wells were completed and prepared in South Ratqa for the operation of this facility. For the first time in the company›s history, successive steam pumping was initiated in the pilot project in the northern part of the field. In addition, six old wells have been

KOC Crude Production Capacity [MMBOPD]

2015/2016 2016/2017 2017/2018

3.017

3.150

2.950

3.000

3.050

3.100

3.150

3.200

3.151

21Kuwait Oil CompanyAnnual Report 2017/2018

restored and produced since 1980. In order to reduce the cost of heavy oil production, the company succeeded in establishing and expanding the gas pipeline instead of diesel in steam production required for pilot projects. The company also attempted to reduce the cost of processing and analyzing petrophysical data in the Lower Fars reservoir through the use of local resources within KOC. In addition to the above, KOC continues to inspect and analyze oil reservoirs and conduct geological studies and pilot projects, which contribute to increase the Heavy Oil reserves.As for heavy oil from the field of Um Niqa field, the production capacity has reached 18,000.

22 Kuwait Oil CompanyAnnual Report 2017/2018

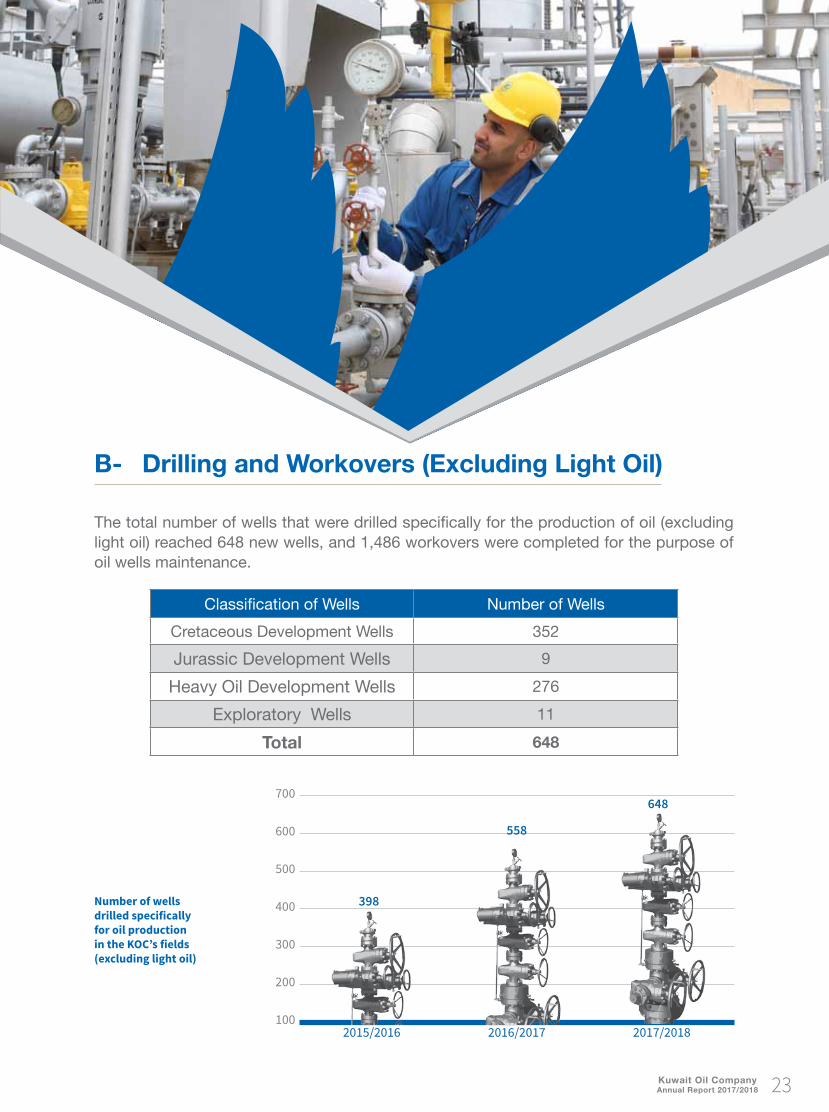

B- Drilling and Workovers (Excluding Light Oil)

The total number of wells that were drilled specifically for the production of oil (excluding light oil) reached 648 new wells, and 1,486 workovers were completed for the purpose of oil wells maintenance.

Number of wells drilled specifically for oil production in the KOC’s fields (excluding light oil)

600

700

Classification of Wells Number of WellsCretaceous Development Wells 352Jurassic Development Wells 9

Heavy Oil Development Wells 276Exploratory Wells 11

Total 648

2015/2016 2016/2017 2017/2018

558

100

200

300

400

500

648

398

23Kuwait Oil CompanyAnnual Report 2017/2018

24 Kuwait Oil CompanyAnnual Report 2017/2018

2nd Strategic Objective:Realize the Potential from Gas

25Kuwait Oil CompanyAnnual Report 2017/2018

KOC is making every effort to achieve its strategic goal by 2040 to reach 2.0 Billion SCFD of Non-Associated Gas. In this regard, the total daily production of Associated Gas and Non-Associated Gas at the end of last year was 1.777 Billion SCFD, while production of Non-Associated Gas reached 215 MMSCFD. For the first time since the start of Non-Associated Gas production, highest production levels of 264 MMSCFD peaked in March 2018.

A- Production Capacity of Associated Gas and Non-Associated Gas

26 Kuwait Oil CompanyAnnual Report 2017/2018

The percentage of Gas Flaring in KOC fields it reached 4.16%. One of the initiative taken by the company to reduce the rate of Gas Flaring is to provide the maximum possible gas feed to the Gas Sweetening Facility continuously and at 60 MMSCFD, in order to optimize the use of gas during AGRP shutdown. Workshops were also held with other K-Companies to enhance communication and resolve all operational problems related to the Kuwait National Petroleum Company (KNPC).Among The company achievements in this regard, is the construction of Gas Booster Station Project (BS-171) of West Kuwait operation area was completed in October 2017, in addition to the delivery of the 12-inch LNG line to Kuwait Oil Tanker Company to transport gas products from Mina Al Ahmadi to Umm Al-Aish gas plant safely to produce gas cylinders.

Number of Deep Wells in KOC’s Fields

B- Drilling and Workover of Jurassic Reservoirs (Non-Associated Gas)

24 deep wells were drilled to reach the amount of Non-Associated Gas targeted and to implement the exploration program of the company, and completed 40 workover to maintain Non-Associated Gas wells.

25

30

2015/2016 2016/2017 2017/2018

15

-

5

10

15

20

24

18

Classification of Wells Number of WellsDeep Developmental Wells (Jurassic) 14Deep Exploratory Wells (Jurassic) 10

Total 24

27Kuwait Oil CompanyAnnual Report 2017/2018

28 Kuwait Oil CompanyAnnual Report 2017/2018

3rd Strategic Objective:Grow Reserves for a Sustainable Production

29Kuwait Oil CompanyAnnual Report 2017/2018

The company has a steady growth in the reserves and Non-Conventional Hydrocarbon resources in order to achieve its 2040 strategic goals and increase Production Capacity. A large quantity of new significant undocumented Hydrocarbon resources volumes were identified in the company; and transfer them to the relevant groups to start doing the necessary to increase the original stock and Hydrocarbon reserves of the company.On the other hand, the first phase of Sabriya chemical injection test (SAMA EOR pilot) was launched which is the first pilot in Carbonate formation in the Middle East for technical and commercial evaluation to maintain production and increase reserves. In addition, successfully completed Single Well Chemical Tracer Test showed a significant reduction in oil saturation remaining in the field of Rawdhatain Zubair by 6%, using the chemical trace of the well, which preserves the production and increase the recovery factor at the end of the life of production.A Corporate Assurance Tool was designed to manage and ensure the health of the petroleum reservoirs in terms of enabling the company to implement the best reservoir management practices and ensure maximum production sustainability. Also, the classification and definitions of Non-Conventional sources of KOC have been approved, helping to unlock the potential of additional resources to meet KOC’s 2040 strategic objectives.A plan for the development of the Umm Niqa - Lower Fars reservoir in polymer mode has been finalized to test whether the enhanced oil recovery will help the company achieve 50,000 BOPD from this reservoir for the growth of reserves for a sustainable future and assessing the effectiveness of the chemical injection technology.Regarding Reserve Replacement Ratio, KOC managed to replace more than 102% (three years rolling average of Reserves Replacement Ratio – Barrel Oil Equivalent (BOE)) through exploration and development, comparing with target of 100%.

A- Reservoir Assessment Studies

30 Kuwait Oil CompanyAnnual Report 2017/2018

B- Seismic Survey Operations

The field operations of the 3D Seismic exploratory survey project in Kuwait Bay and surrounding areas have been successfully completed using advanced and diverse technology utilized in documenting the seismic survey data. KOC honored the supporting parties who made this project a success, which is one of the largest geophysical projects associated with shallow water in the world.

31Kuwait Oil CompanyAnnual Report 2017/2018

32 Kuwait Oil CompanyAnnual Report 2017/2018

C- Exploratory Drilling Activities

During the fiscal year 2018/2017, a number of exploratory drilling operations have been completed, which will contribute to achieving the strategic objectives of the company in terms of adding reserves and production, including:

1. Cretaceous Layer• Discovery of Light oil in Ratawi Limestone reservoir in Mutriba (MU-17), where the first

oil test result was 503 barrels of oil per day with (38.5 API).• Discovery of Light oil in Ratawi Shale and Limestone reservoir in Mutriba (MU-22),

where the first oil test result was 2,627 barrels of oil per day with (27.5 API).• Discovery of Light oil in Ratawi Limestone reservoir in Sabriyah (SA-662), where the

first oil test result was 1,737 barrels of oil per day with (35 API).• Discovery of oil in Lower Fars reservoir in Sabriyah with Heavy Oil extraction.• Discovery in Burgan in Bahrah Field (BH-44), where the first oil test result was 3,342

barrels of oil per day with (34 API).

2. Jurassic Layer• Discovery of Light oil in Middle Marrat reservoir in Sukhaibriyat Prospect (SUK-02),

where the first oil test result was 1,909 barrels of oil per day with (50 API) in addition to 5.877 million SCFD of associated gas.

• Discovery of Light oil in Upper Marrat reservoir in Shaham Prospect (SM-002). Where the first oil test result was 617 barrels of oil per day (48 API) in addition to and 0.3 Million SCFD associated gas.

• Discovery of Light oil in Najmah-Sargelu reservoir in Umm Roos Prospect (UR-03), where the first oil test result was 103 barrels of oil per day (47 API) in addition to and 0.15 Million SCFD associated gas.

33Kuwait Oil CompanyAnnual Report 2017/2018

34 Kuwait Oil CompanyAnnual Report 2017/2018

4th Strategic Objective:Be an Employer of Choice

35Kuwait Oil CompanyAnnual Report 2017/2018

Kuwait Oil Company is striving to enhance the skills and human energies, providing them attractive work environment, and working on reaching highest job satisfaction levels among them. It also seeks to attract Kuwaitis as encouragement to the national employment. Here, we mention the most important achievements in this regard during the fiscal year 2017/2018.KOC exerted enormous efforts to facilitate recruitment of 840 employees, 633 of whom are Kuwaitis graduates. Accordingly, the total number of Kuwait Oil Company’s employees at the end of the fiscal year reached 10,984 employees including the medical and nursing staff. Hence, the percentage of Kuwaitis including the medical and nursing staff reached 81.2% (including Medical and nursing stuff), while it reached 88.5% excluding the medical and nursing staff.In order to create job opportunities for Kuwaitis in the contracts and to encourage the private sector to attract national employment; around 3,156 Kuwaitis were accepted, hence, Kuwaitis in contracts reached approximately 26%.As part of its continuous efforts to provide the best learning opportunities for its employees,

36 Kuwait Oil CompanyAnnual Report 2017/2018

in conjunction with the highest academic institutions, KOC is implementing the following programs:

• “Learning on Demand” program with Harvard School of Business. The program consists of 24 subjects relating to Management Development. To date, 222 fast track employees have participated in this program.

• The drilling worker program in cooperation with the General Authority for Applied Education and Training, which is one of the objectives of the Kuwaiti employment group in the contracts to settle the best practices in the field of drilling and operation of wells where the program continued for the second year in a row to provide about 50 Kuwaiti workers trained and qualified to work in this area Competency required.

The company also continued several initiatives to develop its employees, including 28 employees trained in the Republic of South Korea. In addition, 133 employees received training with International Oil Companies abroad, in order to enhance scientific, technical and research programs needed to improve the company’s production capacities.Also, KOC has organized 3,749 job-related training courses inside and outside the State of Kuwait covering various specializations. The number of training opportunities reached 32,867 in accordance with employees training plan set by the company for the employees’ career development, in addition to 6,602 training opportunities using other developmental tools. Moreover, the company organized training for 746 Kuwaitis in contracts who completed training in various courses in coordination with KPC Petroleum Training Center, to maintain skilled and competent manpower to operate the Company’s operations efficiently.As the company interested in youth and their talents enhancement, the company continued “Future Talents” program for oil sector staff, which aims to develop functional processes and improve youth talents. The program contained 14 innovative projects for number of young employees in KOC, KPC, and other oil companies.

Some of the challenges faced by Kuwait Oil Company during the fiscal year 2017/2018 related to recruitments and training:

• Increasing job awareness of the employees in the contracts and raise the functional efficiency. KOC handled this challenge by organizing enlightenment meetings for all contract workers, by department.

• Qualifying and training Kuwaiti workers covering the needs of the contractor and the technical teams in the company. The company is seeking to increase training programs organized in coordination with the General Authority for Applied Education.

The Kaizen Gallery Walk was also held where employees presented their projects that applied Kaizen Mechanism. This reflects the company’s support and attention of Senior Management to the efforts exerted by the employees and appreciation for their creativity and efforts. The performances demonstrated proved Kaizen’s success in achieving its objectives, particularly through what has been introduced from outputs that contributed to greater efficiency and the elimination of unnecessary spending and time.

37Kuwait Oil CompanyAnnual Report 2017/2018

38 Kuwait Oil CompanyAnnual Report 2017/2018

5th Strategic Objective:Realize Value from Technology

39Kuwait Oil CompanyAnnual Report 2017/2018

The testing and pilots conducted on modern technologies mentioned here or previously provide new means to increase reserves and production. It is worth mentioning that the full-field deployment of this same technology is what will enhance and increase production capacity. Among these technologies, we mention:

KOC, has successfully deployed innovative technology where it consists of two systems, “LPC Pressure Corer” to retrieve large diameter cores and the “PCAL System” for analysis of retained reservoir fluids. Also, for the first time worldwide successful In-Situ Pressurized coring run was conducted on Rig “SP-186” using High Performance Water Based Mud technology has been completed, utilizing recycled Hydro-guard with high salinity to have low solids accumulation, Polymer lumps and well-bore instability. To maximize safety and improve drilling performance, specialized Casing Running Tool was utilized for the first time in Kuwait which it is contributing to speed up running casing which reduced costs by $ 40,000 and reduced the time required for this process. In addition, Surgi Squeeze Acid has been utilized for the first time for a multilateral well “MN-210” where it offers a quick, effective method to help boost production from open hole horizontal by creating multi fractures. In addition, the technology contributed to save the total cost of the well.

40 Kuwait Oil CompanyAnnual Report 2017/2018

Because the company is a pioneer in the use of modern technologies, Rig “SD-16” used a new Bit Technology ‘’Terra Adapt’’ in the two layers of Mutriba and Burgan which was first applied in Kuwait. It contributed to reducing the vibrations resulting from drilling operations with increasing penetration rate of 44%. In addition, savings in drilling hours, which resulted in a reduction of the total cost of drilling operations.Crude oil was also loaded using “Gravity Filling Thereby” technology in oil pipelines from oil storage tanks to shipping vessels, which reduced the use of artificial pumps, especially at peak times, without causing delays for international oil export vessels.In the management and development of fields in KOC’s areas, Field Data Quality and Optimization System (FDQOS) has been developed to provide a solution to smart field operations for field production and optimization. These are some of the key features that are enabled the best decision making for the upper management:

• Modification of crude oil production targets.• Minimizing of gas flaring in certain areas or gathering centers.• Reduction of associated water production resulting from oil production.• Simulation of new or modified gathering center capacities.• Forecast of production gain through a new gathering center plant.

41Kuwait Oil CompanyAnnual Report 2017/2018

42 Kuwait Oil CompanyAnnual Report 2017/2018

6th Strategic Objective:Strengthen Our Commitment to HSSE

43Kuwait Oil CompanyAnnual Report 2017/2018

A- HealthIn the area of health, the new Ahmadi Hospital was inaugurated in April 2017 under the patronage of His Highness the Amir Sheikh Sabah Al-Ahmad Al-Jaber Al-Sabah. KOC announced that Ahmadi Hospital has completed the transfer of patients from several suites in the specialized hospital to the new hospital building in less than three hours.

In spite of the intensive efforts in order to achieve the company’s strategy by 2040, the company strives to achieve maximum levels of Security, Safety, Environmental protection and Health insurance, which are part of its strategy and priorities. Thus, efforts continues in this area in parallel with its efforts to achieve 2040 strategy goals.

44 Kuwait Oil CompanyAnnual Report 2017/2018

B- Safety

C- Security

Regarding Safety, KOC’s efforts and endeavors are focused to reduce the Lost Time Injury Frequency Rate (LTIFR), which reached 0.016 accidents per 200,000 working hours at year-end.In order to strengthen the safety and health rules in the drilling areas of the company, emergency stop safety feature for Auger System was installed to prevent and reduce risks of rig personnel who authorized for maintenance while drilling. On the other hand, seven locations in KOC’s fields were cleared from explosives and contaminated soil.KOC has achieved the Golden Medal Award for Health & Safety and the Golden Award for Fleet Safety for Export & Marine Fields for the year 2017/2018 of the Royal Society for the Prevention of Accidents in the export and marine category.The company regrets the record of two fatalities of contractors for this year 2017/2018 during the months of April and September 2017, one of which was in one of the drilling sites of the company and the other resulted from a road accident. KOC has conducted the necessary investigations to find out the causes and circumstances of accidents, and the necessary to prevent the occurrence of such in the future.

The company Completed an exercise to re-evaluate Ahmadi Township security requirements for the upcoming “Ahmadi Township Security Requirements – Phase II” project. In the framework of Cyber Security in K-Companies, KOC hosted the regular meeting of the Cyber Security Committee of the oil sector, which discussed several key issues related to information security and the committee’s various activities within the K-Companies, such as awareness campaigns and security workshops for oil sector employees.

45Kuwait Oil CompanyAnnual Report 2017/2018

D- Environment

The company continued its efforts towards reducing the quantities of volume of oil spilled within the operation areas; the volume spilled reached 540 barrels at year end. Through September 2017, KOC successfully combated two oil pollution spots, one near Al-Zour and the other near Mina Al-Zour. The General Authority for the Environment and the Kuwait Integrated Petroleum Industries Company praised Kuwait Oil Company’s efforts to contain the crisis.In the framework of the best practices, two emergency training exercises were conducted for the oil leaks in the sea, in the presence of representatives from the General Environment Authority, the Ministry of Electricity and Water, the National Petroleum Company and Saudi Chevron. Work model has been approved by KOC and National Petroleum Company to secure and transport carbon dioxide from national oil refineries to the Minagish field in West Kuwait where this will support the reduction of greenhouse gas emissions at the oil sector level.On the other hand, KOC has organized several environmental campaigns, including “Day of Biodiversity” and “Earth Day” 2017, in the presence of a group of government agencies and external environmental organizations to promote awareness and commitment to preserving the environment. During the campaign, the company planted 300 trees and distributed 350 trees. A panel discussion entitled “Waste Management and Soil Remediation Forum” was organized with the participation of different entities where experiences in the field of environmental technology were shared and discussed.Through the project of excavation and transportation of heavy contaminated soil in North Kuwait, high-pollution liquid oil lakes were cleaned up and contaminated soil was transported from different areas and locations in Umm Al-Aish. Total estimated areas of cleared wet oil lakes are approximately 730 thousand meter squared; in addition to treating nearly 590 thousand cubic meter of contaminated soil; which was severely impacting any development in Umm Al-Aish’s oil field. In the same context, five million square meters of heavy contaminated soil have been cleared with an estimated volume of two million cubic meters that was transported to the newly constructed landfills in North and South of Kuwait. In addition, short, long-term carbon capture, storage strategies and GHG emission reduction techniques have been developed to reduce emissions in Kuwait. Moreover, KOC received the Maritime Standard Award 2017 for Marine Colony under “Environment” category; which was held on October 2017 in Dubai.

46 Kuwait Oil CompanyAnnual Report 2017/2018

47Kuwait Oil CompanyAnnual Report 2017/2018

48 Kuwait Oil CompanyAnnual Report 2017/2018

7th Strategic Objective:Strive For Excellence in Performance

49Kuwait Oil CompanyAnnual Report 2017/2018

50 Kuwait Oil CompanyAnnual Report 2017/2018

KOC is exerting its efforts and always strives for excellence and superiority performance, all these continuous efforts aimed to increase Crude Production Capacity targeting 4.250 Million BOPD by 2040. The most important achievements are:The Center of Excellence recently organized a discussion session on water isolation in oil wells. The session highlighted the latest technologies invented to tackle the issue of water at the bottom of wells. Specialists from Water Handling Teams from Exploration and Production companies along with a number of experts from the Center of Excellence participated in the session.In the same context, a specialized workshop which focused on the importance of the application of petroleum hydro geochemistry which helps understand the evolution of Kuwait’s sedimentary basin and the development of its petroleum systems. The importance of the application of chloride and bromide isotopes in formation waters was discussed as an identification mark in a recent exploratory well for the “Gotnia Formation”. In addition, detailed presentations were presented on the innovative technology and its applications and their use in Kuwait’s crude oil.On the other hand, KOC recently signed a Memorandum of Understanding (MoU) with the Ministry of Public Works, to supply 300,000 BBLs/day of triple-treated water from Kabd Station. The purpose in using the treated-water in the Company’s operations is to improve water quality where the addition of low salinity water to crude oil helps to reduce the concentration of high water salinity associated with oil, as well as accelerate the separation process, and that the agreement will serve the company’s strategy to reach the levels of production target.Moreover, the company participated in numerous conferences, forums and exhibitions in order to attain excellence in performance. Likewise, it organized different events, and presented several technical papers. Here are some of the conferences and exhibitions:

• Oil Flow Measurement Technology Conference at the South East Asia.• Global Corrosion Conference and Exhibition in the United Arab Emirates.• “PetroServ 2017” for petroleum and energy in Tunisia.• “GEO 2018” for Geoscience Conference and Exhibition in Bahrain.• Operational Excellence in Oil and Gas Conference at United Arab Emirates.• Conference of the European Society of Geophysics in France.• Kuwait Third Oil & Gas Exhibition & Conference.

51Kuwait Oil CompanyAnnual Report 2017/2018

52 Kuwait Oil CompanyAnnual Report 2017/2018

8th Strategic Objective:Contribute to Enterprise and State

KOC has launched numerous campaigns and implemented initiatives as part of its corporate social responsibility efforts, some of which including the opening of the Fire Training Center in Burgan, which is the first of its kind in the world in terms of technology and simulation systems and control used in it. This center is a national project primarily because it will receive firefighters from the various sectors of the State and the oil companies associated with the aim of training them on all types of fires and in all circumstances and potential locations. The center is located in the Burgan area, covering an area of 60 thousand square meters. It includes 10 models of facilities similar to those in the company’s operations and includes 75 different training scenarios.

53Kuwait Oil CompanyAnnual Report 2017/2018

54 Kuwait Oil CompanyAnnual Report 2017/2018

KOC’s Aspirations towards meeting its Strategic Objectives for 2018/2019

• Continue building production capacity of crude oil in accordance with the Strategic Directions. KOC also looks forward to continuing the implementation of projects to increase production such as the Gathering Center (GC-31) in the North Kuwait in order to contribute increasing the production capacity of North Kuwait area to 1 MMBOPD. KOC also looking forward to commence the construction work of the Gathering Center (GC-32) in the area of operations in South and East Kuwait to deal with the production of new oil from Burgan Marrat and sour crude oil from Burgan Minagish field.

• Focusing on water treatment, handling and injection operations for reservoirs to increase their production capacity.

• Continue the development of Jurassic Gas fields projects in North Kuwait, where the company aims to achieve a production capacity equivalent to 0.50 billion cubic feet per day by introducing the third Jurassic Production Facility (JPF-ER) in the East Raudhatain field in North Kuwait to produce Light Oil and Non-Associated Gas (40,000 barrels of light oil and 100 million cubic feet of gas per day). The company then aims to raise this production capacity to 1.0 billion cubic feet of Non-Associated Gas by establishing four new Jurassic Production Facilities.

• The development of Heavy Oil reservoirs in North Kuwait by acquiring the required technology, training the company cadres and achieve production capacity equivalent to 60 MBOPD from the field of “Lower Fars reservoir“ through commissioning the Heavy Oil Central Production Facility during 2018/2019. In addition, KOC will continue the development of the field of Umm Niqa “Lower Fars” to increase its production capacity to 25 MBOPD.

• Signing the contracts of the offshore drilling project as part of the onshore and offshore exploration operations to support the company’s production capacity.

• Improve and develop production methods using the best of modern and advanced technology:1. Work on the implementation of pilot and actual Water Flood projects to improve the

company’s expertise in this area.2. To develop the company’s capabilities in the use of EOR technology through the

implementation of pilot projects.• Advancing forward with crude oil segregation projects according to its types.• Continue reducing the Gas Flaring to 1% at the level of Kuwait Oil Company.• Continue modernizing Ahmadi Township.

55Kuwait Oil CompanyAnnual Report 2017/2018

56 Kuwait Oil CompanyAnnual Report 2017/2018

Financial statements and independent auditor’s report

for the year ended 31 March 2018

57Kuwait Oil CompanyAnnual Report 2017/2018

Kuwait Oil Company K.S.C. State of Kuwait Contents Page

Independent auditor’s report 1 - 3 Statement of financial position 4 Statement of profit or loss and other comprehensive income 5 Statement of changes in equity 6 Statement of cash flows 7 Notes to the financial statements 8 - 31

1

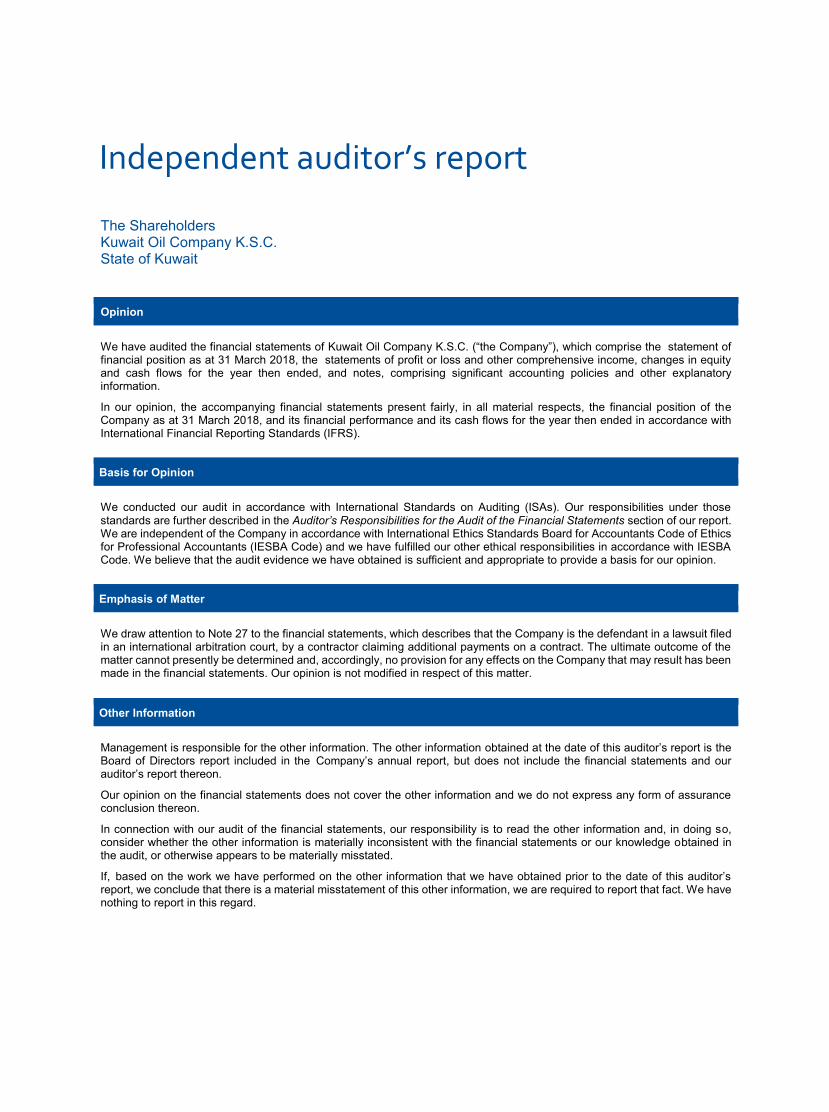

Independent auditor’s report

The Shareholders Kuwait Oil Company K.S.C. State of Kuwait

Opinion

We have audited the financial statements of Kuwait Oil Company K.S.C. (“the Company”), which comprise the statement of financial position as at 31 March 2018, the statements of profit or loss and other comprehensive income, changes in equity and cash flows for the year then ended, and notes, comprising significant accounting policies and other explanatory information.

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Company as at 31 March 2018, and its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards (IFRS).

Basis for Opinion

We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company in accordance with International Ethics Standards Board for Accountants Code of Ethics for Professional Accountants (IESBA Code) and we have fulfilled our other ethical responsibilities in accordance with IESBA Code. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Emphasis of Matter

We draw attention to Note 27 to the financial statements, which describes that the Company is the defendant in a lawsuit filed in an international arbitration court, by a contractor claiming additional payments on a contract. The ultimate outcome of the matter cannot presently be determined and, accordingly, no provision for any effects on the Company that may result has been made in the financial statements. Our opinion is not modified in respect of this matter.

2

Other Information

Management is responsible for the other information. The other information obtained at the date of this auditor’s report is the Board of Directors report included in the Company’s annual report, but does not include the financial statements and our auditor’s report thereon.

Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated.

If, based on the work we have performed on the other information that we have obtained prior to the date of this auditor’s report, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with IFRS, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also: - Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design

and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

- Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate

in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control.

- Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related

disclosures made by management.

3

- Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Company to cease to continue as a going concern.

- Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether

the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Report on Other Legal and Regulatory Requirements

We further report that we have obtained the information and explanations that we required for the purpose of our audit and the financial statements include the information required by the Companies Law No. 1 of 2016, as amended, and its Executive Regulations and the Company’s Memorandum and Articles of Association, as amended. In our opinion, proper books of account have been kept by the Company, an inventory count was carried out in accordance with recognized procedures and the accounting information given in the Board of Directors’ report agrees with the books of accounts of the Company. We have not become aware of any violations of the provisions of the Companies Law No. 1 of 2016, as amended, and its Executive Regulations, or of the Company’s Memorandum and Articles of Association, as amended, during the year ended 31 March 2018 that might have had a material effect on the business of the Company or on its financial position.

Safi A. Al-Mutawa License No 138 “A” of KPMG Safi Al-Mutawa & Partners Member firm of KPMG International

2

Other Information

Management is responsible for the other information. The other information obtained at the date of this auditor’s report is the Board of Directors report included in the Company’s annual report, but does not include the financial statements and our auditor’s report thereon.

Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated.

If, based on the work we have performed on the other information that we have obtained prior to the date of this auditor’s report, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with IFRS, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also: - Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design

and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

- Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate

in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control.

- Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related

disclosures made by management.

3

- Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Company to cease to continue as a going concern.

- Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether

the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Report on Other Legal and Regulatory Requirements

We further report that we have obtained the information and explanations that we required for the purpose of our audit and the financial statements include the information required by the Companies Law No. 1 of 2016, as amended, and its Executive Regulations and the Company’s Memorandum and Articles of Association, as amended. In our opinion, proper books of account have been kept by the Company, an inventory count was carried out in accordance with recognized procedures and the accounting information given in the Board of Directors’ report agrees with the books of accounts of the Company. We have not become aware of any violations of the provisions of the Companies Law No. 1 of 2016, as amended, and its Executive Regulations, or of the Company’s Memorandum and Articles of Association, as amended, during the year ended 31 March 2018 that might have had a material effect on the business of the Company or on its financial position.

Safi A. Al-Mutawa License No 138 “A” of KPMG Safi Al-Mutawa & Partners Member firm of KPMG International

2

Other Information

Management is responsible for the other information. The other information obtained at the date of this auditor’s report is the Board of Directors report included in the Company’s annual report, but does not include the financial statements and our auditor’s report thereon.

Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated.

If, based on the work we have performed on the other information that we have obtained prior to the date of this auditor’s report, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with IFRS, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s financial reporting process.

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also: - Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design

and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

- Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate

in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control.

- Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related

disclosures made by management.

Kuwait Oil Company K.S.C. State of Kuwait Statement of financial position as at 31 March 2018

4

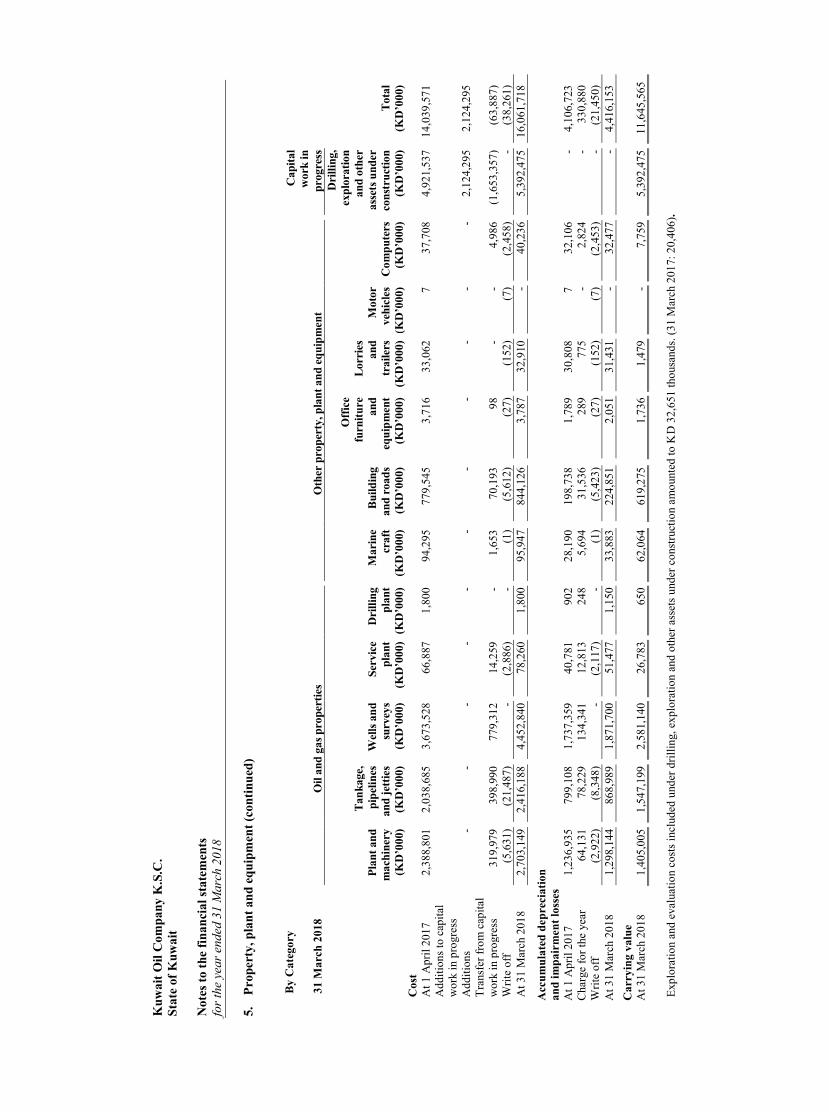

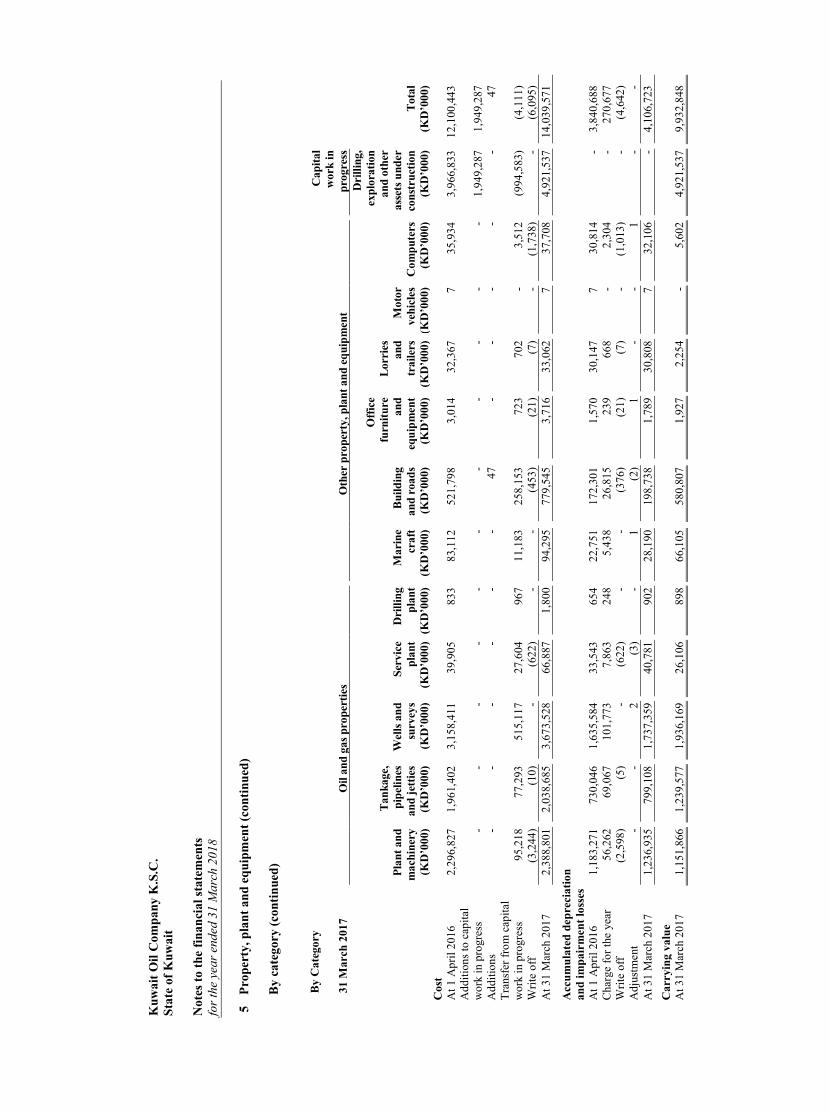

2018 2017 Note KD’000 KD’000 Assets Property, plant and equipment: Crude oil and general purpose 5,366,550 4,356,718 Gas collection and transmission 774,543 534,323 Drilling and exploration 111,441 119,171 Export operations 97 124 Mobile plant 459 975 Capital work in progress 5,392,475 4,921,537 Total property, plant and equipment 5 11,645,565 9,932,848 Intangible assets 6 88,379 29,045 Construction inventories 7 156,586 197,969 Receivable from Parent Company 9 15,094 15,094 Non-current assets 11,905,624 10,174,956 Consumable inventories 7 104,892 111,897 Advances and other receivables 8 560,239 521,846 Amounts due from group companies 15 (b) 93,077 68,282 Cash and cash equivalents 10 7,565 10,713 Current assets 765,773 712,738 Total assets 12,671,397 10,887,694 Equity Share capital – authorized, issued and fully paid shares of KD 1 each 11

30,188

30,188

Shareholder’s current account 11 2,114,791 2,114,791 Statutory reserve 11 15,094 15,094 Total equity 2,160,073 2,160,073 Liabilities Due to Parent Company, net 9 8,713,827 7,129,749 Post employment benefits 12 447,450 347,799 Non-current liabilities 9,161,277 7,477,548 Accounts payable and other liabilities 13 942,563 920,452 Dividend payable 14 407,484 329,621 Current liabilities 1,350,047 1,250,073 Total liabilities 10,511,324 8,727,621 Total equity and liabilities 12,671,397 10,887,694

The accompanying notes form an integral part of these financial statements.

Mohammad Al Jazzaf Chairman

Jamal Abdul Aziz Ja’afar Chief Executive Officer

Kuwait Oil Company K.S.C. State of Kuwait Statement of profit or loss and other comprehensive income for the year ended 31 March 2018

5

2018 2017 Note KD’000 KD’000

Revenue: Revenue (net of royalty, levy and marketing fees) 16 3,142,706 2,666,466 Operating cost (cost of production): Contract services (701,307) (624,968) Employee cost (673,184) (560,760) Material cost (61,926) (72,827) Depreciation, amortization and write off 5&6 (352,244) (273,899) Total operating cost 17 (1,788,661) (1,532,454) Other operating income 18 52,480 27,564 Recoverable costs 19 137,025 113,675 Cost of production (1,599,156) (1,391,215) Deferred cost recognized (44,516) (46,694) Deferred cost 64,009 44,516 Total cost of sales (1,579,663) (1,393,393) Gross profit 1,563,043 1,273,073 General and administrative expenses 20 (108,055) (95,974) Net operating profit 1,454,988 1,177,099 Interest income 353 159 Directors’ remuneration 21 (42) (42) Net profit before contribution to shareholder 1,455,299 1,177,216 Contribution to the shareholder 22 (1,047,815) (847,595) Net profit and total comprehensive income for the year (transferable to Parent Company) 14

407,484

329,621

The accompanying notes form an integral part of these financial statements.

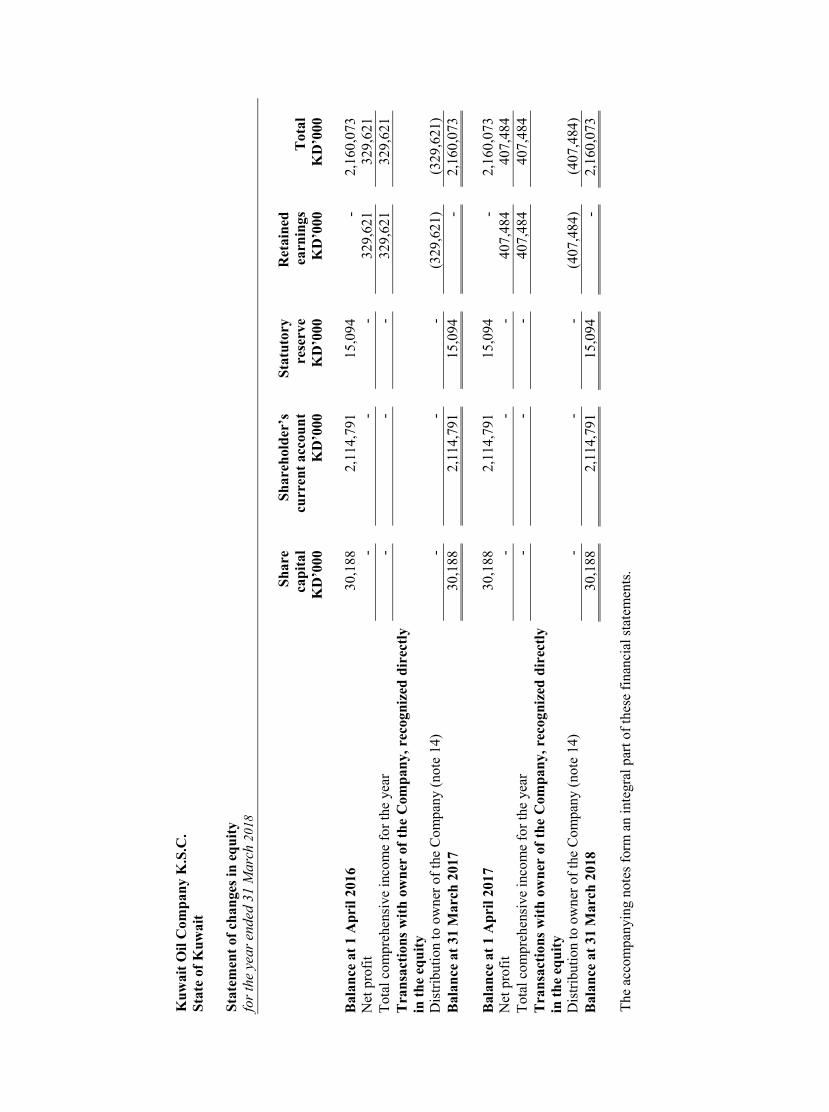

Kuw

ait O

il C

ompa

ny K

.S.C

. St

ate

of K

uwai

t St

atem

ent o

f cha

nges

in e

quity

fo

r the

yea

r end

ed 3

1 M

arch

201

8

6

Sh

are

capi

tal

Sh

areh

olde

r’s

curr

ent a

ccou

nt

St

atut

ory

rese

rve

R

etai

ned

earn

ings

Tot

al

K

D’0

00

K

D’0

00

K

D’0

00

K

D’0

00

K

D’0

00

Bal

ance

at 1

Apr

il 20

16

30,1

88

2,

114,

791

15

,094

-

2,16

0,07

3 N

et p

rofit

-

-

-

329

,621

329

,621

To

tal c

ompr

ehen

sive

inco

me

for t

he y

ear

-

-

-

329

,621

329

,621

T

rans

actio

ns w

ith o

wne

r of

the

Com

pany

, rec

ogni

zed

dire

ctly

in

the

equi

ty

Dis

tribu

tion

to o

wne

r of t

he C

ompa

ny (n

ote 14

)

-

-

-

(

329,

621)

(329

,621

) B

alan

ce a

t 31

Mar

ch 2

017

30,1

88

2,

114,

791

15,0

94

-

2,

160,

073

Bal

ance

at 1

Apr

il 20

17

30,1

88

2,

114,

791

15

,094

-

2,16

0,07

3 N

et p

rofit

-

-

-

407,

484

40

7,48

4 To

tal c

ompr

ehen

sive

inco

me

for t

he y

ear

-

-

-

407,

484

40

7,48

4 T

rans

actio

ns w

ith o

wne

r of

the

Com

pany

, rec

ogni

zed

dire

ctly

in

the

equi

ty

D

istri

butio

n to

ow

ner o

f the

Com

pany

(not

e 14

)

-

-

-

(

407,

484)

(407

,484

) B

alan

ce a

t 31

Mar

ch 2

018

30,1

88

2,

114,

791

15,0

94

-

2,

160,

073

The

acco

mpa

nyin

g no

tes f

orm

an

inte

gral

par

t of t

hese

fina

ncia

l sta

tem

ents

.

Kuwait Oil Company K.S.C. State of Kuwait Statement of cash flows for the year ended 31 March 2018

7

2018 2017 Note KD’000 KD’000 Cash flows from operating activities Net profit 407,484 329,621 Adjustments for: Abortive drilling expenditure 17 8,530 - Provision for obsolete and slow moving inventories 1,012 40 Depreciation, amortization and write off 5&6 352,244 273,899 Contribution to the shareholder 9 1,047,815 847,595 Provision for post employment benefits 12 124,007 51,441 1,941,092 1,502,596 Changes in: - consumable inventories 5,993 (2,288) - advances and other receivables (38,393) (5,388) - receivable from the Parent Company 9 (3,142,706) (2,666,466) - other movements in the Parent Company balances 9 (879) (10,850) - accounts with group companies (24,795) (5,139) - accounts payable and other liabilities 22,111 136,544 Cash used in operations (1,237,577) (1,050,991) Post employment benefits paid 12 (24,356) (48,828) Net used in operating activities (1,261,933) (1,099,819) Cash flows from investing activities Acquisition of property, plant and equipment 5&6 (2,124,295) (1,949,334) Abortive drilling 17 (8,530) - Changes in construction inventories 41,383 (16,531) Net cash used in investing activities (2,091,442) (1,965,865) Cash flows from financing activities Funding from the Parent Company 9 3,350,227 3,066,327 Net cash generated from financing activities 3,350,227 3,066,327 Net change in cash and cash equivalents (3,148) 643 Cash and cash equivalents at beginning of the year 10,713 10,070 Cash and cash equivalents at end of the year 10 7,565 10,713

The accompanying notes form an integral part of these financial statements.

Kuwait Oil Company K.S.C. State of Kuwait Notes to the financial statements for the year ended 31 March 2018

8

1. Reporting entity

Kuwait Oil Company K.S.C. (“the Company”) is a wholly owned subsidiary of Kuwait Petroleum Corporation (“the Parent Company” or “KPC”). The Parent Company is wholly owned by the Government of the State of Kuwait. The Company is engaged in exploration, drilling, production and transportation of hydrocarbon resources within the State of Kuwait. The Company is also engaged in the storage of crude oil and its export. Hydrocarbon resources managed by the Company are the sovereign property of the State of Kuwait. Crude oil is extracted from reserves in Kuwait and, on the instructions of the Parent Company, is exported as blended crude or passed to Kuwait National Petroleum Company K.S.C. (“KNPC”) for further processing or to the Ministry of Electricity and Water for power generation. Gas produced is treated similarly. The sales and marketing of crude oil produced by the Company is undertaken by the Parent Company. The Company owns no oil and gas reserves nor any oil and gas inventory other than those required for operations. The Company also provides marine services to KNPC’s Mina Al-Ahmadi and Mina Abdulla refineries and the oil pier at Mina Al-Shuaiba. KNPC is charged for direct costs relating to these activities. The Company charges group companies for medical and other services provided to their employees. Effective 1 April 2007, the Parent Company changed the reporting structure of the Company to become a profit centre. Prior to 1 April 2007, the Company was reporting to the Parent Company as a cost centre with its costs fully reimbursed by the Parent Company. Under these revised arrangements, the Company’s revenue is determined as the revenue from the sale of crude oil net of certain charges by the Parent Company (see policy on revenue recognition). In addition, 72% of the net profit is payable to the Parent Company as a contribution (Note 22). The Company’s registered office is P.O. Box 9758, Ahmadi 61008, State of Kuwait. These financial statements were approved and authorized for issue by the Board of Directors on 22 April 2018 and are subject to approval of the Shareholder at the annual general assembly.

2. Basis of preparation

a) Statement of compliance The financial statements have been prepared in accordance with the International Financial Reporting Standards (“IFRS”), the requirements of the Companies Law No. 1 of 2016, and its Executive Regulations, and the Company’s Articles of Association and the Ministerial Order No. 18 of 1990.

b) Basis of measurement These financial statements are prepared under the historical cost or amortized cost basis. The financial statements are prepared on a going concern basis. All funding requirements of the Company are met by the Parent Company.

c) Functional and presentation currency

These financial statements are presented in Kuwaiti Dinars rounded to the nearest thousand (KD “000”), which is the Company’s functional and presentation currency.

Kuwait Oil Company K.S.C. State of Kuwait Notes to the financial statements for the year ended 31 March 2018

9

d) Standards and interpretations not yet adopted A number of new standards, amendments to standards and interpretations are effective for annual periods beginning on 1 April 2018 and earlier application is permitted. However, the Company has not early adopted any of these new or amended standards in preparing these financial statements. The significant standards the Company will apply from 1 April 2018 or later are as follows: IFRS 15: Revenue from contracts with customers

The standard, effective for annual periods beginning on or after January 1, 2018, establishes a single and comprehensive framework for determining whether, how much and when revenue is recognized. It replaces the following existing standards and interpretations upon its effective date:

IAS 18 – Revenue, IAS 11 – Construction Contracts, IFRIC 13 – Customer Loyalty Programs, IFRIC 15 – Agreements for the Construction of Real Estate, IFRIC 18 – Transfers of Assets from Customers, and, SIC 31 – Revenue-Barter Transactions Involving Advertising Services

This standard applies to all revenue arising from contracts with customers, unless the contracts are in the scope of other standards. Its requirements also provide a model for the recognition and measurement of gains and losses on disposal of certain non-financial assets, including property, plant, vessels and equipment. The standard will also specify a comprehensive set of disclosure requirements regarding the nature, extent and timing as well as any uncertainty of revenue and corresponding cash flows with customers. Under IFRS 15, an entity recognizes when (on as) a performance obligation is satisfied, i.e. when “control” of the goods as services underlying the particular performance obligation is transferred to customers. The Company is currently assessing the impact of above matter under IFRS 15.

The Company has anticipated that IFRS 15 will be adopted in the Company's financial statements when it becomes mandatory. Based on the current accounting treatment of the Company’s major sources of revenue (Note 3(g), the management does not anticipate that the application of IFRS 15 will have a significant impact on the financial position and/or financial performance of the Company, apart from providing more extensive disclosures on the Company’s revenue transactions. However, as the management is still in the process of assessing the full impact of the application of IFRS 15 on the Company’s financial statements as it is not practicable to provide a reasonable financial estimate of the effect until the management complete the detailed review.

IFRS 9: Financial Instruments

The IASB issued the final version of IFRS 9 Financial Instruments in July 2014, that replaces IAS 39 Financial Instruments: Recognition and Measurement and all previous versions of IFRS 9. IFRS 9 brings together all three aspects of the accounting for financial instruments project: classification and measurement, impairment and hedge accounting. IFRS 9 is effective for annual periods beginning on or after 1 January 2018, with early application permitted. Except for hedge accounting, retrospective application is required but providing comparative information is not compulsory. For hedge accounting, the requirements are generally applied prospectively, with some limited exceptions.

Kuwait Oil Company K.S.C. State of Kuwait Notes to the financial statements for the year ended 31 March 2018

10

The Company will avail of the exemption allowing it not to restate comparative information for prior periods. Differences in the carrying amounts of financial assets and financial liabilities resulting from the adoption of IFRS 9 are required to be recognised in opening retained earnings and reserves as at 1 April 2018.

Company has not performed a detailed impact assessment of IFRS 9 as the Company expects no significant impact on its statement of financial position and equity resulting from transition to IFRS 9.

Classification and measurement

The Company does not expect a significant impact on its financial position or equity on applying the classification and measurement requirements of IFRS 9. It expects to continue measuring loans and receivables and other financial liabilities at amortised cost.

Impairment

IFRS 9 requires the Company to record expected credit losses on all its loans and receivables, either on a 12 month or lifetime basis. The Company will apply simplified approach and record lifetime expected losses on all its receivables.

Hedge Accounting

As at 31 March 2018, the Company does not have any hedge relationships. Hence, the hedging requirements of IFRS 9 will not have a significant impact on Company’s financial statements.

Disclosure

The new standard also introduces expanded disclosure requirements and changes in presentation. These are expected to change the nature and extent of the Company’s disclosures about its financial instruments particularly in the year of the adoption of the new standard.

IFRS 16 – Leases